MARKET INSIGHTS

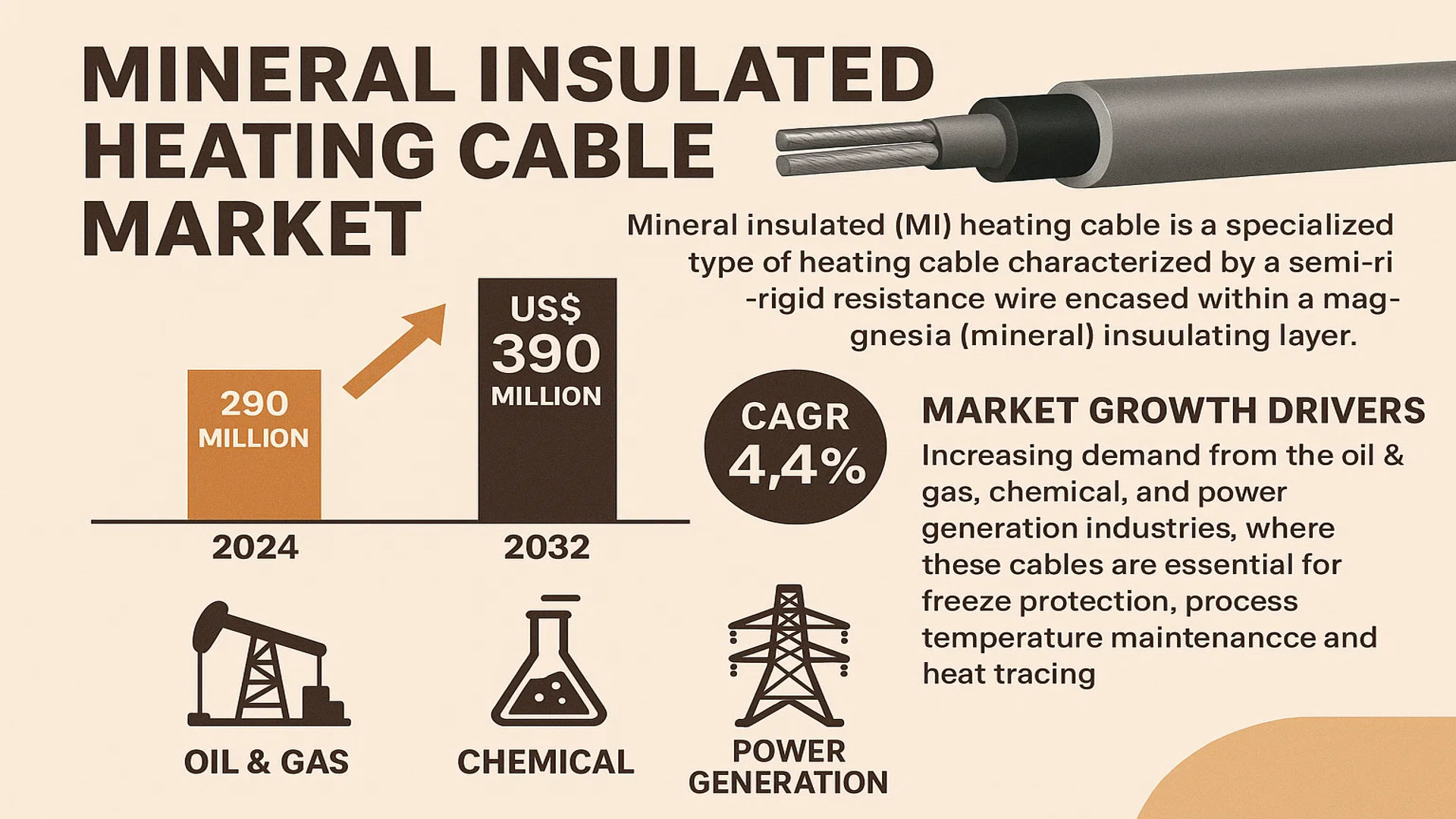

The global Mineral Insulated Heating Cable Market was valued at 290 million in 2024 and is projected to reach US$ 390 million by 2032, at a CAGR of 4.4% during the forecast period.

Mineral insulated (MI) heating cable is a specialized type of heating cable characterized by a semi-rigid resistance wire encased within a magnesia (mineral) insulating layer. These cables are engineered for applications demanding high power output, high exposure temperatures, or extreme resistance to environmental corrosives. They are fundamentally different from polymer-insulated variants, offering superior performance in harsh industrial environments.

The market growth is primarily driven by increasing demand from the oil & gas, chemical, and power generation industries, where these cables are essential for freeze protection, process temperature maintenance, and heat tracing. Furthermore, stringent safety regulations and the need for reliable heating solutions in critical infrastructure are contributing to market expansion. The competitive landscape is consolidated, with the top ten players, including Raychem, Thermon, and Emerson, accounting for approximately 60% of the global market share, indicating a high level of industry concentration.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Oil & Gas and Chemical Processing Industries to Accelerate Market Growth

The global mineral insulated heating cable market is experiencing robust growth driven by the expansion of oil and gas, petrochemical, and chemical processing industries. These sectors require reliable freeze protection and process temperature maintenance in extreme environments, where mineral insulated cables excel due to their high temperature resistance and durability. With the oil and gas industry projected to invest over $500 billion annually in upstream, midstream, and downstream operations, the demand for high-performance heating solutions continues to rise. Mineral insulated cables provide critical operational safety by preventing pipeline freezing, maintaining viscosity in transfer lines, and ensuring process fluid temperatures remain within optimal ranges. Their ability to withstand temperatures up to 600°C and resist corrosive chemicals makes them indispensable in refineries, offshore platforms, and chemical plants where safety and reliability are paramount.

Stringent Safety Regulations and Industrial Automation Trends to Boost Adoption

Increasingly stringent industrial safety regulations worldwide are driving the adoption of mineral insulated heating cables across various sectors. Regulatory bodies have implemented rigorous standards for industrial heating systems, particularly in hazardous areas where explosion-proof and intrinsically safe equipment is mandatory. Mineral insulated cables meet these requirements with their hermetically sealed construction and superior electrical insulation properties. The global focus on industrial safety has intensified following several high-profile industrial accidents, leading to revised safety codes that specifically recommend or require mineral insulated heating solutions in critical applications. Furthermore, the trend toward industrial automation and Industry 4.0 initiatives has created additional demand for reliable heating solutions that can integrate with smart control systems and predictive maintenance platforms, positioning mineral insulated cables as preferred solutions in modern industrial facilities.

Infrastructure Development and Cold Climate Applications to Fuel Market Expansion

Significant infrastructure development in emerging economies and cold climate regions worldwide is creating substantial opportunities for mineral insulated heating cable applications. The construction of new industrial facilities, commercial buildings, and transportation infrastructure in regions experiencing extreme winter conditions requires effective snow melting and freeze protection systems. Mineral insulated heating cables are increasingly specified for roof and gutter de-icing, pipe freeze protection, and surface snow melting in commercial and residential buildings. The global construction industry’s continued growth, particularly in cold climate regions where heating cable usage is essential for operational continuity, supports market expansion. Additionally, infrastructure modernization projects in developed economies often include upgrading heating systems to more efficient and reliable mineral insulated solutions, further driving market growth through replacement and retrofit applications.

MARKET CHALLENGES

High Initial Investment and Installation Complexity to Constrain Market Penetration

The mineral insulated heating cable market faces significant challenges related to high initial costs and complex installation requirements. These cables typically cost 30-50% more than conventional heating cables due to their specialized construction using magnesium oxide insulation and corrosion-resistant sheathing materials. The installation process requires trained professionals with specific expertise in handling rigid cables and proper termination techniques, adding to the overall project costs. This cost premium can be prohibitive for price-sensitive projects or regions with budget constraints, limiting market penetration in developing economies. Additionally, the specialized tools and testing equipment required for proper installation represent additional investment for contractors, creating barriers to widespread adoption despite the long-term benefits of mineral insulated systems.

Other Challenges

Technical Expertise Shortage

The industry faces a growing shortage of qualified installation technicians and engineers with specific expertise in mineral insulated heating systems. This skills gap has become more pronounced as experienced professionals retire and knowledge transfer to new technicians has been insufficient. The complexity of designing, installing, and maintaining these systems requires specialized training that is not widely available, creating project delays and quality concerns that can deter potential users from selecting mineral insulated solutions.

Competition from Alternative Technologies

Increasing competition from self-regulating and constant wattage heating cables presents ongoing challenges for market growth. These alternative technologies have improved their performance characteristics while maintaining lower initial costs and easier installation requirements. While mineral insulated cables offer superior performance in extreme conditions, the perception of adequate performance from less expensive alternatives in moderate applications continues to impact market share, particularly in price-conscious market segments.

MARKET RESTRAINTS

Economic Volatility and Raw Material Price Fluctuations to Limit Market Growth

Economic volatility and fluctuations in raw material prices present significant restraints for the mineral insulated heating cable market. The manufacturing process requires specialized materials including nickel-chromium resistance wire, high-purity magnesium oxide, and corrosion-resistant sheath materials such as copper, stainless steel, or Incoloy. Price volatility in these raw materials, particularly metals which can experience price swings of 20-40% annually, creates manufacturing cost uncertainties that are challenging to pass through to customers. Economic downturns in key end-use industries, particularly oil and gas, often lead to project delays or cancellations, directly impacting demand for heating solutions. The capital-intensive nature of many applications means that during economic uncertainty, companies prioritize essential expenditures, sometimes deferring heating system upgrades or expansions that would utilize mineral insulated cables.

Lengthy Design and Approval Processes to Slow Market Adoption

The comprehensive design, engineering, and approval processes required for mineral insulated heating cable projects create additional restraints on market growth. These systems often require detailed thermal design calculations, hazardous area classifications, and compliance with multiple international standards, resulting in extended project timelines. The approval process for installations in regulated industries such as oil and gas, chemicals, and nuclear facilities can take several months, during which projects may be reevaluated or alternative solutions considered. This extended sales cycle affects manufacturers’ production planning and inventory management, while the complexity of design requirements can deter smaller engineering firms from specifying mineral insulated solutions, opting instead for simpler heating technologies with faster implementation timelines.

Limited Awareness and Perception Issues to Hinder Market Development

Limited awareness about the benefits of mineral insulated heating cables and perception issues regarding their application suitability restrain market development in certain regions and industries. Despite their superior performance characteristics, many specifiers and end-users remain unfamiliar with the technology or perceive it as overly complex for their requirements. This knowledge gap is particularly evident in emerging markets where technical expertise and experience with advanced heating solutions may be limited. Additionally, the perception that mineral insulated cables are only necessary for extreme conditions leads to underutilization in applications where their reliability and longevity would provide significant value. Overcoming these awareness challenges requires substantial educational efforts and demonstration projects, which represent additional investment for manufacturers and slow market penetration rates.

MARKET OPPORTUNITIES

Renewable Energy and Electrification Trends to Create New Application Opportunities

The global transition toward renewable energy and electrification presents significant growth opportunities for mineral insulated heating cable manufacturers. Solar thermal plants, biomass facilities, and hydrogen production infrastructure require high-temperature heating solutions for process maintenance and freeze protection. The emerging hydrogen economy, in particular, creates substantial demand for heating cables capable of maintaining cryogenic temperatures and withstanding hydrogen embrittlement. Mineral insulated cables’ ability to operate efficiently in these challenging environments positions them ideally for renewable energy applications. Additionally, the electrification of industrial processes as part of decarbonization efforts drives demand for electric heating solutions to replace fossil fuel-based systems, creating new market segments where mineral insulated technology offers distinct advantages in safety and efficiency.

Technological Advancements and Smart Integration to Enable Premium Applications

Ongoing technological advancements in mineral insulated heating cable design and integration with smart monitoring systems create opportunities for premium applications and value-added services. Manufacturers are developing cables with improved flexibility, easier termination options, and enhanced monitoring capabilities that address traditional installation challenges. Integration with IoT platforms enables predictive maintenance, energy optimization, and remote monitoring features that justify higher price points through demonstrated operational savings. These technological improvements open opportunities in data centers, pharmaceutical manufacturing, and food processing facilities where precise temperature control and reliability are critical. The ability to provide complete heating solutions with advanced control and monitoring capabilities allows manufacturers to move beyond component supply toward system integration services, creating higher-margin business opportunities.

Emerging Market Infrastructure Development to Drive Long-Term Growth

Infrastructure development in emerging economies, particularly in extreme climate regions, provides long-term growth opportunities for the mineral insulated heating cable market. Countries investing in oil and gas infrastructure, industrial development, and modern building standards represent untapped markets where mineral insulated technology can establish strong positions. The increasing adoption of international standards and safety codes in these regions drives demand for certified heating solutions that meet global requirements. Additionally, urbanization trends in cold climate countries create sustained demand for building heating applications where mineral insulated cables offer superior performance and safety characteristics. Strategic market entry and localization efforts in these developing regions can establish strong market positions that support decades of growth as infrastructure continues to develop and modernize.

MINERAL INSULATED HEATING CABLE MARKET TRENDS

Rising Demand for Energy-Efficient and Safe Industrial Processes to Emerge as a Key Trend

The global push for enhanced operational safety and energy efficiency in industrial settings is significantly driving the adoption of mineral insulated (MI) heating cables. These cables are renowned for their robust construction, featuring a magnesium oxide (MgO) insulation that provides exceptional thermal conductivity, chemical inertness, and fire resistance. This makes them indispensable in high-temperature and harsh environments prevalent in sectors like oil & gas, chemical processing, and power generation. The market is witnessing a compound annual growth rate (CAGR) of 4.4%, propelled by stringent industrial safety regulations and the need to prevent pipe freeze-ups and maintain process temperatures in critical applications. Furthermore, the superior performance of MI cables in extreme conditions, capable of withstanding temperatures exceeding 600°C, positions them as a preferred solution over polymer-insulated alternatives, fostering steady market expansion.

Other Trends

Infrastructure Modernization and Expansion in Emerging Economies

Significant infrastructure development and modernization projects across emerging economies in Asia and the Middle East are creating substantial demand for reliable heating solutions. Major investments in oil refineries, petrochemical plants, and commercial construction necessitate advanced trace heating systems for process maintenance and freeze protection. The industrial application segment, which holds a dominant market share of over 65%, is the primary beneficiary of this trend. Government initiatives aimed at boosting manufacturing output and upgrading aging infrastructure further accelerate the integration of these high-performance heating systems, ensuring consistent market growth in these rapidly developing regions.

Technological Advancements and Product Innovation

Manufacturers are continuously investing in research and development to enhance the performance and application scope of mineral insulated heating cables. Recent innovations focus on improving flexibility for easier installation in complex pipe networks and developing more efficient and durable sheath materials, such as Incoloy, to extend product lifespan in highly corrosive environments. The development of advanced monitoring and control systems that integrate with these cables allows for precise temperature management and predictive maintenance, reducing energy consumption and operational downtime. This focus on innovation is crucial for meeting the evolving demands of end-users for smarter, more reliable, and cost-effective heating solutions, thereby securing a competitive edge in the market.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Technological Innovation and Strategic Expansion to Secure Market Position

The global mineral insulated heating cable market exhibits a semi-consolidated structure, characterized by the presence of a mix of multinational corporations and specialized regional manufacturers. The top ten players collectively commanded approximately 60% of the global market share in 2024, underscoring the significant influence of leading entities. Raychem (a brand of nVent Electric PLC) stands as a dominant force, renowned for its technologically advanced product lines and extensive global distribution network, particularly strong in North America and Europe. Their offerings are critical in demanding industrial applications requiring high exposure temperatures and corrosion resistance.

Thermon Group Holdings, Inc. and Emerson Electric Co. also hold considerable market shares, a position bolstered by their comprehensive suite of thermal solutions and deep-rooted relationships across key end-user industries like oil & gas, chemical processing, and power generation. Their growth is further propelled by continuous investment in research and development, leading to innovations that enhance cable efficiency, durability, and ease of installation.

Furthermore, these established players are actively pursuing growth through strategic acquisitions and geographical expansions into emerging economies, aiming to capitalize on increasing industrialization and infrastructure development. This aggressive expansion strategy is anticipated to further solidify their market positions throughout the forecast period.

Meanwhile, specialized manufacturers such as Bartec GmbH and Chromalox (a division of Spirax-Sarco Engineering plc) are strengthening their foothold by focusing on niche applications and stringent safety standards, particularly in hazardous locations and extreme environments. Their strategy involves significant R&D expenditure and forming strategic partnerships to develop customized solutions, ensuring they remain competitive and relevant in an evolving market landscape.

List of Key Mineral Insulated Heating Cable Companies Profiled

- nVent Electric PLC (Raychem) (U.S.)

- Thermon Group Holdings, Inc. (U.S.)

- Bartec GmbH (Germany)

- Wuhu Jiahong New Material Co., Ltd. (China)

- Anhui Huanrui Heating Manufacturing Co., Ltd. (China)

- Emerson Electric Co. (U.S.)

- Anbang Electric Group Co., Ltd. (China)

- Anhui Huayang Electric Cable Co., Ltd. (China)

- Eltherm GmbH (Germany)

- Chromalox (Spirax-Sarco Engineering plc) (U.S.)

- SST Group (India)

- Isopad Ltd. (U.K.)

- Thanglong Electric (Vietnam)

- BriskHeat (a division of Spirax-Sarco Engineering plc) (U.S.)

Segment Analysis:

By Type

Double Conductor Segment Leads the Market Due to Enhanced Safety and Ease of Installation

The market is segmented based on type into:

- Single Conductor

- Subtypes: Standard, High-Temperature, and others

- Double Conductor

- Subtypes: Parallel, Series, and others

- Others

- Subtypes: Custom configurations and specialty cables

By Application

Industrial Segment Dominates Owing to Extensive Use in Process Temperature Maintenance and Freeze Protection

The market is segmented based on application into:

- Industrial

- Subtypes: Oil & Gas pipelines, chemical processing plants, power generation facilities

- Residential

- Subtypes: Underfloor heating, roof and gutter de-icing, pipe tracing

- Commercial

- Subtypes: Snow melting systems for walkways and driveways, HVAC temperature maintenance

By End User

Oil & Gas Sector is a Key End User Driven by Critical Need for Pipeline Heat Tracing

The market is segmented based on end user into:

- Oil & Gas

- Chemical

- Power & Energy

- Construction

- Others

By Temperature Rating

High-Temperature Cables Hold Significant Share for Demanding Industrial Applications

The market is segmented based on temperature rating into:

- Low Temperature (up to 150°C)

- Medium Temperature (150°C to 400°C)

- High Temperature (above 400°C)

Regional Analysis: Mineral Insulated Heating Cable Market

Asia-Pacific

The Asia-Pacific region dominates the global Mineral Insulated Heating Cable market, accounting for approximately 45% of total consumption by volume. This leadership position is driven by massive industrial expansion, particularly in China and India, where rapid infrastructure development and heavy investments in oil & gas, chemical processing, and power generation sectors create sustained demand. China’s “Made in China 2025” initiative continues to fuel advanced manufacturing, requiring reliable freeze protection and process heating solutions in harsh environments. While cost-competitiveness remains crucial, there is a noticeable shift toward higher-quality, durable MI cables to reduce maintenance costs and enhance operational safety. The region’s harsh climatic conditions in northern areas and growing focus on energy efficiency further accelerate adoption.

North America

North America represents a mature yet steadily growing market, characterized by stringent safety standards and a strong emphasis on reliability and longevity in industrial applications. The region’s well-established oil & gas industry, particularly in the Gulf Coast and Canadian oil sands, relies heavily on MI heating cables for critical pipe tracing and freeze protection in extreme temperatures. Recent investments in LNG export facilities and chemical plant expansions are driving demand. Furthermore, the modernization of aging infrastructure and the need for corrosion-resistant heating solutions in coastal and industrial settings support market growth. The presence of key players like Thermon, Chromalox, and Emerson ensures a competitive landscape focused on innovation and compliance with rigorous U.S. and Canadian regulations.

Europe

Europe’s market is shaped by strict environmental and safety regulations, alongside a strong industrial base requiring high-performance heating solutions. The region’s focus on energy efficiency and reducing carbon footprints aligns with the durable and efficient nature of mineral insulated cables, which offer excellent thermal conductivity and long service life. Germany, the U.K., and the Nordic countries are significant contributors, driven by their advanced chemical, pharmaceutical, and marine industries. The EU’s emphasis on industrial safety and the need for heating solutions in low-temperature climates, particularly in Scandinavia and Russia, bolster demand. However, market growth is tempered by high initial costs and competition from alternative heating technologies in less demanding applications.

Middle East & Africa

This region shows promising growth potential, primarily fueled by extensive oil, gas, and petrochemical projects in GCC countries like Saudi Arabia and the UAE. The extreme ambient temperatures and corrosive desert environments necessitate robust heating solutions for pipeline maintenance, tank heating, and process sustainment. Large-scale projects, such as Saudi Arabia’s Vision 2030 and ongoing investments in refining capacity, are key drivers. However, the market’s development is uneven, with slower adoption in African nations due to limited industrial infrastructure and investment constraints. Nonetheless, the critical need for reliable heating in oil & gas applications ensures steady demand, with international suppliers actively expanding their presence.

South America

South America’s market is emerging, driven mainly by the oil & gas sector in Brazil and Argentina. Offshore drilling activities and pipeline projects in remote and corrosive environments create opportunities for MI heating cable applications. However, economic volatility and political uncertainties often delay large-scale investments, impacting market growth. While countries like Chile and Colombia are gradually investing in industrial and energy infrastructure, the region’s overall adoption rate remains moderate. Price sensitivity and competition from lower-cost alternatives sometimes hinder the widespread use of premium MI cables, though their superior performance in critical applications continues to attract interest.

Report Scope

This market research report provides a comprehensive analysis of the global Mineral Insulated Heating Cable market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of IoT, advancements in heating cable design, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mineral Insulated Heating Cable Market?

-> Mineral Insulated Heating Cable Market was valued at 290 million in 2024 and is projected to reach US$ 390 million by 2032, at a CAGR of 4.4% during the forecast period.

Which key companies operate in Global Mineral Insulated Heating Cable Market?

-> Key players include Raychem, Thermon, Bartec, Emerson, Chromalox, Eltherm, SST, Anhui Huanrui, Wuhu Jiahong, Anbang, and Anhui Huayang, among others.

What are the key growth drivers?

-> Key growth drivers include demand from oil & gas and chemical processing industries, stringent safety regulations, and expansion of commercial and residential infrastructure.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America and Europe remain dominant markets.

What are the emerging trends?

-> Emerging trends include development of energy-efficient cables, integration with smart building systems, and increased use in freeze protection applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...