MARKET INSIGHTS

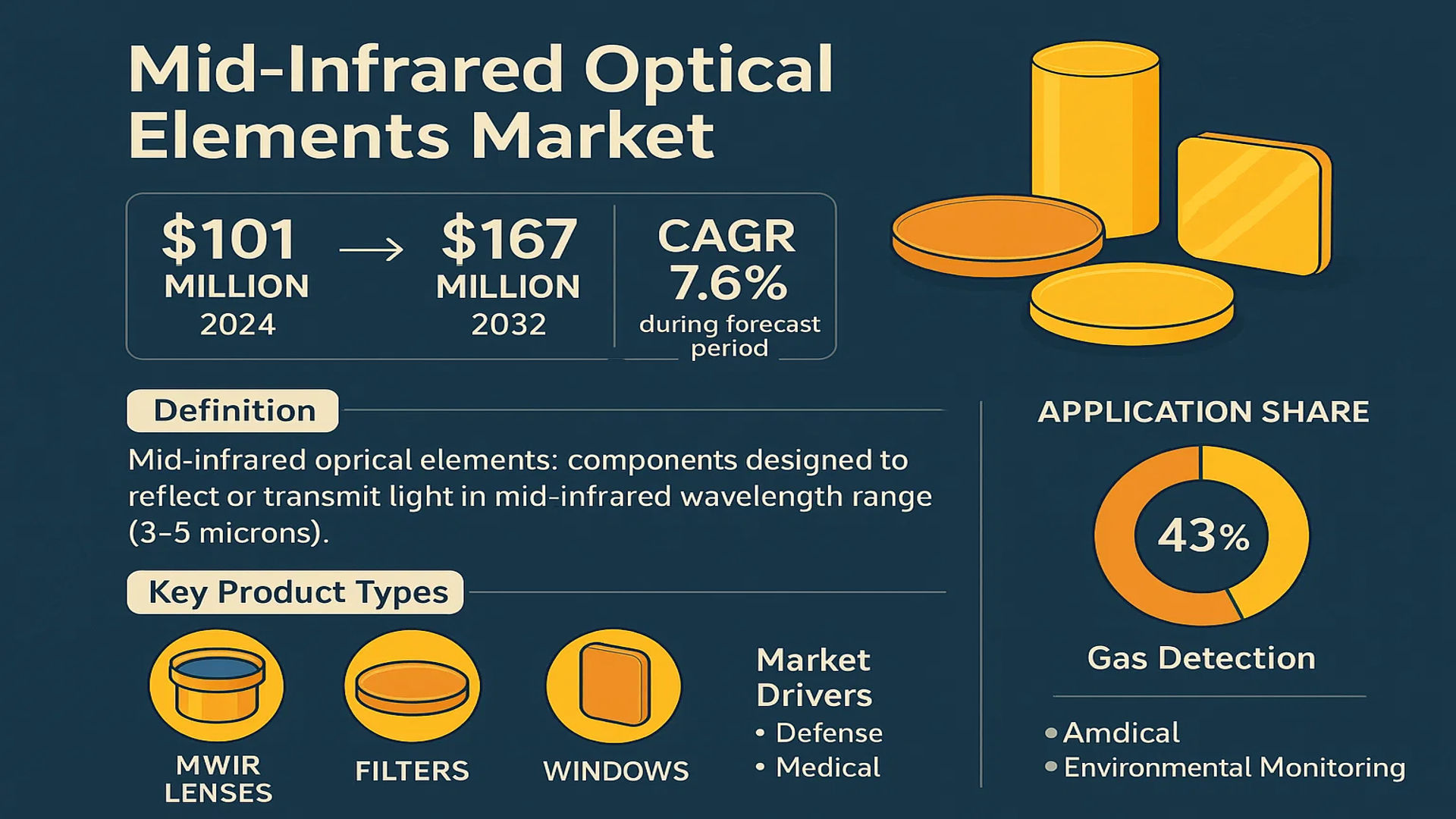

The global Mid-Infrared Optical Elements Market was valued at 101 million in 2024 and is projected to reach US$ 167 million by 2032, at a CAGR of 7.6% during the forecast period.

Mid-infrared optical elements are specialized components designed to reflect or transmit light in the mid-infrared wavelength range (3-5 microns). These elements play a critical role in applications requiring infrared imaging, spectroscopy, and thermal detection. Key product types include MWIR lenses, filters, and windows, primarily manufactured using specialized materials like zinc selenide and germanium that offer high transmittance, refractive index, and thermal stability.

Market growth is driven by increasing demand across defense, medical, and environmental monitoring sectors. For instance, the gas detection segment accounts for 43% of application share due to stringent industrial safety regulations. Europe dominates the market with 36% revenue share, followed by Asia-Pacific (34%), where China’s growing defense and healthcare sectors are accelerating adoption. Key players like Umicore, Jenoptik, and Edmund Optics collectively hold over 30% market share, with recent investments in advanced coatings and compact optical designs further propelling industry expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Infrared Imaging in Security and Defense to Accelerate Market Growth

The global mid-infrared optical elements market is experiencing significant growth due to increasing adoption of infrared imaging technologies in security and defense sectors. Mid-infrared optical components, such as lenses and filters, are critical in thermal imaging systems used for surveillance, target identification, and night-vision applications. With rising geopolitical tensions and security concerns, defense budgets in key regions such as North America and Europe have surged, leading to higher procurement of advanced imaging systems. These components are integral to modern military equipment, driving demand for high-performance mid-infrared optical elements.

Additionally, advances in material science have improved the durability and efficiency of these elements, making them more reliable for harsh operational environments. The growing modernization of military infrastructure and increasing investments in unmanned aerial vehicles (UAVs) further contribute to market expansion.

Expansion of Gas Detection and Environmental Monitoring Applications

The application of mid-infrared optical elements in gas detection and environmental monitoring is another key driver of market growth. These components are essential for spectrometers and sensors that detect hazardous gases, greenhouse emissions, and industrial pollutants. Stringent environmental regulations worldwide, particularly in North America and Europe, have increased the demand for precise and efficient monitoring systems.

Moreover, the energy sector’s reliance on infrared-based leak detection systems in oil and gas pipelines has amplified the need for reliable mid-infrared optics. Innovations in optical coating technologies have enhanced the sensitivity and selectivity of these systems, further boosting their adoption.

➤ The gas detection segment accounts for over 43% of the mid-infrared optical elements market, underscoring its dominance in applications.

Besides environmental monitoring, medical diagnostics also benefit from mid-infrared technologies, particularly in non-invasive testing and disease detection, fostering additional market opportunities.

MARKET RESTRAINTS

High Manufacturing Costs Impede Market Expansion

Despite strong market growth, high production costs of mid-infrared optical elements remain a critical challenge. The specialized materials required—such as zinc selenide and germanium—are expensive and subject to supply chain constraints. Advanced manufacturing processes, including precision grinding and anti-reflective coating applications, add to the overall cost, limiting affordability for price-sensitive markets.

These materials must meet stringent performance criteria, often requiring custom fabrication, which further increases production expenses. Small and medium-sized enterprises (SMEs) face particular difficulties in securing cost-effective supply chains, restricting their ability to compete with larger players.

Technical Complexities in Optical Design Challenge Adoption

Mid-infrared optical systems demand precise alignment and calibration to function optimally. Any deviation in lens positioning or coating uniformity can degrade performance, making integration into end-use applications technically demanding. The need for specialized expertise in optical design and maintenance further complicates market penetration.

Additionally, thermal stability issues emerge when operating in extreme environments, affecting long-term reliability. These technical obstacles require continuous R&D investment, deterring some manufacturers from expanding their product portfolios.

MARKET OPPORTUNITIES

Advancements in Laser Technology Open New Market Avenues

Emerging laser applications in material processing, medical surgery, and defense present lucrative growth opportunities for mid-infrared optical elements. High-power laser systems increasingly utilize infrared optics for beam shaping and wavelength tuning, creating demand for precision components.

Additionally, medical laser systems for dermatology and ophthalmology rely heavily on mid-infrared lenses and filters, opening new revenue streams. The expansion of industrial laser cutting and welding also fuels market prospects.

Strategic Collaborations and Government Funding Boost Innovation

Increased government funding for defense and aerospace R&D is accelerating technological advancements in mid-infrared optics. Key industry players are forming strategic partnerships to enhance production capabilities and develop next-generation optical solutions.

Moreover, rising investments in climate monitoring and renewable energy infrastructure drive the demand for high-performance optical sensors, further expanding market potential. With continuous improvements in material science and manufacturing techniques, the industry is poised for sustained long-term growth.

MID-INFRARED OPTICAL ELEMENTS MARKET TRENDS

Demand for Precision Optical Solutions Drives Mid-Infrared Market Growth

The global Mid-Infrared Optical Elements market is witnessing significant expansion due to increasing demand for high-precision optical components in critical applications. With the market valued at $101 million in 2024 and projected to reach $167 million by 2032, the sector demonstrates a robust 7.6% CAGR. This growth stems from the unique properties of mid-infrared optics, particularly their ability to operate effectively in the 3-5 micron wavelength range where many gases and materials exhibit distinctive absorption signatures. Recent advancements in materials science have enhanced the performance and durability of zinc selenide and germanium-based components, which collectively account for over 60% of optical materials used in this spectrum.

Other Trends

Expansion in Environmental Monitoring Applications

Gas detection and environmental monitoring currently dominate mid-infrared optical element applications, holding about 43% of the market share. Strict environmental regulations worldwide are accelerating adoption of infrared-based monitoring systems, particularly for detecting greenhouse gases and industrial emissions. The development of compact, field-deployable FTIR spectrometers incorporating advanced mid-IR optics has enabled real-time air quality monitoring with detection sensitivities below 1 part per billion for many compounds. While conventional systems remain important, there’s growing demand for miniaturized components compatible with IoT-enabled environmental sensors.

Technological Advancements in Military and Security Systems

The security and defense sector represents another key growth area, currently accounting for approximately 28% of mid-IR optical element applications. Modern thermal imaging systems for surveillance and targeting increasingly rely on high-performance MWIR lenses to achieve superior image resolution at longer ranges. Recent conflicts have demonstrated the tactical advantages of mid-wave infrared systems, particularly in low-visibility conditions. Manufacturers are responding by developing ruggedized optical assemblies with enhanced durability and performance characteristics, including broadband anti-reflection coatings that maintain over 95% transmission across the MWIR spectrum. These innovations are particularly crucial for integration into next-generation unmanned systems and soldier-worn sensor packages.

Regional Market Dynamics and Competitive Landscape

Europe currently leads the mid-infrared optical elements market with 36% global share, supported by strong industrial and research infrastructure. However, Asia-Pacific is rapidly closing the gap with 34% market share, driven by expanding manufacturing capabilities in China and increasing defense spending across the region. The competitive landscape remains concentrated, with the top four players – Umicore, Edmund Optics, Jenoptik, and Andover Corporation – collectively holding over 30% of the market. Product innovation remains critical, evidenced by recent launches of aspheric MWIR lenses with reduced weight and improved thermal stability for aerospace applications. Material science breakthroughs in chalcogenide glasses may potentially reshape the market by offering cost-effective alternatives to traditional crystalline materials.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic R&D Investments and Product Differentiation Drive Market Positioning

The global mid-infrared optical elements market features a competitive landscape with a mix of established corporations and specialized manufacturers. The market remains moderately concentrated, with the top four players—Umicore N.V., Edmund Optics Inc., Jenoptik AG, and Andover Corporation—collectively accounting for over 30% of the market share as of 2024. Europe leads in market dominance, holding around 36% of global revenues, followed closely by Asia-Pacific and North America.

Umicore N.V. maintains a strong foothold due to its vertically integrated supply chain and advanced material science capabilities, particularly in zinc selenide and germanium-based optical components. Meanwhile, Edmund Optics Inc. has carved a niche in customized mid-infrared solutions, supported by its extensive distribution network across industrial and defense sectors. Both companies are intensifying their focus on high-growth applications like gas detection systems, which represent 43% of the market demand.

New entrants and mid-sized players are gaining traction through technological differentiation. For instance, LightPath Technologies, Inc. recently expanded its molded chalcogenide glass optics production, addressing cost barriers in thermal imaging applications. Similarly, Jenoptik AG augmented its market position through the 2023 acquisition of a laser optics specialist, broadening its infrared product lineup.

The competitive dynamics are further shaped by regional expertise. Asian manufacturers like Wavelength Opto-Electronic leverage localized supply chains to cater to the region’s 34% market share, while North American firms prioritize defense and medical applications through collaborations with research institutions. Notably, over 60% of new product launches in 2023-2024 featured anti-reflective coatings for harsh environments, reflecting industry-wide emphasis on durability.

List of Key Mid-Infrared Optical Elements Manufacturers

- Umicore N.V. (Belgium)

- Edmund Optics Inc. (U.S.)

- Jenoptik AG (Germany)

- Andover Corporation (U.S.)

- Alkor Technologies (Russia)

- Solaris Optics SA (Poland)

- Thorlabs, Inc. (U.S.)

- Lattice Materials LLC (U.S.)

- LightPath Technologies, Inc. (U.S.)

- Asphericon GmbH (Germany)

- IRD Ceramics (U.K.)

Segment Analysis:

By Type

MWIR Lens Segment Dominates the Market Due to Growing Demand in Imaging and Sensing Applications

The mid-infrared optical elements market is segmented based on type into:

- MWIR Lens

- MWIR Filters

- Others

By Application

Gas Detection and Environmental Monitoring Leads the Market Due to Stringent Industrial Regulations

The market is segmented based on application into:

- Gas Detection and Environmental Monitoring

- Medical and Biomedical Applications

- Security and Defense

- Others

By Material

Germanium-Based Components Hold Significant Market Share Due to Optical Efficiency

Mid-infrared optical elements are segmented by material type into:

- Zinc Selenide (ZnSe)

- Germanium (Ge)

- Silicon (Si)

- Others

Regional Analysis: Mid-Infrared Optical Elements Market

Europe

Europe is the leading market for mid-infrared optical elements, accounting for 36% of global demand, driven by robust investments in defense, medical technologies, and environmental monitoring systems. Germany and France dominate with well-established manufacturing ecosystems for precision optics, supported by companies like Jenoptik AG and Umicore N.V. The EU’s focus on emission monitoring under directives such as the Industrial Emissions Directive (IED) has accelerated demand for gas detection systems utilizing MWIR filters and lenses. High R&D expenditure—averaging 2.2% of GDP—fosters innovation in optical coatings and materials like zinc selenide. However, stringent environmental and safety regulations increase production costs, creating challenges for smaller suppliers.

Asia-Pacific

The Asia-Pacific region holds a 34% market share, with China leading due to its expansive manufacturing capabilities for infrared components in security, industrial, and healthcare applications. Japan and South Korea follow, specializing in high-performance MWIR lenses for automotive night vision and semiconductor inspection. India’s market is growing at a rapid pace, driven by government initiatives like “Make in India” to bolster domestic optics production. Cost-sensitive demand keeps conventional germanium-based components dominant, although environmental policies are gradually shifting preferences toward advanced materials. Supply chain efficiencies and competitive labor costs position the region as a production hub, but intellectual property concerns persist.

North America

North America captures 23% of the market, propelled by defense applications and environmental compliance requirements. The U.S. is the largest consumer, leveraging MWIR optics in military surveillance (e.g., FLIR systems) and methane detection for oil & gas operations. Companies like Edmund Optics and LightPath Technologies benefit from federal funding in aerospace and medical research. Stricter EPA regulations on emissions monitoring sustain demand for high-precision filters. However, reliance on imports for raw materials like germanium and zinc selenide exposes the region to supply chain vulnerabilities, while labor costs challenge price competitiveness.

South America

The region shows nascent growth, with Brazil and Argentina investing in infrared applications for agriculture and mining. The lack of localized production forces reliance on European and North American imports, inflating costs. Economic instability and underdeveloped regulatory frameworks slow adoption, though rising awareness of infrared spectroscopy in environmental testing hints at untapped potential. Expanding industrial sectors and foreign partnerships could unlock opportunities in the long term.

Middle East & Africa

This emerging market is driven by defense and oilfield applications, particularly in the UAE and Saudi Arabia. Infrared optics are increasingly used for border security and pipeline leak detection. Limited local expertise and high dependency on imports hinder market penetration, but infrastructure modernization programs and foreign collaborations offer growth avenues. Africa’s market remains constrained by budget limitations, though South Africa shows promise in medical and research applications.

Report Scope

This market research report provides a comprehensive analysis of the global Mid-Infrared Optical Elements market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 101 million in 2024 and is projected to reach USD 167 million by 2032, growing at a CAGR of 7.6%.

- Segmentation Analysis: Detailed breakdown by product type (MWIR Lens, MWIR Filters, Others), application (Gas Detection, Medical, Defense, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (23% share), Europe (36% share), Asia-Pacific (34% share), and other regions with country-level analysis.

- Competitive Landscape: Profiles of 14 key players including Umicore N.V., Edmund Optics, and Jenoptik AG, covering their product portfolios, market shares (top 4 players hold 30% share), and strategic developments.

- Technology Trends: Assessment of material innovations (zinc selenide, germanium), coating technologies, and integration with infrared systems.

- Market Drivers & Restraints: Analysis of factors such as growing defense spending, environmental monitoring needs, alongside challenges like high material costs.

- Stakeholder Analysis: Strategic insights for optical component manufacturers, system integrators, and investors in the mid-IR ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mid-Infrared Optical Elements Market?

-> Mid-Infrared Optical Elements Market was valued at 101 million in 2024 and is projected to reach US$ 167 million by 2032, at a CAGR of 7.6% during the forecast period 2032.

Which key companies operate in this market?

-> Leading players include Umicore, Edmund Optics, Jenoptik, Andover Corporation, Thorlabs, and LightPath Technologies.

What are the key growth drivers?

-> Growth is driven by increasing defense & security applications (43% market share), environmental monitoring needs, and medical diagnostics adoption.

Which region dominates the market?

-> Europe leads with 36% market share, followed by Asia-Pacific (34%) as the fastest-growing region.

What are the emerging trends?

-> Emerging trends include advanced coating technologies, miniaturization of components, and integration with AI-based imaging systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...