MARKET INSIGHTS

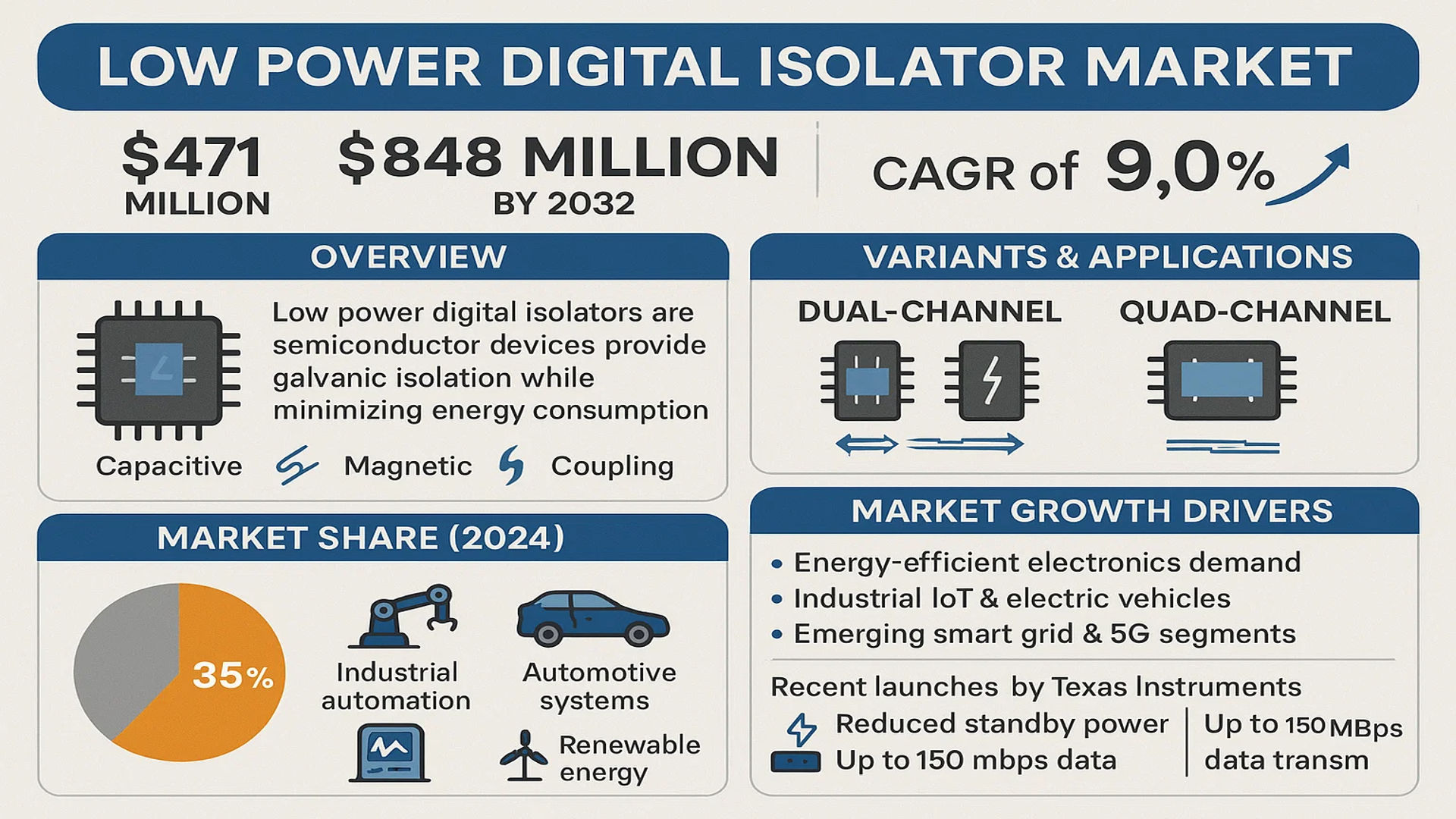

The global Low Power Digital Isolator Market was valued at 471 million in 2024 and is projected to reach US$ 848 million by 2032, at a CAGR of 9.0% during the forecast period.

Low power digital isolators are semiconductor devices that provide galvanic isolation between circuit sections while minimizing energy consumption. These components use capacitive or magnetic coupling techniques to transmit digital signals across isolation barriers without direct electrical connection, protecting sensitive electronics from voltage spikes and noise. Key variants include dual-channel and quad-channel isolators, with applications spanning industrial automation, automotive systems, medical equipment, and renewable energy infrastructure.

The market growth is driven by increasing demand for energy-efficient electronics across industries, particularly in industrial IoT and electric vehicles where power optimization is critical. While industrial automation remains the dominant application segment accounting for over 35% of market share in 2024, emerging sectors like smart grid technologies and 5G infrastructure are creating new growth opportunities. Recent product launches from major players like Texas Instruments and Analog Devices focus on reducing standby power consumption below 1mW while maintaining high-speed data transmission capabilities up to 150Mbps.

MARKET DYNAMICS

MARKET DRIVERS

Growth of Industrial Automation to Accelerate Low Power Digital Isolator Adoption

The industrial automation sector is experiencing rapid expansion with investments exceeding $200 billion globally in 2024. This growth directly drives demand for low power digital isolators as they are essential components in factory automation systems, robotics, and process control equipment. These isolators provide critical galvanic isolation that prevents ground loops and protects sensitive electronics from high voltages in industrial environments. The transition towards Industry 4.0 and smart manufacturing further strengthens this demand, as connected industrial systems require robust signal isolation to maintain operational reliability.

Expansion of Renewable Energy Infrastructure Creates New Applications

The global renewable energy sector is projected to grow at 8.5% CAGR through 2030, creating substantial opportunities for low power digital isolators. Solar inverters, wind turbine control systems, and battery management solutions all require high-efficiency isolation components to ensure safe operation while minimizing power consumption. Digital isolators with power consumption below 1mW per channel are becoming particularly valuable in distributed energy systems where efficiency directly impacts operational costs. Recent technological advances have enabled isolators to withstand voltages up to 5kV while maintaining ultra-low power characteristics.

Automotive Electrification Revolution Demands Advanced Isolation Solutions

With electric vehicle production expected to reach 40 million units annually by 2030, automotive applications represent one of the fastest-growing segments for low power digital isolators. These components are critical in battery management systems, onboard chargers, and traction inverters where they provide isolation between high-voltage components (up to 800V in next-generation EVs) and low-voltage control circuits. The automotive industry’s stringent requirements for reliability, temperature tolerance, and power efficiency make low power digital isolators the preferred choice over traditional optocouplers.

MARKET RESTRAINTS

Technical Challenges in High-Temperature Environments Limit Applications

While low power digital isolators perform well in standard conditions, maintaining their ultra-low power characteristics at extreme temperatures remains an engineering challenge. Many industrial and automotive applications require components to operate reliably at temperatures exceeding 125°C, where traditional semiconductor-based isolators may experience increased leakage currents that degrade power efficiency. This limitation prevents their deployment in certain harsh environment applications where optocouplers still maintain an advantage.

Other Restraints

Legacy System Compatibility Issues

The transition from optocouplers to digital isolators faces resistance in legacy industrial systems where existing designs are optimized for optical isolation components. System redesigns required to accommodate digital isolator interfaces can increase implementation costs and slow adoption rates.

Certification Complexity for Safety-Critical Applications

Achieving necessary safety certifications (such as UL, IEC, and VDE) for medical and automotive applications remains resource-intensive. The stringent testing requirements and lengthy certification processes can delay product launches by 6-12 months, delaying revenue realization for manufacturers.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Market Stability

The semiconductor shortage crisis demonstrated the vulnerability of digital isolator supply chains, with lead times extending beyond 52 weeks at the peak of disruptions. While conditions have improved, ongoing geopolitical tensions and raw material supply uncertainties continue to challenge manufacturers. The specialized fabrication processes required for high-performance isolators limit the number of qualified foundries, creating bottlenecks during demand surges.

Other Challenges

Intellectual Property Disputes

The competitive landscape has seen increasing patent litigation around digital isolation technologies as companies seek to protect their proprietary designs. These legal disputes can restrict market access for new entrants and create uncertainty for end-users evaluating long-term supply availability.

Design Complexity in High-Speed Applications

While digital isolators excel in many applications, maintaining signal integrity at data rates above 150Mbps while preserving low power characteristics presents ongoing engineering challenges. This limits their adoption in certain high-speed communications applications where power efficiency is critical.

MARKET OPPORTUNITIES

Emerging Medical Electronics Applications Show Strong Growth Potential

The medical electronics market, valued at nearly $7 billion in 2024, presents significant opportunities for low power digital isolators. Patient monitoring equipment, portable diagnostic devices, and implantable medical electronics increasingly adopt these components for their superior reliability and energy efficiency compared to traditional isolation solutions. The trend towards telemedicine and home healthcare devices creates additional demand for compact, low-power isolation solutions that can operate reliably for extended periods on battery power.

Advancements in Wireless Power Systems Open New Markets

The development of next-generation wireless charging systems for consumer electronics, medical devices, and automotive applications requires sophisticated power management with robust isolation. Low power digital isolators capable of operating in the MHz frequency range are enabling more efficient inductive power transfer systems while maintaining critical safety isolation barriers. Industry leaders are investing heavily in developing isolators specifically optimized for these emerging wireless power applications.

Miniaturization Trend Creates Demand for Integrated Solutions

The continuous drive towards smaller form factors in consumer electronics and IoT devices has created demand for advanced isolation solutions that combine multiple channels in single packages while maintaining ultra-low power characteristics. Recent product launches have demonstrated multi-channel isolators in packages as small as 3mm x 3mm with power consumption below 0.5mW per channel. This trend enables new applications in portable electronics where space and power constraints previously limited isolation options.

LOW POWER DIGITAL ISOLATOR MARKET TRENDS

Energy Efficiency Driving Adoption Across Industrial and Automotive Sectors

The low power digital isolator market is experiencing robust growth, projected to expand from $471 million in 2024 to $848 million by 2032 at a 9.0% CAGR, largely driven by the global push toward energy-efficient electronics. These components have become indispensable in industrial automation systems, where they enable noise-free signal transmission between high-voltage and low-voltage circuits while consuming minimal power. Modern manufacturing plants increasingly deploy digital isolators in motor drives, programmable logic controllers (PLCs), and robotics to ensure operational safety and reliability. Simultaneously, automotive electrification trends—particularly in electric vehicle powertrains and battery management systems—are creating substantial demand. With Tier 1 suppliers prioritizing lightweight, low-power solutions, digital isolators are replacing bulkier optocouplers in 48V mild-hybrid systems and onboard chargers.

Other Trends

Integration with Next-Gen Semiconductor Technologies

Silicon carbide (SiC) and gallium nitride (GaN) semiconductor adoption is reshaping isolation requirements in power electronics applications. Digital isolators compatible with these wide-bandgap materials are gaining traction in solar inverters, DC-DC converters, and server power supplies. Recent innovations include isolators with reinforced isolation ratings up to 5kVrms and data rates exceeding 150Mbps—critical for high-performance computing and 5G infrastructure. Furthermore, chipset manufacturers are embedding power regulation and signal conditioning functions within isolation ICs, reducing board space by up to 30% compared to discrete solutions.

Healthcare and Consumer Electronics Emerging as Growth Frontiers

The medical equipment segment presents significant opportunities, particularly for patient monitoring devices and portable diagnostic tools requiring robust isolation in compact form factors. Regulatory standards like IEC 60601-1 are accelerating the shift from optocouplers to digital isolators in ventilators, ECG machines, and ultrasound systems. Meanwhile, consumer electronics manufacturers are leveraging these components in wearable devices and smart home systems to enhance safety while extending battery life. The proliferation of wireless charging pads and USB-C power delivery systems has further expanded the addressable market, with dual-channel isolators seeing particular demand for bidirectional communication interfaces.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Energy-Efficient Innovations to Maintain Competitive Edge

The low power digital isolator market is characterized by a mix of established semiconductor giants and emerging specialized manufacturers vying for market share. The industry is witnessing intensified competition as companies accelerate development of ultra-low-power isolation solutions for next-generation applications in industrial automation, automotive, and IoT sectors. Texas Instruments currently leads the market with an approximate 22% revenue share in 2024, leveraging its comprehensive product portfolio and established distribution networks across North America and Asia-Pacific regions.

Analog Devices and Infineon Technologies follow closely, collectively accounting for nearly 30% of the global market. These companies have strengthened their positions through strategic acquisitions and continuous R&D investments focused on improving isolator power efficiency and integration capabilities. Recent product launches featuring sub-1mA current consumption demonstrate the technological arms race driving the sector forward.

The competitive environment continues to evolve as mid-sized players adopt aggressive expansion strategies. Broadcom Inc. and ROHM Semiconductor have made significant inroads into the industrial automation segment by introducing ruggedized isolators capable of withstanding harsh operating conditions while maintaining minimal power draw. These companies are also expanding manufacturing capacities in key Asian markets to reduce lead times and enhance customer responsiveness.

Meanwhile, Chinese manufacturers like Mornsun Power and Shanghai Chipanalog Microelectronics are disrupting traditional supply chains by offering cost-competitive alternatives. These regional players are capturing market share in domestic renewable energy and smart grid applications, forcing multinational corporations to reconsider their pricing strategies in price-sensitive markets.

List of Key Low Power Digital Isolator Companies

- Analog Devices, Inc. (U.S.)

- Skyworks Solutions, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- Broadcom Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Vicor Corporation (U.S.)

- NVE Corporation (U.S.)

- ROHM Semiconductor (Japan)

- Mornsun Power (China)

- Renesas Electronics Corporation (Japan)

Segment Analysis:

By Type

Dual-Channel Digital Isolators Lead Due to Their Cost-Effectiveness and Wide Application Scope

The market is segmented based on type into:

- Dual-Channel Digital Isolator

- Subtypes: Capacitive-coupled, Magnetic-coupled, and others

- Quad-Channel Digital Isolator

- Six-Channel Digital Isolator

- Others

By Application

Industrial Control Dominates Due to High Demand for Safe Signal Transmission in Harsh Environments

The market is segmented based on application into:

- Industrial Control

- New Energy

- Digital Power

- Healthcare

- Consumer Electronics

- Others

By Isolation Technology

Capacitive-Coupled Isolation Leads the Market Due to Higher Data Rates and Better Performance

The market is segmented based on isolation technology into:

- Capacitive-Coupled Isolation

- Magnetic-Coupled Isolation

- Optical Isolation

- Others

By End User

Industrial Automation Sector Accounts for Significant Share Due to Critical Safety Requirements

The market is segmented based on end user into:

- Industrial Automation

- Energy Sector

- Medical Equipment

- Telecommunications

- Others

Regional Analysis: Low Power Digital Isolator Market

Asia-Pacific

The Asia-Pacific region dominates the global low power digital isolator market, accounting for over 40% of revenue share in 2024. This leadership position is driven by rapid industrialization in China and India, coupled with strong demand from the automotive and industrial automation sectors. China, in particular, benefits from its robust electronics manufacturing ecosystem and government initiatives like “Made in China 2025,” which prioritizes energy-efficient semiconductor components. Additionally, the expanding renewable energy sector across Southeast Asia accelerates demand for isolators in solar inverters and battery management systems. Japan and South Korea contribute significantly due to their advanced automotive and consumer electronics industries, where miniaturization and power efficiency are critical.

North America

North America is a key innovator in low power digital isolator technology, with the U.S. leading due to stringent safety regulations in industries like healthcare and aerospace. The region’s market growth is bolstered by increasing investments in industrial IoT (IIoT) and electric vehicles (EVs), where isolators ensure signal integrity in high-noise environments. Major players like Texas Instruments and Analog Devices drive R&D efforts, focusing on ultra-low-power (<1mA) isolators for battery-operated devices. Canada’s growing renewable energy projects further stimulate demand, particularly in grid-tied inverters requiring robust isolation solutions.

Europe

Europe’s market thrives on its strong automotive and industrial automation sectors, where EU mandates like the Electromagnetic Compatibility (EMC) Directive enforce strict isolation standards. Germany is the largest contributor, with its Industrie 4.0 initiatives pushing demand for isolators in smart factories. The region also sees rising adoption in medical equipment, owing to CE certification requirements for patient safety. However, slower growth in consumer electronics partially offsets these gains. Vendors here prioritize eco-friendly designs, aligning with the EU’s Circular Economy Action Plan.

South America

This region exhibits moderate growth, primarily fueled by Brazil’s burgeoning industrial sector and Argentina’s renewable energy projects. While economic instability limits large-scale investments, increasing automation in mining and oil/gas operations creates niche opportunities for low power isolators. Local manufacturers face challenges competing with imported solutions from Asia and North America due to higher costs. Nevertheless, government efforts to modernize infrastructure, such as Brazil’s “Nova Indústria Brasil” plan, could unlock long-term potential.

Middle East & Africa

The MEA market remains nascent but shows promise, particularly in GCC countries investing heavily in smart cities and renewable energy. The UAE and Saudi Arabia lead in adopting isolators for solar power plants and oilfield automation. However, irregular regulatory frameworks and reliance on imports hinder faster growth. South Africa emerges as a focal point for industrial applications, though currency volatility affects procurement. The region’s expansion will likely align with broader economic diversification programs over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Low Power Digital Isolator markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Low Power Digital Isolator market was valued at USD 471 million in 2024 and is projected to reach USD 848 million by 2032, growing at a CAGR of 9.0%.

- Segmentation Analysis: Detailed breakdown by product type (Dual-Channel, Quad-Channel), application (Industrial Control, New Energy, Digital Power, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market with significant growth in industrial automation.

- Competitive Landscape: Profiles of leading market participants, including Analog Devices, Texas Instruments, Broadcom, Infineon, and Skyworks Solutions, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in semiconductor isolation, integration with IoT devices, and advancements in energy-efficient designs.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as industrial automation adoption and demand for energy-efficient electronics, along with challenges like supply chain constraints and regulatory compliance.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in low-power isolation technologies.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Low Power Digital Isolator Market?

->Low Power Digital Isolator Market was valued at 471 million in 2024 and is projected to reach US$ 848 million by 2032, at a CAGR of 9.0% during the forecast period.

Which key companies operate in Global Low Power Digital Isolator Market?

-> Key players include Analog Devices, Texas Instruments, Broadcom, Infineon, Skyworks Solutions, NVE, and ROHM, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation expansion, rising demand for energy-efficient electronics, and increasing adoption in electric vehicles and renewable energy systems.

Which region dominates the market?

-> Asia-Pacific is the dominant market due to rapid industrialization, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration with IoT devices, development of ultra-low-power isolators, and increased adoption in medical electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...