MARKET INSIGHTS

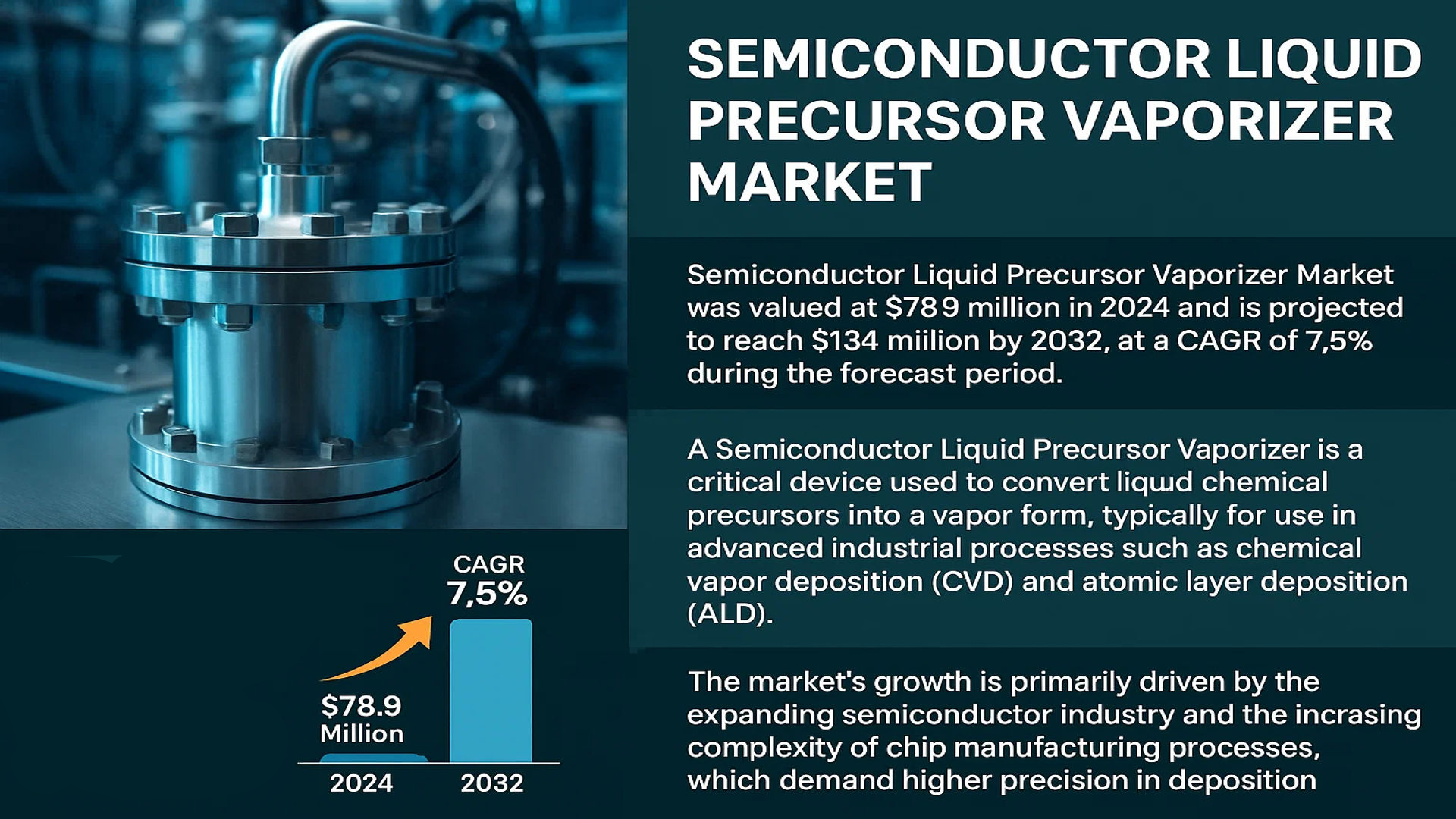

The global Semiconductor Liquid Precursor Vaporizer Market was valued at 78.9 million in 2024 and is projected to reach US$ 134 million by 2032, at a CAGR of 7.5% during the forecast period.

A Semiconductor Liquid Precursor Vaporizer is a critical device used to convert liquid chemical precursors into a vapor form, typically for use in advanced industrial processes such as chemical vapor deposition (CVD) and atomic layer deposition (ALD). These vaporizers are essential components in the fabrication of thin-film coatings and semiconductor devices, ensuring precise and controlled delivery of precursor materials.

The market’s growth is primarily driven by the expanding semiconductor industry and the increasing complexity of chip manufacturing processes, which demand higher precision in deposition techniques. Furthermore, advancements in 3D NAND and logic devices are pushing the need for more sophisticated vaporization systems. While the U.S. remains a significant market, China is rapidly emerging as a major consumer and producer, reflecting the broader geographical shift in semiconductor manufacturing. Key players such as HORIBA, Brooks Instrument, and Air Liquide dominate the market, continuously innovating to meet the stringent requirements of next-generation semiconductor fabrication.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Adoption of Advanced Semiconductor Fabrication Processes to Drive Market Expansion

The semiconductor industry’s relentless pursuit of miniaturization and enhanced performance is significantly driving demand for liquid precursor vaporizers. These critical components enable precise delivery of vaporized precursors in atomic layer deposition (ALD) and chemical vapor deposition (CVD) processes, which are fundamental to manufacturing advanced logic and memory chips. With the industry transitioning to sub-5nm technology nodes, the requirement for ultra-thin, conformal films has intensified, necessitating sophisticated vaporization systems. The global semiconductor equipment market, valued at over $100 billion annually, continues to grow at approximately 7-9% yearly, directly correlating with increased demand for precision deposition equipment. Furthermore, the proliferation of 3D NAND flash memory and advanced DRAM technologies requires increasingly complex multi-layer deposition processes, creating sustained demand for high-performance vaporization systems capable of handling diverse liquid precursors with exceptional consistency and control.

Expansion of Compound Semiconductor and Power Device Manufacturing to Fuel Growth

The rapid growth of compound semiconductors for power electronics, RF devices, and photonics applications represents a significant driver for the liquid precursor vaporizer market. Gallium nitride (GaN) and silicon carbide (SiC) device manufacturing, which is projected to grow at a compound annual growth rate of over 15% through 2030, heavily relies on metalorganic chemical vapor deposition (MOCVD) processes. These processes require precise vaporization of liquid metalorganic precursors at controlled temperatures and flow rates. The electric vehicle revolution, which utilizes power semiconductors extensively, has accelerated investment in compound semiconductor fabrication facilities worldwide. Additionally, the emerging market for micro-LED displays, expected to reach multi-billion dollar valuation by 2030, depends on sophisticated MOCVD processes that utilize advanced vaporization systems for consistent, high-quality epitaxial growth.

Increasing Complexity of Semiconductor Materials and Processes to Boost Demand

The semiconductor industry’s evolution toward novel materials and architectures is creating new opportunities for liquid precursor vaporizer systems. The integration of high-k dielectric materials, metal gates, and emerging materials such as ruthenium, cobalt, and two-dimensional materials requires specialized vaporization capabilities. The development of advanced packaging technologies, including 3D integration and heterogeneous packaging, demands precise deposition of barrier layers, seed layers, and insulating films. This complexity drives innovation in vaporizer design, particularly for precursors with challenging vaporization characteristics or thermal sensitivity. The market is responding with systems featuring improved temperature control, reduced memory effects, and enhanced compatibility with low-vapor-pressure precursors, enabling manufacturers to achieve the required film properties and process uniformity for next-generation semiconductor devices.

MARKET RESTRAINTS

High Capital Investment and Operational Costs to Limit Market Penetration

The significant capital expenditure required for advanced liquid precursor vaporizer systems presents a substantial barrier to market growth, particularly for smaller semiconductor manufacturers and research institutions. High-performance vaporizers designed for semiconductor applications typically incorporate sophisticated temperature control systems, precision flow controllers, and advanced materials resistant to corrosive precursors, resulting in manufacturing costs that can exceed $50,000 per unit. Additionally, the operational expenses associated with these systems, including maintenance, calibration, and consumable replacements, contribute to total cost of ownership concerns. The semiconductor industry’s cyclical nature further complicates investment decisions, as manufacturers may delay capital equipment purchases during market downturns. This financial barrier is particularly pronounced in emerging semiconductor markets where access to capital is more constrained.

Technical Complexity and Integration Challenges to Hinder Adoption

The integration of liquid precursor vaporizers into existing semiconductor fabrication processes presents significant technical challenges that restrain market growth. These systems must maintain precise temperature control within ±0.1°C to ensure consistent vaporization rates, requiring sophisticated thermal management systems. The phenomenon of precursor decomposition at elevated temperatures presents particular difficulties for thermally sensitive compounds, potentially leading to chamber contamination and process drift. Additionally, compatibility issues between vaporizer materials and aggressive precursors can cause corrosion, particle generation, and system degradation. The industry’s transition to multi-precursor processes further complicates system design, as vaporizers must maintain isolation between different chemicals while ensuring rapid switching capabilities. These technical hurdles require extensive engineering expertise and process development time, delaying implementation and increasing adoption costs.

Stringent Performance Requirements and Reliability Concerns to Constrain Growth

Semiconductor manufacturing demands exceptionally high levels of reliability and performance from all process equipment, creating significant challenges for liquid precursor vaporizer adoption. These systems must demonstrate mean time between failures exceeding 10,000 hours while maintaining process stability better than 1% variation over extended production runs. The industry’s zero-defect mentality leaves little tolerance for equipment-induced process variations or particulate contamination. Furthermore, the increasing use of exotic precursors with challenging physical properties exacerbates reliability concerns, as these materials often exhibit non-ideal vaporization behavior or thermal degradation characteristics. The requirement for rapid maintenance and minimal downtime creates additional pressure on vaporizer design, necessitating quick-disconnect features and simplified service procedures that can conflict with performance optimization. These stringent requirements force manufacturers to invest heavily in reliability engineering and quality control, increasing development costs and time to market.

MARKET CHALLENGES

Precursor Compatibility and Material Degradation Issues to Challenge Market Development

The semiconductor industry’s expanding portfolio of liquid precursors presents significant compatibility challenges for vaporizer systems. Many advanced precursors exhibit aggressive chemical properties that can degrade common construction materials, leading to particle generation, metal contamination, and system failure. The trend toward lower temperature processes necessitates vaporizers capable of handling precursors with reduced thermal stability, requiring innovative heating methodologies and material selections. Additionally, the industry’s movement toward aqueous-based precursors introduces corrosion concerns not present with traditional organic solvents. These compatibility issues necessitate extensive materials testing and precursor-specific system designs, increasing development costs and limiting system versatility. The challenge is particularly acute for foundries and memory manufacturers running diverse product mixes, as they require vaporizers capable of handling multiple precursors with varying chemical properties without cross-contamination or performance degradation.

Other Challenges

Process Uniformity and Repeatability Demands

Achieving and maintaining process uniformity across large substrate areas and over extended production runs represents a persistent challenge for liquid precursor vaporizer systems. Variations in vaporization efficiency, temperature distribution, and flow characteristics can lead to film thickness non-uniformities exceeding acceptable limits for advanced semiconductor devices. The industry’s transition to larger wafer sizes, particularly the adoption of 300mm and emerging 450mm platforms, exacerbates these challenges by requiring more uniform vapor distribution across increased surface areas. Additionally, the phenomenon of precursor depletion and concentration changes during vaporization can cause process drift over time, necessitating sophisticated compensation algorithms and real-time monitoring systems.

Technical Expertise and Knowledge Gap

The specialized nature of liquid precursor vaporization technology creates a significant knowledge gap that challenges market expansion. Effective system operation requires understanding of fluid dynamics, thermal management, precursor chemistry, and process integration—a combination of expertise rarely found in single individuals. This knowledge deficit is particularly problematic in emerging semiconductor regions where experienced process engineers are scarce. The complexity of troubleshooting vaporizer-related process issues often leads to extended downtime and yield learning cycles, discouraging adoption among risk-averse manufacturers. Furthermore, the proprietary nature of many vaporizer designs limits knowledge sharing and best practice development within the industry, perpetuating the expertise shortage.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Packaging and Heterogeneous Integration to Create New Growth Avenues

The rapid evolution of advanced packaging technologies presents substantial opportunities for liquid precursor vaporizer systems. The industry’s shift toward 2.5D and 3D integration, heterogeneous packaging, and system-in-package architectures requires sophisticated deposition processes for barrier layers, seed layers, and dielectric films. These applications often utilize liquid precursors with specific vaporization requirements that differ from traditional front-end processes. The advanced packaging market, growing at approximately 8% annually, represents a significant expansion opportunity for vaporizer manufacturers. Additionally, the emergence of through-silicon via (TSV) technology and fan-out wafer-level packaging demands conformal deposition in high-aspect-ratio features, requiring precise vapor delivery and concentration control that advanced vaporizer systems can provide. This market segment’s less stringent purity requirements compared to front-end processes also allows for more flexible system designs and faster innovation cycles.

Development of Sustainable and Environmentally Friendly Processes to Drive Innovation

Increasing environmental regulations and sustainability initiatives within the semiconductor industry are creating opportunities for next-generation liquid precursor vaporizer systems. The industry’s focus on reducing greenhouse gas emissions and hazardous chemical usage drives demand for vaporizers that minimize precursor consumption and waste generation. Advanced systems featuring reduced dead volume, improved vaporization efficiency, and enhanced precursor utilization can significantly decrease environmental impact while lowering operational costs. Additionally, the development of vaporizers compatible with greener alternative precursors presents innovation opportunities. The semiconductor industry’s commitment to achieving carbon neutrality by 2050, coupled with increasing regulatory pressure on perfluorocarbon emissions, incentivizes manufacturers to adopt more efficient deposition processes. This sustainability focus particularly benefits vaporizer systems capable of handling novel precursors with lower global warming potential and reduced environmental impact.

Integration of Industry 4.0 Technologies and Smart Manufacturing to Enable Premium Solutions

The integration of digital technologies and Industry 4.0 principles into semiconductor manufacturing equipment presents significant opportunities for liquid precursor vaporizer systems. Smart vaporizers featuring real-time monitoring, predictive maintenance capabilities, and digital twin integration can command premium pricing while providing tangible operational benefits. The ability to monitor precursor consumption, vaporization efficiency, and system health in real time enables proactive maintenance and reduces unscheduled downtime. Additionally, the collection and analysis of process data can provide insights for optimization and yield improvement. The semiconductor industry’s increasing adoption of smart manufacturing initiatives, with investments exceeding $5 billion annually in digital transformation, creates a receptive market for intelligent vaporizer systems. These advanced capabilities particularly appeal to high-volume manufacturers seeking to maximize equipment utilization and process stability through data-driven optimization and predictive analytics.

SEMICONDUCTOR LIQUID PRECURSOR VAPORIZER MARKET TRENDS

Miniaturization and Advanced Node Manufacturing to Drive Market Growth

The relentless pursuit of semiconductor miniaturization, particularly the transition to sub-5nm and sub-3nm process nodes, is fundamentally reshaping the requirements for deposition processes. This evolution necessitates unprecedented precision in precursor delivery, directly fueling demand for high-performance liquid precursor vaporizers. Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD) techniques, critical for creating ultra-thin, conformal films in advanced logic and memory devices, are heavily reliant on the consistent and controlled vaporization of liquid sources. The market is responding with innovations in vaporizer design that minimize precursor waste, enhance vapor purity by reducing particle generation, and improve process repeatability. This is paramount for high-volume manufacturing where a deviation of even a few percentage points in precursor flow can lead to significant yield loss. The global market, valued at 78.9 million in 2024, is projected to grow at a CAGR of 7.5%, reaching 134 million by 2032, largely propelled by these technological demands from leading-edge foundries and memory manufacturers.

Other Trends

Expansion of the Electric Vehicle and Renewable Energy Sectors

While advanced computing drives demand at one end, the massive expansion of the electric vehicle (EV) and renewable energy infrastructure is creating substantial growth in another segment. The production of power semiconductors, wide-bandgap materials like silicon carbide (SiC) and gallium nitride (GaN), and various sensors essential for EVs and solar inverters, all utilize ALD and CVD processes. These applications often require the deposition of specialized materials, such as high-κ dielectrics and metal barriers, which are delivered via liquid precursors. The robust growth in EV sales, which surpassed 10 million units globally in 2022 and continues to climb, directly correlates with increased manufacturing capacity for associated semiconductors. This, in turn, accelerates the adoption of liquid precursor vaporizers in fabrication facilities dedicated to automotive-grade chips, creating a diversified and resilient demand stream beyond traditional computing.

Geopolitical and Supply Chain Factors Influencing Regional Production

Geopolitical initiatives aimed at securing regional semiconductor supply chains are profoundly impacting equipment procurement patterns, including vaporizers. Policies like the U.S. CHIPS and Science Act and similar efforts in the European Union are catalyzing the construction of new fabrication plants and the expansion of existing ones outside of the traditional manufacturing hubs in Asia. This strategic decoupling or de-risking is leading to a more distributed global manufacturing footprint. Consequently, equipment suppliers are experiencing demand growth across multiple regions simultaneously. For instance, while China remains a massive market, the U.S. market is also expanding significantly, estimated at a multi-million dollar size in 2024. This trend necessitates that vaporizer manufacturers adapt their logistics, service, and support networks to a truly global scale, ensuring timely installation and maintenance for a geographically dispersed customer base, which presents both a challenge and an opportunity for market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Positioning Drive Market Leadership

The global Semiconductor Liquid Precursor Vaporizer market exhibits a semi-consolidated structure, characterized by the presence of several established players alongside emerging specialized manufacturers. These companies compete intensely on technological superiority, precision, reliability, and the ability to serve the demanding requirements of semiconductor fabrication processes like Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD). The market’s growth is intrinsically linked to the broader semiconductor industry’s expansion and its relentless pursuit of miniaturization and advanced material deposition techniques.

HORIBA stands as a dominant force in this market, leveraging its extensive expertise in measurement and analysis technologies. The company’s vaporizers are renowned for their high precision in flow control and stability, which are critical parameters for ensuring uniform thin-film deposition. Their strong global sales and distribution network, particularly across key semiconductor manufacturing hubs in Asia and North America, solidify their leading position. Furthermore, HORIBA’s significant investment in R&D focuses on enhancing vaporization efficiency for next-generation precursors, ensuring they remain at the forefront of innovation.

MSP Corporation (a TSI company) and Brooks Instrument also command significant market share. MSP is highly regarded for its expertise in aerosol science, which directly translates into advanced vaporizer designs that minimize particle generation and prevent precursor decomposition—a common challenge in the process. Brooks Instrument, a provider of advanced flow measurement and control solutions, leverages this core competency to offer vaporizers with exceptional accuracy and repeatability. The growth of these companies is propelled by their deep application knowledge and their ability to provide integrated solutions that include not just the vaporizer but also associated control systems.

Additionally, these leading players are actively pursuing growth through strategic initiatives. This includes geographical expansion into emerging semiconductor markets, new product launches designed for novel precursor chemistries, and technical collaborations with major semiconductor equipment OEMs and chemical suppliers. These efforts are crucial for capturing a larger share of the projected market growth.

Meanwhile, other notable players are strengthening their foothold. Air Liquide, primarily known as a industrial gas supplier, leverages its vast experience in gas delivery and handling to produce reliable and safe vaporization systems. LINTEC and KEMSTREAM are focusing on innovation and cost-competitive solutions to cater to a broader segment of the market. Companies based in Asia, such as Beijing Sevenstar Huachuang Meter, are growing their presence by effectively serving the massive domestic semiconductor industry in China, often focusing on providing robust and cost-effective alternatives.

List of Key Semiconductor Liquid Precursor Vaporizer Companies Profiled

- HORIBA (Japan)

- MSP (TSI) (U.S.)

- SIGA GmbH (Germany)

- Brooks Instrument (U.S.)

- LINTEC (Japan)

- KEMSTREAM (France)

- Air Liquide (France)

- SEMPA (France)

- Beijing Sevenstar Huachuang Meter (China)

Segment Analysis:

By Type

Direct Liquid Injection Type Segment Dominates Due to Superior Precision and Control in High-Volume Manufacturing

The market is segmented based on type into:

- Direct Liquid Injection Type

- Mixed Injection Type

- Others

By Application

Chemical Vapor Deposition (CVD) Segment Leads Due to its Pivotal Role in Advanced Semiconductor Fabrication

The market is segmented based on application into:

- Atomic Layer Deposition (ALD)

- Chemical Vapor Deposition (CVD)

- Others

By End User

Integrated Device Manufacturers (IDMs) Segment Leads Due to Extensive In-House Manufacturing Requirements

The market is segmented based on end user into:

- Integrated Device Manufacturers (IDMs)

- Foundries

- Research and Development Institutes

Regional Analysis: Semiconductor Liquid Precursor Vaporizer Market

Asia-Pacific

The Asia-Pacific region dominates the global Semiconductor Liquid Precursor Vaporizer market, accounting for over 60% of worldwide consumption due to its concentration of semiconductor manufacturing facilities. China, Taiwan, South Korea, and Japan serve as the primary hubs, driven by massive investments in semiconductor fabrication plants (fabs) and government initiatives like China’s “Made in China 2025” and South Korea’s K-Semiconductor Strategy. The region’s growth is propelled by the increasing adoption of advanced nodes (below 10nm) in logic and memory devices, which require precise vaporization for Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD) processes. While cost-competitive manufacturing remains a key characteristic, there is a noticeable shift toward higher-precision vaporizers to meet the stringent requirements of next-generation semiconductor production. Local manufacturers are gaining traction, but international players maintain significant technological leadership.

North America

North America represents a technologically advanced and innovation-driven market for Semiconductor Liquid Precursor Vaporizers, characterized by high R&D investment and the presence of leading semiconductor equipment manufacturers and foundries. The United States, in particular, is a significant market due to its robust semiconductor industry and initiatives such as the CHIPS and Science Act, which allocates substantial funding to bolster domestic semiconductor manufacturing capabilities. This region emphasizes cutting-edge technology, with a strong focus on vaporizers that offer superior precision, reliability, and compatibility with complex precursor chemistries used in advanced processing. Environmental and safety regulations also influence product development, pushing manufacturers toward designs that minimize waste and enhance process control. The demand is primarily driven by logic and memory production, as well as emerging applications in compound semiconductors.

Europe

Europe holds a mature yet steadily growing segment of the Semiconductor Liquid Precursor Vaporizer market, supported by a strong research ecosystem and presence of key semiconductor manufacturers and equipment suppliers. Countries like Germany, France, and the Netherlands are central to the region’s activity, with a focus on specialized semiconductor applications such as power devices, sensors, and MEMS. The market is driven by the need for high-precision vaporization in R&D institutions and production facilities, with an emphasis on process repeatability and material efficiency. Strict environmental regulations under the EU’s REACH directive influence the adoption of vaporizers that can handle newer, more environmentally benign precursors safely. While the region may not match the volume growth of Asia-Pacific, it remains critical for technological innovation and high-value manufacturing.

South America

The Semiconductor Liquid Precursor Vaporizer market in South America is nascent and relatively small compared to other regions. Limited local semiconductor manufacturing infrastructure and economic volatility restrain market growth. However, countries like Brazil are making gradual investments in electronics production, which could spur demand for deposition equipment over the long term. The market currently relies heavily on imports, with vaporizers primarily used in research laboratories and small-scale production. Cost sensitivity is a significant factor, and adoption of advanced vaporizer technologies is slow. Nonetheless, the region presents potential opportunities for suppliers as industrial and technological development initiatives gain momentum.

Middle East & Africa

The Middle East & Africa region represents an emerging market with minimal current demand for Semiconductor Liquid Precursor Vaporizers. The lack of a significant semiconductor manufacturing base limits immediate growth prospects. However, select countries, particularly in the Middle East, are investing in technology diversification as part of broader economic visions, such as Saudi Arabia’s Vision 2030. These initiatives could eventually drive demand for semiconductor fabrication equipment, including vaporizers, particularly for research and specialized production. At present, the market is characterized by infrequent, project-based demand, often linked to academic or government research institutions. Long-term growth will depend on sustained investment in high-tech industrial infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the global Semiconductor Liquid Precursor Vaporizer market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Liquid Precursor Vaporizer Market?

-> Semiconductor Liquid Precursor Vaporizer Market was valued at 78.9 million in 2024 and is projected to reach US$ 134 million by 2032, at a CAGR of 7.5% during the forecast period.

Which key companies operate in Global Semiconductor Liquid Precursor Vaporizer Market?

-> Key players include HORIBA, MSP (TSI), SIGA GmbH, Brooks Instrument, LINTEC, KEMSTREAM, Air Liquide, SEMPA, and Beijing Sevenstar Huachuang Meter, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for advanced semiconductor manufacturing, expansion of ALD and CVD processes, and increasing investments in fab capacity.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include development of high-precision vaporization systems, integration with Industry 4.0 technologies, and focus on reducing precursor waste.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...