Liquid Cooling for AI Data Center Chips Market Insights

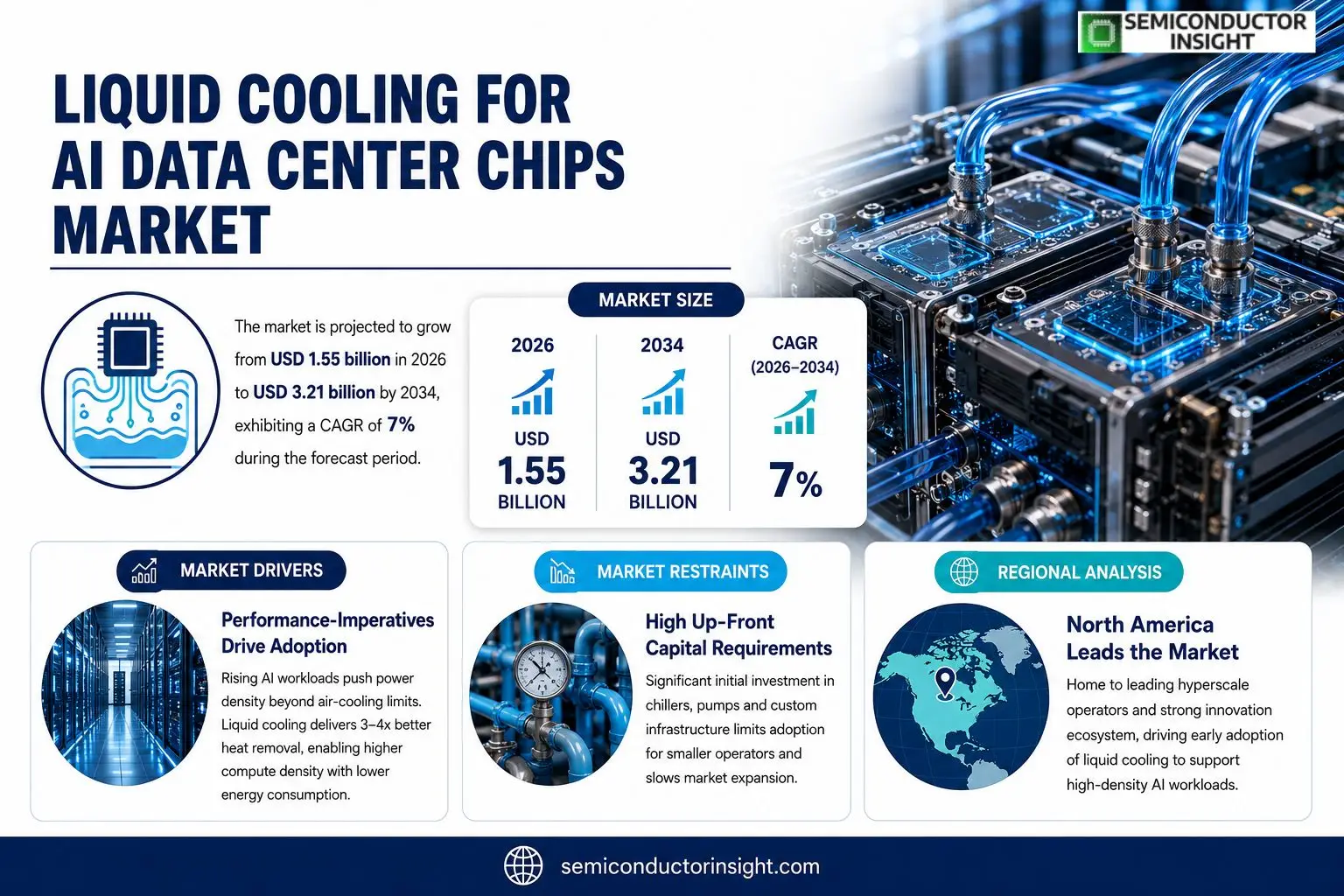

Liquid Cooling for AI Data Center Chips Market size was valued at USD 1.45 billion in 2025. Forecasts indicate expansion from USD 1.55 billion in 2026 to USD 3.21 billion by 2034, delivering a compound annual growth rate of roughly 7 % over the period.

Liquid cooling solutions designed for AI‑focused processors employ direct‑to‑chip coolant delivery or immersion techniques that remove heat more efficiently than traditional air‑based methods. By circulating dielectric fluids close to high‑power‑density silicon dies,often exceeding thermal design power (TDP) levels of 400 W per chip,these systems maintain optimal operating temperatures while reducing energy consumption associated with fans and HVAC equipment.The upward trajectory stems from surging demand for generative‑AI workloads that push compute density beyond conventional limits; consequently operators seek thermal management that preserves performance headroom without inflating power costs. Moreover, leading vendors such as Nvidia, IBM and CoolIT Systems have announced joint programs integrating custom coolant formulations with next‑generation GPU/TPU modules, reinforcing adoption across hyperscale facilities worldwide.

MARKET DRIVERS

Performance Imperatives Drive Adoption

The relentless increase in AI model complexity forces data center operators to pack more compute per square foot. When power density breaches 200 W/ft², traditional air‑cooling systems struggle to keep temperatures within safe margins, prompting a swift migration toward Liquid Cooling for AI Data Center Chips Market solutions that can dissipate heat at three‑to‑four times the efficiency of conventional methods.

Energy Cost Pressures Accelerate Shift

Utilities in major AI hubs now charge up to 15 % more per kilowatt‑hour for peak demand, making the energy savings from liquid cooling financially compelling. Facilities that deploy closed‑loop chillers report up to a 30 % reduction in overall PUE, translating into multi‑million‑dollar operational benefits over a five‑year horizon.

➤ The average power density of AI accelerators topped 250 W/ft² in 2023, driving a 60 % surge in liquid‑cooling deployments across hyperscale sites.

From a strategic standpoint, the capital outlay for liquid‑cooling infrastructure is increasingly justified by the ability to maintain higher compute loads without expanding rack footprints, thereby deferring costly real‑estate expansions.

MARKET CHALLENGES

Integration Complexity Hinders Rapid Rollout

Designing servers around liquid‑cooling loops demands a redesign of motherboard layouts, sealing mechanisms, and coolant routing. Early‑stage adopters often encounter delays as OEMs and integrators calibrate leak‑proof assemblies, a process that can add 3–4 weeks to deployment timelines.

Other Challenges

Maintenance Skill Gap

Technicians accustomed to air‑based HVAC lack the certification to service high‑pressure coolant systems, forcing firms to invest in specialized training programs or outsource to niche service providers, both of which inflate operating expenses.Reliability assurances also present a hurdle; while liquid cooling reduces thermal throttling, any coolant contamination incident can precipitate catastrophic chip failures, compelling operators to adopt rigorous monitoring protocols that further complicate day‑to‑day management.

MARKET RESTRAINTS

High Up‑Front Capital Requirements

Initial investment for a fully engineered liquid‑cooling deployment,including chillers, pumps, and custom‑fabricated rack kits,easily exceeds $150 k per 100‑rack module. Smaller operators, lacking deep cash reserves, view this outlay as a barrier to entry, especially when ROI calculations hinge on uncertain AI workload growth.

Regulatory and Safety Compliance Adds Overhead

Handling refrigerants and potable‑grade coolants subjects data centers to environmental and occupational health regulations. Compliance audits require detailed documentation and periodic testing, inflating both administrative and engineering costs.Furthermore, the limited number of certified component suppliers concentrates market power among a handful of vendors, restricting price negotiations and slowing innovation diffusion across the broader ecosystem.

MARKET OPPORTUNITIES

Edge Data Centers as Growth Vectors

Edge deployments, positioned close to end‑users for latency‑critical AI inference, often operate within constrained footprints where air cooling cannot meet thermal ceilings. Deploying compact liquid‑cooling modules enables edge operators to host high‑density AI chips without compromising space or energy efficiency.

Modular Cooling Kits Accelerate Time‑to‑Market

Vendors are now offering plug‑and‑play liquid‑cooling kits that integrate with standard 4‑U server form factors. This modularity reduces engineering lead times by up to 40 %, allowing cloud providers to respond swiftly to spikes in AI demand.

Chip‑Level Immersion Technologies Open New Revenue Streams

Emerging AI silicon that tolerates direct dielectric immersion eliminates the need for traditional cold‑plate interfaces. Companies that can bundle immersion‑ready chips with turnkey cooling infrastructure are positioned to capture a premium share of the next wave of AI hardware spend.

Liquid Cooling for AI Data Center Chips Market Trends

Shift Toward Direct‑to‑Chip Liquid Cooling

Operators are replacing traditional air‑based heat exchangers with systems that pump dielectric fluid directly onto the silicon surface of AI‑focused processors. Because modern GPUs and TPUs routinely exceed 400 W of thermal design power, the liquid pathway provides a tighter temperature margin and cuts fan‑related electricity by roughly 20 %. The reduction in cooling‑related power draw translates into lower operational expenses, while the more uniform heat removal frees headroom for sustained burst workloads. In practice, data‑center operators report that direct‑to‑chip solutions enable higher rack densities without triggering thermal throttling, a benefit that directly supports the economics of generative‑AI services.

Other Trends

Immersion Cooling Gains Traction

Immersion tanks, filled with non‑conductive fluids, are moving from pilot projects to production‑scale deployments in hyperscale facilities. By submerging entire server boards, these installations eliminate the need for individual cold plates and simplify cabling, which reduces both capital outlay and failure points. Early adopters have demonstrated that immersion can sustain power densities above 600 W per unit, a level that would overwhelm conventional air systems. The technology also eases humidity control requirements, allowing facilities to concentrate on power‑efficiency measures rather than climate‑management. As more vendors certify hardware for fluid compatibility, the barrier to entry for immersion cooling continues to erode.

Vendor‑Led Integration Programs

Major chip makers and cooling specialists are formalizing joint development programs that bundle custom coolant formulations with next‑generation AI accelerators. These collaborations shorten validation cycles, giving data‑center owners a plug‑and‑play pathway to upgrade aging infrastructure. From a procurement perspective, the bundled approach reduces the total cost of ownership because it aligns warranty terms and streamlines spare‑parts inventories. For service providers, the ability to promise consistent thermal performance across heterogeneous hardware simplifies capacity planning and improves service‑level agreements. The unifying effect of these programs is reshaping supply‑chain dynamics, encouraging OEMs to favor partners that can deliver an integrated cooling‑hardware ecosystem.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics Shaping the Liquid‑Cooling Landscape for AI Chips

At the forefront of the ecosystem, Nvidia anchors the market by integrating proprietary liquid‑cooling channels directly into its high‑performance GPU families. The company’s partnership framework with CoolIT Systems and IBM enables joint engineering of dielectric fluids that match the thermal envelope of next‑generation AI accelerators. This collaboration not only shortens time‑to‑deployment for hyperscale operators but also establishes a de‑facto standard for coolant‑to‑die interfaces, compelling downstream system integrators to adopt compatible designs. The resulting concentration around a few technology stacks creates a tiered supply chain where OEMs such as Dell Technologies and Hewlett Packard Enterprise build full‑rack solutions around the Nvidia‑CoolIT reference architecture, while niche specialists concentrate on peripheral components like pumps, heat exchangers and monitoring software.Beyond the marquee alliances, a cadre of specialized vendors is carving out distinct niches. Asetek and Tangent Solutions focus on compact, retrofit‑ready modules for edge data centers, leveraging modular pump designs that appeal to customers with limited floor space. Companies such as Supermicro and Lenovo differentiate by embedding liquid‑cooling loops within blade servers, targeting AI‑intensive workloads that demand density without sacrificing serviceability. Meanwhile, emerging firms like CoolData, GRC (Green Revolution Cooling) and Iceotope invest heavily in immersion‑cooling chemistries, arguing that direct submersion offers superior thermal headroom for future AI chips exceeding 600 W TDP. These players collectively broaden the competitive set, ensuring that procurement decisions hinge on a balance of performance, cost of ownership and ecosystem compatibility.

List of Key Liquid Cooling for AI Data Center Chips Companies Profiled

- Nvidia

- CoolIT Systems

- IBM

- Dell Technologies

- Hewlett Packard Enterprise

- Intel

- Supermicro

- Lenovo

- Asetek

- Tangent Solutions

- CoolData

- GRC (Green Revolution Cooling)

- Iceotope

- AMD

- Google Cloud

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Direct‑to‑Chip delivers coolant directly to the silicon surface, enabling rapid heat extraction from high‑power‑density AI accelerators; ‑ It integrates seamlessly with existing rack architectures, minimizing disruption for operators; ‑ The approach supports modular upgrades, allowing data centers to scale cooling capacity in line with evolving AI workloads. |

| By Application |

|

Training Accelerators dominate because intensive generative‑AI models generate sustained high thermal loads; ‑ Liquid cooling preserves performance headroom, reducing throttling during prolonged training cycles; ‑ Vendors are co‑designing custom coolant formulations with GPU/TPU manufacturers to maximize thermal conductivity while maintaining electrical safety. |

| By End User |

|

Hyperscale Cloud Providers lead adoption due to the need for relentless compute density and cost‑effective power usage; ‑ They evaluate total‑facility energy footprints, preferring liquid cooling for its ability to lower fan and HVAC loads; ‑ Strategic partnerships with silicon vendors ensure that cooling solutions are embedded early in the design pipeline, accelerating deployment cycles. |

| By Cooling Architecture |

|

Closed‑Loop External Systems are favored for large‑scale deployments because they provide predictable coolant circulation and easy maintenance; ‑ Their modular design aligns with rack‑level standardization, helping operators expand capacity without major retrofits; ‑ Continuous fluid monitoring enhances reliability, a critical factor for mission‑critical AI workloads. |

| By Integration Strategy |

|

OEM‑Embedded Cooling Modules are emerging as the preferred pathway for next‑generation AI chips; ‑ By embedding coolant delivery channels within the processor package, latency is minimized and thermal uniformity is maximized; ‑ Collaborative programs among silicon designers, coolant manufacturers, and system integrators accelerate market acceptance and drive innovation. |

Regional Analysis: Liquid Cooling for AI Data Center Chips Market

North America

Leading hyperscalers allocate a sizable portion of their capex to retrofit legacy halls with liquid‑cooling loops, recognizing that thermal headroom directly translates into compute density. This investment trend fuels a cascade of demand for modular heat exchangers and high‑efficiency pumps, encouraging vendors to standardize components that can be deployed at scale.

Federal incentives tied to carbon‑reduction targets have been calibrated to favor technologies that lower PUE (Power Usage Effectiveness). By linking grant eligibility to demonstrable cooling efficiency, policymakers indirectly accelerate the market uptake of liquid‑cooling architectures for AI chips.

Universities along the West Coast and in the Midwest have launched interdisciplinary programs that blend thermal‑fluid dynamics with semiconductor design. Graduates from these programs quickly become assets for firms seeking to integrate cooling considerations early in chip architecture, shortening development cycles.

Enterprise AI labs report that liquid‑cooled racks enable sustained inference workloads without throttling, which directly improves service‑level agreements. This operational advantage drives a willingness to experiment with higher‑density board designs that would otherwise be untenable under air cooling.

Europe

European data‑center operators are navigating a fragmentary regulatory landscape that varies from country to country, yet the overarching emphasis on sustainability creates a shared incentive for liquid‑cooling adoption. Major cloud providers in Germany and the Nordics have begun pilot projects that pair AI accelerators with sealed‑loop cooling modules, citing lower acoustic footprints and reduced auxiliary power consumption. The region’s mature engineering ecosystem, anchored by precision‑manufacturing hubs in France and Italy, supplies high‑quality components such as custom‑machined cold plates. While capital allocation remains cautious compared with North America, the convergence of ESG reporting requirements and a growing pool of green‑finance capital is nudging the market toward broader deployment over the next few years.

Asia‑Pacific

The Asia‑Pacific market is characterized by rapid data‑center construction in emerging economies, but the pace of liquid‑cooling integration differs markedly across the sub‑region. In Japan and South Korea, early‑stage collaborations between semiconductor fabs and cooling specialists have yielded turnkey solutions that are being rolled out in urban edge facilities. Conversely, in India and Southeast Asia, the primary barrier remains the high upfront cost of retrofitting existing halls, prompting operators to favor modular, pre‑engineered cooling pods that can be added incrementally. Nonetheless, the surge in AI‑driven services, coupled with tightening energy‑efficiency standards in China, is prompting a strategic reassessment of thermal management approaches.

South America

South American data‑center operators are still in the exploratory phase of liquid‑cooling technology. The region’s electricity pricing volatility drives a pragmatic interest in solutions that can smooth peak demand, yet limited local expertise hampers large‑scale rollout. Partnerships with North American vendors are emerging, allowing South American firms to import proven designs while training local engineers. Brazil’s recent tax incentives for energy‑efficient equipment are expected to catalyze the first wave of commercial deployments, particularly in financial‑services data hubs that require consistent latency for AI workloads.

Middle East & Africa

In the Middle East, ultra‑hot ambient conditions make air cooling increasingly untenable for high‑performance AI clusters, prompting a shift toward liquid‑cooling theorems that can maintain chip temperatures within safe margins. Sovereign wealth funds have begun allocating a portion of their technology portfolios to companies developing closed‑loop cooling systems, viewing them as strategic assets for national AI initiatives. Across Africa, the market remains nascent, but pilot projects in South Africa’s fintech sector are testing low‑cost, modular cooling kits that leverage locally sourced coolant fluids, indicating a potential pathway for scalable adoption as broadband penetration improves.

Report Scope

This market research report provides a comprehensive analysis of the Liquid Cooling for AI Data Center Chips Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Liquid Cooling for AI Data Center Chips Market?

-> Liquid Cooling for AI Data Center Chips Market was valued at USD 1.45 billion in 2025 and is expected to reach USD 3.21 billion by 2034, reflecting a compound annual growth rate of approximately 7 % over the forecast period.

Which key companies operate in Liquid Cooling for AI Data Center Chips Market?

-> Key players include Nvidia, IBM, and CoolIT Systems, among other technology leaders driving integration of custom coolant formulations with next‑generation AI processors.

What are the key growth drivers?

-> Key growth drivers include surging demand for generative‑AI workloads, the need for higher compute density, and the pursuit of energy‑efficient thermal management solutions that lower fan and HVAC power consumption.

Which region dominates the market?

-> Adoption is strongest in North America and Asia‑Pacific, where hyperscale data‑center operators are rapidly deploying liquid‑cooling implementations to support AI acceleration.

What are the emerging trends?

-> Emerging trends include direct‑to‑chip coolant delivery, immersion cooling techniques, and the development of bespoke dielectric fluids tailored for high‑power‑density AI chips.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...