MARKET INSIGHTS

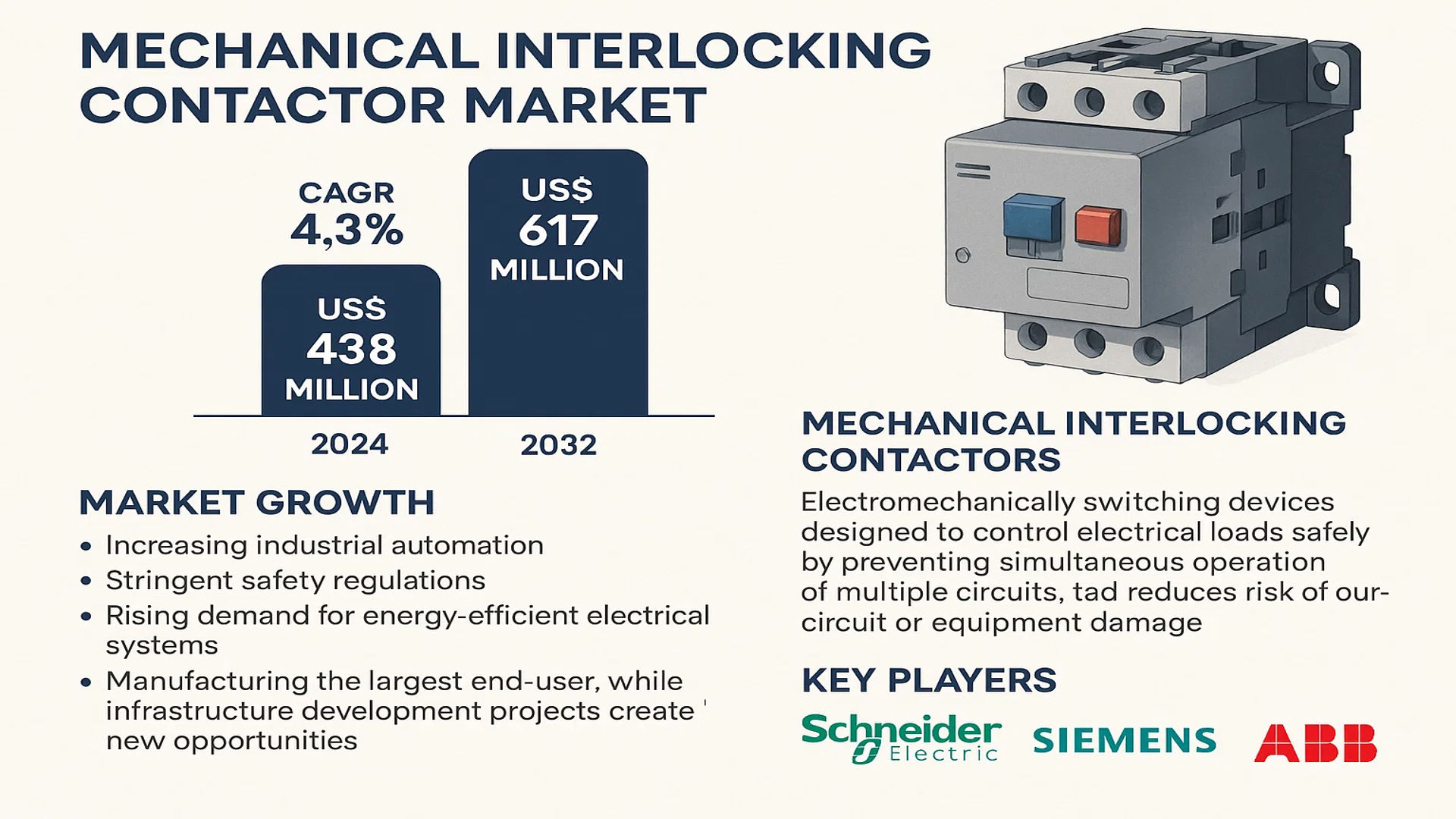

The global Mechanical Interlocking Contactor Market size was valued at US$ 438 million in 2024 and is projected to reach US$ 617 million by 2032, at a CAGR of 4.3% during the forecast period 2025-2032.

Mechanical interlocking contactors are electromechanical switching devices designed to control electrical loads safely by preventing simultaneous operation of multiple circuits. These devices incorporate a physical interlock mechanism that ensures only one contactor can be engaged at a time, reducing the risk of short circuits or equipment damage. They are widely used in industrial motor control, lighting systems, and power distribution applications.

The market growth is driven by increasing industrial automation, stringent safety regulations, and rising demand for energy-efficient electrical systems. While the manufacturing sector remains the largest end-user, infrastructure development projects are creating new opportunities. Key players like Schneider Electric, Siemens, and ABB are investing in smart contactor technologies with IoT integration, further accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Industrial Automation Boom Accelerates Demand for Reliable Electromechanical Components

The global push toward industrial automation continues to drive significant growth in the mechanical interlocking contactor market, with manufacturing sectors increasingly adopting these critical components to enhance operational efficiency. Recent data shows that automation investments in discrete manufacturing sectors have grown at a compound annual rate of over 10% since 2020, creating sustained demand for contactors that can withstand rigorous industrial environments. Mechanical interlocking contactors play a vital role in automation systems by preventing hazardous simultaneous operation of incompatible circuits, making them indispensable for safety-critical applications ranging from assembly lines to material handling systems.

Stringent Safety Regulations Propel Market Adoption

Heightened focus on workplace safety standards across industries is compelling companies to upgrade their electrical infrastructure with compliant components. Mechanical interlocking contactors help organizations meet rigorous international standards such as IEC 60947-4-1 and UL 508 by providing fail-safe operation against accidental contact closure. The implementation of these safety measures has become particularly crucial in high-risk sectors like oil & gas and mining, where electrical incidents can have catastrophic consequences. Regulatory bodies continue to tighten equipment certification requirements, creating a sustained replacement cycle for older contactor systems that cannot meet modern safety benchmarks.

➤ For instance, recent updates to NFPA 70E regulations have mandated more rigorous arc flash prevention measures in industrial settings, directly increasing the need for properly interlocked contactor solutions.

Furthermore, the growing complexity of industrial control systems has made mechanical interlocks essential for preventing operational errors in multi-motor applications. This trend is particularly evident in sectors like water treatment and power generation, where precise sequencing of equipment activation is critical to system integrity.

MARKET RESTRAINTS

High Installation and Maintenance Costs Limit Market Penetration

While mechanical interlocking contactors offer superior reliability, their complex installation requirements and maintenance needs create barriers to wider adoption, particularly in cost-sensitive markets. The total cost of ownership for these systems can be 20-30% higher than standard contactor solutions when factoring in specialized mounting hardware and periodic alignment checks. This pricing pressure is particularly acute in developing regions where budget constraints lead many operators to opt for less sophisticated alternatives despite the safety trade-offs.

Other Constraints

Space Constraints in Compact Control Panels

Modern industrial control cabinets are being designed with increasingly dense footprints to save space, creating compatibility challenges for traditional mechanical interlock solutions. The physical bulk of interlocking mechanisms often conflicts with the push for minimized panel sizes, forcing compromises in either functionality or spatial efficiency.

Limited Flexibility in System Modifications

Unlike their electronic counterparts, mechanically interlocked contactors require physical reconfiguration when control logic needs adjustment. This limitation makes them less adaptable to production line changes or process improvements, slowing their adoption in dynamic manufacturing environments where layout flexibility is prioritized.

MARKET CHALLENGES

Transition to Smart Manufacturing Creates Compatibility Issues

The rapid emergence of Industry 4.0 technologies presents integration challenges for traditional mechanical interlocking systems. As factories implement IoT-enabled devices and predictive maintenance systems, legacy mechanical solutions struggle to provide the digital feedback loops required by modern monitoring platforms. This technological gap is prompting many operators to consider electronic alternatives despite the mechanical versions’ proven reliability advantages in basic safety applications.

Additionally, the lack of standardization across manufacturers creates interoperability issues, with different brands frequently using proprietary interlock mechanisms that prevent mixing components. This vendor lock-in effect limits procurement flexibility and complicates replacement part sourcing, particularly for older systems where original components may no longer be available.

MARKET OPPORTUNITIES

Modernization of Aging Industrial Infrastructure Presents Growth Potential

The urgent need to upgrade obsolete electrical systems in developed economies represents a significant opportunity for mechanical interlocking contactor manufacturers. Many industrial facilities in North America and Europe continue to operate with contactors installed 20-30 years ago, creating a substantial replacement market as these components reach end-of-life. The superior mechanical durability of modern interlocking contactors, with lifespans exceeding 1 million operations in some models, makes them particularly attractive for these upgrade projects.

The renewable energy sector also offers promising growth avenues, as solar farms and wind turbine installations require robust contactor solutions capable of withstanding harsh environmental conditions. Mechanical interlocks provide particular value in these applications by ensuring fail-safe operation of critical power routing functions where electronic controls might be vulnerable to electromagnetic interference or extreme temperatures.

MECHANICAL INTERLOCKING CONTACTOR MARKET TRENDS

Industrial Automation Boom Drives Demand for Mechanical Interlocking Contactors

The global mechanical interlocking contactor market is experiencing robust growth due to accelerating industrial automation across manufacturing, power generation, and infrastructure sectors. As industries prioritize operational efficiency, mechanical interlocking contactors have become essential components in motor control centers and power distribution systems, ensuring safe switching between circuits. The market is projected to grow at a compound annual growth rate of over 5% during the forecast period, reaching a valuation of several billion dollars by 2032. Manufacturing facilities account for the largest application segment, followed by energy distribution systems, where these devices prevent dangerous cross-connections between power sources.

Other Trends

Safety Standards Compliance

Stringent safety regulations in electrical systems worldwide are significantly influencing product development in the mechanical interlocking contactor space. New IEC and UL certifications require contactors to withstand higher voltages while minimizing arcing risks, pushing manufacturers to innovate with durable arc-quenching materials. Thermal management has become a critical design consideration, with leading suppliers introducing contactors capable of handling currents up to 800A without performance degradation. This focus on reliability aligns with industrial needs for maintenance-free operation in harsh environments.

Energy Efficiency Requirements Reshape Product Designs

The push toward sustainable operations has driven adoption of energy-efficient contactor models that reduce power losses by up to 30% compared to conventional designs. Modern mechanical interlocking systems now incorporate low-power holding coils and optimized magnetic circuits to meet stringent energy codes. Manufacturers are also expanding production of dustproof and waterproof enclosures rated IP65 or higher, addressing demand from renewable energy installations and outdoor industrial applications. Asia-Pacific represents the fastest-growing regional market, with China accounting for nearly 40% of global demand due to rapid industrialization and smart grid deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

Industrial Automation Giants Compete Through Innovation and Reliability

The global mechanical interlocking contactor market features a competitive landscape dominated by established electrical component manufacturers, with several emerging players gaining traction through specialized solutions. Schneider Electric and Siemens collectively hold approximately 35% market share as of 2024, leveraging their extensive distribution networks and reputation for high-reliability industrial components. These companies maintain leadership through continuous R&D investments, with Siemens alone allocating over €5.2 billion annually to industrial automation innovations.

ABB and Eaton have significantly strengthened their market position through strategic acquisitions and product diversification. ABB’s acquisition of Cylon Controls in 2023 enhanced its building automation capabilities, while Eaton’s 2022 purchase of a 50% stake in Jiangsu YiNENG Electric intensified competition in the Asia-Pacific contactor market. Both companies now offer integrated solutions combining mechanical interlocking with digital monitoring capabilities, addressing growing demand for smart industrial components.

Meanwhile, regional players like Chint (China) and LS Industrial Systems (South Korea) are rapidly expanding internationally. Chint reported 18% year-over-year growth in electromechanical component sales in 2023, capitalizing on cost advantages and localized support networks. These companies are increasingly challenging established players in developing markets where price sensitivity remains high.

The market also sees active participation from specialized manufacturers such as WEG Industries (Brazil) and TONGOU (China), who focus on niche applications like marine and mining equipment. WEG’s 2023 product recall incident demonstrated the critical importance of quality control in this sector, prompting industry-wide reassessments of manufacturing standards.

List of Key Mechanical Interlocking Contactor Manufacturers

- Schneider Electric (France)

- ABB (Switzerland)

- Siemens (Germany)

- Eaton Corporation (U.S.)

- Legrand (France)

- Galco Industrial Electronics (U.S.)

- Chint Group (China)

- LS Industrial Systems (South Korea)

- WEG Industries (Brazil)

- TONGOU Electric (China)

- Clipsal (Australia)

- Suntree Electric (China)

- CNC Electric (China)

- CHKO (China)

Segment Analysis:

By Type

AC Contactors Segment Dominates Due to Widespread Industrial Applications

The market is segmented based on type into:

- AC Contactors

- DC Contactors

By Application

Industrial Motor Segment Leads in Adoption Due to Automation Requirements

The market is segmented based on application into:

- Industrial Motor

- Lighting Control

- Other

By End User

Manufacturing Sector Dominates Usage for Safety-Critical Operations

The market is segmented based on end user into:

- Manufacturing

- Energy and Utilities

- Construction

- Transportation

- Others

By Safety Standard

IEC-Compliant Products Show Higher Adoption in Global Markets

The market is segmented based on safety standard into:

- IEC Standards

- UL Standards

- Other Regional Standards

Regional Analysis: Mechanical Interlocking Contactor Market

Asia-Pacific

The Asia-Pacific region dominates the mechanical interlocking contactor market, accounting for over 40% of global demand in 2024, driven by rapid industrialization in China, India, and Southeast Asian nations. The region’s strong manufacturing base, particularly in automotive, consumer electronics, and heavy industries, fuels the need for robust motor control solutions. China’s “Made in China 2025” initiative boosts automation investments, while India’s growing infrastructure projects create parallel demand. However, price sensitivity in emerging markets limits premium product adoption, favoring domestic manufacturers offering cost-competitive alternatives to Western brands.

North America

North America holds the second-largest market share, characterized by stringent safety standards (UL, NEC) and advanced industrial automation. The U.S. accounts for nearly 70% of regional demand, with Canada following at 20%. Key drivers include factory modernization under the Inflation Reduction Act and reshoring of manufacturing. The region shows strong preference for smart contactors with IoT integration, though high manufacturing costs and skilled labor shortages pose challenges. Major players like Eaton and Schneider Electric lead innovation with energy-efficient solutions for data centers and renewable energy applications.

Europe

Europe’s mature market emphasizes energy efficiency and compliance with IEC standards, particularly in Germany, France, and Italy which together contribute 65% of regional sales. The EU’s focus on Industry 4.0 and sustainable manufacturing accelerates replacement of legacy systems with advanced contactors. Strict regulations like RoHS and REACH impact material sourcing, increasing production costs. While Western Europe shows steady growth, Eastern Europe emerges as a manufacturing hub with lower-cost alternatives. The region faces intensifying competition from Asian suppliers offering similar specifications at 20-30% lower prices.

South America

The South American market remains nascent but displays 5-7% annual growth potential, led by Brazil’s industrial sector and mining operations. Infrastructure development in Argentina and Chile creates opportunities, though economic instability and import dependencies hinder market expansion. Price competition is fierce, with Chinese and local brands capturing over 50% market share. Limited technical expertise in rural areas restricts adoption of sophisticated systems, keeping demand focused on basic mechanical interlocking functionality for motor control applications.

Middle East & Africa

This region shows fragmented demand, with UAE, Saudi Arabia, and South Africa accounting for 60% of regional consumption. Oil & gas projects drive premium product demand, while construction sectors rely on mid-range solutions. Africa’s market remains underpenetrated due to infrastructure gaps, though initiatives like Nigeria’s industrial growth plan show promise. The lack of local manufacturing forces reliance on imports, creating supply chain vulnerabilities. While growth lags other regions, strategic investments in smart cities and energy projects present long-term opportunities for contactor suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Mechanical Interlocking Contactor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (AC Contactors, DC Contactors), application (Industrial Motor, Lighting Control, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of smart controls, safety standards compliance, and evolving industry regulations.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mechanical Interlocking Contactor Market?

-> Mechanical Interlocking Contactor Market size was valued at US$ 438 million in 2024 and is projected to reach US$ 617 million by 2032, at a CAGR of 4.3% during the forecast period 2025-2032.

Which key companies operate in Global Mechanical Interlocking Contactor Market?

-> Key players include Schneider Electric, ABB, Siemens, Eaton, WEG Industries, and Legrand, among others, which collectively hold over 60% of the market share.

What are the key growth drivers?

-> Key growth drivers include industrial automation trends, increasing demand for safety-compliant electrical components, and expansion of manufacturing infrastructure globally.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (38% in 2024), driven by rapid industrialization in China and India, while North America leads in technological advancements.

What are the emerging trends?

-> Emerging trends include integration with IoT for remote monitoring, development of compact and energy-efficient models, and increased focus on modular contactor designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...