MARKET INSIGHTS

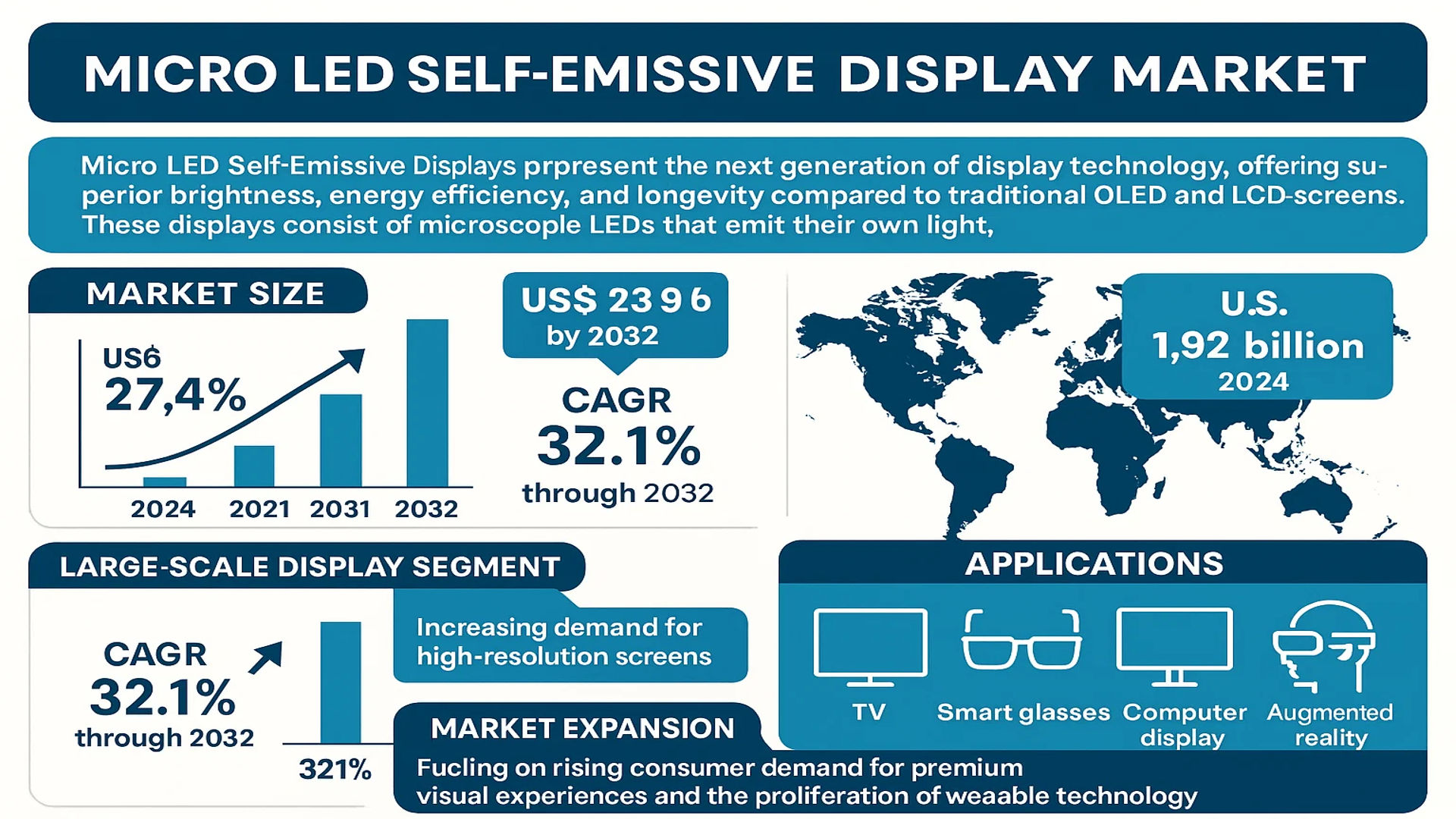

The global Micro LED Self-Emissive Display Market size was valued at US$ 2.0 billion in 2024 and is projected to reach US$ 13.9 billion by 2032, at a CAGR of 27.4% during the forecast period 2025-2032. The U.S. market size is estimated at USD 420 million in 2024, while China is expected to reach USD 1.92 billion by 2032. The Large-scale Display segment, driven by increasing demand for high-resolution screens, is anticipated to grow at a CAGR of 32.1% through 2032.

Micro LED Self-Emissive Displays represent the next generation of display technology, offering superior brightness, energy efficiency, and longevity compared to traditional OLED and LCD screens. These displays consist of microscopic LEDs that emit their own light, eliminating the need for backlighting while delivering exceptional contrast ratios and color accuracy. Applications span across TVs, smart glasses, computer displays, and augmented reality devices, with major tech giants investing heavily in commercialization.

The market expansion is fueled by rising consumer demand for premium visual experiences and the proliferation of wearable technology. Recent developments include Samsung’s 2023 launch of a 89-inch Micro LED TV and Apple’s patent filings for Micro LED integration in future devices. Key players such as LG Display and Sony are accelerating production capabilities to meet projected demand, with the top five manufacturers controlling over 65% of 2024’s global revenue share.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Superior Display Technologies in Consumer Electronics to Propel Market Growth

The global Micro LED self-emissive display market is experiencing robust growth due to increasing demand for high-resolution, energy-efficient displays across consumer electronics. Micro LEDs offer superior brightness, contrast ratios, and longevity compared to traditional LCD and OLED technologies, making them ideal for premium televisions and smartphones. The global television market alone is expected to surpass 220 million units annually by 2026, with premium models increasingly adopting Micro LED technology. Recent advances in manufacturing processes have improved yield rates from less than 50% to over 70%, accelerating commercial viability for mass-market applications.

Emerging Applications in AR/VR and Automotive Displays to Accelerate Adoption

Micro LED technology is gaining traction in augmented reality devices and automotive displays due to its exceptional performance in sunlight visibility and low power consumption. The AR/VR headset market is projected to exceed 50 million units by 2027, with major manufacturers integrating Micro LED displays for their compact size and high pixel density capabilities. In automotive applications, the technology enables superior head-up displays that maintain clarity under direct sunlight while consuming minimal power. These expanding use cases across industries are creating a $3.5 billion addressable market opportunity for Micro LED displays beyond traditional consumer electronics.

Furthermore, government investments in advanced display manufacturing are enhancing production capabilities globally, particularly in Asia-Pacific regions where semiconductor expertise continues to expand rapidly.

MARKET CHALLENGES

High Manufacturing Costs and Yield Challenges to Constrain Market Expansion

While Micro LED technology offers superior performance characteristics, the market faces substantial challenges in mass production scalability. Current manufacturing costs remain prohibitively high, with production expenses for large-scale Micro LED displays exceeding traditional LCD panels by 300-400%. The complex transfer process required to place millions of microscopic LEDs results in low yields, increasing per-unit costs. Even with recent process improvements, defect rates remain above acceptable thresholds for consumer pricing models, limiting adoption primarily to premium product segments.

Other Challenges

Technology Integration Complexities

The integration of Micro LED displays requires precise alignment at micron-level tolerances, creating significant engineering challenges. Thermal management and power distribution become increasingly complex as pixel densities exceed 10,000 PPI for AR/VR applications.

Material Supply Constraints

Limited availability of specialized substrates and epitaxial materials creates supply chain bottlenecks. Current manufacturing capacity can only support approximately 20% of projected demand through 2028 without substantial new facility investments.

MARKET RESTRAINTS

Competition from Alternative Display Technologies to Slow Market Penetration

Micro LED adoption faces strong competition from continually improving OLED and mini-LED technologies that offer comparable performance at lower price points. OLED manufacturing costs have decreased by over 60% in the past five years while achieving similar contrast ratios, making them more accessible for mid-range products. The display technology market remains highly cost-sensitive, with consumers showing reluctance to pay premium prices for incremental visual quality improvements. This creates significant price elasticity challenges, particularly in emerging markets where display preferences prioritize affordability over technological sophistication.

Other Restraints

Limited Standardization Across Manufacturing

The absence of industry-wide standards for Micro LED production creates interoperability issues between components from different suppliers. This fragmentation increases development costs and complicates supply chain management for device manufacturers.

Intellectual Property Barriers

Dense patent portfolios held by major corporations create legal uncertainties for new market entrants. Several key manufacturing processes remain protected, requiring costly licensing agreements that can delay product development cycles by 12-18 months.

MARKET OPPORTUNITIES

Emerging Applications in Healthcare and Industrial Sectors to Create New Revenue Streams

Beyond consumer electronics, Micro LED technology presents significant growth potential in medical imaging and industrial applications where display performance directly impacts operational outcomes. Surgical displays requiring high dynamic range and color accuracy are transitioning to Micro LED solutions, creating a $750 million niche market. Industrial applications including flight simulators and military-grade displays benefit from the technology’s durability and sunlight readability, with projected adoption rates exceeding 8% annually through 2030. These specialized applications demonstrate greater cost tolerance and may serve as proving grounds for technology maturation before broader consumer market penetration.

Strategic Collaborations to Accelerate Technological Advancements

Recent partnerships between display manufacturers and semiconductor companies are driving innovation in Micro LED production techniques. Collaborative R&D efforts have reduced pixel pitch requirements by 40% since 2021 while improving transfer yields through advanced laser-assisted processes. These joint ventures combine expertise in LED fabrication with display integration, potentially reducing mass production costs to competitive levels within five years. Such technological convergence creates opportunities throughout the value chain, from materials suppliers to end-product integrators, enabling new business models in the display ecosystem.

➤ The market outlook for Micro LED displays remains strong, with government initiatives supporting domestic display manufacturing capabilities in multiple regions potentially overcoming current supply chain constraints.

MICRO LED SELF-EMISSIVE DISPLAY MARKET TRENDS

Rising Demand for High-End Consumer Electronics to Drive Micro LED Adoption

The Micro LED self-emissive display market is witnessing significant traction, fueled by the increasing demand for high-resolution, power-efficient displays in premium electronics. Leading manufacturers such as Apple and Samsung are investing heavily in commercializing Micro LED technology for applications like TVs, smart glasses, and augmented reality (AR) devices. The market is projected to grow at a compound annual growth rate (CAGR) of over 40% between 2024 and 2032, driven by the superior image quality and energy efficiency of Micro LEDs compared to OLED and LCD alternatives. Recent advancements in manufacturing, including mass transfer techniques and defect repair solutions, are reducing production costs, making the technology more viable for mass-market adoption.

Other Trends

Expansion in AR/VR and Automotive Displays

The rapid growth of augmented and virtual reality applications is accelerating the adoption of Micro LED displays in head-mounted devices. Companies like Oculus and Sony are leveraging Micro LED’s high brightness and pixel density to create immersive experiences with lower power consumption. Additionally, automotive manufacturers are increasingly integrating Micro LED displays into dashboards and infotainment systems due to their durability in extreme conditions. This trend is expected to boost the small and medium-sized display segment, which is anticipated to account for 35% of the market share by 2030.

Technological Challenges and Supply Chain Constraints

Despite its potential, the Micro LED industry faces significant hurdles, including high production costs and yield issues. Current technologies require intricate fabrication processes, with defect rates remaining a bottleneck for scalability. However, collaborations between key players like LG Display and startups such as Play Nitride are driving innovations in chip manufacturing and assembly techniques. Furthermore, China’s investments in domestic production aim to reduce reliance on imported displays, which could reshape the global supply chain dynamics. While these challenges persist, advancements in modular and hybrid manufacturing approaches are expected to lower entry barriers for new market players.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Giants and Innovators Drive Competitive Dynamics in Micro LED Display Market

The global Micro LED Self-Emissive Display market features a highly competitive landscape dominated by major electronics corporations and specialized innovators. Apple Inc. and Samsung Electronics currently lead the market, accounting for a combined revenue share of over 35% in 2024. Their dominance stems from substantial R&D investments and early adoption of Micro LED technology in premium consumer electronics.

Sony Corporation maintains strong positioning through its high-end display solutions, particularly in the professional and large-scale display segments. Meanwhile, LG Display has been accelerating its Micro LED development to compete in both the consumer TV and commercial display markets.

The competitive intensity is further heightened by emerging specialists such as Play Nitride and VueReal, who are driving innovation in manufacturing processes to address current yield challenges. These companies are actively forming strategic alliances with display panel manufacturers to commercialize their technologies.

Several players are adopting vertical integration strategies to secure supply chains and reduce production costs. Recent industry movements include Samsung’s increased investment in Micro LED production capacity and Apple’s acquisition of specialist Micro LED technology firms to secure its future product roadmap.

List of Key Micro LED Display Companies Profiled

- Apple Inc. (U.S.)

- Samsung Electronics (South Korea)

- Sony Corporation (Japan)

- Oculus VR (U.S.)

- VueReal (Canada)

- LG Display (South Korea)

- Play Nitride (Taiwan)

- eLUX (U.S.)

- Rohinni (U.S.)

- Aledia (France)

- MICLEDI (Belgium)

Segment Analysis:

By Type

Large-scale Display Segment Dominates Due to High Demand in Commercial and Public Displays

The market is segmented based on type into:

- Large-scale Display

- Small & Medium-sized Display

By Application

TV Segment Leads Due to Rapid Adoption in Premium Home Entertainment Systems

The market is segmented based on application into:

- TV

- Smart Glasses

- Computer Display

- Others

By Technology

Full-Color Micro LED Technology Thrives Owing to Superior Brightness and Efficiency

The market is segmented based on technology into:

- Monochrome Micro LED

- Full-Color Micro LED

- Hybrid Micro LED

By End User

Consumer Electronics Sector Dominates with High Adoption in Smart Devices

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Healthcare

- Retail & Advertising

- Others

Regional Analysis: Micro LED Self-Emissive Display Market

Asia-Pacific

Asia-Pacific dominates the Micro LED self-emissive display market, driven by strong manufacturing ecosystems, technological advancements, and high demand for premium displays. Countries like China, South Korea, and Japan are leading the adoption due to significant investments in research and development. China’s display manufacturing capabilities, backed by companies like BOE and TCL CSOT, contribute to the region’s leadership. Meanwhile, South Korean giants such as Samsung and LG Display are pioneering Micro LED commercialization, focusing on large-scale displays and AR/VR applications. High consumer electronics demand and government support for next-gen display technologies further accelerate growth.

North America

North America is a key innovator in Micro LED technology, with major players like Apple and start-ups such as VueReal driving advancements. The U.S. market benefits from strong R&D investments, particularly in smart glasses and high-end TVs. Consumer demand for energy-efficient, high-resolution displays and increasing adoption of augmented reality devices fuel market expansion. However, high production costs remain a challenge, slowing mass-market penetration. Collaborations between tech companies and display manufacturers are crucial for overcoming scalability issues and enhancing commercial viability.

Europe

Europe shows steady growth in Micro LED adoption, supported by stringent energy efficiency regulations and strong AR/VR application development. Companies like Aledia in France and MICLEDI in Belgium are key innovators, focusing on Micro LED microdisplays for wearables and automotive HUDs. The region’s emphasis on sustainability aligns well with Micro LED’s low-power advantages. However, limited local manufacturing capabilities and reliance on Asian suppliers constrain faster market expansion. Despite this, partnerships with global display leaders and investment in niche applications ensure long-term potential.

South America

South America’s Micro LED market is nascent, with growth primarily driven by imports of high-end consumer electronics. While countries like Brazil and Argentina have rising disposable incomes, adoption is limited by premium pricing and infrastructural challenges. Local production is virtually nonexistent, making the region heavily dependent on foreign suppliers. Nevertheless, as global costs decrease and regional digital transformation accelerates, Micro LED displays may see gradual uptake, particularly in commercial and luxury segments.

Middle East & Africa

The Middle East & Africa market remains in early stages, with adoption concentrated in high-end commercial and hospitality sectors. The UAE and Saudi Arabia lead demand, driven by smart city initiatives and luxury retail applications. However, limited local expertise and high costs restrict broader penetration. While the region shows long-term promise due to increasing urbanization and digitalization, near-term growth will depend on global supply chain improvements and affordability.

Report Scope

This market research report provides a comprehensive analysis of the Global Micro LED Self-Emissive Display Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at US$ 2.0 billion in 2024 and is projected to reach US$ 13.9 billion by 2032, growing at a CAGR of 27.4%.

- Segmentation Analysis: Detailed breakdown by product type (Large-scale Display, Small & Medium-sized Display) and application (TV, Smart Glasses, Computer Display, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets like the U.S., China, Japan, and Germany.

- Competitive Landscape: Profiles of leading market participants including Apple, Samsung, Sony, LG Display, and VueReal, covering their product offerings, R&D investments, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging Micro LED technologies, manufacturing advancements, and integration with AR/VR applications.

- Market Drivers & Restraints: Evaluation of factors like demand for high-resolution displays and challenges in mass production yield rates.

- Stakeholder Analysis: Strategic insights for display manufacturers, component suppliers, and investors regarding market opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Micro LED Self-Emissive Display Market?

-> Micro LED Self-Emissive Display Market size was valued at US$ 2.0 billion in 2024 and is projected to reach US$ 13.9 billion by 2032, at a CAGR of 27.4% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Apple, Samsung, Sony, LG Display, VueReal, Play Nitride, and eLUX, among others.

What are the key growth drivers?

-> Growth is driven by increasing demand for high-resolution displays, energy-efficient technologies, and adoption in AR/VR applications.

Which region dominates the market?

-> Asia-Pacific leads in market share due to strong manufacturing presence, while North America shows fastest growth in adoption.

What are the emerging trends?

-> Emerging trends include advancements in mass transfer technology, miniaturization of LEDs, and integration with flexible displays.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...