MicroLED Display Market Insights

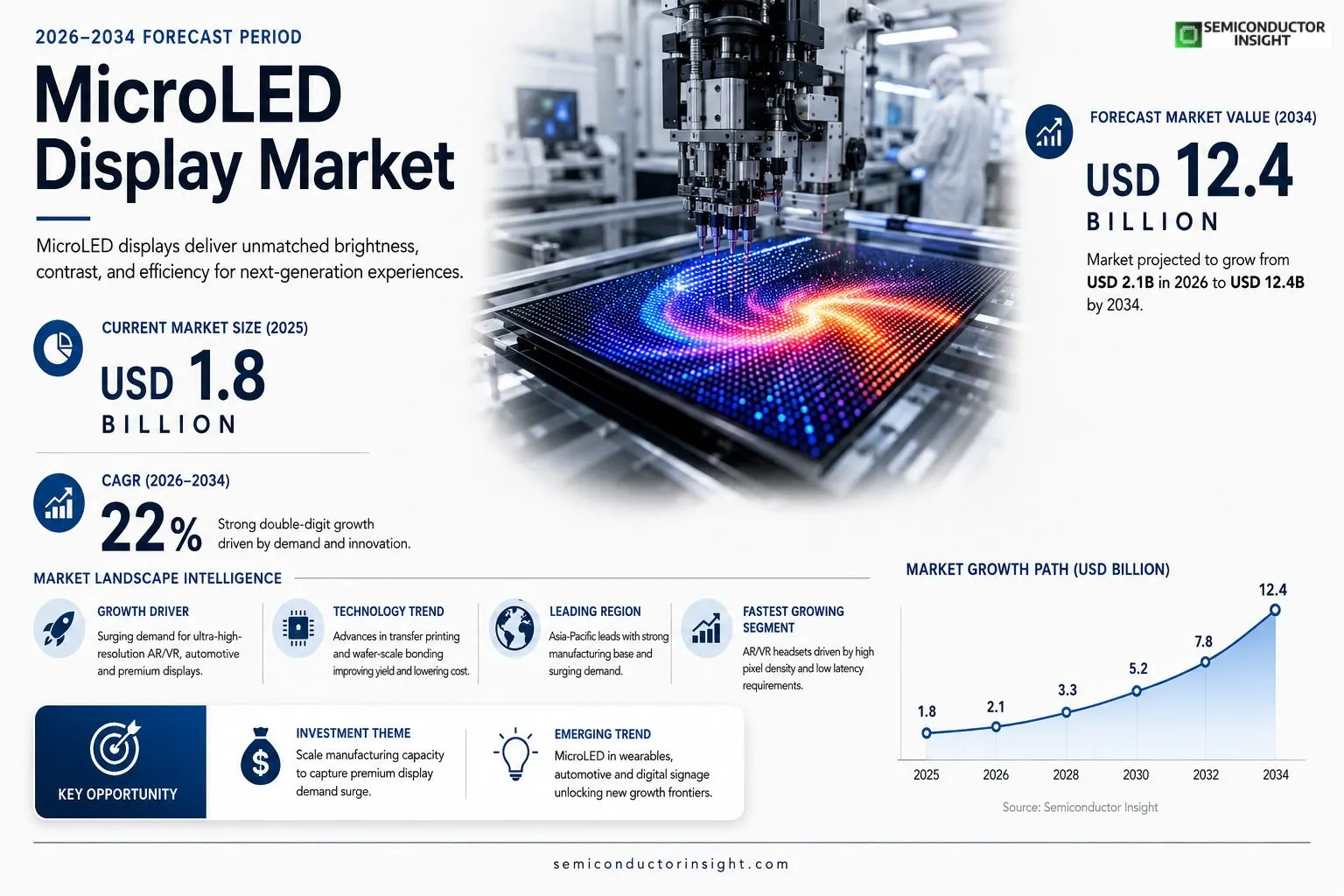

MicroLED Display Market size was valued at USD 1.8 billion in 2025. The market is projected to grow from USD 2.1 billion in 2026 to USD 12.4 billion by 2034, exhibiting a CAGR of 22% during the forecast period.

MicroLED displays are self‑emissive panels composed of microscopic inorganic LEDs that act as individual pixels, delivering superior brightness, contrast, energy efficiency and longer lifespan compared with LCD or OLED technologies.

The market is accelerating because consumer demand for high‑resolution AR/VR headsets, automotive infotainment screens and ultra‑thin televisions is rising sharply; however, manufacturing yield challenges remain significant. Furthermore, major investments from Samsung, Apple and Sony are driving scale‑up of production lines, while emerging applications in wearables and digital signage further broaden adoption.

MARKET DRIVERS

Rising Consumer Demand for Ultra‑High‑Resolution Displays

MicroLED Display Market is being propelled by a surge in consumer preference for larger, brighter screens in smartphones, wearables, and premium televisions. Manufacturers are leveraging MicroLED’s ability to deliver over 1,000 nits of brightness while maintaining low power consumption, creating a compelling value proposition for early adopters.

Advancements in Mass‑Production Techniques

Recent breakthroughs in wafer‑scale bonding and transfer printing have reduced unit costs by roughly 20% compared with early‑stage prototypes. These manufacturing efficiencies enable OEMs to scale production volumes without sacrificing the pixel‑level precision that distinguishes MicroLED from OLED and LCD technologies.

➤ MicroLED offers superior brightness, durability, and energy efficiency, positioning it as a next‑generation display solution.

Enterprise adoption is also expanding, with automotive heads‑up displays and AR/VR headsets integrating MicroLED for improved contrast and extended lifespan. This cross‑industry traction further reinforces the long‑term growth outlook of MicroLED Display Market.

MARKET CHALLENGES

High Capital Expenditure for Production Infrastructure

Establishing a full‑scale MicroLED fab requires significant upfront investment in precision alignment equipment and cleanroom facilities. The capital intensity creates a barrier for new entrants and prolongs the payback period for existing players.

Other Challenges

Yield Optimization

Maintaining high yields across billions of micro‑LED chips remains technically demanding. Even minor defects can lead to noticeable dead pixels, impeding product reliability and increasing scrap rates.In addition, supply‑chain constraints for high‑purity gallium nitride (GaN) substrates can delay production schedules, making it harder for manufacturers to meet fast‑changing market demand.

MARKET RESTRAINTS

Limited Content Ecosystem Compatibility

Although MicroLED hardware is maturing, many content creation workflows and software tools remain optimized for LCD and OLED pipelines. The lack of standardized calibration profiles and color‑grading processes hampers rapid adoption in broadcast and cinema applications.

MARKET OPPORTUNITIES

Emerging Applications in AR/VR and Automotive

AR/VR headsets demand displays with high pixel density, low latency, and minimal burn‑in risk—all strengths of MicroLED. Companies are already prototyping 5‑inch MicroLED modules that could double current resolution benchmarks, opening a sizable niche market.Automotive manufacturers are also exploring MicroLED for instrument clusters and augmented reality windshields, where the technology’s high brightness ensures readability under direct sunlight while reducing power draw compared with conventional LEDs.Furthermore, the rollout of 5G infrastructure is expected to accelerate demand for edge devices with superior visual performance, creating downstream opportunities for MicroLED Display Market to capture new revenue streams.

MicroLED Display Market Trends

Rising Demand in AR/VR and Automotive Infotainment

MicroLED Display Market is experiencing a notable shift as consumer expectations for immersive visual experiences intensify. High‑resolution augmented and virtual reality headsets now require panels that can deliver exceptional brightness and contrast while maintaining low power consumption, qualities that only self‑emissive MicroLED technology can consistently provide. Simultaneously, automotive manufacturers are integrating larger, curved infotainment screens that must perform reliably across a wide temperature range; MicroLED displays meet these criteria through their inherent durability and extended lifespan. Major ecosystem players such as Samsung and Sony have announced multi‑billion‑dollar investments to expand production capacity, signaling confidence in sustained demand. This convergence of consumer electronics and vehicle integration creates a robust growth engine that is reshaping supply chain priorities and prompting tier‑one component suppliers to accelerate tooling upgrades.

Other Trends

Manufacturing Yield Challenges

Despite strong commercial interest, MicroLED Display Market faces persistent yield constraints that stem from the microscopic size of individual LED pixels. Transfer‑printing processes must align millions of sub‑micron emitters onto a substrate with nanometer precision, and even minor misplacements can render a panel unusable. As a result, many manufacturers report lower-than‑expected first‑pass yields, which drives up unit costs and slows time‑to‑market. Industry analysts note that incremental improvements in automation, such as AI‑guided inspection systems and advanced wafer‑level bonding techniques, are gradually reducing defect rates. However, until yield thresholds consistently exceed 80 percent, large‑scale adoption in cost‑sensitive segments like mainstream television will remain cautious.

Emerging Opportunities in Wearables and Digital Signage

Beyond flagship devices, MicroLED Display Market is expanding into niche applications that benefit from its thin form factor and high energy efficiency. Wearable health monitors and smart glasses are leveraging MicroLED panels to achieve brighter displays without compromising battery life, enabling longer usage periods for end‑users. In parallel, digital signage installations in high‑traffic venues are adopting MicroLED modules to deliver vivid imagery even under direct sunlight, while also reducing maintenance cycles due to the technology’s long operational lifespan. These emerging use‑cases diversify the market’s revenue streams and encourage a broader ecosystem of design houses and OEMs to explore custom form factors, further reinforcing the technology’s strategic relevance across multiple industries.

COMPETITIVE LANDSCAPEKey Industry Players

MicroLED Display Market Competitive Landscape

MicroLED Display Market is currently dominated by a few large semiconductor and consumer‑electronics firms that have the scale to invest in high‑volume production lines. Samsung Electronics leads the segment with its “Neo QLED” and “The Wall” product families, leveraging its advanced OLED and LCD fabs to achieve high yields. Sony follows closely, focusing on professional‑grade MicroLED panels for broadcasting and cinema applications, while Apple has entered the ecosystem as a major customer and co‑developer, driving demand for ultra‑high‑resolution panels in AR/VR headsets. These tier‑1 players shape market structure through vertically integrated supply chains, significant R&D budgets, and strategic partnerships that accelerate the transition from pilot to mass production.Beyond the leaders, a diverse set of niche manufacturers and component suppliers are expanding the ecosystem. LG Display and TCL are scaling up their TV‑oriented MicroLED lines, targeting premium consumer markets. BOE Technology Group and Sharp are leveraging their LCD expertise to enter automotive infotainment and digital signage. Specialty firms such as Epistar, Leyard, and Plessey provide LED chipsets, backplane technologies, and packaging solutions that enable smaller form‑factor devices. Emerging Chinese players including AU Optronics and Innolux are focusing on cost‑effective modules for wearables and portable displays, while Corning supplies the glass substrates essential for high‑temperature processing. Collectively, these companies broaden the competitive landscape and support the projected CAGR of over 20 % through 2034.

List of Key MicroLED Companies Profiled

- Samsung Electronics

- Sony Corporation

- Apple Inc.

- LG Display

- TCL Technology

- BOE Technology Group

- Sharp Corporation

- Epistar Corp.

- Leyard Optoelectronic

- Plessey Semiconductors

- AU Optronics

- Innolux Corporation

- Corning Incorporated

- MicroLED Displays Inc.

- LuxVue Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Self‑emissive MicroLED is emerging as the dominant technological choice because it delivers unmatched brightness, contrast, and longevity.

|

| By Application |

|

Consumer Electronics lead the adoption curve, driven by demand for high‑resolution televisions and next‑generation handheld devices.

|

| By End User |

|

Home Entertainment remains the primary driver, as users seek cinema‑like picture quality in living spaces.

|

| By Integration Level |

|

Embedded Modules are gaining traction because they allow manufacturers to incorporate MicroLED into complex form factors.

|

| By Adoption Phase |

|

Mainstream Adoption is now the focal point as ecosystems mature and supply‑chain constraints ease.

|

Regional Analysis: Asia-Pacific

Asia-Pacific

Driven by the demand for premium displays in smartphones, televisions, and wearable devices, the consumer electronics segment constitutes a major driver of MicroLED adoption in Asia-Pacific. The region’s vast consumer base and the high propensity for technology adoption create a favorable environment for MicroLEDs to gain traction.

The automotive industry in Asia-Pacific is undergoing a rapid transformation, with increasing demand for advanced in-car displays. MicroLEDs offer significant advantages in terms of brightness, contrast, and energy efficiency, making them well-suited for automotive applications such as instrument clusters and infotainment systems.

The growing commercial sector in Asia-Pacific, encompassing retail, advertising, and digital signage, presents substantial opportunities for MicroLED displays. The ability to create vibrant, energy-efficient, and long-lasting displays is highly valued in these applications.

Emerging applications in industrial control panels and medical visualization systems are contributing to the growth of the MicroLED market in Asia-Pacific, leveraging the technology’s durability and high-clarity visuals.

North America

North America represents a significant market for MicroLED Displays, particularly in high-end consumer electronics and specialized industrial applications. The region’s advanced technological infrastructure and strong focus on research and development make it a key area for innovation in display technology. The market here is driven by the demand for premium displays in smartphones, televisions, and automotive applications. While adoption rates are currently moderate, the region’s affluent consumer base and robust investment in technological advancements suggest promising growth potential. The focus is on delivering superior visual experiences and incorporating MicroLEDs into high-value products.

Europe

Europe is steadily gaining traction in MicroLED Display Market, with a focus on automotive, industrial, and architectural applications. Stringent energy efficiency regulations and a growing emphasis on sustainability are driving interest in MicroLED technology. The region’s strong manufacturing base and established automotive industry create opportunities for MicroLED adoption in in-car displays. European research institutions are also actively involved in advancing MicroLED technology, fostering innovation and market development. The adoption pace is influenced by the cost-effectiveness of MicroLEDs compared to established display technologies.

Asia-Pacific

Asia-Pacific is the leading region in MicroLED Display Market, spearheaded by countries like China, South Korea, and Japan. This region exhibits a strong manufacturing ecosystem, a large consumer base, and significant government support for technological innovation. The demand for advanced displays in smartphones, televisions, and automotive applications is a key driver of market growth. The presence of major display manufacturers and component suppliers in this region further contributes to its dominance in the MicroLED market. Cost competitiveness and rapid technological advancements are hallmarks of the Asia-Pacific market.

South America

South America presents a nascent but potentially growing market for MicroLED Displays. The increasing disposable incomes and rising demand for consumer electronics are creating opportunities for MicroLED adoption. Initial applications are expected to focus on high-end consumer devices and commercial displays. However, challenges related to infrastructure development and economic stability may hinder rapid market growth.

Middle East & Africa

The Middle East & Africa region is an emerging market for MicroLED Displays. Investments in infrastructure projects, particularly in the automotive and commercial sectors, are expected to drive demand for advanced display solutions. The region’s growing consumer electronics market and increasing adoption of smart technologies create a favorable environment for MicroLED adoption in the long term. However, market growth is currently limited by relatively high costs and the need for greater awareness of the technology’s benefits.

Report Scope

This market research report provides a comprehensive analysis of the MicroLED Display Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MicroLED Display Market?

-> MicroLED Display Market was valued at USD 1.8 billion in 2025 and is expected to reach USD 12.4 billion by 2034. The market is projected to grow from USD 2.1 billion in 2026 to that level, exhibiting a CAGR of 22% during the forecast period.

Which key companies operate in MicroLED Display Market?

-> Key players include Samsung, Apple, Sony, among others, driving scale‑up of production lines.

What are the key growth drivers?

-> Key growth drivers include rising consumer demand for high‑resolution AR/VR headsets, automotive infotainment screens, ultra‑thin televisions, and significant investments in manufacturing capacity.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, supported by strong demand in consumer electronics and automotive sectors, while North America and Europe also show substantial adoption.

What are the emerging trends?

-> Emerging trends include wearable displays, digital signage applications, and integration of MicroLED technology in next‑generation mixed‑reality devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...