Market Insights

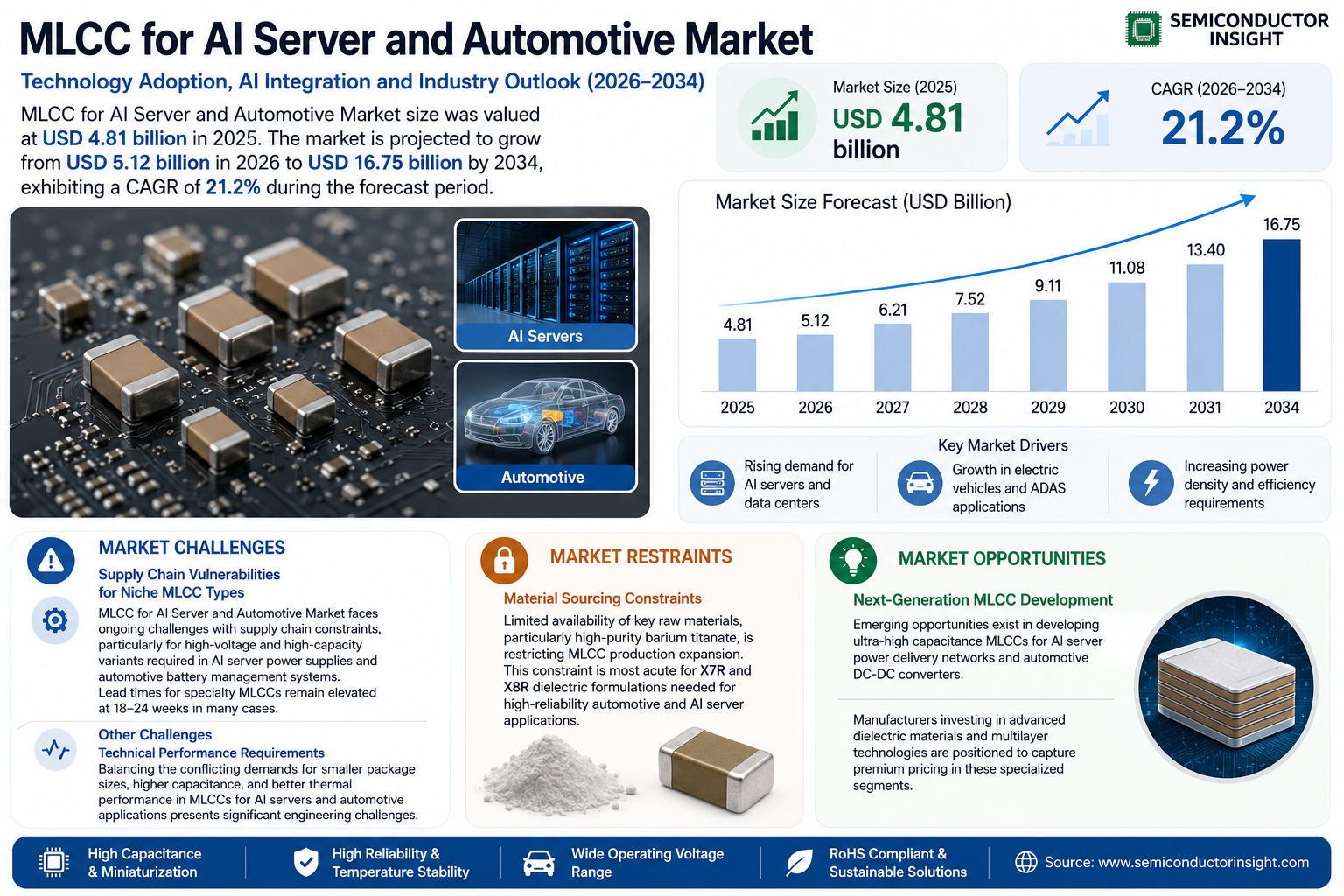

Global MLCC for AI Server and Automotive Market size was valued at USD 4.81 billion in 2025. The market is projected to grow from USD 5.12 billion in 2026 to USD 16.75 billion by 2034, exhibiting a CAGR of 21.2% during the forecast period.

MLCC (Multi-Layer Ceramic Capacitors) are critical components used in AI servers and automotive electronics, characterized by their compact size, high capacitance, and reliability. These capacitors consist of alternating layers of ceramic dielectric and metal electrodes, enabling efficient energy storage and signal stabilization. In AI servers, MLCCs ensure stable power delivery for high-performance computing, while in automotive applications, they support advanced systems like ADAS (Advanced Driver Assistance Systems) and electric vehicle powertrains.

The market growth is driven by increasing demand for AI computing infrastructure and the rapid electrification of vehicles. A single AI server can utilize over 10,000 MLCCs, with requirements for miniaturized, high-capacity components accelerating adoption. Meanwhile, electric vehicles use approximately twice as many MLCCs compared to traditional internal combustion engine vehicles, further boosting demand. Leading manufacturers like Murata and Samsung Electro-Mechanics dominate the high-end segment with specialized products meeting stringent automotive-grade certifications such as AEC-Q200.

MARKET DRIVERS

Growing Demand for High-Capacity MLCCs in AI Servers

The rapid expansion of AI server infrastructure is driving demand for high-capacity MLCCs, which are essential for power management and signal conditioning. With AI workloads requiring up to 30% more MLCCs per server than traditional data centers, manufacturers are scaling production to meet this critical need.

Automotive Electrification Accelerating MLCC Adoption

Electric vehicles utilize 5-8x more MLCCs than conventional automobiles, with advanced driver-assistance systems (ADAS) and onboard computing demanding reliable passive components. The global push toward vehicle electrification is creating sustained demand growth in this sector.

Increased miniaturization requirements in both AI server and automotive applications are forcing manufacturers to develop smaller form-factor MLCCs with higher capacitance values, creating additional revenue opportunities.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Niche MLCC Types

MLCC for AI Server and Automotive Market faces ongoing challenges with supply chain constraints, particularly for high-voltage and high-capacity variants required in AI server power supplies and automotive battery management systems. Lead times for specialty MLCCs remain elevated at 18-24 weeks in many cases.

Other Challenges

Technical Performance Requirements

Balancing the conflicting demands for smaller package sizes, higher capacitance, and better thermal performance in MLCCs for AI servers and automotive applications presents significant engineering challenges.

MARKET RESTRAINTS

Material Sourcing Constraints

Limited availability of key raw materials, particularly high-purity barium titanate, is restricting MLCC production expansion. This constraint is most acute for X7R and X8R dielectric formulations needed for high-reliability automotive and AI server applications.

MARKET OPPORTUNITIES

Next-Generation MLCC Development

Emerging opportunities exist in developing ultra-high capacitance MLCCs for AI server power delivery networks and automotive DC-DC converters. Manufacturers investing in advanced dielectric materials and multilayer technologies are positioned to capture premium pricing in these specialized segments.

MLCC for AI Server and Automotive Market Trends

AI Server Demand Driving MLCC Innovation

The exponential growth in AI computing density has created unprecedented demand for MLCCs in server applications. Modern AI servers now incorporate tens of thousands of MLCCs per unit, with rack configurations requiring hundreds of thousands. This surge has accelerated development of specialized low-voltage, high-capacitance components with reduced equivalent series resistance (ESR) while maintaining miniaturization. MLCC for AI Server and Automotive Market particularly favors ultra-compact 0402-size components that can withstand high-frequency operations.

Other Trends

Automotive Sector Transformation

Vehicle electrification has dramatically increased MLCC requirements, with new energy vehicles demanding twice the MLCC count of traditional combustion engines. Advanced driver assistance systems (ADAS), battery management systems (BMS), and power electronics all require automotive-grade MLCCs with X8R/X9R material specifications for high-temperature stability. The automotive MLCC market prioritizes components meeting AEC-Q200 certification standards.

Competitive Landscape Shifts

Japanese and South Korean manufacturers currently dominate the high-end MLCC for AI Server and Automotive segments, with Murata and Samsung Electro-Mechanics controlling over 80% of server MLCC market share. In automotive applications, Taiyo Yuden, TDK, and Kyocera maintain leadership through advanced dielectric technologies. Domestic manufacturers are making progress in mid-range segments while investing heavily in R&D for high-end market penetration.

The MLCC industry has transitioned from cyclical commodity status to sustained structural growth driven by simultaneous demand from AI infrastructure buildouts and automotive electrification. Future competition will focus on material science breakthroughs in ceramic dielectrics, precision manufacturing capabilities, and strategic supply chain development.

COMPETITIVE LANDSCAPE

Key Industry Players

Japan and South Korea Dominate High-End MLCC Market for AI and Automotive Applications

MLCC for AI Server and Automotive Market for AI servers and automotive applications is dominated by Japanese and South Korean manufacturers, with Murata and Samsung Electro-Mechanics collectively holding over 80% market share in high-end AI server MLCCs. These players have established strong technological barriers, particularly in miniaturized high-capacity solutions (0402/0201 sizes) and automotive-grade X8R/X9R materials. Murata leads in ultra-high capacitance density offerings, while Samsung provides cost-effective mid-range solutions optimized for AI server racks requiring thousands of capacitors per unit.

In the automotive segment, Taiyo Yuden, TDK, and Kyocera (AVX) have secured leadership positions through AEC-Q200 certified products deeply integrated with global automakers. Chinese manufacturers like Yageo and Walsin Technology are rapidly catching up through capacity expansions and automotive qualification breakthroughs, though still primarily serving mid-to-low voltage applications. The market exhibits a clear technology hierarchy, with Japanese firms controlling 90%+ of high-reliability automotive MLCCs above 100V.

List of Key MLCC for AI Server and Automotive Companies Profiled

- Murata Manufacturing

- Samsung Electro-Mechanics (SEMCO)

- TDK Corporation

- Kyocera (AVX)

- Taiyo Yuden

- Walsin Technology

- Yageo Corporation

- Fenghua Advanced Technology

- Holy Stone Enterprise

- Nippon Chemi-Con

- Darfon Electronics

- Eyang Technology

- Vishay Intertechnology

- KEMET Electronics

- Johanson Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

MLCC for Automotive is witnessing accelerated adoption due to the electrification and autonomous driving trends.

|

| By Application |

|

ADAS Systems represent the fastest-growing application segment, driven by autonomous vehicle development.

|

| By End User |

|

Automotive OEMs are driving significant growth through electric vehicle adoption and smart car features.

|

| By Technology Level |

|

High-End MLCCs dominate the AI and automotive sectors due to stringent performance requirements.

|

| By Certification |

|

AEC-Q200 Certified capacitors are becoming industry standard for automotive applications.

|

Regional Analysis: Asia-Pacific MLCC for AI Server and Automotive Market

Japan

Japanese automakers lead in implementing MLCC-heavy architectures for ADAS and vehicle electrification, with established standards for component reliability and longevity in harsh automotive environments.

Major Japanese tech firms are building domestic AI server farms requiring specialized MLCCs, creating vertically integrated demand from local component manufacturers familiar with high-reliability requirements.

Japanese chemical companies develop proprietary dielectric materials enabling MLCCs that meet both automotive-grade temperature ranges and AI server power conditioning needs simultaneously.

Tight collaboration between Japanese MLCC makers and end-users allows for customized specifications in AI server racks and EV powertrains, reducing time-to-market for new technologies.

South Korea

South Korea’s MLCC market benefits from its leadership in consumer electronics transitioning into AI hardware. Major Korean manufacturers are adapting high-volume MLCC production lines for automotive-grade components while maintaining cost advantages. The country’s strong position in memory semiconductors creates natural synergies for AI server MLCC solutions. Korean suppliers are particularly aggressive in miniaturization technologies critical for space-constrained automotive applications.

China

China’s MLCC sector demonstrates rapid technology catch-up in both AI server and automotive applications, buoyed by massive domestic EV production. Chinese manufacturers excel in cost-competitive, high-volume MLCC production with increasing qualifications for automotive use. Government-supported R&D focuses on overcoming technical barriers in high-reliability MLCCs for autonomous driving systems and data center power management.

Taiwan

Taiwan’s MLCC market thrives through its semiconductor ecosystem, with strong positioning in AI server components. Taiwanese firms lead in packaging technologies that optimize MLCC performance for GPU clusters and AI accelerator cards. The island’s foundry relationships enable co-development of MLCC solutions specifically tuned for leading-edge compute architectures.

Southeast Asia

Emerging as an MLCC production hub, Southeast Asia benefits from Japanese and Korean investment in regional facilities. The growing automotive manufacturing base drives demand for locally-sourced MLCCs, while data center expansions create parallel demand for server-grade components. Regional trade agreements facilitate component movement within the Asia-Pacific electronics ecosystem.

Report Scope

This market research report provides a comprehensive analysis of the MLCC for AI Server and Automotive Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of MLCCs in powering advancements across industries such as AI computing, automotive electronics, telecommunications, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, material innovations, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MLCC for AI Server and Automotive Market?

-> MLCC for AI Server and Automotive Market size was valued at USD 4.81 billion in 2025. The market is projected to grow from USD 5.12 billion in 2026 to USD 16.75 billion by 2034, exhibiting a CAGR of 21.2% during the forecast period.

What is the growth rate (CAGR) of MLCC for AI Server and Automotive Market?

-> The market is expected to grow at a CAGR of 21.2% during 2025-2034.

Which key companies operate in MLCC for AI Server and Automotive Market?

-> Key players include Murata, TDK, Samsung (SEMCO), Kyocera (AVX), Taiyo Yuden, Walsin Technology, Darfon, Fenghua Electronics, Yageo, Eyang, Holy Stone, and Nippon Chemi-Con.

What are the key growth drivers?

-> Key growth drivers include exponential growth in AI computing demand, increasing adoption of electric vehicles, advanced driver-assistance systems (ADAS), and rising requirements for high-reliability electronic components.

Which region dominates the market?

-> Asia dominates the market with Japan and South Korea leading in high-end MLCC production, while China is accelerating domestic breakthroughs.

What are the emerging trends?

-> Emerging trends include development of X8R/X9R material specifications, miniaturization of high-capacity capacitors, and increasing integration of MLCCs in autonomous vehicle systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...