MARKET INSIGHTS

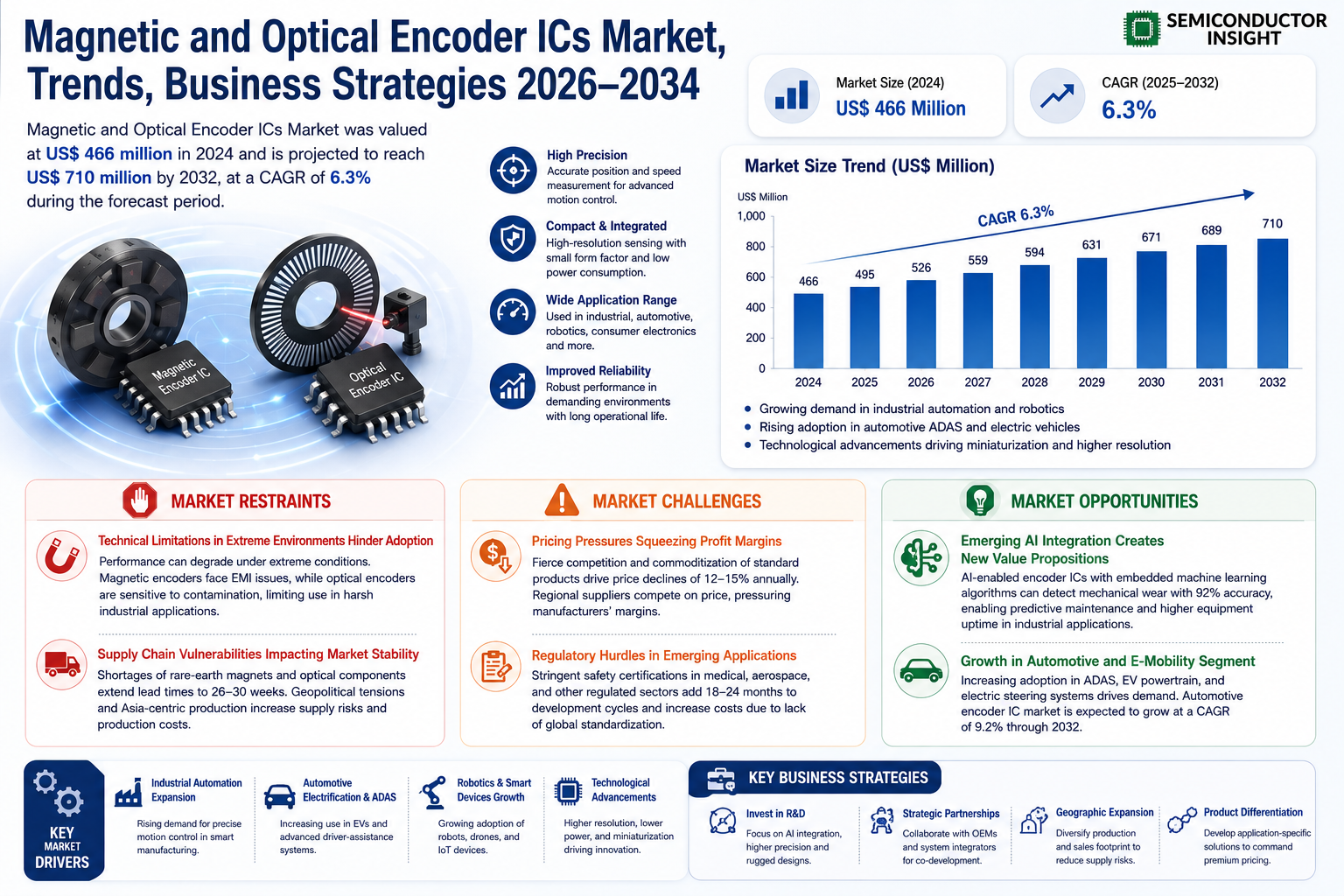

The global Magnetic and Optical Encoder ICs Market was valued at 466 million in 2024 and is projected to reach US$ 710 million by 2032, at a CAGR of 6.3% during the forecast period.

Encoder ICs are critical sensing components that convert mechanical motion into electrical signals for precise position, speed, and direction feedback in motion control systems. These integrated circuits come in two primary technologies: magnetic encoder ICs which detect magnetic field variations, and optical encoder ICs that use light patterns for position sensing. Both types play vital roles across industries requiring high-accuracy motion control.

Market growth is being driven by increasing automation across manufacturing sectors, rising demand for precision motion control in robotics and medical equipment, and the expanding electric vehicle market. The semiconductor industry’s overall growth – projected to reach USD 790 billion by 2029 at 6% CAGR – provides a strong foundation, though encoder ICs are growing faster than the broader market. Key players like Broadcom, AMS, and TE Connectivity are investing in advanced encoder technologies to meet evolving industry requirements for smaller form factors and higher resolution.

MARKET DYNAMICS

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation to Fuel Magnetic and Optical Encoder IC Demand

The global industrial automation sector, valued at over $200 billion in 2024, is accelerating the adoption of precision motion control systems where encoder ICs play a pivotal role. As factories transition towards Industry 4.0 standards, the need for accurate position feedback in robotics, CNC machines, and automated assembly lines has grown exponentially. Magnetic encoder ICs are particularly gaining traction due to their durability in harsh environments, with shipments projected to increase by 8.2% annually through 2030. This trend is reinforced by growing investments in smart manufacturing across major economies like China, Germany, and the U.S.

Electric Vehicle Production Boom Creating New Growth Avenues

The electric vehicle revolution is generating significant demand for encoder ICs in motor control applications. With global EV sales expected to surpass 40 million units annually by 2030, the need for precise rotor position sensing in traction motors presents substantial opportunities. Optical encoder ICs are being widely adopted in high-performance EV drivetrains due to their superior resolution, while magnetic variants dominate in auxiliary systems where ruggedness is prioritized. Automakers are increasingly collaborating with semiconductor manufacturers to develop specialized encoder solutions that meet the stringent requirements of next-generation electric powertrains.

IoT Proliferation Driving Miniaturized Encoder Solutions

The Internet of Things ecosystem is creating demand for compact, energy-efficient encoder ICs across consumer and industrial applications. Emerging use cases in smart home appliances, wearable devices, and edge computing equipment require encoder solutions that balance performance with power efficiency. This has led to innovations in encoder packaging technologies, with chip-scale packages now accounting for 35% of total shipments in the consumer electronics segment. Furthermore, the integration of encoder ICs with wireless communication protocols enables real-time monitoring capabilities that align with Industry 4.0 requirements.

MARKET RESTRAINTS

Technical Limitations in Extreme Environments Hinder Adoption

While encoder ICs offer significant advantages, their performance can degrade under extreme operating conditions. Magnetic encoders face challenges in environments with strong electromagnetic interference, potentially causing signal distortion. Optical variants are particularly sensitive to contamination, with particulate matter reducing accuracy by up to 30% in industrial settings. These technical constraints limit application in sectors like oil & gas and heavy manufacturing, where alternative solutions remain preferred despite higher costs. Ongoing R&D efforts focus on advanced shielding techniques and sealed packaging to address these limitations.

Supply Chain Vulnerabilities Impacting Market Stability

The semiconductor industry’s ongoing supply chain challenges continue to affect encoder IC availability. Specialized materials like rare-earth magnets and high-grade optical components face periodic shortages, with lead times extending to 26-30 weeks for certain product categories. Geopolitical tensions further complicate procurement strategies, as over 60% of encoder IC production remains concentrated in Asia. Manufacturers are responding by diversifying sourcing strategies and increasing safety stock levels, but these measures contribute to higher production costs that may ultimately impact end-market pricing.

MARKET CHALLENGES

Pricing Pressures Squeezing Profit Margins

Intense competition in the encoder IC market is driving aggressive price competition, particularly in standardized product categories. Average selling prices for basic magnetic encoder ICs have declined by 12-15% annually since 2020, forcing manufacturers to focus on value-added features to maintain profitability. The commoditization of entry-level products has been accelerated by the emergence of regional suppliers in China and Southeast Asia, who compete primarily on price. Industry leaders are responding by focusing on proprietary technologies and custom solutions that command premium pricing in specialized applications.

Regulatory Hurdles in Emerging Applications

As encoder ICs penetrate regulated industries like medical devices and aerospace, compliance requirements are becoming increasingly stringent. New safety certifications for critical applications can add 18-24 months to product development cycles, delaying time-to-market. The lack of global standardization in functional safety requirements further increases certification costs, particularly for manufacturers serving multiple geographic markets. These regulatory challenges are prompting strategic partnerships between encoder IC suppliers and end-users to jointly develop compliant solutions from initial design stages.

MARKET OPPORTUNITIES

Emerging AI Integration Creates New Value Propositions

The integration of artificial intelligence with encoder systems is opening new frontiers in predictive maintenance and performance optimization. Smart encoder ICs equipped with embedded machine learning algorithms can detect mechanical wear patterns with 92% accuracy – significantly improving equipment uptime in industrial settings. This capability is generating premium pricing opportunities, with AI-enabled encoder solutions commanding 30-40% higher margins than conventional products. Manufacturers are investing heavily in edge computing capabilities to bring intelligence closer to the point of data generation.

Renewable Energy Sector Presents Untapped Potential

The global transition to renewable energy is creating substantial demand for encoder solutions in wind turbines and solar tracking systems. Wind energy applications alone are projected to require 8 million encoder units annually by 2028, driven by maintenance cycle optimizations and new turbine installations. These applications demand extreme reliability, with operational lifespans exceeding 20 years in harsh environmental conditions. Encoder manufacturers are developing specialized products with enhanced corrosion resistance and reduced component count to meet these rigorous requirements while maintaining cost competitiveness.

MAGNETIC AND OPTICAL ENCODER ICS MARKET TRENDS

Automation and Robotics Adoption Driving Market Expansion

The increasing adoption of automation technologies and robotics across multiple industries is significantly elevating the demand for magnetic and optical encoder ICs. These components provide critical motion feedback in industrial automation, robotics, and servo systems, ensuring precision and reliability. The global industrial automation market is projected to grow at a compound annual growth rate (CAGR) of nearly 8% through 2030, with Asia-Pacific leading due to rapid industrialization. Encoder ICs are increasingly being used in collaborative robots (cobots), assembly line automation, and CNC machines, where high-resolution position detection is essential. Furthermore, the shift toward smart manufacturing (Industry 4.0) has accelerated investments in sensor technologies, contributing to the growing encoder IC market.

Other Trends

Rising Demand in Automotive and Electric Vehicles

The automotive sector is experiencing a surge in demand for encoder ICs, primarily due to advancements in electric vehicles (EVs) and autonomous driving systems. Position sensing in EVs, particularly for motor control and battery management, relies heavily on high-precision magnetic encoders. With global EV sales expected to surpass 17 million units annually by 2028, the market for encoder ICs in this segment is poised for sustained growth. Additionally, optical encoders are widely used in advanced driver-assistance systems (ADAS), where they enhance sensor feedback for electronic control units (ECUs). The integration of these ICs in powertrain, steering, and brake systems is creating new revenue opportunities for manufacturers.

Miniaturization and Enhanced Performance in Consumer Electronics

The push toward miniaturization in consumer electronics is reshaping the encoder IC landscape. Smartphones, wearables, and IoT devices now require compact yet highly efficient position sensing solutions. Optical encoders, in particular, are benefiting from the trend toward smaller form factors and higher resolution, as they provide precise feedback for haptic feedback modules, camera autofocus mechanisms, and touch-sensitive interfaces. Meanwhile, advancements in magnetic encoder ICs have led to improved noise immunity and durability, making them ideal for rugged consumer and industrial applications. As the demand for connected devices increases, the encoder IC market is also experiencing growth in edge computing applications where low-latency motion control is critical.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Competition in the Encoder IC Market

The global magnetic and optical encoder ICs market features a dynamic competitive landscape dominated by established semiconductor manufacturers and specialized sensor providers. The market is projected to grow at a CAGR of 6.3% from 2024-2032, reaching $710 million, intensifying competition among key players. Broadcom leads the market with its comprehensive portfolio of high-resolution optical encoder solutions, particularly for industrial automation applications where precision positioning is critical.

AMS OSRAM (formerly ams AG) has emerged as a strong competitor through its innovative magnetic encoder ICs that combine high accuracy with robust performance in harsh environments. The company’s recent acquisition of OSRAM has further strengthened its position in optoelectronic solutions. Similarly, TE Connectivity maintains significant market share through its diverse encoder IC offerings that cater to automotive and industrial sectors, where reliability under extreme conditions is paramount.

While these major players dominate the high-volume segments, specialized manufacturers like IC-Haus and RLS compete effectively in niche applications requiring custom solutions. Their ability to provide application-specific integrated circuits (ASICs) for demanding environments gives them a competitive edge in aerospace and medical equipment markets. Furthermore, Asian players such as SEIKO NPC are gaining traction by offering cost-competitive alternatives without compromising performance standards.

The market is witnessing strategic shifts as companies invest in new manufacturing technologies and form alliances to address emerging application areas. New Japan Radio recently expanded its encoder IC production capacity to meet growing demand from robotics manufacturers, while Hamamatsu is focusing on developing miniaturized optical encoder solutions for next-generation wearable devices. These developments indicate an industry-wide push towards more compact, energy-efficient designs with enhanced functionality.

List of Leading Magnetic and Optical Encoder IC Companies

- Broadcom Inc. (U.S.)

- AMS OSRAM (Austria)

- TE Connectivity (Switzerland)

- New Japan Radio Co., Ltd. (Japan)

- IC-Haus GmbH (Germany)

- SEIKO NPC Corporation (Japan)

- RLS d.o.o. (Slovenia)

- PREMA Semiconductor GmbH (Germany)

- Hamamatsu Photonics K.K. (Japan)

Segment Analysis:

By Type

Optical Encoder ICs Segment Leads Due to High Precision in Industrial Automation

The market is segmented based on type into:

- Magnetic Encoder ICs

- Subtypes: Hall-effect, magnetoresistive, and others

- Optical Encoder ICs

- Subtypes: Incremental, absolute, and others

By Application

Industrial Automation Drives Demand Due to Growing Smart Factory Adoption

The market is segmented based on application into:

- Industrial automation

- Automotive

- Consumer electronics

- Medical equipment

- Aerospace & defense

- Others

By Resolution

High-Resolution Segment Gains Traction for Precision Applications

The market is segmented based on resolution into:

- Low resolution (≤12-bit)

- Medium resolution (13-16-bit)

- High resolution (≥17-bit)

By Output Type

Digital Output Dominates for Seamless System Integration

The market is segmented based on output type into:

- Analog output

- Digital output

- Subtypes: Parallel, serial, and fieldbus

Regional Analysis: Magnetic and Optical Encoder ICs Market

North America

The North American market for magnetic and optical encoder ICs remains technologically advanced, driven by strong demand from industries such as automotive, aerospace, and industrial automation. The U.S. leads in innovation, with companies investing in high-precision encoders for robotics and electric vehicle applications. Government initiatives, such as the Chips and Science Act, which allocates $52 billion for semiconductor manufacturing, provide additional growth opportunities. However, stringent regulatory compliance and high manufacturing costs pose challenges for local players. The region’s focus on Industry 4.0 and smart manufacturing is expected to sustain demand for encoder ICs, particularly in motion control systems.

Europe

Europe’s magnetic and optical encoder ICs market benefits from a robust industrial manufacturing sector, particularly in Germany and Italy, where advanced automation is a priority. The EU’s Horizon Europe program supports research in semiconductor technologies, fostering innovation in encoder IC applications. However, energy cost fluctuations and economic uncertainties have impacted manufacturing investments. Despite this, demand remains steady in medical equipment and renewable energy sectors, where high-resolution encoders are essential. The push toward digital transformation in European factories is expected to drive long-term growth, although competition from Asian manufacturers remains fierce.

Asia-Pacific

Asia-Pacific dominates the encoder IC market due to massive electronics manufacturing hubs in China, Japan, and South Korea. China’s industrial automation expansion, particularly in robotics and consumer electronics, fuels substantial demand for cost-effective encoder solutions. While optical encoders lead in high-precision applications, magnetic encoders are widely adopted in automotive and heavy machinery due to their durability. The region benefits from strong supply chain integration, though intellectual property concerns and price sensitivity restrict premium product adoption. India’s growing semiconductor ecosystem also presents new opportunities, driven by government incentives for local electronics production.

South America

South America’s encoder IC market remains in its early stages, with Brazil and Argentina showing gradual growth in industrial automation. Economic instability and fluctuating raw material costs often delay large-scale adoption of advanced encoder technologies. However, increasing foreign investments in automotive and food processing industries are driving demand for mid-range encoder ICs. Local manufacturers primarily rely on imports due to limited semiconductor fabrication capabilities. Still, initiatives to modernize legacy industrial systems could unlock growth potential in the long term.

Middle East & Africa

The Middle East & Africa region shows nascent but promising growth, particularly in the UAE and Saudi Arabia, where smart manufacturing initiatives are emerging. The oil and gas sector’s reliance on rugged encoder ICs for control systems sustains demand, though broader industrial use remains limited. In Africa, infrastructure constraints and a lack of technical expertise slow adoption, but increasing foreign manufacturing investments signal future opportunities. As regional industries transition toward automation, encoder ICs will likely see incremental growth, though progress will be uneven.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Magnetic and Optical Encoder ICs markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Magnetic and Optical Encoder ICs market was valued at USD 466 million in 2024 and is projected to reach USD 710 million by 2032, growing at a CAGR of 6.3%.

- Segmentation Analysis: Detailed breakdown by product type (Magnetic Encoder ICs and Optical Encoder ICs), application (Medical Equipment, Machine Tools, Consumer Electronics, Assembly Equipment), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market due to rapid industrialization.

- Competitive Landscape: Profiles of leading market participants including Broadcom, AMS, TE Connectivity, and Hamamatsu, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in encoder ICs, integration with IoT systems, miniaturization trends, and evolving industry standards for precision motion control.

- Market Drivers & Restraints: Evaluation of factors driving market growth including automation trends and Industry 4.0 adoption, along with challenges such as supply chain constraints and technical limitations.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in motion control systems.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Magnetic and Optical Encoder ICs Market?

-> Magnetic and Optical Encoder ICs Market was valued at 466 million in 2024 and is projected to reach US$ 710 million by 2032, at a CAGR of 6.3% during the forecast period.

Which key companies operate in Global Magnetic and Optical Encoder ICs Market?

-> Key players include Broadcom, AMS, New Japan Radio, TE Connectivity, IC-Haus, SEIKO NPC, RLS, PREMA Semiconductor, and Hamamatsu.

What are the key growth drivers?

-> Key growth drivers include industrial automation trends, increasing adoption of Industry 4.0, and demand for precision motion control systems across various industries.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing region, driven by manufacturing growth in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of encoder ICs, integration with IoT systems, and development of high-resolution optical encoders for advanced applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...