Medical Electronic Components Market Insights

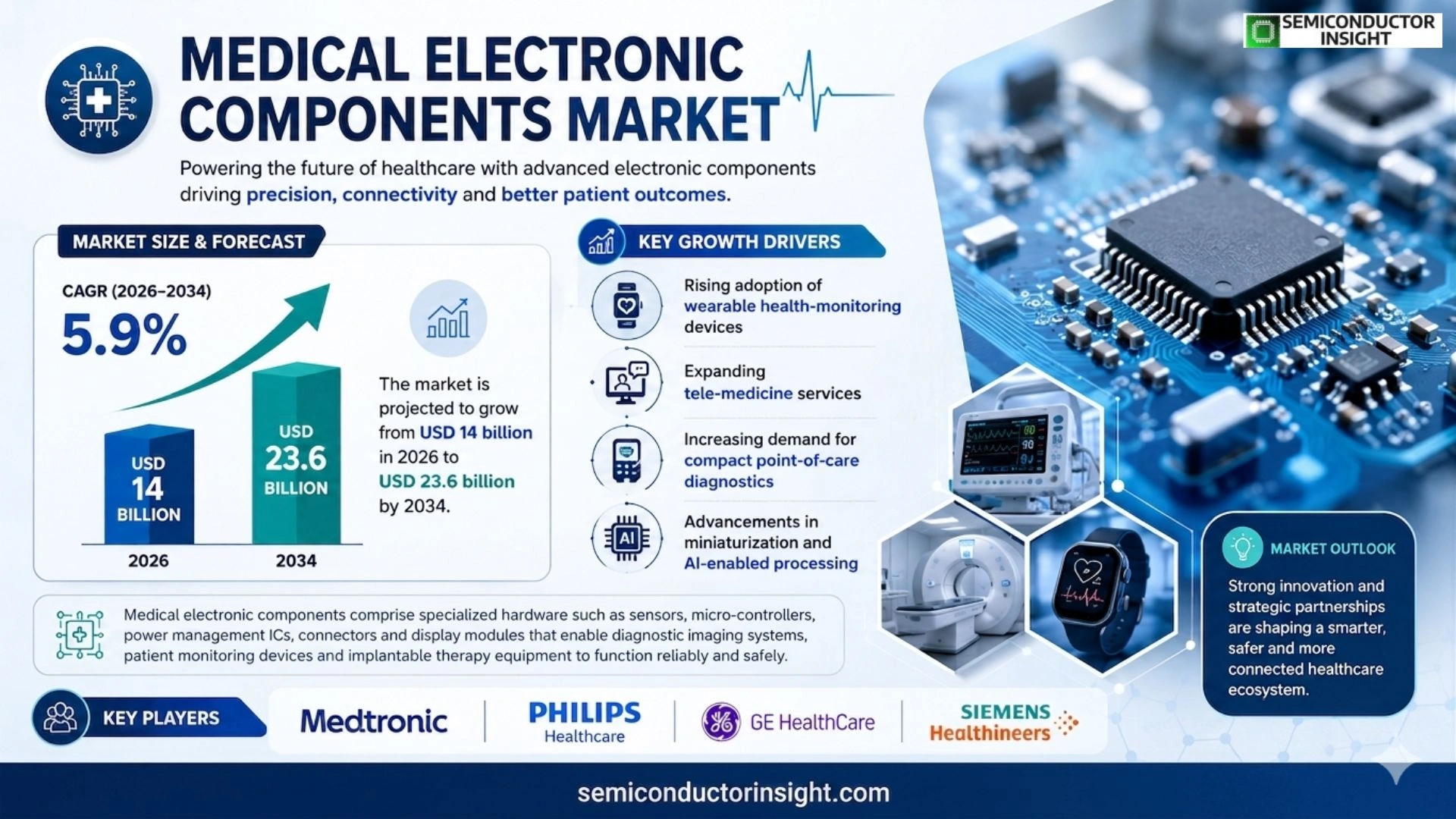

Global Medical Electronic Components Market size was valued at USD 14 billion in 2025. The market is projected to grow from USD 14 billion in 2025 to USD 23.6 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period.

Medical electronic components comprise specialized hardware such as sensors, micro‑controllers, power management ICs, connectors and display modules that enable diagnostic imaging systems, patient monitoring devices and implantable therapy equipment to function reliably and safely.

The market is experiencing rapid growth due to several factors, including rising adoption of wearable health‑monitoring wearables, expanding tele‑medicine services and increasing demand for compact point‑of‑care diagnostics. Furthermore, advancements in miniaturization and AI‑enabled processing are driving component innovation. Key players such as Medtronic, Philips Healthcare, GE Healthcare and Siemens Healthineers are actively investing in R&D partnerships,e.g., Siemens’ February 2024 collaboration with Qualcomm on AI edge chips,to capture emerging opportunities.

MARKET DRIVERS

Growing Demand for Wearable Diagnostics

Medical Electronic Components Market is being propelled by a surge in wearable diagnostic devices that enable continuous patient monitoring. Hospitals and clinics are increasingly adopting these solutions to improve outcomes and reduce readmission rates, driving robust component sales.

Advancements in Miniaturization Technology

Recent breakthroughs in semiconductor fabrication allow sensors and processors to occupy millimeter‑scale footprints. This miniaturization expands design flexibility for implantable and portable equipment, boosting demand for high‑precision chips and connectors.

➤ Integrated sensor modules are reducing device size while improving accuracy.

Overall, these drivers create a virtuous cycle where higher performance fuels broader clinical adoption, positioning Medical Electronic Components Market for sustained expansion.

MARKET CHALLENGES

Supply Chain Vulnerabilities

Geopolitical tensions and raw‑material shortages have introduced lead times that can exceed six months for specialty semiconductors. Manufacturers of medical components must balance inventory costs against the risk of production delays.

Other Challenges

High Component Costs

The rigorous certification processes for medical-grade parts increase production expenses, which in turn raise the overall cost of healthcare devices and can slow market adoption.

MARKET RESTRAINTS

Stringent Regulatory Approval Processes

Regulators require extensive validation of every electronic component used in medical devices, extending time‑to‑market and inflating development budgets. Compliance with standards such as IEC 60601 adds another layer of complexity.

Cybersecurity expectations are also rising, compelling manufacturers to embed advanced encryption and secure firmware updates, which further escalates design costs.

In addition, a limited pool of engineers experienced in both electronics and regulatory affairs constrains the ability to scale production quickly.

MARKET OPPORTUNITIES

Emergence of AI-Enabled Diagnostic Platforms

Artificial intelligence algorithms integrated with high‑speed processors enable real‑time analysis of physiological signals. This convergence creates new revenue streams for component suppliers that can deliver AI‑optimized hardware.

Expansion in Emerging Markets such as Southeast Asia and Latin America offers considerable upside, as healthcare infrastructure investments drive demand for affordable, reliable electronic modules.

The rapid growth of telehealth services is stimulating the need for compact, low‑power communication chips, opening a clear pathway for vendors to capture market share.

Medical Electronic Components Market Trends

Wearable Health Monitoring and Tele‑medicine Integration

The rise of remote patient care has accelerated demand for compact, low‑power sensors and connectivity modules that power wearable monitors and tele‑medicine platforms. Manufacturers are prioritizing components that combine real‑time data capture with secure wireless transmission, enabling clinicians to track vital signs outside traditional facilities. This shift is reflected in a growing share of battery‑efficient micro‑controllers and power‑management ICs designed for continuous operation over extended periods. As health systems adopt decentralized diagnostics, Medical Electronic Components Market is seeing a clear move toward highly integrated solutions that reduce device footprint while maintaining accuracy and reliability.

Other Trends

AI‑Enabled Miniaturization

Advances in artificial‑intelligence algorithms are driving component miniaturization, allowing diagnostic equipment to embed sophisticated signal‑processing capabilities directly on the chip. Recent releases of edge‑AI processors demonstrate how pattern‑recognition functions can be performed locally, minimizing latency for critical imaging systems and point‑of‑care devices. This trend supports faster clinical decision‑making and reduces reliance on cloud infrastructure, which is particularly valuable in bandwidth‑constrained environments. The convergence of AI and hardware design is creating a new class of smart components that adapt to patient‑specific conditions in real time.

Strategic Partnerships and R&D Investments

Leading firms are amplifying innovation through collaborations that blend medical expertise with semiconductor technology. Notably, a 2024 alliance between a major health‑technology group and a leading chipmaker has yielded AI edge chips tailored for implantable therapy equipment. Similar joint ventures are focusing on next‑generation display modules and secure connector systems, ensuring compliance with stringent regulatory standards while delivering enhanced performance. These strategic partnerships underline a market trajectory that values co‑development and shared risk, positioning the sector for sustained growth as demand for sophisticated medical devices continues to expand.

COMPETITIVE LANDSCAPE

Key Industry Players

Medical Electronic Components Market – Competitive Overview

Medical Electronic Components Market is dominated by a handful of large integrated device manufacturers that combine deep semiconductor expertise with dedicated healthcare divisions. Medtronic leads the space by supplying power management ICs and sensor modules for implantable therapy devices, while Philips Healthcare and GE Healthcare leverage their imaging platform portfolios to secure long‑term contracts for high‑precision display and sensor solutions. Siemens Healthineers has accelerated its presence through strategic R&D partnerships, notably the 2024 collaboration with Qualcomm on AI‑edge chips that embed advanced analytics directly into diagnostic equipment. This concentration of capabilities creates a tiered structure where a few global giants capture the bulk of high‑value contracts, and smaller specialist firms compete for niche component niches in wearables and point‑of‑care diagnostics.

Beyond the primary tier, several niche players are shaping the market through innovation in miniaturization, low‑power design, and AI integration. Companies such as Analog Devices, Texas Instruments, and STMicroelectronics provide high‑performance mixed‑signal and sensor ICs that power next‑generation patient monitors. Qualcomm and NXP Semiconductors focus on connectivity and edge‑computing modules for tele‑medicine platforms. Meanwhile, TE Connectivity and TDK supply robust connectors and passive components that meet stringent medical safety standards. This diversified ecosystem ensures a steady pipeline of specialized solutions that support overall market growth and technology differentiation.

List of Key Medical Electronic Components Companies Profiled

- Medtronic

- Philips Healthcare

- GE Healthcare

- Siemens Healthineers

- Abbott Laboratories

- Texas Instruments

- Analog Devices

- STMicroelectronics

- NXP Semiconductors

- Qualcomm

- TE Connectivity

- TDK

- Infineon Technologies

- Broadcom

- Maxim Integrated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Sensors

|

| By Application |

|

Patient Monitoring Devices

|

| By End User |

|

Hospitals

|

| By Technology |

|

AI‑Enabled Processing

|

| By Market Trend |

|

Telemedicine Integration

|

Regional Analysis: North America

North America

The North American medical electronic components market is significantly driven by an aging population, increasing prevalence of chronic diseases, and a growing focus on preventative healthcare. Technological advancements in areas like diagnostics, imaging, and therapeutic devices are also key factors propelling market expansion.

Significant trends shaping the North American market include the integration of artificial intelligence (AI) and machine learning (ML) into medical devices, the rise of Internet of Medical Things (IoMT), and increasing adoption of wearable medical technology. These trends are creating new opportunities for component manufacturers to develop and offer innovative solutions.

The North American medical electronic components market is moderately competitive, with a mix of established global players and regional specialists. Key players are focusing on strategic partnerships, product innovation, and expanding their presence in emerging sub-segments to gain a competitive edge.

The future outlook for Medical Electronic Components Market in North America remains positive, with consistent growth expected over the forecast period. Continued innovation, favorable regulatory policies, and increasing healthcare expenditure will further drive market expansion.

Europe

The European medical electronic components market is characterized by a highly regulated environment and a strong emphasis on quality and safety. The region encompasses diverse healthcare systems and varying levels of economic development, influencing market dynamics across different countries. Innovation is a key driver, with significant investment in areas like minimally invasive surgery and advanced diagnostics. The push for sustainable healthcare solutions is also impacting component selection and design.

Asia-Pacific

Asia-Pacific is the fastest-growing market for medical electronic components, driven by increasing healthcare spending, a rising aging population, and expanding access to healthcare services. China, Japan, and India are key contributors to this growth, presenting significant opportunities for component manufacturers. The market is witnessing a shift towards localized manufacturing and a growing demand for cost-effective solutions.

South America

Medical Electronic Components Market in South America is relatively nascent but offers considerable growth potential. Increasing healthcare awareness, rising disposable incomes, and government initiatives to improve healthcare infrastructure are driving demand. The market is characterized by a fragmented distribution network and a focus on basic medical devices.

Middle East & Africa

The Middle East & Africa region presents a unique opportunity for medical electronic components, driven by increasing healthcare investments and a growing prevalence of chronic diseases. The region is witnessing a surge in demand for advanced medical devices and diagnostic equipment, leading to a corresponding increase in the need for sophisticated electronic components.

Report Scope

This market research report provides a comprehensive analysis of the Medical Electronic Components Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Medical Electronic Components Market?

-> Medical Electronic Components Market was valued at USD 14 billion in 2025 and is expected to reach USD 23.6 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period.

Which key companies operate Medical Electronic Components Market?

-> Key players include Medtronic, Philips Healthcare, GE Healthcare, and Siemens Healthineers, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of wearable health‑monitoring devices, expanding tele‑medicine services, increasing demand for compact point‑of‑care diagnostics, and advancements in miniaturization and AI‑enabled processing.

Which region dominates the market?

-> Regional dominance information is not specified in the provided reference.

What are the emerging trends?

-> Emerging trends include miniaturization of components, AI‑enabled edge processing, and integration of IoT capabilities into medical devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...