Medical Embedded Systems Market Insights

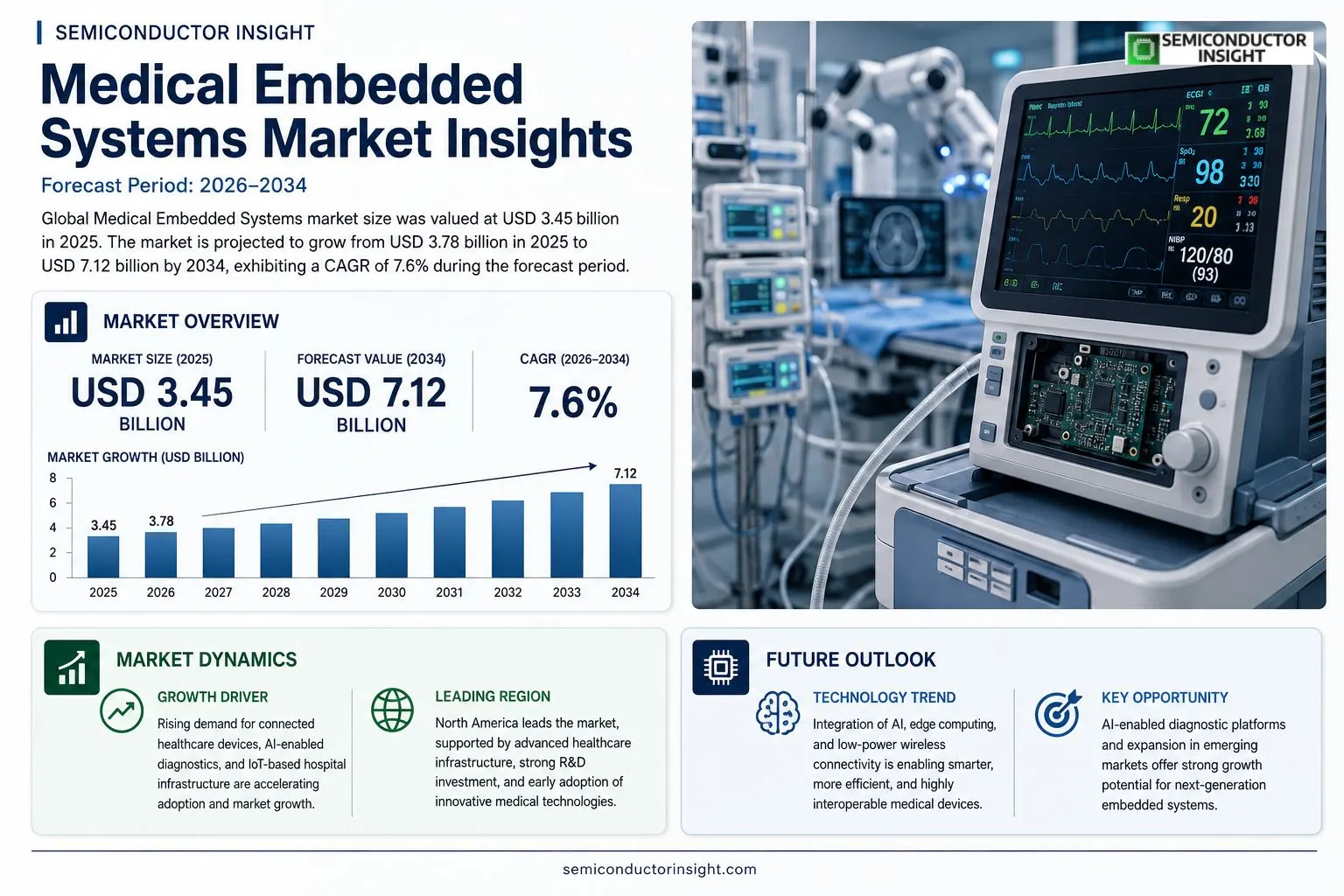

Global Medical Embedded Systems market size was valued at USD 3.45 billion in 2025. The market is projected to grow from USD 3.78 billion in 2025 to USD 7.12 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period.

Medical embedded systems are specialized computing platforms integrated into healthcare devices such as infusion pumps, diagnostic imaging equipment, wearable monitors, and robotic surgical tools. These systems combine real‑time operating systems, sensor interfaces, and secure communication protocols to process physiological data, control therapeutic actions, and ensure patient safety while complying with stringent regulatory standards.

The market is experiencing robust expansion driven by rising demand for remote patient monitoring, increasing adoption of AI‑enabled diagnostics, and growing investment in IoT‑based hospital infrastructure. Furthermore, regulatory incentives for digital health solutions and the push toward personalized medicine are accelerating deployments worldwide. Key playersincluding Philips Healthcare, Medtronic, GE Healthcare, Siemens Healthineers, and Abbottare advancing their portfolios through strategic partnerships and continuous firmware innovations that enhance device reliability and data interoperability.

MARKET DRIVERS

Rising Demand for Connected Healthcare Devices

Medical Embedded Systems Market is being propelled by a surge in wearable monitors, implantable sensors, and bedside diagnostic units that enable real‑time patient data transmission. Hospitals are allocating up to 15 % of their IT budget to integrated platforms that support remote monitoring, driving steady revenue growth.

Regulatory Support and Reimbursement Policies

Governments across North America and Europe have introduced reimbursement codes for tele‑health enabled devices, reducing financial barriers for providers. This policy environment accelerates adoption cycles, with projected annual sales increases of 8 % for compliant solutions.

➤ Integration of AI enhances diagnostic accuracy and reduces false‑positive rates by up to 12 %.

Manufacturers are also benefitting from standardization initiatives such as IEC 62304, which streamline certification timelines and lower development costs, further reinforcing market momentum.

MARKET CHALLENGES

Complexity of System Integration

Embedding advanced analytics into legacy medical equipment requires extensive hardware redesign and rigorous validation. Engineering teams face 30‑40 % longer development cycles, which can delay product launches and erode competitive advantage.

Other Challenges

Cybersecurity Vulnerabilities

The increased connectivity of embedded modules expands the attack surface, prompting hospitals to invest heavily in encryption and intrusion‑detection systems. Failure to address these risks can result in regulatory penalties and loss of patient trust.

MARKET RESTRAINTS

High Capital Expenditure for Upgrades

Upgrading existing infrastructure to accommodate next‑generation embedded controllers often requires capital outlays exceeding $200 million for large health systems, limiting budget flexibility in constrained fiscal periods.Additionally, the fragmented supplier ecosystem creates procurement bottlenecks, as hospitals must negotiate with multiple OEMs to ensure component compatibility, extending lead times.Lastly, stringent validation protocols for software updates increase the time and cost required to roll out new features, discouraging frequent innovation cycles.

MARKET OPPORTUNITIES

Growth of AI‑Enabled Diagnostic Platforms

Artificial‑intelligence algorithms embedded directly into medical devices can perform edge‑computing analysis, reducing reliance on cloud connectivity and enabling faster clinical decisions. This capability opens new revenue streams in intensive care and emergency response settings.Emerging markets in Asia‑Pacific are investing heavily in digital health infrastructure, presenting a 20 % compound annual growth potential for locally adapted embedded solutions.Furthermore, partnerships between semiconductor firms and healthcare providers are accelerating the development of ultra‑low‑power chips, which extend battery life for implantable devices and support longer monitoring periods.

Medical Embedded Systems Market Trends

Acceleration of Remote Patient Monitoring

Medical Embedded Systems Market is being reshaped by a surge in remote patient monitoring solutions that require highly reliable, low‑latency processors embedded in wearable and bedside devices. Healthcare providers are deploying infusion pumps, wearable vitals trackers, and home‑based diagnostic kits that rely on real‑time operating systems to capture and transmit physiological data securely. Regulatory bodies have introduced streamlined pathways for software‑defined medical devices, encouraging manufacturers to integrate advanced sensor fusion and edge‑AI capabilities. This regulatory encouragement, combined with the growing preference for virtual care models, is driving manufacturers to prioritize firmware that supports over‑the‑air updates, ensuring continuous compliance and device safety. The result is a measurable shift toward decentralized care, where embedded platforms act as the connective tissue between patients and cloud‑based analytics platforms.

Other Trends

AI‑Enabled Diagnostic Instruments

AI‑enabled diagnostic instruments represent a second pillar of growth within Medical Embedded Systems Market. Imaging modalities such as portable ultrasound and point‑of‑care radiography now incorporate neural‑network accelerators that pre‑process images before transmission to central PACS systems. These accelerators reduce latency, improve diagnostic accuracy, and enable real‑time decision support at the point of care. Leading vendors are investing in secure communication protocols that meet the stringent data‑privacy requirements of health information exchanges. Firmware updates now embed model‑version controls, allowing hospitals to roll out algorithm improvements without hardware changes. By embedding AI directly into the device stack, manufacturers are delivering differentiated value propositions that combine clinical efficacy with operational efficiency.

IoT Integration Across Hospital Infrastructure

The integration of Internet‑of‑Things (IoT) technologies into hospital infrastructure is emerging as a decisive trend for Medical Embedded Systems Market. Smart infusion pumps, networked ventilators, and connected surgical robots are being linked through interoperable middleware that aggregates device telemetry for predictive maintenance and resource optimization. Hospitals are adopting unified device management platforms that provide centralized monitoring dashboards, enabling rapid identification of fault conditions and reducing downtime. Partnerships between equipment manufacturers and cloud service providers are accelerating the rollout of edge‑compute gateways that preprocess data locally, thereby minimizing bandwidth consumption and enhancing latency‑critical applications such as closed‑loop drug delivery. This convergence of embedded hardware, secure networking, and analytics is positioning hospitals to achieve higher levels of operational resilience while supporting emerging care models.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Dynamics in Medical Embedded Systems 2025‑2034

Medical Embedded Systems Market is anchored by a handful of global giants that control the majority of high‑value platforms. Philips Healthcare, Medtronic, GE Healthcare, Siemens Healthineers and Abbott dominate the landscape by offering end‑to‑end computing solutions for imaging equipment, infusion pumps, robotic surgical tools and AI‑driven diagnostics. These incumbents benefit from deep regulatory expertise, extensive firmware development capabilities and strategic alliances with original equipment manufacturers (OEMs). The market structure remains oligopolistic at the upper tier, while a growing ecosystem of contract manufacturers and software‑only vendors provides niche components that feed into the larger platforms.Beyond the primary tier, a diverse set of niche innovators is expanding the breadth of functionality across specialized clinical domains. Boston Scientific, Johnson & Johnson (DePuy Synthes), Baxter International, Becton Dickinson, Canon Medical Systems, Roche Diagnostics, Samsung Medison, Fujifilm Healthcare, Nihon Kohden, Mindray, Edwards Lifesciences and Stryker are leveraging proprietary sensor integration, wearable monitoring and point‑of‑care analytics to differentiate their offerings. These players often pursue targeted partnerships or acquisitions to embed secure, real‑time operating systems into devices that address emerging therapeutic workflows such as remote patient monitoring, personalized medicine and AI‑enhanced image interpretation.

List of Key Medical Embedded Systems Companies Profiled

- Philips Healthcare

- Medtronic

- GE Healthcare

- Siemens Healthineers

- Abbott

- Boston Scientific

- Johnson & Johnson (DePuy Synthes)

- Baxter International

- Becton Dickinson

- Canon Medical Systems

- Roche Diagnostics

- Samsung Medison

- Fujifilm Healthcare

- Nihon Kohden

- Mindray

- Edwards Lifesciences

- Stryker

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hardware Platforms

|

| By Application |

|

Diagnostic Imaging Equipment

|

| By End User |

|

Hospitals & Clinics

|

| By Technology |

|

Artificial Intelligence Integration

|

| By Regulation |

|

FDA 21 CFR Part 820 Compliance

|

Regional Analysis: North America

North America

The adoption of advanced technologies like AI and IoT is significantly impacting Medical Embedded Systems Market in North America. These technologies are enabling the development of more intelligent and connected medical devices, leading to improved patient outcomes and enhanced operational efficiency.

Navigating the complex regulatory landscape in North America, particularly the FDA guidelines, is a key consideration for market players. Compliance with these regulations is essential for bringing new Medical Embedded Systems to market.

The North American Medical Embedded Systems market is highly competitive, with both large multinational corporations and smaller specialized companies vying for market share. Innovation and strategic partnerships are crucial for success in this environment.

Significant investment is flowing into the Medical Embedded Systems sector in North America, driven by the potential for innovation and growth. Venture capital funding and corporate R&D initiatives are key drivers of this investment.

North America

The North American Medical Embedded Systems market is experiencing robust growth, driven by increasing healthcare expenditure and a growing emphasis on technologically advanced medical solutions. The demand for systems used in patient monitoring, implantable devices, and diagnostic equipment is particularly strong. The integration of wireless communication and data analytics is a key trend shaping this market.

Europe

Europe presents a significant opportunity for Medical Embedded Systems, with a focus on innovation and stringent quality standards. The market is driven by an aging population and a growing need for cost-effective healthcare solutions. Key areas of growth include minimally invasive surgery and remote patient monitoring.

Asia-Pacific

The Asia-Pacific region is emerging as a high-growth market for Medical Embedded Systems, fueled by increasing healthcare spending and a growing middle class. Countries like China and India are witnessing rapid adoption of these systems due to expanding healthcare infrastructure and government initiatives.

South America

South America offers a promising market for Medical Embedded Systems, with increasing healthcare investments and a growing awareness of advanced medical technologies. The demand for diagnostic and monitoring systems is expected to rise in the coming years.

Middle East & Africa

The Middle East & Africa region presents a growing market for Medical Embedded Systems, driven by increasing healthcare awareness and government initiatives to improve healthcare infrastructure. The demand for advanced medical devices and diagnostic equipment is expected to rise in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Medical Embedded Systems Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Medical Embedded Systems Market?

-> Medical Embedded Systems Market was valued at USD 3.45 billion in 2025 and is expected to reach USD 7.12 billion by 2034.

Which key companies operate in Medical Embedded Systems Market?

-> Key players include Philips Healthcare, Medtronic, GE Healthcare, Siemens Healthineers, and Abbott, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for remote patient monitoring, increasing adoption of AI‑enabled diagnostics, growing investment in IoT‑based hospital infrastructure, regulatory incentives for digital health solutions, and the push toward personalized medicine.

Which region dominates the market?

-> The reference does not specify a single dominant region; market growth is observed globally across major regions.

What are the emerging trends?

-> Emerging trends include integration of AI and IoT in medical devices, expansion of remote monitoring platforms, and heightened focus on cybersecurity and data interoperability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...