MARKET INSIGHTS

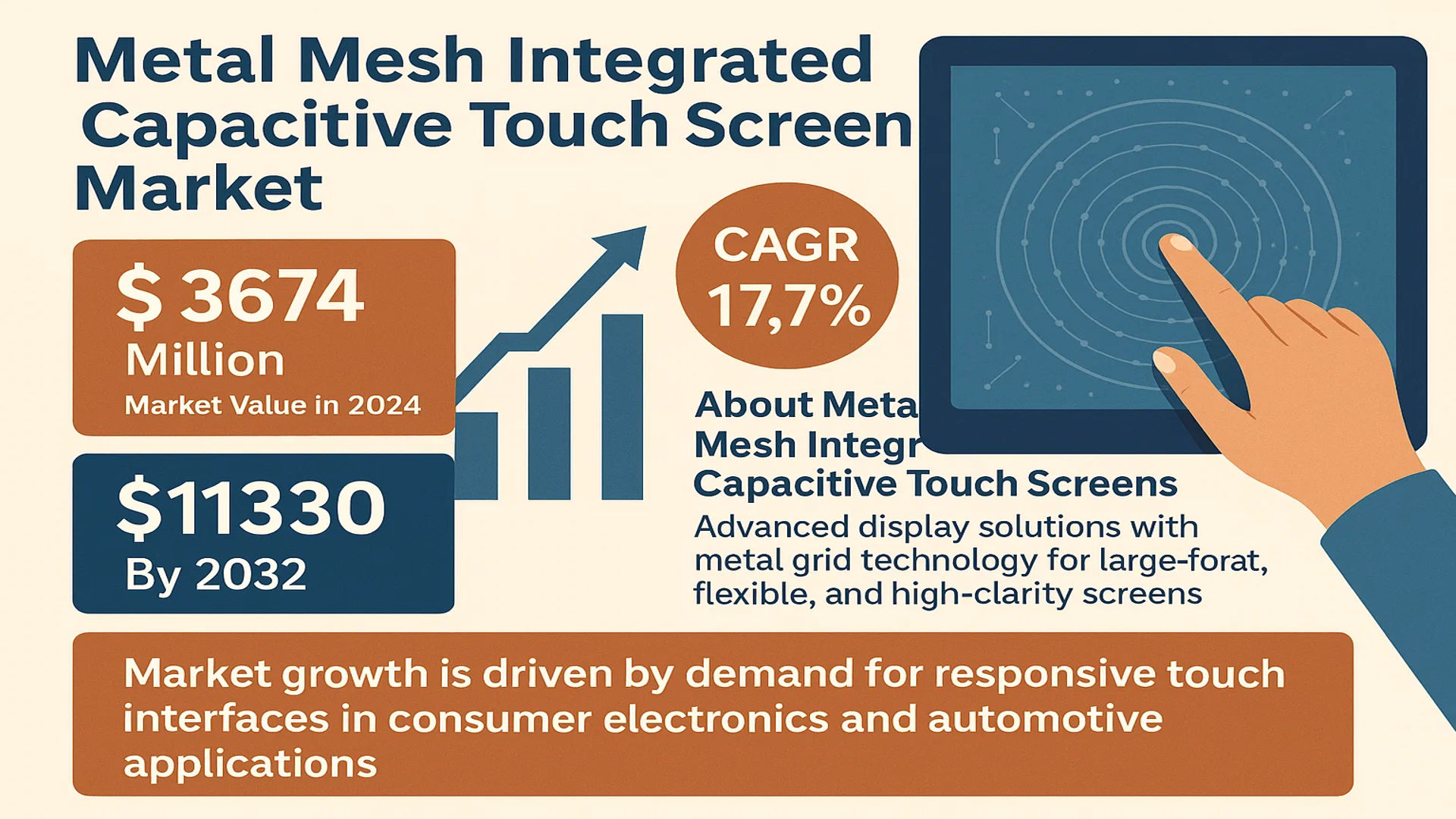

The global Metal Mesh Integrated Capacitive Touch Screen market was valued at 3674 million in 2024 and is projected to reach US$ 11330 million by 2032, at a CAGR of 17.7% during the forecast period.

Metal mesh integrated capacitive touch screens are advanced display solutions that utilize metal grid technology to enhance performance. These screens replace traditional ITO (indium tin oxide) electrodes with fine metallic grid patterns, offering superior conductivity, durability, and touch sensitivity. The technology is particularly advantageous for large-format displays, flexible screens, and devices requiring high optical clarity.

The market growth is driven by increasing demand for responsive touch interfaces in consumer electronics and automotive applications. While copper-based metal mesh dominates the market due to cost-effectiveness, silver-based alternatives are gaining traction in premium devices. Key players like TPK Holding and Nissha Printing are expanding production capacities to meet the growing demand from smartphone and automotive display manufacturers. The Asia-Pacific region, particularly China, accounts for over 45% of global production capacity as of 2024.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Large-Screen Interactive Displays to Accelerate Market Expansion

The increasing adoption of large-format interactive displays across multiple industries is a key driver for metal mesh capacitive touch screens. The global interactive display market is projected to exceed 12 billion units by 2026, with education and corporate sectors accounting for over 60% of installations. Metal mesh technology’s superior scalability makes it ideal for screens ranging from 20 to 86 inches, enabling seamless touch functionality without sacrificing optical clarity. Recent developments in automotive infotainment systems, which now average 12.3-inch displays in premium vehicles, further demonstrate this technology’s growing application scope.

Advancements in Flexible Display Technologies to Boost Adoption

The emergence of flexible and foldable display solutions represents a significant growth opportunity. Metal mesh touchscreens demonstrate exceptional performance in flexible applications due to their mechanical durability and low resistance to bending stress. The foldable display market is forecasted to grow at 41% CAGR through 2030, with major smartphone manufacturers already integrating metal mesh solutions in their newest models. These screens maintain consistent touch performance through over 200,000 folding cycles, making them preferred for next-generation mobile devices.

Additionally, the technology’s compatibility with curved surfaces enables innovative applications in automotive interiors and public kiosks. Several luxury automakers have recently adopted curved instrument clusters using metal mesh technology, demonstrating its reliability in demanding environments.

➤ Metal mesh touchscreens achieve up to 90% transmittance rates while offering 40% lower resistivity compared to traditional ITO solutions, making them ideal for high-performance applications.

The combination of these technical advantages with falling production costs is expected to drive widespread adoption across multiple industries.

MARKET RESTRAINTS

High Manufacturing Complexity and Yield Challenges Restrict Market Penetration

Despite its advantages, metal mesh technology faces significant production hurdles. The manufacturing process requires precise deposition of metallic grid patterns at micron-level resolutions, with typical production yields currently hovering around 70-75% for large format screens. This results in higher per-unit costs compared to conventional touch technologies, particularly for displays under 15 inches. The complex photolithography and etching processes contribute to approximately 30% higher capital expenditures for production facilities.

Additional Technical Constraints

Material Cost Volatility

The reliance on precious metals like silver for conductive grids exposes manufacturers to commodity price fluctuations. The spot price of silver has shown 28% annual volatility over the past five years, creating challenges for cost forecasting and supply chain management.

Moisture Sensitivity

Certain metal mesh formulations demonstrate sensitivity to environmental moisture, requiring additional protective coatings that add to production costs. This limitation particularly impacts applications in high-humidity environments such as outdoor kiosks and marine equipment.

MARKET CHALLENGES

Competition from Alternative Technologies Impacts Market Share

The metal mesh segment faces intensifying competition from emerging touch technologies. Silver nanowire solutions now achieve comparable conductivity at potentially lower costs, while self-capacitive designs eliminate the need for discrete sensor layers altogether. The alternative touch technologies market is projected to grow at 22% CAGR through 2030, potentially limiting metal mesh adoption in price-sensitive segments.

Other Critical Challenges

Supply Chain Bottlenecks

Specialized equipment required for metal mesh production faces lead times of 6-9 months, slowing capacity expansion. Recent semiconductor shortages have further exacerbated equipment availability issues across the display industry.

Standardization Gaps

The lack of universal specifications for metal mesh patterning creates interoperability challenges. Device manufacturers report up to 15% performance variation between different suppliers’ products, complicating design-in processes.

MARKET OPPORTUNITIES

Expansion into Industrial and Medical Applications Creates New Growth Vectors

The growing digitization of industrial interfaces presents significant opportunities. Metal mesh technology’s resistance to electromagnetic interference makes it particularly suitable for factory automation equipment, where traditional touchscreens often fail. Industrial HMI applications are projected to account for 25% of metal mesh demand by 2027, up from just 12% in 2024. Medical devices represent another promising sector, with touch-enabled diagnostic equipment growing at 18% annually.

Emerging applications in augmented reality interfaces and transparent displays also show strong potential. Several major technology firms are developing see-through metal mesh solutions for next-generation heads-up displays, combining high transparency with precise touch detection. These innovations could unlock entirely new product categories in both consumer and professional markets.

The technology’s compatibility with emerging 8K resolution standards further enhances its future prospects, as traditional touch technologies struggle with the increased signal density requirements of ultra-high-definition displays.

METAL MESH INTEGRATED CAPACITIVE TOUCH SCREEN MARKET TRENDS

Advancements in Flexible and Large-Size Displays Drive Market Expansion

The global Metal Mesh Integrated Capacitive Touch Screen market is witnessing rapid growth, driven by increasing demand for high-performance touch solutions in consumer electronics and automotive applications. With a projected CAGR of 17.7%, the market is set to expand from $3.67 billion in 2024 to $11.33 billion by 2032, largely fueled by the rising adoption of flexible and large-format displays. Metal mesh technology replaces traditional ITO electrodes with fine conductive metal grids, improving touch sensitivity and durability while enabling thinner and more responsive touch interfaces. The development of ultra-thin, foldable, and curved screens has further accelerated demand, particularly in smartphones, tablets, and automotive infotainment systems.

Other Trends

Rising Demand in Automotive and Industrial Applications

While consumer electronics remain the dominant application sector, automotive and industrial automation segments are gaining momentum. Metal mesh touch screens are increasingly used in vehicle dashboards, navigation systems, and industrial control panels due to their high durability and resistance to electromagnetic interference. The rise of connected and autonomous vehicles is further amplifying adoption rates. Meanwhile, industrial automation applications benefit from the technology’s robustness in harsh environments, driving 17% year-over-year growth in this segment as of 2024.

Material Innovation and Competitive Landscape

Copper-based metal mesh currently leads the market with over 60% revenue share in 2024, owing to its cost efficiency and conductivity. However, silver-based alternatives are gaining traction in premium applications due to superior optical clarity, with manufacturers like Nissha Printing and TPK investing heavily in R&D. The market remains highly competitive, with the top five players holding approximately 45% market share. Recent mergers, such as collaborations between display manufacturers and touch sensor specialists, are reshaping the industry ecosystem to offer integrated solutions. China and the U.S. continue to be focal points for production and innovation, accounting for nearly 55% of global demand collectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Shape Market Dynamics

The global metal mesh integrated capacitive touch screen market exhibits a moderately fragmented landscape with a mix of leading manufacturers and emerging players competing for market share. The industry is characterized by rapid technological advancements and increasing demand for high-performance touch solutions across consumer electronics, automotive, and industrial applications.

FORTEC Integrated and Nissha Printing currently hold dominant positions in this space, leveraging their expertise in large-format touch screen manufacturing and strong distribution networks across Asia and North America. These companies are focusing on developing ultra-thin, flexible displays to meet the growing demand for foldable devices – a segment projected to grow at 21% CAGR from 2024-2028.

Asian manufacturers like TPK and AU Optronics are gaining significant traction through aggressive pricing strategies and large-scale production capabilities. However, their growth is somewhat constrained by ongoing supply chain complexities and raw material price volatility affecting metal mesh production costs, particularly for silver-based solutions which currently account for 38% of the market.

Meanwhile, MELFAS and Innolux are investing heavily in R&D to develop next-generation touch solutions with improved durability and reduced power consumption. Recent collaborations between display manufacturers and automotive companies suggest promising growth potential for in-vehicle touch applications, which could account for 22% of the market by 2026.

List of Key Metal Mesh Touch Screen Manufacturers

- FORTEC Integrated (China)

- Nissha Printing (Japan)

- TPK Holding Co. (Taiwan)

- Wintek Corporation (Taiwan)

- Young Fast Optoelectronics (Taiwan)

- AU Optronics (Taiwan)

- HannsTouch Solution (Taiwan)

- Innolux Corporation (Taiwan)

- Iljin Display (South Korea)

- MELFAS (South Korea)

- Truly Semiconductors (China)

- TSI Touch (U.S.)

- Fujifilm (Japan)

- Laibao Hi-Tech (China)

- Micron Optoelectronics (China)

Market competition is intensifying as established players leverage their manufacturing scale while newer entrants focus on niche applications. The recent introduction of hybrid metal mesh-nanowire solutions by several companies indicates an industry-wide push toward next-gen transparent conductive materials that could redefine market dynamics in coming years.

Segment Analysis:

By Type

Copper Based Metal Mesh Segment Leads Due to High Conductivity and Cost-Effectiveness

The market is segmented based on type into:

- Copper Based Metal Mesh

- Subtypes: Single-layer copper mesh, multi-layer copper mesh

- Silver Based Metal Mesh

- Subtypes: Pure silver mesh, silver alloy mesh

- Others

- Including novel alloy combinations and hybrid materials

By Application

Consumer Electronics Sector Dominates with Increasing Demand for Large-Format Touch Displays

The market is segmented based on application into:

- Consumer Electronics

- Smartphones

- Tablets

- Laptops

- Smart TVs

- Automotive

- Infotainment systems

- Control panels

- Digital dashboards

- Medical Devices

- Diagnostic equipment interfaces

- Surgical operation panels

- Industrial Automation

- Control panels

- HMI interfaces

- Others

By Resolution

High-Resolution Applications Drive Market Growth for Enhanced Visual Experience

The market is segmented based on resolution into:

- Standard Resolution (≤1080p)

- High Resolution (2K-4K)

- Ultra High Resolution (≥ 4K)

By Screen Size

Large Screen Segment Gains Traction for Commercial Applications

The market is segmented based on screen size into:

- Small (≤10 inches)

- Medium (10-32 inches)

- Large (≥32 inches)

Regional Analysis: Metal Mesh Integrated Capacitive Touch Screen Market

Asia-Pacific

The Asia-Pacific region dominates the global metal mesh integrated capacitive touch screen market, accounting for over 50% of worldwide demand. This leadership stems from China’s massive electronics manufacturing ecosystem, where companies like BOE, Tianma, and TPK mass-produce touch panels for smartphones, tablets, and automotive displays. Japan remains a key innovation hub, with companies like Nissha Printing developing ultra-thin metal mesh solutions for foldable devices. While cost-driven manufacturers initially favored traditional ITO touchscreens, the superior durability and performance of metal mesh technology is driving rapid adoption across premium devices. India’s expanding consumer electronics sector presents new opportunities, though local production capabilities remain limited compared to China.

North America

North America represents the second-largest market, fueled by strong demand from the automotive and industrial sectors. U.S.-based companies are early adopters of metal mesh touchscreens for applications requiring durability and precision, such as medical equipment and ruggedized tablets. The region benefits from close collaboration between manufacturers like 3M and Microchip Technology with display developers. However, higher production costs compared to Asia have led many North American brands to source touch panels from overseas suppliers, creating supply chain dependencies. Recent investments in domestic advanced manufacturing aim to reduce this reliance.

Europe

European adoption focuses on high-end applications where performance justifies the premium pricing of metal mesh technology. German automotive manufacturers lead in integrating these touchscreens for infotainment systems, valuing their superior optical clarity and responsiveness in varying temperatures. The region’s strict product safety and environmental regulations have accelerated development of RoHS-compliant metal mesh solutions. While Europe hosts few large-scale manufacturers, research institutions and startups are pioneering advancements in flexible and transparent metal mesh designs for next-generation displays.

South America

The South American market remains in growth phase, constrained by limited local manufacturing capabilities and reliance on imports. Brazil represents the largest regional consumer, primarily for consumer electronics applications. Economic volatility and currency fluctuations continue to challenge stable market expansion. However, increasing foreign investment in Mexican electronics production could stimulate regional availability of metal mesh touch solutions at more competitive price points in coming years.

Middle East & Africa

This emerging market shows promising demand in specialized segments like industrial control systems and digital signage, though volume remains low compared to other regions. The UAE and Saudi Arabia are adopting metal mesh touchscreens for high-end commercial applications, while African nations mainly utilize the technology through imported consumer devices. Infrastructure limitations and lower purchasing power currently restrict widespread adoption, but the region’s growing urbanization suggests long-term potential as manufacturing ecosystems develop.

Report Scope

This market research report provides a comprehensive analysis of the Global Metal Mesh Integrated Capacitive Touch Screen Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 3,674 million in 2024 and is projected to reach USD 11,330 million by 2032, growing at a CAGR of 17.7%.

- Segmentation Analysis: Detailed breakdown by product type (Copper Based Metal Mesh, Silver Based Metal Mesh, Others), application (Consumer Electronics, Automotive, Medical Devices, Industrial Automation), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including FORTEC Integrated, Nissha Printing, TPK, Wintek, AU Optronics, and others, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies in metal mesh touchscreens, including advancements in conductivity, flexibility, and integration with next-gen displays.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as demand for large-size displays and foldable devices, along with challenges like material costs and manufacturing complexity.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, investors, and policymakers regarding market opportunities and competitive positioning.

The report employs primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Metal Mesh Integrated Capacitive Touch Screen Market?

->Metal Mesh Integrated Capacitive Touch Screen market was valued at 3674 million in 2024 and is projected to reach US$ 11330 million by 2032, at a CAGR of 17.7% during the forecast period.

Which key companies operate in this market?

-> Key players include FORTEC Integrated, Nissha Printing, TPK, Wintek, AU Optronics, HannsTouch Solution, Innolux, and MELFAS, among others.

What are the key growth drivers?

-> Growth is driven by rising demand for large-format touchscreens, foldable displays, and automotive infotainment systems, along with superior performance compared to traditional ITO solutions.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, while North America shows strong growth in high-end applications.

What are the emerging trends?

-> Emerging trends include integration with flexible OLED displays, development of hybrid metal mesh solutions, and increasing adoption in automotive HMI systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...