MARKET INSIGHTS

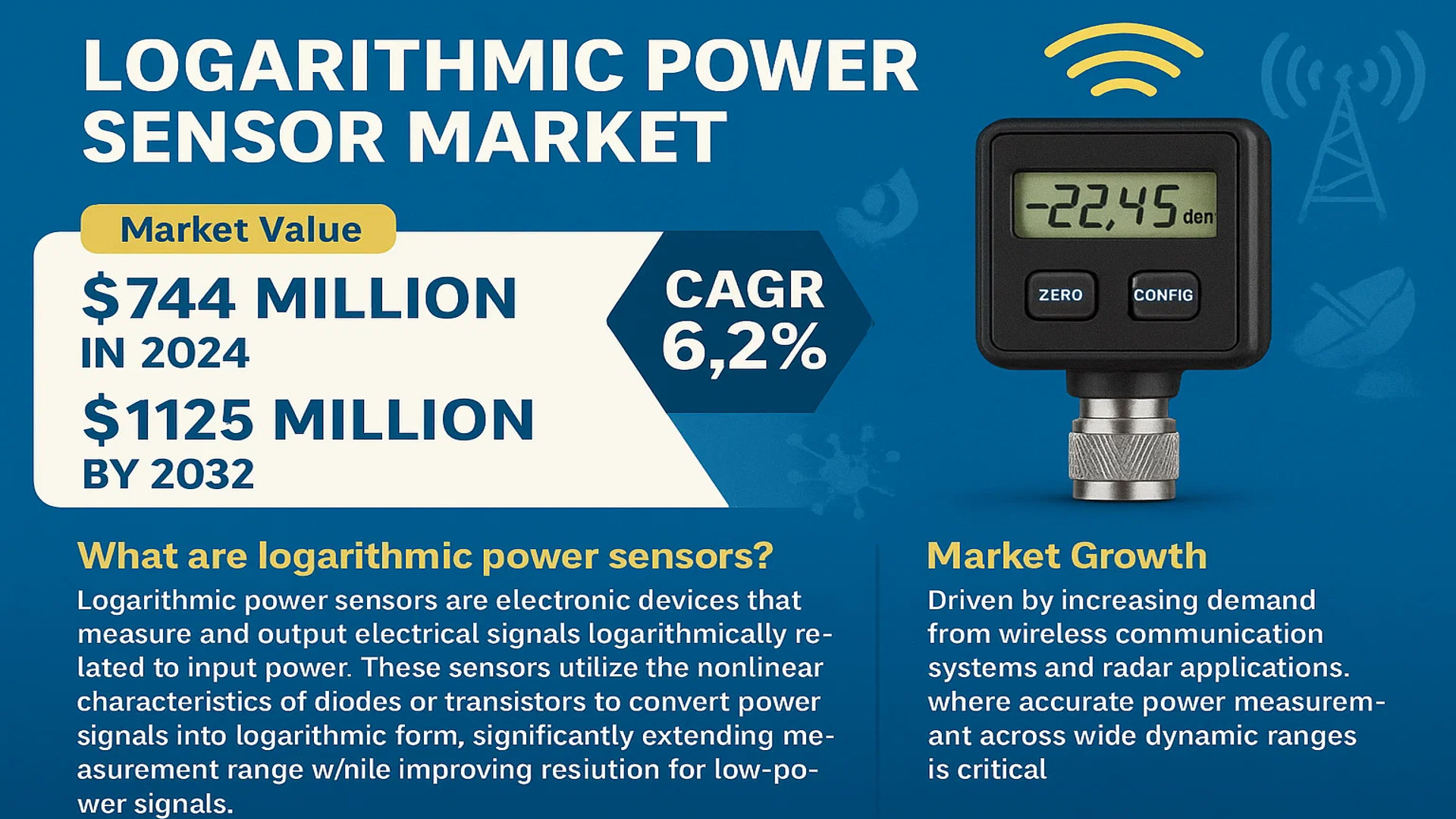

The global Logarithmic Power Sensor Market was valued at 744 million in 2024 and is projected to reach US$ 1125 million by 2032, at a CAGR of 6.2% during the forecast period.

Logarithmic power sensors are specialized electronic devices that measure and output electrical signals logarithmically related to input power. These sensors utilize the nonlinear characteristics of diodes or transistors to convert power signals into logarithmic form, significantly extending measurement range while improving resolution for low-power signals. The technology simplifies power ratio calculations and is widely adopted in applications requiring wide dynamic range measurements.

The market growth is driven by increasing demand from wireless communication systems and radar applications, where accurate power measurement across wide dynamic ranges is critical. Furthermore, advancements in 5G technology and expanding IoT networks are creating new opportunities for logarithmic power sensor adoption. Key players like Keysight, Rohde & Schwarz, and Anritsu dominate the market with comprehensive product portfolios, while emerging applications in optical power measurement are contributing to market expansion. The U.S. currently holds the largest market share, though Asia-Pacific is expected to show the highest growth rate due to rapid technological adoption in China and Japan.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Wireless Communication Technologies to Spur Market Growth

The global logarithmic power sensor market is experiencing robust growth, primarily driven by the rapid expansion of wireless communication technologies. With the ongoing deployment of 5G networks and increasing adoption of IoT devices, there is surging demand for precise power measurement solutions. The number of connected IoT devices is projected to exceed 29 billion by 2027, creating substantial opportunities for power sensor manufacturers. Logarithmic power sensors play a critical role in optimizing signal integrity and ensuring reliable power measurements across various frequency ranges, including microwave and millimeter-wave bands. The telecommunications industry accounts for nearly 40% of the total market demand, making it the largest application segment.

Advancements in Radar and Defense Systems to Boost Adoption

The defense sector’s increasing investment in advanced radar systems is another significant driver for logarithmic power sensors. Modern phased-array radars require high-precision power measurement capabilities to ensure optimal performance across varying signal conditions. The global defense expenditure has surpassed $2 trillion, with radar systems accounting for a substantial portion of this investment. Logarithmic power sensors offer distinct advantages in radar applications due to their ability to measure wide dynamic ranges (typically 60-80 dB) while maintaining excellent accuracy. Their use is particularly critical in electronic warfare systems, where rapid power level assessment can be mission-critical.

Additionally, the growing adoption of automated test equipment (ATE) in manufacturing processes represents a key growth avenue. As production volumes increase across semiconductor and electronics industries, the need for efficient testing solutions incorporating logarithmic power measurement becomes more pronounced.

Emergence of New Optical Power Measurement Applications

The optical power measurement segment is witnessing accelerated growth due to expanding fiber optic network deployments and photonics research. Logarithmic sensors are finding increasing application in optical power monitoring systems, particularly in dense wavelength division multiplexing (DWDM) networks. The global fiber optics market is expected to grow at a 7.5% CAGR through 2030, driven by escalating bandwidth requirements across telecom and data center applications. These sensors enable precise power measurements across the entire optical spectrum while offering the dynamic range necessary for modern optical networks.

MARKET RESTRAINTS

High Cost of Advanced Power Sensors Limiting Market Penetration

While demand is growing, the logarithmic power sensor market faces significant barriers due to the high cost of advanced measurement solutions. Precision power sensors incorporating logarithmic amplifiers and calibration circuits can cost several thousand dollars per unit, putting them out of reach for many small and medium enterprises. The manufacturing process requires specialized semiconductor fabrication and precise calibration procedures, contributing to elevated production costs. This pricing pressure is particularly acute in price-sensitive emerging markets where cost considerations often outweigh performance requirements.

Technical Challenges in High-Frequency Applications

As operating frequencies continue to increase into millimeter-wave and terahertz ranges, logarithmic power sensors face technical limitations. Maintaining measurement accuracy above 60 GHz becomes increasingly challenging due to signal integrity issues and parasitic effects in sensor circuits. These limitations affect adoption in cutting-edge applications such as 6G research and advanced radar systems where ultra-high frequency operation is essential.

Supply Chain Constraints for Specialized Components

The market continues to face supply chain challenges for critical components such as logarithmic amplifiers and precision diodes. Many of these components have lead times exceeding 20 weeks, creating bottlenecks in sensor manufacturing. The industry’s reliance on specialized semiconductor processes further exacerbates these supply constraints, particularly during periods of high demand.

MARKET OPPORTUNITIES

Integration with AI and Machine Learning Presents New Growth Avenues

The combination of logarithmic power sensors with AI-driven data analysis represents a significant opportunity for market expansion. Intelligent power monitoring systems can leverage the wide dynamic range of logarithmic sensors while applying machine learning algorithms for predictive maintenance and performance optimization. This integration is particularly valuable in 5G base stations and edge computing applications where real-time power monitoring helps prevent network outages. The global market for AI in test and measurement is projected to grow at over 25% CAGR through 2030, creating substantial demand for smart sensor solutions.

Expansion into Medical and Scientific Instrumentation

Logarithmic power sensors are finding new applications in medical imaging systems and scientific instrumentation where precise power monitoring is critical. MRI systems, spectroscopy equipment, and particle accelerators increasingly incorporate these sensors for beam power measurement and control. The global medical device market, valued at over $500 billion, presents significant untapped potential for specialized power measurement solutions. As imaging resolutions improve and therapeutic applications expand, the demand for high-performance power sensors in these applications is expected to accelerate.

The development of miniaturized sensors for portable applications also offers growth potential. Compact logarithmic power sensors with low power consumption are enabling new use cases in field-deployable test equipment and handheld measurement devices. These devices are particularly valuable for field service technicians and maintenance personnel requiring high-performance measurements in mobile scenarios.

MARKET CHALLENGES

Maintaining Measurement Accuracy Across Wide Temperature Ranges

The logarithmic power sensor market faces persistent challenges in maintaining measurement accuracy across extended temperature ranges. While typical laboratory environments maintain controlled conditions, industrial and outdoor applications expose sensors to temperature variations that can exceed 100°C range. These thermal variations introduce measurement errors in logarithmic amplifiers and detector circuits, requiring complex temperature compensation techniques. Manufacturers must balance the need for precision with the realities of diverse operating environments, often resulting in trade-offs between performance and robustness.

Standardization and Calibration Complexity

The industry lacks universal calibration standards for logarithmic power measurements, creating challenges for system integrators. Each manufacturer employs proprietary calibration methodologies, making direct comparisons between different sensor models difficult. This standardization gap complicates the process of sensor selection and integration, particularly in multi-vendor test and measurement systems.

Rapid Technological Obsolescence

The fast pace of technological advancement in wireless communications and semiconductor technologies creates constant pressure for sensor upgrades. Many existing logarithmic power sensor designs become obsolete within 3-5 years as new communication standards and frequency bands emerge. This rapid technology turnover increases development costs and shortens product lifecycles, presenting ongoing challenges for manufacturers seeking to maintain profitability.

LOGARITHMIC POWER SENSOR MARKET TRENDS

Advancements in Telecommunication and 5G Deployment Driving Demand

The logarithmic power sensor market is experiencing significant growth, driven by the rapid expansion of telecommunication networks and the global rollout of 5G infrastructure. These sensors play a crucial role in measuring power levels across wide dynamic ranges, making them indispensable in RF and microwave applications. With 5G networks requiring precise power monitoring for signal integrity and efficiency, industry projections indicate a 19% year-over-year increase in adoption of high-performance logarithmic sensors for base stations and network equipment. Furthermore, the integration of these sensors in millimeter-wave (mmWave) frequency bands, where accurate power measurement is critical for maintaining network performance, has created new opportunities for market expansion.

Other Trends

Growing Adoption in Defense and Aerospace Applications

Logarithmic power sensors are increasingly being deployed in defense and aerospace systems, particularly for radar and electronic warfare applications. The ability to measure power levels across extremely wide dynamic ranges—often exceeding 80 dB—makes these sensors ideal for detecting weak signals in noisy environments. Military modernization programs worldwide are incorporating advanced radar systems that require precise power measurement capabilities, contributing to a 12% annual growth in defense sector demand. Additionally, satellite communication systems are leveraging logarithmic sensors for both ground stations and onboard spacecraft, further driving market expansion in this segment.

Miniaturization and Integration Fueling Product Innovation

Manufacturers are focusing on developing compact, integrated logarithmic power sensor solutions to meet the needs of space-constrained applications. Recent advancements have led to chip-scale packaging of sensor components while maintaining the high dynamic range and accuracy required for critical measurements. This trend is particularly evident in portable test equipment and field-deployable systems, where size and power efficiency are paramount. The market has responded positively to these innovations, with compact sensor modules now accounting for over 30% of new product introductions. Furthermore, the integration of digital interfaces like USB and Ethernet with logarithmic sensors has simplified connectivity with modern test and measurement systems, creating new opportunities in automated testing environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Market Competition

The global logarithmic power sensor market features a dynamic competitive environment where established players dominate through technological advancements and strategic expansions. Keysight Technologies leads the market with its comprehensive portfolio of high-precision sensors, holding a significant revenue share as of 2024. The company’s dominance stems from its strong R&D capabilities and widespread adoption in wireless communication and radar systems.

Similarly, Rohde & Schwarz and Anritsu have cemented their positions as key players, leveraging their expertise in test and measurement solutions. Both companies are focusing on expanding their sensor offerings for 5G and optical applications, which is expected to fuel their growth in the coming years.

The market also sees growing competition from specialized manufacturers like Vaunix and Mini-Circuits, which are gaining traction through cost-effective solutions for small and medium enterprises. These players are actively investing in miniaturized sensor technologies to cater to the increasing demand for compact measurement devices.

Meanwhile, traditional test equipment giants including NI (National Instruments) and Tektronix are reinforcing their market positions through strategic acquisitions and partnerships. Their extensive distribution networks and brand recognition continue to give them an edge in both developed and emerging markets.

List of Key Logarithmic Power Sensor Manufacturers

- Keysight Technologies (U.S.)

- Rohde & Schwarz (Germany)

- Anritsu Corporation (Japan)

- NI (National Instruments) (U.S.)

- Tektronix (U.S.)

- Teledyne Technologies (U.S.)

- Bird Technologies (U.S.)

- Vaunix Technology Corp. (U.S.)

- Mini-Circuits (U.S.)

- Analog Devices (U.S.)

Segment Analysis:

By Type

Diode-based Segment Holds Major Market Share Due to High Accuracy and Wide Dynamic Range

The market is segmented based on type into:

- Diode-based

- Subtypes: Schottky diode and PIN diode

- Transistor-based

By Application

Wireless Communications Dominates Market Demand Due to 5G Network Expansion

The market is segmented based on application into:

- Wireless communications

- Radar systems

- Optical power measurement

- Test and measurement equipment

- Others

By Frequency Range

Microwave Frequency Range Segment Leads With Growing Demand in Defense Applications

The market is segmented based on frequency range into:

- DC to 1 GHz

- 1 GHz to 10 GHz

- 10 GHz to 40 GHz

- 40 GHz and above

By End-User Industry

Telecommunications Sector Accounts for Largest Share Due to Network Infrastructure Modernization

The market is segmented based on end-user industry into:

- Telecommunications

- Aerospace and defense

- Semiconductor

- Research and development

- Others

Regional Analysis: Logarithmic Power Sensor Market

North America

North America dominates the logarithmic power sensor market, with the U.S. accounting for the largest revenue share. The region’s leadership stems from its advanced wireless communication infrastructure and significant investments in 5G deployment, radar systems, and defense technologies. Major players like Keysight, NI, and Tektronix are headquartered here, driving innovation in diode-based and transistor-based power sensors. The demand is further fueled by stringent calibration standards in aerospace and telecommunications, requiring high-precision power measurement. However, high costs of advanced sensors and supply chain disruptions pose challenges for smaller businesses adopting this technology.

Asia-Pacific

The Asia-Pacific region is witnessing the fastest growth in the logarithmic power sensor market, with China, Japan, and South Korea leading the charge. This surge is driven by massive 5G infrastructure projects, expanding semiconductor manufacturing, and government initiatives like China’s “Made in China 2025.” The region benefits from cost-effective production capabilities and rising demand for optical power measurement in consumer electronics. While transistor-based sensors are gaining traction due to their wider dynamic range, price sensitivity remains a barrier for high-end applications. Local players such as Anritsu are competing globally, though they face stiff competition from established Western brands.

Europe

Europe maintains a strong position in the market, supported by its robust automotive radar systems and industrial automation sector. Countries like Germany and France emphasize high-accuracy power measurement for automotive LiDAR and renewable energy systems under strict EU electromagnetic compatibility (EMC) regulations. Companies like Rohde & Schwarz are key contributors, focusing on R&D for low-power wireless applications. The shift toward Industry 4.0 and IoT further propels demand, though slower 5G rollout compared to Asia and North America slightly limits growth potential in communications applications.

South America

South America’s market is emerging, with Brazil being the primary adopter of logarithmic power sensors for basic wireless communication testing and academic research. Budget constraints and limited local manufacturing capabilities result in dependence on imports, primarily from North American and European suppliers. The region shows potential in radar and satellite communication applications but faces challenges due to economic instability and lack of standardized testing protocols. Nevertheless, increasing foreign investments in telecom infrastructure hint at future growth opportunities.

Middle East & Africa

This region represents a niche but growing market, with demand centered around oil & gas infrastructure monitoring and defense applications. Countries like Israel and Saudi Arabia are investing in advanced radar and signal intelligence systems, creating opportunities for high-end power sensors. The lack of local expertise and limited R&D investment slows adoption rates, but partnerships with global manufacturers and infrastructure development projects are gradually expanding the market’s scope.

Report Scope

This market research report provides a comprehensive analysis of the Global Logarithmic Power Sensor Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Logarithmic Power Sensor market was valued at USD 744 million in 2024 and is projected to reach USD 1125 million by 2032, growing at a CAGR of 6.2%.

- Segmentation Analysis: Detailed breakdown by product type (Diode-based, Transistor-based), application (Wireless Communications, Radar Systems, Optical Power Measurement, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific showing the fastest growth.

- Competitive Landscape: Profiles of leading market participants, including NI, Keysight, Rohde & Schwarz, Anritsu, and Teledyne Technologies, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with IoT systems, and advancements in semiconductor design for power measurement applications.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for 5G infrastructure, increasing adoption in defense systems, along with challenges like supply chain constraints and high development costs.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, and investors regarding market opportunities and the evolving technological landscape.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Logarithmic Power Sensor Market?

-> Logarithmic Power Sensor Market was valued at 744 million in 2024 and is projected to reach US$ 1125 million by 2032, at a CAGR of 6.2% during the forecast period.

Which key companies operate in Global Logarithmic Power Sensor Market?

-> Key players include NI, Keysight, Rohde & Schwarz, Anritsu, Teledyne Technologies, Bird Technologies, and Tektronix, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, increasing defense spending, and growing demand for high-precision power measurement in telecommunications and industrial applications.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to show the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with AI for predictive maintenance, and development of wide-bandwidth sensors for next-generation communication systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...