MARKET INSIGHTS

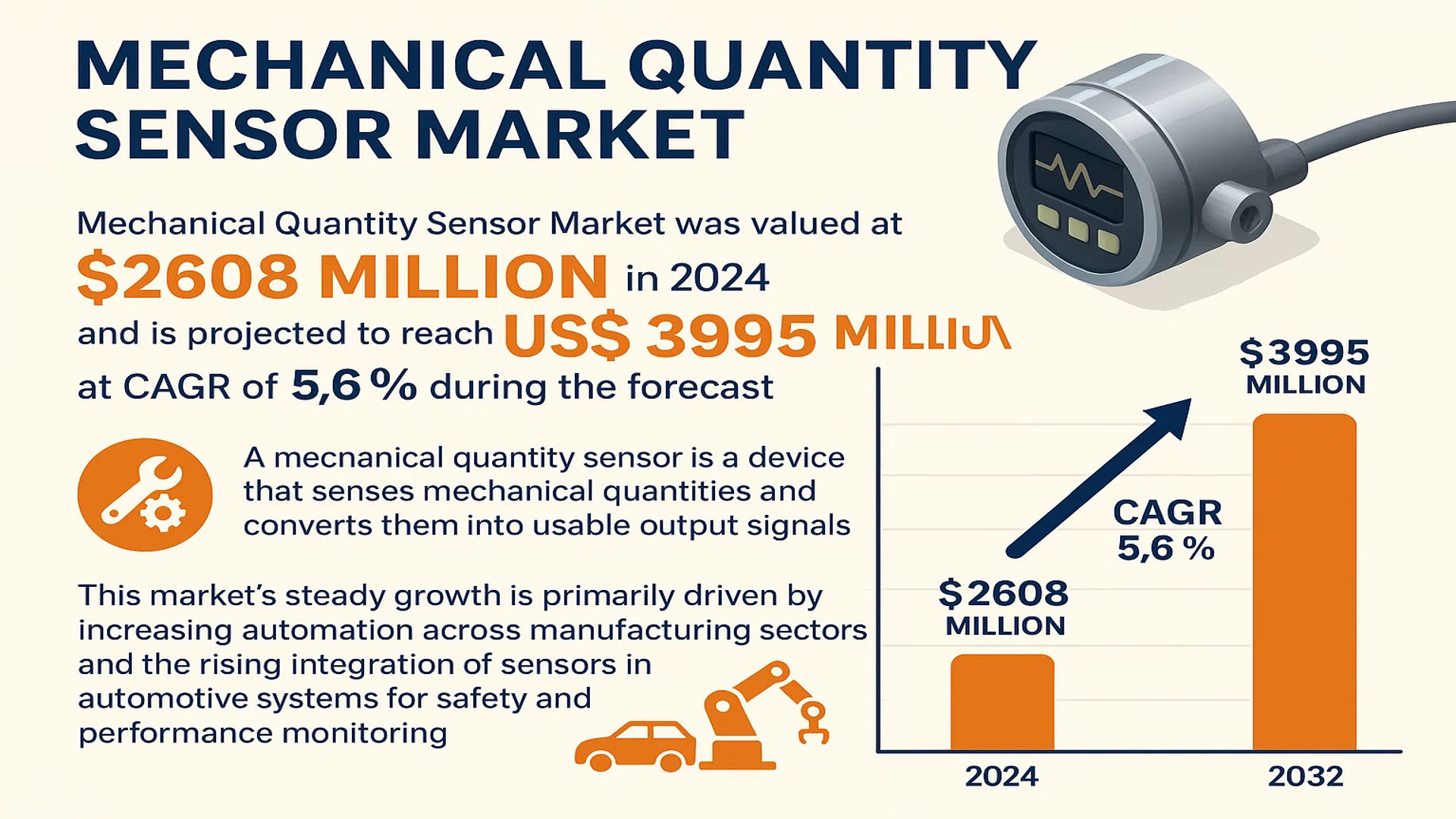

The global Mechanical Quantity Sensor Market was valued at 2608 million in 2024 and is projected to reach US$ 3995 million by 2032, at a CAGR of 5.6% during the forecast.

A mechanical quantity sensor is a device that senses mechanical quantities and converts them into usable output signals. These sensors utilize materials or structures sensitive to mechanical parameters to form their sensing elements, translating measurements of force, torque, pressure, tension, stress, strain, acceleration, angular velocity, vibration, and rotation speed into electrical signals. They are fundamental components within the broader category of physical quantity sensors.

This market’s steady growth is primarily driven by increasing automation across manufacturing sectors and the rising integration of sensors in automotive systems for safety and performance monitoring. Furthermore, the expansion of consumer electronics and the burgeoning robotics industry are creating significant demand. Key players such as TE Connectivity, Honeywell, and Sensata Technologies dominate the landscape, continuously innovating to enhance sensor accuracy, miniaturization, and reliability for diverse applications ranging from industrial control to aerospace.

MARKET DYNAMICS

MARKET DRIVERS

Rising Industrial Automation and Industry 4.0 Adoption to Propel Market Growth

The global push towards industrial automation and smart manufacturing under Industry 4.0 initiatives is significantly driving demand for mechanical quantity sensors. These sensors are critical components in automated systems, providing real-time data on parameters like pressure, force, and vibration to enable precise control and monitoring. Manufacturing facilities worldwide are increasingly integrating IoT-enabled sensors to enhance operational efficiency, reduce downtime, and improve product quality. The industrial automation market is experiencing substantial growth, with investments in smart factory technologies expected to reach unprecedented levels. This trend is particularly strong in regions with advanced manufacturing sectors, where mechanical quantity sensors are essential for maintaining competitive advantage through improved process control and predictive maintenance capabilities.

Expanding Automotive Safety and Electrification Requirements to Boost Demand

The automotive industry’s increasing focus on safety systems and vehicle electrification is creating robust demand for mechanical quantity sensors. Advanced driver assistance systems (ADAS) require precise measurement of various mechanical parameters for functions such as electronic stability control, tire pressure monitoring, and crash detection. The global automotive sensor market continues to grow as regulatory mandates for vehicle safety become more stringent worldwide. Additionally, the transition to electric vehicles necessitates sophisticated sensor systems for battery management, motor control, and thermal management. With electric vehicle production increasing annually, the need for reliable mechanical quantity sensors in automotive applications is expected to maintain strong growth momentum throughout the forecast period.

Growing Aerospace and Defense Applications to Drive Market Expansion

The aerospace and defense sector represents a significant growth driver for mechanical quantity sensors, particularly given increasing investments in aircraft modernization and unmanned systems. These sensors are crucial for monitoring structural health, engine performance, and flight control systems in both commercial and military aircraft. The global aerospace industry is experiencing increased demand for new aircraft, driven by growing air travel and fleet replacement needs. Defense applications require highly reliable sensors for mission-critical systems, including weapons guidance, navigation, and vehicle stabilization. Recent developments in space exploration and satellite technologies further contribute to the expanding application scope for precision mechanical sensors in extreme environments.

MARKET RESTRAINTS

High Development and Manufacturing Costs to Limit Market Penetration

The sophisticated nature of mechanical quantity sensors often results in high development and production costs, which can restrain market growth, particularly in price-sensitive applications. Advanced sensors require specialized materials, precision manufacturing processes, and rigorous testing to ensure reliability and accuracy. These factors contribute to higher product costs that may deter adoption in cost-conscious market segments. Additionally, the need for custom calibration and application-specific design further increases development expenses. While high-performance applications in aerospace and medical sectors can absorb these costs, commercial and consumer applications face greater price sensitivity that may limit market expansion.

Technical Complexity and Integration Challenges to Hinder Adoption

The integration of mechanical quantity sensors into complex systems presents significant technical challenges that can restrain market growth. These sensors often require sophisticated signal conditioning, calibration, and data processing capabilities to deliver accurate measurements. System integrators must address issues such as electromagnetic interference, temperature variations, and mechanical mounting considerations that affect sensor performance. The need for specialized expertise in sensor selection, installation, and maintenance creates additional barriers to adoption, particularly for small and medium-sized enterprises with limited technical resources. Furthermore, compatibility issues with existing systems and the requirement for customized solutions can delay implementation and increase overall project costs.

Intense Competition and Price Pressure to Impact Profitability

The mechanical quantity sensor market faces intense competition from both established players and new entrants, leading to significant price pressure that can restrain market growth. Numerous manufacturers compete across various sensor types and applications, creating a highly fragmented competitive landscape. This competition often drives prices downward, particularly for standard sensor types with lower technical differentiation. Price pressure is especially pronounced in consumer electronics and automotive applications, where cost reduction is a continuous requirement. While innovation and technological advancement continue, the need to maintain competitive pricing can limit research and development investments and impact overall market profitability.

MARKET CHALLENGES

Maintaining Measurement Accuracy Under Harsh Operating Conditions

Mechanical quantity sensors frequently operate in challenging environments that can compromise measurement accuracy and reliability. Extreme temperatures, high vibration, corrosive atmospheres, and electromagnetic interference present significant challenges for sensor performance. Industrial applications often expose sensors to conditions that can cause drift, hysteresis, or complete failure if not properly addressed. The automotive industry particularly faces challenges with sensors operating across temperature ranges from sub-zero to elevated temperatures while maintaining precision. Developing sensors that can withstand these conditions without compromising performance requires advanced materials, sophisticated compensation techniques, and robust packaging solutions that increase complexity and cost.

Other Challenges

Miniaturization Requirements

The ongoing trend toward smaller and more compact devices creates challenges in sensor design and manufacturing. Miniaturization often conflicts with performance requirements, as smaller sensors may have reduced sensitivity or increased susceptibility to environmental factors. Consumer electronics and medical devices particularly demand increasingly smaller sensors without compromising accuracy or reliability, presenting significant engineering challenges that require innovative solutions and advanced manufacturing techniques.

Calibration and Maintenance Demands

Mechanical quantity sensors require regular calibration and maintenance to ensure ongoing accuracy, creating operational challenges for end-users. The need for specialized calibration equipment and trained personnel can be particularly challenging for organizations with distributed operations or limited technical resources. Additionally, the trend toward networked sensors in IoT applications increases the complexity of maintaining calibration across large sensor arrays, requiring sophisticated management systems and protocols.

MARKET OPPORTUNITIES

Emerging IoT and Smart City Applications to Create New Growth Avenues

The expansion of Internet of Things applications and smart city initiatives presents substantial opportunities for mechanical quantity sensor manufacturers. Smart infrastructure projects worldwide are incorporating sensors for structural health monitoring, traffic management, and environmental monitoring. These applications require reliable mechanical quantity sensors to measure parameters such as vibration, pressure, and strain in civil structures, transportation systems, and utility networks. The growing investment in smart city technologies globally creates a expanding market for sensors that can provide long-term, reliable performance in diverse outdoor environments with minimal maintenance requirements.

Advancements in MEMS Technology to Enable New Applications

Recent advancements in Micro-Electro-Mechanical Systems technology are creating new opportunities for mechanical quantity sensors in previously inaccessible applications. MEMS-based sensors offer advantages in size, cost, and power consumption while maintaining high performance levels. These technological improvements are enabling new applications in wearable devices, medical implants, and consumer electronics where traditional sensors were previously unsuitable. The continued innovation in MEMS fabrication techniques and materials science is expected to further expand the application range for mechanical quantity sensors while reducing costs through mass production capabilities.

Growing Renewable Energy Sector to Drive Sensor Demand

The rapidly expanding renewable energy sector represents a significant growth opportunity for mechanical quantity sensors. Wind turbine applications require sophisticated sensors for condition monitoring, blade pitch control, and structural health assessment. Solar tracking systems utilize sensors for position and force feedback to optimize energy capture. The global transition toward renewable energy sources is driving increased investment in these technologies, creating sustained demand for reliable mechanical quantity sensors capable of operating in demanding environmental conditions while providing accurate measurements over extended periods.

MECHANICAL QUANTITY SENSOR MARKET TRENDS

Integration of IoT and Industry 4.0 Drives Demand for Smart Sensing Solutions

The proliferation of the Internet of Things (IoT) and the global shift towards Industry 4.0 are fundamentally reshaping the mechanical quantity sensor landscape. These sensors are increasingly being embedded with connectivity features, enabling real-time data acquisition, remote monitoring, and predictive maintenance capabilities. In smart manufacturing environments, for instance, connected force and torque sensors facilitate condition-based monitoring of critical machinery, drastically reducing unplanned downtime. The global market for industrial IoT is projected to exceed $1.1 trillion by 2028, a growth trajectory that directly fuels the adoption of intelligent mechanical sensors. This trend is further accelerated by the development of low-power, wireless sensor nodes that can operate for extended periods in harsh industrial settings, transmitting vital data on vibration, pressure, and strain to centralized control systems for analysis and actionable insights.

Other Trends

Miniaturization and Enhanced Precision

A significant and persistent trend is the relentless drive towards miniaturization without compromising on performance. This is particularly critical in sectors like consumer electronics, medical devices, and advanced robotics, where space constraints are paramount. The development of Micro-Electro-Mechanical Systems (MEMS) technology has been a cornerstone of this evolution, allowing for the production of sensors that are not only incredibly small but also offer high accuracy, low power consumption, and cost-effectiveness. For example, MEMS-based accelerometers and pressure sensors are now ubiquitous in smartphones, wearables, and automotive safety systems. This trend is pushing the boundaries of what’s possible, enabling new applications in minimally invasive surgical instruments and compact industrial automation equipment where precise measurement in a tiny form factor is essential.

Expansion in Automotive and Robotics Applications

The automotive and robotics industries are emerging as powerhouse drivers for the mechanical quantity sensor market. The transition to electric and autonomous vehicles requires a sophisticated network of sensors for functions ranging from battery management system monitoring (pressure, temperature) to advanced driver-assistance systems (ADAS) that rely on inertial measurement units for stability control. Similarly, the robotics revolution, encompassing everything from industrial arms to collaborative robots (cobots) and service robots, is heavily dependent on force, torque, and tactile sensors. These sensors provide the essential feedback for safe human-robot interaction, precise object manipulation, and accurate navigation. With the industrial robotics market itself expected to surpass $95 billion by 2028, the demand for high-performance mechanical quantity sensors integrated into these systems is experiencing a corresponding and substantial surge.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership

The global mechanical quantity sensor market exhibits a fragmented yet dynamic competitive structure, characterized by the presence of multinational conglomerates, specialized sensor manufacturers, and emerging regional players. TE Connectivity and Honeywell International Inc. are recognized as dominant forces, leveraging their extensive product portfolios that span multiple sensor types—including strain gauge, piezoresistive, and capacitive technologies—and their entrenched relationships across the automotive, industrial automation, and aerospace sectors. Their global distribution networks and consistent investment in research and development solidify their leading positions.

Similarly, Sensata Technologies and HBK (Hottinger Brüel & Kjær, part of Spectris) command significant market share, primarily due to their deep application expertise and focus on high-precision measurement solutions. Sensata’s stronghold in automotive sensing and HBK’s leadership in test and measurement applications provide them with resilient, diversified revenue streams. Their growth is further propelled by strategic acquisitions and continuous product innovation aimed at meeting evolving industry standards for accuracy and reliability.

Meanwhile, several other established players are aggressively expanding their market influence. Companies like Kistler Group and Vishay Precision Group (VPG) are focusing on technological differentiation, particularly in piezoelectric and advanced strain gauge sensors, catering to niche but high-value applications in manufacturing and process control. Their strategy involves not only product development but also forging partnerships with OEMs to integrate sensors into smarter, more connected systems.

The competitive environment is further intensified by the activities of firms such as Amphenol Corporation and Panasonic Corporation, who are strengthening their market presence through significant investments in MEMS (Micro-Electro-Mechanical Systems) technology and IoT-enabled sensor solutions. Their efforts are concentrated on enhancing sensor miniaturization, energy efficiency, and connectivity features, which are increasingly critical in consumer electronics, robotics, and new energy applications. Because these sectors demand sensors that can operate in compact spaces and communicate seamlessly with other devices, innovation in integration and functionality becomes a key competitive battleground.

Additionally, regional specialists like WIKA Group in pressure measurement and Keli Sensing Technology (Ningbo) in strain gauge sensors are expanding their global footprint through targeted geographical expansions and by tailoring products to meet local regulatory and performance requirements. Their growth underscores the importance of understanding regional market nuances and building a responsive, localized supply chain.

Overall, competition is expected to further intensify over the coming years, driven by the accelerating adoption of industrial automation, electric vehicles, and smart infrastructure. Market participants are consequently prioritizing strategies that encompass not only product innovation and portfolio diversification but also sustainability initiatives and the development of cost-effective solutions for price-sensitive markets.

List of Key Companies Profiled

- TE Connectivity (Switzerland)

- Honeywell International Inc. (U.S.)

- Sensata Technologies (U.S.)

- HBK (Spectris) (U.K.)

- Kistler Group (Switzerland)

- Vishay Precision Group (VPG) (U.S.)

- Amphenol Corporation (U.S.)

- Panasonic Corporation (Japan)

- WIKA Group (Germany)

- MinebeaMitsumi Inc. (Japan)

- Nissha Co., Ltd. (Japan)

- Novanta Inc. (U.S.)

- Flintec AB (Sweden)

- Futek Advanced Sensor Technology, Inc. (U.S.)

- Tekscan, Inc. (U.S.)

- Keli Sensing Technology (Ningbo) Co., Ltd. (China)

- ZEMIC Europe GmbH (Germany)

- Memsensing Microsystems (Suzhou) Co., Ltd. (China)

Segment Analysis:

By Type

Piezoresistive Type Segment Leads the Market Due to High Reliability and Cost-Effectiveness Across Industrial Applications

The market is segmented based on type into:

- Strain Gauge Type

- Piezoresistive Type

- Piezoelectric Type

- Capacitive Type

- Others

By Application

Automotive Segment Holds Significant Share Owing to Extensive Use in Vehicle Safety Systems and Powertrain Management

The market is segmented based on application into:

- Industrial Control

- Automobile

- Consumer Electronics

- Medical

- Aerospace

- Others

By End-User Industry

Manufacturing Sector Represents a Major End-User Driven by Automation and Precision Measurement Needs

The market is segmented based on end-user industry into:

- Automotive Manufacturing

- Industrial Equipment Manufacturing

- Aerospace and Defense

- Electronics and Semiconductors

- Healthcare and Medical Devices

- Others

Regional Analysis: Mechanical Quantity Sensor Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global mechanical quantity sensor market, accounting for over 45% of global consumption by volume. This dominance is fueled by the massive manufacturing ecosystems in China, Japan, and South Korea, which are heavily reliant on industrial automation and robotics. China’s “Made in China 2025” initiative continues to drive significant investment in advanced manufacturing equipment, all of which require precise force, pressure, and torque sensing. Furthermore, the region’s booming consumer electronics sector, led by giants in smartphone and wearable production, creates immense demand for miniaturized sensors, particularly capacitive and piezoresistive types. While cost-competition remains fierce, local manufacturers are rapidly advancing their technological capabilities, challenging established international players and making the region both the largest consumer and a formidable production hub.

North America

Characterized by its focus on high-value, technologically advanced applications, the North American market is a hub for innovation. Stringent safety regulations, especially in the automotive and aerospace sectors, mandate the use of highly reliable sensors for crash testing, structural health monitoring, and precision control systems. The region’s strong aerospace and defense industry, supported by entities like NASA and major defense contractors, demands sensors capable of operating in extreme environments, driving development in piezoelectric and advanced strain gauge technologies. Additionally, the ongoing push for industrial IoT and smart manufacturing under initiatives like the Advanced Manufacturing Partnership (AMP) is accelerating the adoption of intelligent, connected sensors that provide predictive maintenance data, making North America a critical market for premium, high-performance solutions.

Europe

The European market is driven by a combination of robust automotive engineering, strict industrial standards, and a growing emphasis on sustainability. Germany, as the heart of the European automotive industry, is a major consumer of sensors for engine management, transmission systems, and vehicle testing. The region’s commitment to industrial excellence, encapsulated in frameworks like Industry 4.0, promotes the integration of smart sensors into automated production lines for quality control and efficiency. Furthermore, environmental directives push for more efficient machinery and renewable energy systems, such as wind turbines, which utilize large-scale load and torque sensors for optimal performance. European manufacturers are often leaders in precision and calibration, focusing on high-accuracy applications in medical devices and scientific instrumentation, which supports a stable demand for top-tier sensor products.

South America

The market in South America is emerging, with growth primarily tied to the region’s industrial and agricultural equipment manufacturing sectors. Countries like Brazil and Argentina have significant automotive and machinery industries that require mechanical quantity sensors for production and product integration. However, the market’s expansion is often tempered by economic volatility, which can delay capital expenditure on new manufacturing technology and limit the adoption of advanced sensor systems. While there is a baseline demand for essential sensors in industrial maintenance and basic automation, the widespread penetration of high-end, connected sensor solutions is slower compared to more developed regions. Nonetheless, long-term industrial development plans present a gradual growth opportunity for sensor suppliers.

Middle East & Africa

This region represents a developing market with potential tied to infrastructure development and industrialization efforts. Key growth areas include the oil & gas sector, where sensors are critical for downstream processing equipment and pipeline monitoring, and construction, where equipment manufacturing requires basic sensing capabilities. Nations in the Gulf Cooperation Council (GCC), such as Saudi Arabia and the UAE, are investing in economic diversification plans that include building advanced manufacturing capabilities, which could spur future demand. However, the current market size is relatively small, and progress is often constrained by a focus on commodity exports rather than high-value manufacturing. The adoption of sophisticated sensor technology is therefore incremental, with growth expected to be steady but slower than in global leading regions.

Report Scope

This market research report provides a comprehensive analysis of the global Mechanical Quantity Sensor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mechanical Quantity Sensor Market?

-> Mechanical Quantity Sensor Market was valued at 2608 million in 2024 and is projected to reach US$ 3995 million by 2032, at a CAGR of 5.6% during the forecast.

Which key companies operate in Global Mechanical Quantity Sensor Market?

-> Key players include Sensata Technologies, TE Connectivity, Honeywell, Amphenol, and Panasonic, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation, automotive electrification, robotics adoption, and increasing demand for precision measurement in manufacturing.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 45% of global revenue in 2024, driven by manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with IoT platforms, development of MEMS-based sensors, and increasing adoption in renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...