MARKET INSIGHTS

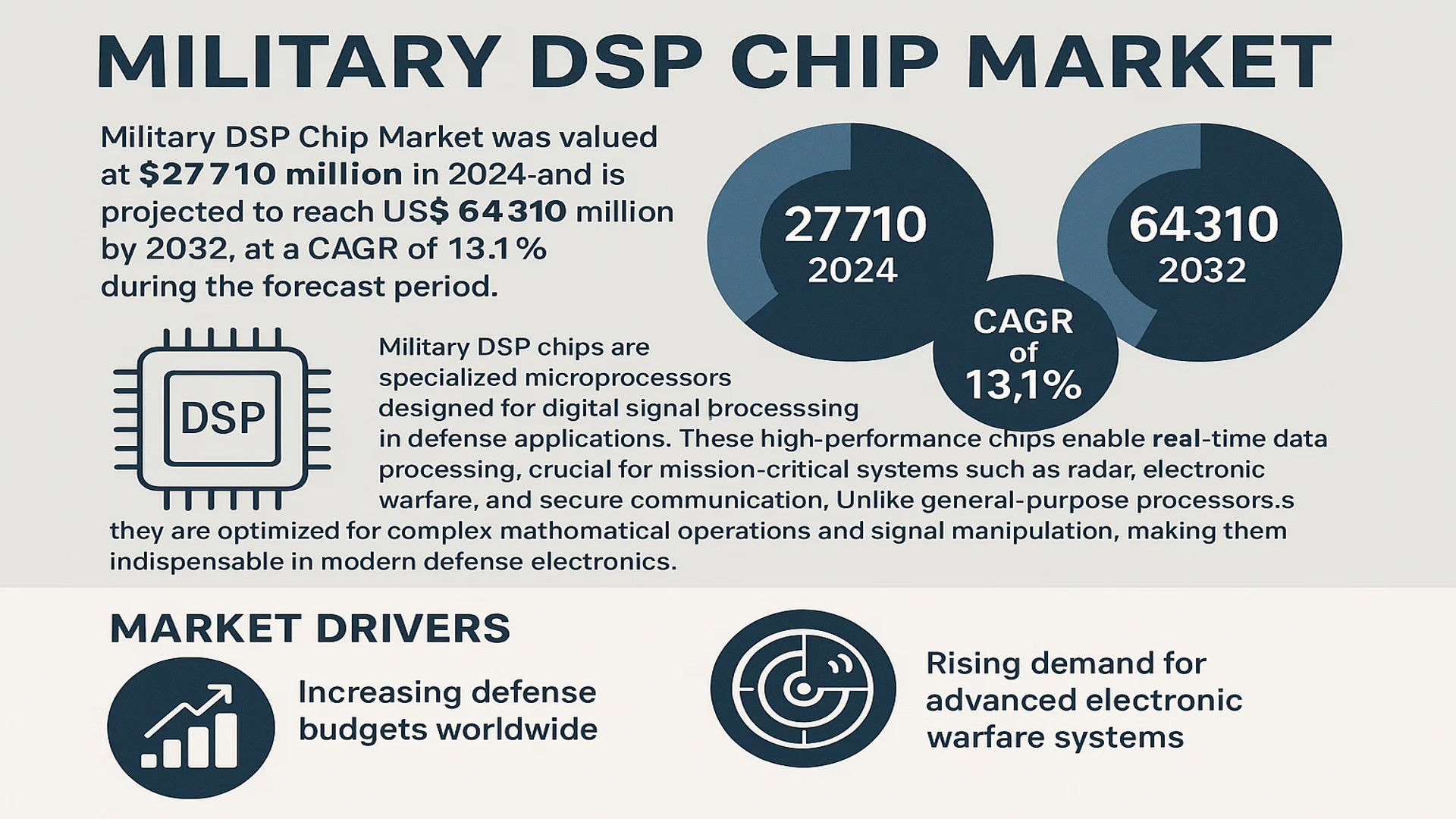

The global Military DSP Chip Market was valued at 27710 million in 2024 and is projected to reach US$ 64310 million by 2032, at a CAGR of 13.1% during the forecast period.

Military DSP chips are specialized microprocessors designed for digital signal processing in defense applications. These high-performance chips enable real-time data processing, crucial for mission-critical systems such as radar, electronic warfare, and secure communication. Unlike general-purpose processors, they are optimized for complex mathematical operations and signal manipulation, making them indispensable in modern defense electronics.

The market growth is driven by increasing defense budgets worldwide and the rising demand for advanced electronic warfare systems. Furthermore, technological advancements in artificial intelligence (AI) and machine learning (ML) are pushing the need for more powerful DSP chips capable of handling complex algorithms. Key players like Texas Instruments (TI), Analog Devices (ADI), and China Electronics Technology Group Corporation are investing heavily in R&D to develop next-generation military-grade DSP solutions with enhanced security and processing capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Military Modernization Programs to Drive DSP Chip Adoption

Global defense spending has reached record levels, with nations accelerating military modernization initiatives to enhance their technological edge. Digital Signal Processing (DSP) chips are becoming critical components in advanced radar systems, electronic warfare platforms, and secure communication networks. The U.S. has allocated over $842 billion for defense in 2024, with significant portions dedicated to upgrading legacy systems with cutting-edge DSP capabilities. These chips enable real-time signal processing for threat detection, encrypted communications, and precision targeting – capabilities that are increasingly vital in modern asymmetric warfare scenarios.

Growing Demand for AI-Enabled Defense Systems to Accelerate Market Growth

The integration of artificial intelligence with military systems is creating unprecedented demand for high-performance DSP chips. Modern AI-powered surveillance, autonomous vehicles, and cognitive electronic warfare systems require DSP processors capable of handling complex algorithms with low latency. Military-grade DSP chips now incorporate specialized AI cores that can process vast amounts of sensor data in real-time while consuming minimal power. This technological shift is evident in programs like the U.S. Army’s Project Convergence, which aims to connect sensors, shooters, and decision-makers through AI-enhanced networks.

Furthermore, the development of software-defined radios and spectrum-agile communication systems is driving the need for reprogrammable DSP architectures. These flexible solutions allow militaries to adapt to evolving electronic warfare threats without requiring hardware replacements.

➤ For instance, the F-35 fighter jet’s advanced electronic warfare system relies heavily on multi-core DSP processors capable of simultaneously processing radar, communications, and threat detection signals.

MARKET RESTRAINTS

Stringent Export Controls and Supply Chain Vulnerabilities to Limit Market Expansion

The military DSP chip market faces significant constraints due to strict international export regulations, particularly for advanced semiconductor technologies. Many nations have implemented comprehensive controls on the transfer of high-performance DSP chips, creating artificial market barriers. The CHIPS and Science Act in the United States has further tightened restrictions on technology transfers to certain geopolitical regions. These controls not only limit market access but also complicate supply chains for global defense contractors operating across multiple jurisdictions.

Additionally, the concentration of semiconductor manufacturing capacity in specific geographic regions creates supply chain vulnerabilities. Recent global chip shortages have demonstrated how production bottlenecks can impact defense procurement timelines, with some military programs experiencing delays of 12-18 months for critical DSP components. The sensitive nature of military-grade chips means that manufacturers must maintain separate production lines and qualify suppliers through rigorous security vetting processes.

MARKET CHALLENGES

Technical Complexities in Developing Radiation-Hardened DSP Solutions

Designing DSP chips for military applications presents unique engineering challenges, particularly for space and high-altitude platforms. Radiation-hardened components must withstand extreme environmental conditions while maintaining computational performance. The development cycle for such specialized chips often exceeds 24-36 months, with qualification testing alone taking up to 12 months. Additionally, military DSP chips must meet rigorous reliability standards, typically requiring Mean Time Between Failures (MTBF) measurements exceeding 100,000 hours.

Other Challenges

Thermal Management Issues

High-performance DSP chips generate significant heat, requiring sophisticated cooling solutions in space-constrained military platforms. This thermal challenge has led to increased development of 3D packaging techniques and liquid cooling systems specifically for defense applications.

Cybersecurity Vulnerabilities

Military DSP chips face growing threats from sophisticated cyber attacks targeting firmware and hardware vulnerabilities. Ensuring secure boot mechanisms and tamper-resistant designs adds complexity and cost to the development process.

MARKET OPPORTUNITIES

Advancements in Semiconductor Manufacturing to Enable Next-Generation Military DSP Solutions

The transition to advanced semiconductor nodes, particularly 7nm and below, offers significant opportunities for military DSP chip performance improvements. Smaller process nodes enable higher transistor density, lower power consumption, and enhanced computational capabilities – critical factors for next-generation military systems. Manufacturers are leveraging these advancements to produce DSP chips that deliver up to 40% better performance per watt compared to previous generations.

Additionally, the development of heterogeneous computing architectures combining DSP cores with AI accelerators and FPGA fabrics creates new possibilities for adaptive signal processing in military applications. These innovations are particularly valuable for software-defined radio systems and cognitive electronic warfare platforms that must adapt to rapidly changing threat environments.

Geopolitical dynamics are also driving increased investment in sovereign semiconductor capabilities, with several nations establishing dedicated defense foundries. This trend is expected to create new market opportunities for specialized military DSP chip manufacturers capable of meeting stringent national security requirements.

MILITARY DSP CHIP MARKET TRENDS

Increasing Demand for High-Performance Signal Processing in Defense Systems

The global military DSP chip market is experiencing rapid growth due to escalating defense budgets and the need for advanced signal processing capabilities in modern warfare systems. Valued at $27.71 billion in 2024, the market is projected to reach $64.31 billion by 2032, reflecting a 13.1% CAGR. This surge is primarily driven by expanding applications in radar systems, secure communications, and electronic warfare, where DSP chips enable real-time processing of complex signals. Furthermore, the integration of AI-enhanced DSP architectures allows military systems to process vast amounts of sensor data with unprecedented speed and accuracy, directly supporting autonomous defense platforms and battlefield decision-making systems.

Other Trends

Shift Towards Multi-Core DSP Architectures

Military applications increasingly favor multi-core DSP chips over traditional single-core solutions because of their superior parallel processing capabilities. Modern defense systems require simultaneous handling of multiple signal processing tasks, such as radar imaging, encrypted communications, and threat detection, which multi-core chips can manage more efficiently. Recent advancements have seen DSP architectures incorporating 4-16 cores with specialized accelerators for matrix operations, significantly improving performance in complex computational tasks like synthetic aperture radar (SAR) processing and frequency-hopping spread spectrum analysis.

Growing Need for Radiation-Hardened DSP Solutions

The expansion of space-based defense systems has dramatically increased demand for radiation-hardened DSP chips capable of withstanding harsh environments. These specialized components now account for 18-22% of total military DSP shipments, particularly for satellites and high-altitude surveillance platforms. Manufacturers are developing chips with error-correcting memory and latch-up protection circuits that maintain functionality even in extreme radiation conditions. While terrestrial systems still dominate volume sales, the space segment is growing nearly 45% faster than other military applications, reflecting strategic investments in orbital defense infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Defense Electronics Giants Accelerate Innovations to Secure Market Leadership

The military DSP chip market exhibits a concentrated competitive landscape with Texas Instruments (TI) and Analog Devices Inc. (ADI) collectively holding over 45% revenue share. These industry titans have dominated the sector through their defense-grade chip designs that meet stringent MIL-SPEC standards for reliability in harsh environments.

While TI maintains technological leadership with its TMS320 series processors – widely adopted in radar and secure communication systems – ADI counters with breakthrough analog-to-digital conversion technologies. Recent advancements include ADI’s 16-bit converters achieving 500 MSPS sampling rates, critical for electronic warfare systems.

The market also sees strong participation from China Electronics Technology Group Corporation (CETC), which has rapidly expanded its footprint following Beijing’s military modernization initiatives. CETC’s indigenous DSP solutions now power approximately 28% of China’s defense electronics, reducing reliance on Western suppliers.

Mid-tier competitors like Motorola Solutions (through its government segment) and Lucent Technologies are focusing on software-defined radio applications. However, their market positions face pressure from the emergence of multi-core DSP architectures that enable parallel processing for AI-powered defense systems.

Notably, the competitive dynamic is shifting as commercial chipmakers adapt consumer technologies for defense applications. Zilog’s recent partnership with Lockheed Martin to repurpose IoT processors for unmanned systems exemplifies this trend, potentially disrupting traditional military suppliers.

List of Key Military DSP Chip Manufacturers

- Texas Instruments (U.S.)

- Analog Devices Inc. (U.S.)

- Motorola Solutions (U.S.)

- Lucent Technologies (U.S.)

- Zilog (U.S.)

- China Electronics Technology Group Corporation (China)

Segment Analysis:

By Type

Multi-core DSP Segment Leads Due to High Performance in Complex Military Applications

The military DSP chip market is segmented based on type into:

- Single Core DSP

- Subtypes: Fixed-point, Floating-point, and others

- Multi-core DSP

By Application

Radar Systems Segment Dominates Due to Critical Defense Applications

The market is segmented based on application into:

- Radar Systems

- Communication Systems

- GPS and Navigation

- Electronic Warfare

- Others

By End-User

Defense Sector Captures Majority Share Due to Strategic Military Modernization Initiatives

The market is segmented based on end-user into:

- Defense Sector

- Homeland Security

- Aerospace

By Technology

FPGA-based DSP Solutions Gain Traction in Military Applications

The market is segmented based on technology into:

- ASIC-based DSP

- FPGA-based DSP

- SoC-based DSP

Regional Analysis: Military DSP Chip Market

North America

North America dominates the Military DSP Chip market, accounting for approximately 35% of global revenue in 2024, driven by substantial defense spending and advanced technological adoption. The U.S. Department of Defense has prioritized next-generation signal processing technologies, allocating $842 billion for defense in 2024, with significant portions dedicated to radar and communication system modernization. Key players like Texas Instruments and Analog Devices lead innovation in multi-core DSP solutions for military applications. However, strict export controls and ITAR regulations create barriers for international collaboration, potentially slowing some segments of market growth.

Europe

Europe maintains a strong position in the Military DSP Chip sector, with NATO members collectively investing €380 billion in defense modernization programs. The region shows particular strength in radar processing applications, with countries like Germany and France developing proprietary DSP architectures for sovereign security systems. While the EU’s defense industrial strategy promotes local semiconductor production, reliance on U.S. IP cores for certain high-performance DSPs creates some supply chain vulnerabilities. Recent collaborations between academia and defense contractors aim to develop specialized DSP solutions for encrypted battlefield communications.

Asia-Pacific

The fastest-growing regional market, Asia-Pacific is projected to expand at a CAGR exceeding 15% through 2032, led by China’s military modernization initiatives. The region demonstrates strong demand for both indigenous and imported DSP solutions, with applications spanning electronic warfare, missile guidance, and satellite communication systems. India’s recent focus on ‘Atmanirbhar Bharat’ (self-reliant India) in defense has spurred local DSP chip development, though technical gaps remain in high-frequency processing capabilities. Meanwhile, Japan and South Korea continue to advance their DSP architectures through partnerships with global semiconductor leaders.

Middle East & Africa

Military DSP adoption in this region centers on surveillance and border security applications, with Gulf Cooperation Council nations leading procurement. Countries like Saudi Arabia and the UAE are investing in integrated air defense systems requiring advanced DSP processing capabilities. While the market currently depends largely on imports, localized assembly and testing facilities are emerging to support regional defense needs. Budget constraints in African nations limit widespread adoption, though selective investments in communication infrastructure create niche opportunities for DSP suppliers.

South America

The region shows moderate growth potential in Military DSP applications, primarily for coastal surveillance and internal security operations. Brazil’s armed forces modernization program includes DSP-equipped radar systems, while Argentina focuses on upgrading its military communication networks. Economic instability and fluctuating defense budgets pose challenges for long-term procurement planning. However, joint development programs among South American countries could stimulate regional demand for specialized DSP solutions in the coming decade, particularly for intelligence gathering operations.

Report Scope

This market research report provides a comprehensive analysis of the Global Military DSP Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Military DSP Chip market was valued at USD 27,710 million in 2024 and is projected to reach USD 64,310 million by 2032, growing at a CAGR of 13.1% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Single Core DSP, Multi-core DSP) and application (Radar, Communication Systems, GPS System, Others) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. North America and Asia-Pacific are key regions driving market growth.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include TI, ADI, Motorola, Lucent, Zilog, and China Electronics Technology Group Corporation.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards in military DSP applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increased defense spending, modernization of military systems) along with challenges (supply chain constraints, export restrictions).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Military DSP Chip Market?

-> Military DSP Chip Market was valued at 27710 million in 2024 and is projected to reach US$ 64310 million by 2032, at a CAGR of 13.1% during the forecast period.

Which key companies operate in Global Military DSP Chip Market?

-> Key players include TI, ADI, Motorola, Lucent, Zilog, and China Electronics Technology Group Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include increased defense budgets worldwide, modernization of military communication systems, and rising demand for advanced radar and electronic warfare systems.

Which region dominates the market?

-> North America currently leads the market due to significant defense spending, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include development of AI-powered DSP chips, integration of multi-core processing capabilities, and increased focus on cybersecurity in military applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...