MARKET INSIGHTS

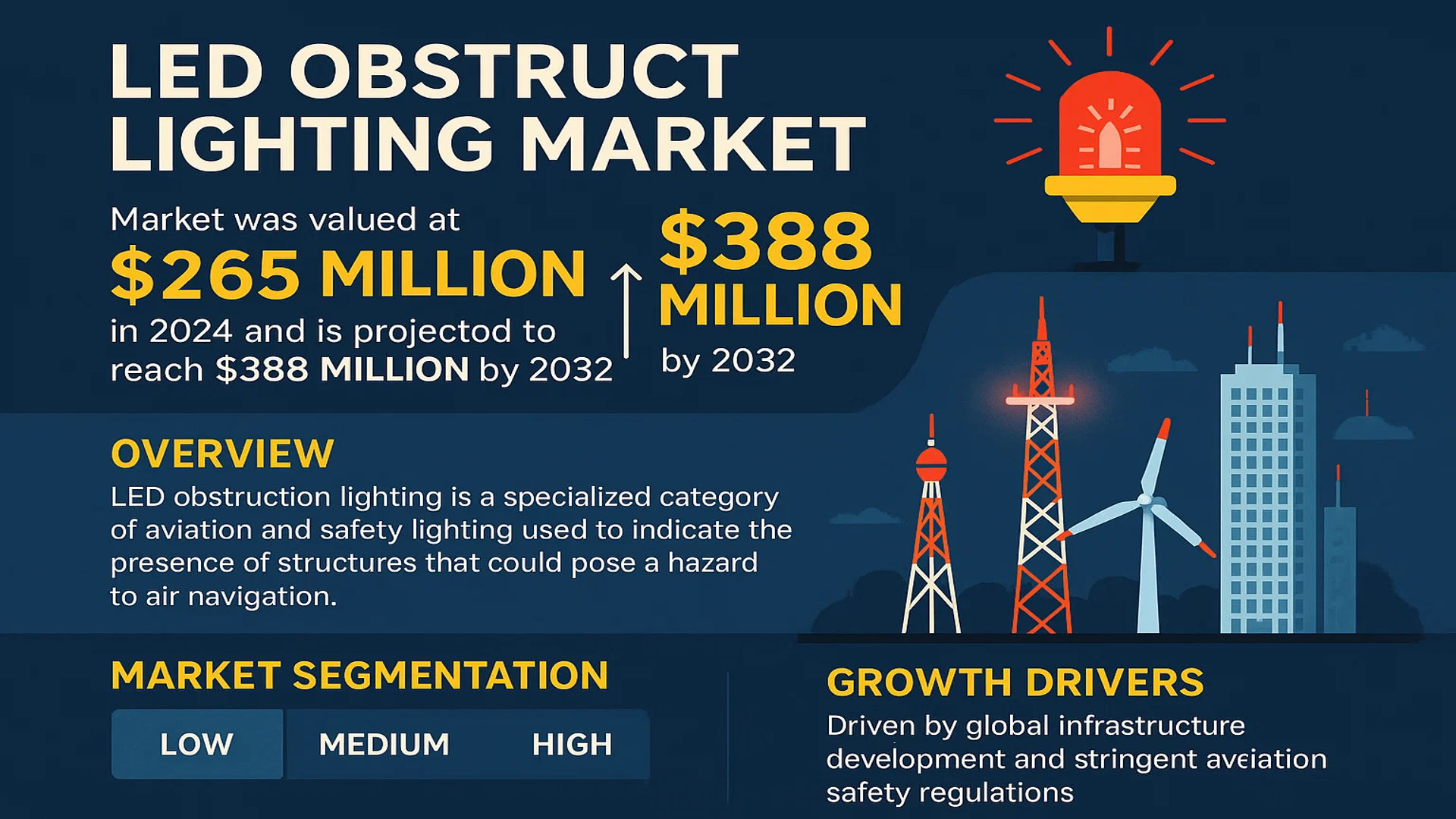

The global LED Obstruct Lighting Market was valued at 265 million in 2024 and is projected to reach US$ 388 million by 2032, at a CAGR of 5.7% during the forecast period.

LED obstruction lighting is a specialized category of aviation and safety lighting used to indicate the presence of structures that could pose a hazard to air navigation. These lights are crucial for ensuring the safety of low-flying aircraft, particularly near tall structures like telecommunication towers, wind turbines, bridges, and skyscrapers. They are designed for high reliability, long service life, and low power consumption, with products segmented by intensity into low, medium, and high-intensity types to meet specific regulatory requirements.

The market’s steady growth is primarily driven by global infrastructure development and stringent aviation safety regulations mandated by bodies like the FAA and ICAO. Furthermore, the ongoing shift from traditional incandescent lighting to energy-efficient LED technology, which offers superior longevity and reduced maintenance costs, is a significant catalyst. Geographically, China dominates consumption with a 29% market share, followed by North America (25%) and Europe (17%), reflecting their extensive investments in telecommunications and renewable energy infrastructure. Key players such as Hughey & Phillips, Dialight, and Orga Aviation collectively hold about 26% of the global market, competing through technological innovation and expansive product portfolios.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Growth in Infrastructure Development and Aviation Safety Regulations to Drive Market Expansion

The global LED obstruct lighting market is experiencing robust growth driven by increasing infrastructure development and stringent aviation safety regulations. The construction of high-rise buildings, telecommunication towers, wind turbines, and bridges has surged, necessitating reliable obstruction lighting systems to ensure air traffic safety. Regulatory bodies worldwide mandate the installation of obstruction lights on structures exceeding certain heights, with specifications often requiring energy-efficient and high-visibility LED solutions. The International Civil Aviation Organization (ICAO) and Federal Aviation Administration (FAA) standards have been updated to include LED technology due to its superior performance characteristics. This regulatory push, combined with global infrastructure investments exceeding $9 trillion annually, creates sustained demand for LED obstruction lighting systems across both developed and emerging economies.

Energy Efficiency and Cost Savings to Accelerate LED Adoption

The transition from traditional incandescent and halogen obstruction lighting to LED technology represents a significant driver for market growth. LED obstruct lights consume up to 80% less energy than conventional lighting systems while providing superior reliability and lifespan. This energy efficiency translates to substantial operational cost savings, particularly for structures requiring 24/7 illumination. The maintenance reduction is equally impactful, with LED systems offering lifespans exceeding 100,000 hours compared to approximately 10,000 hours for traditional lighting. These economic advantages are particularly compelling for large-scale applications such as wind farms, where a single facility may require hundreds of obstruction lights. The total cost of ownership calculation strongly favors LED technology, driving replacement and new installation demand across all market segments.

Technological Advancements and Smart Lighting Integration to Fuel Market Growth

Recent technological advancements in LED obstruct lighting are creating new growth opportunities across the market. The integration of smart monitoring systems, remote diagnostics, and predictive maintenance capabilities represents a significant value addition for end-users. Modern LED obstruction lights now incorporate light sensors, wireless connectivity, and automated reporting features that enhance operational reliability while reducing maintenance costs. The development of solar-powered LED systems has expanded applications to remote locations without reliable grid power. Furthermore, advancements in photometrics and optical design have improved visibility range and compliance with international aviation standards. These technological innovations are driving premium product adoption and creating differentiation opportunities for manufacturers in an increasingly competitive market landscape.

MARKET RESTRAINTS

High Initial Investment Costs to Limit Market Penetration in Price-Sensitive Regions

Despite the long-term cost benefits, the high initial investment required for LED obstruct lighting systems presents a significant restraint for market growth, particularly in developing economies and price-sensitive applications. LED obstruction lights typically command a premium of 40-60% over conventional lighting solutions, creating budgetary challenges for projects with constrained capital expenditure. This cost barrier is especially pronounced in emerging markets where infrastructure development is rapid but funding limitations persist. The sophisticated electronics, specialized materials, and certification requirements for aviation-grade lighting contribute to the higher manufacturing costs. While the return on investment is favorable over the product lifecycle, the upfront cost differential can deter adoption in markets where initial cost considerations outweigh long-term operational savings.

Complex Regulatory Compliance and Certification Requirements to Hinder Market Entry

The LED obstruct lighting market faces significant challenges related to complex regulatory compliance and certification requirements. Products must meet stringent international standards set by organizations including ICAO, FAA, and various national aviation authorities. The certification process involves rigorous testing for photometric performance, environmental durability, reliability, and electromagnetic compatibility. This process can take several months and requires substantial investment in testing facilities and documentation. The complexity increases when products must be certified for multiple regions with differing standards. These regulatory hurdles create barriers to entry for new market participants and can delay product launches even for established manufacturers. The ongoing need to maintain certifications amid evolving standards adds further complexity and cost to market participation.

Technical Limitations in Extreme Environmental Conditions to Constrain Application Scope

LED obstruct lighting systems face performance limitations in extreme environmental conditions that restrict their application scope in certain geographic regions and installations. While LED technology generally offers excellent reliability, specific challenges emerge in environments with temperature extremes, high humidity, salt exposure, or severe weather conditions. Performance degradation can occur in temperatures exceeding 60°C or below -40°C, limiting suitability for desert or arctic applications. Coastal installations face corrosion challenges despite protective measures. Additionally, the visibility range of LED systems can be affected by heavy precipitation, fog, or atmospheric conditions, requiring careful site-specific engineering solutions. These technical constraints necessitate specialized product designs for extreme environments, increasing development costs and limiting the addressable market for standard products.

MARKET CHALLENGES

Intense Price Competition and Market Fragmentation to Challenge Profitability

The LED obstruct lighting market is characterized by intense price competition and significant fragmentation, creating challenges for manufacturer profitability and sustainable growth. The market includes numerous participants ranging from specialized aviation lighting companies to general lighting manufacturers expanding into obstruction applications. This diversity creates pricing pressure as competitors seek market share through aggressive pricing strategies. The situation is exacerbated by the presence of regional manufacturers offering products at substantially lower price points, though sometimes with compromised quality or certification compliance. This competitive landscape forces established players to balance quality maintenance with cost competitiveness, often compressing profit margins. The challenge is particularly acute in emerging markets where price sensitivity is high and regulatory enforcement may be less stringent.

Other Challenges

Supply Chain Vulnerabilities

Global supply chain disruptions present ongoing challenges for LED obstruct lighting manufacturers. The industry relies on specialized components including high-output LEDs, optical materials, and electronic drivers that may have limited sourcing options. Recent global events have highlighted vulnerabilities in extended supply chains, causing production delays and cost increases. The specialized nature of aviation-grade components further complicates sourcing, as alternative suppliers must undergo rigorous qualification processes. These supply chain challenges affect production scheduling, inventory management, and ultimately customer satisfaction across the market.

Technological Obsolescence Risk

Rapid technological advancement creates obsolescence risks for both products and manufacturing processes. The LED technology itself continues to evolve with improvements in efficiency, longevity, and cost-effectiveness. Manufacturers must continuously invest in research and development to maintain competitiveness while managing the transition from older product generations. This requires balancing inventory management of current products with development of next-generation solutions. The pace of change also affects manufacturing equipment and processes, requiring ongoing capital investment to maintain production efficiency and quality standards.

MARKET OPPORTUNITIES

Expansion of Renewable Energy Infrastructure to Create Substantial Growth Opportunities

The global expansion of renewable energy infrastructure, particularly wind power generation, presents substantial growth opportunities for the LED obstruct lighting market. The wind energy sector requires reliable obstruction lighting for turbine arrays that can reach heights exceeding 200 meters. With global wind power capacity projected to grow significantly over the next decade, the demand for specialized obstruction lighting systems is expected to increase correspondingly. Offshore wind farms represent an especially promising segment due to their remote locations and demanding environmental conditions that necessitate robust, maintenance-free lighting solutions. The specific requirements of renewable energy applications, including compatibility with remote monitoring systems and minimal maintenance needs, create opportunities for innovative LED lighting solutions tailored to this growing market segment.

Emerging Smart City Initiatives and 5G Infrastructure Deployment to Drive Future Demand

Emerging smart city initiatives and the global deployment of 5G telecommunications infrastructure are creating new opportunities for LED obstruct lighting applications. Smart city projects often involve the construction of tall structures for various purposes including communication, surveillance, and environmental monitoring. These structures require compliant obstruction lighting integrated with broader smart city systems. The rollout of 5G networks necessitates numerous new towers and antenna installations, many exceeding height thresholds requiring obstruction lighting. The integration capabilities of modern LED systems allow for seamless incorporation into network management systems, providing operational benefits beyond basic safety compliance. This convergence of infrastructure development and digitalization represents a significant growth vector for advanced LED obstruction lighting solutions.

Retrofit and Replacement Market to Offer Sustained Long-Term Opportunities

The extensive installed base of conventional obstruction lighting systems represents a substantial opportunity for LED retrofits and replacements. Many existing structures currently use older technology that consumes excessive energy, requires frequent maintenance, and may not meet updated regulatory standards. The compelling economic case for LED retrofits, combined with regulatory updates mandating improved lighting performance, creates a sustained replacement market. This opportunity spans various structure types including communication towers, high-rise buildings, bridges, and industrial facilities. The retrofit market requires specific product designs that accommodate existing mounting structures and electrical systems while delivering improved performance. Manufacturers developing tailored retrofit solutions can access this substantial market segment without depending solely on new construction activity, providing more stable long-term growth prospects.

LED OBSTRUCT LIGHTING MARKET TRENDS

Integration of Smart Technologies and IoT to Emerge as a Dominant Trend

The global LED obstruct lighting market is undergoing a significant transformation driven by the integration of smart technologies and the Internet of Things (IoT). This trend is revolutionizing how airspace safety is managed by enabling remote monitoring, predictive maintenance, and real-time status reporting of lighting systems. Modern LED obstruction lights are increasingly equipped with sensors and communication modules that allow for centralized control systems to detect failures instantly, schedule maintenance proactively, and optimize energy consumption based on ambient light conditions and weather patterns. This shift towards intelligent systems is not merely an enhancement but a fundamental change in operational efficiency, reducing downtime and manual inspection costs. Furthermore, regulatory bodies are beginning to encourage or mandate such smart features for critical infrastructure, creating a substantial new revenue stream for manufacturers who can offer these advanced, connected solutions. The demand for these sophisticated systems is particularly strong in the development of new urban high-rises and expansive wind farms, where reliable, low-maintenance safety lighting is paramount.

Other Trends

Rapid Expansion of Renewable Energy Infrastructure

The global push towards renewable energy is a powerful driver for the LED obstruct lighting market, particularly for wind energy applications. The construction of new wind farms, especially large-scale offshore installations, requires robust and highly reliable obstruction lighting to ensure aviation safety. These environments demand lights that can withstand harsh marine conditions, high winds, and salt spray corrosion, pushing manufacturers to develop more durable and resilient products. The number of wind turbines installed globally continues to climb, each requiring lighting systems, which directly correlates to market growth. This sector’s specific needs are catalyzing innovation in product design, focusing on longer lifespans and lower power consumption to align with the sustainable ethos of the renewable energy industry itself.

Stringent Regulatory Standards and Safety Compliance

Globally, aviation safety regulations mandated by bodies like the International Civil Aviation Organization (ICAO) and the Federal Aviation Administration (FAA) are becoming increasingly stringent, compelling the adoption of advanced LED obstruction lighting systems. These regulations specify precise technical requirements for light intensity, beam divergence, color, and flash characteristics based on structure height and location. The phasing out of older incandescent and halogen lighting technologies in favor of energy-efficient and more reliable LEDs is often a core component of these updated standards. This regulatory pressure ensures a consistent replacement market as existing structures must retrofit their lighting systems to remain compliant. This creates a stable, long-term demand driver that is less susceptible to economic fluctuations than new construction markets, providing a solid foundation for continued industry growth.

Geographic Market Expansion and Infrastructure Development

While North America and Europe are mature markets driven by retrofit and regulatory compliance, the Asia-Pacific region, led by China, represents the largest and fastest-growing consumption area. This growth is intrinsically linked to massive investments in infrastructure development, including the construction of skyscrapers, long-span bridges, telecommunication towers, and transportation networks. China’s significant market share is a direct result of its rapid urbanization and extensive investments in both civil and industrial infrastructure projects. This regional growth necessitates a corresponding installation of safety lighting, making geographic expansion into emerging economies a critical trend for market players seeking to capture new opportunities and increase their global footprint beyond established regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Global Expansion to Secure Market Position

The global LED obstruct lighting market exhibits a semi-consolidated structure, characterized by the presence of established multinational corporations, specialized mid-sized firms, and emerging regional manufacturers. Hughey & Phillips, Dialight, and Orga Aviation collectively command a significant portion of the market, holding approximately 26% of the global revenue share as of 2024. Hughey & Phillips maintains its leadership position due to its extensive product portfolio compliant with stringent FAA and ICAO regulations, robust distribution network across North America and Europe, and a long-standing reputation for reliability in critical aviation and infrastructure applications.

Dialight leverages its expertise in industrial LED lighting to offer highly durable and energy-efficient obstruction lighting solutions, particularly for the telecommunications and renewable energy sectors. Their growth is further propelled by strategic investments in smart lighting technologies and wireless monitoring systems. Similarly, Orga Aviation strengthens its market foothold through continuous product innovation and a strong focus on the European and Middle Eastern markets, where increasing air traffic and infrastructure development drive demand.

Beyond the top three, companies like Carmanah Technologies and Avlite Systems are aggressively expanding their market presence. These players compete effectively by specializing in solar-powered LED obstruction lights, catering to the growing demand for sustainable and off-grid solutions, especially in remote or environmentally sensitive locations. Their growth strategies often involve securing contracts for large-scale wind farm projects and telecommunications tower deployments.

Meanwhile, several Chinese manufacturers, including Shanghai Nanhua and Shenzhen Ruibu, are becoming increasingly influential, particularly within the Asia-Pacific region which accounts for nearly 29% of global consumption. These companies compete primarily on cost-efficiency and by catering to specific local regulatory standards, making them formidable players in price-sensitive segments. Their expansion is supported by the vast domestic infrastructure development and growing renewable energy installations in China and neighboring countries.

The competitive dynamics are further shaped by ongoing research and development initiatives aimed at enhancing product features such as predictive maintenance, improved photometrics, and integration with Air Navigation Service Provider (ANSP) systems. Strategic mergers, acquisitions, and partnerships for technology sharing and market access are also common tactics employed by key players to consolidate their positions and explore new application areas in the industrial and smart city sectors.

List of Key LED Obstruct Lighting Companies Profiled

- Hughey & Phillips (U.S.)

- Dialight (U.K.)

- Orga Aviation (Netherlands)

- Carmanah Technologies (Canada)

- Avlite Systems (Australia)

- Flash Technology (SPX) (U.S.)

- Obelux (Finland)

- TWR Lighting (U.S.)

- International Tower Lighting (U.S.)

- Hubbell Incorporated (U.S.)

- ADB Airfield Solutions (Belgium)

- OBSTA (Germany)

- TRANBERG (Denmark)

- Shanghai Nanhua (China)

- Shenzhen Ruibu (China)

Segment Analysis:

By Type

Medium Intensity LED Obstruct Light Segment Leads Due to Regulatory Compliance and Versatile Application Across Structures

The market is segmented based on type into:

- Low Intensity LED Obstruct Light

- Medium Intensity LED Obstruct Light

- High Intensity LED Obstruct Light

By Application

Bridges and Buildings Segment Dominates Owing to Extensive Urban Infrastructure Development and Aviation Safety Mandates

The market is segmented based on application into:

- Bridges and Buildings

- Renewable Energy

- Telecommunications

- Industrial

- Others

By End User

Aviation and Aerospace Sector is the Primary End User Driven by Stringent International Civil Aviation Organization (ICAO) Regulations

The market is segmented based on end user into:

- Aviation and Aerospace

- Construction and Infrastructure

- Energy and Utilities

- Government and Defense

- Others

By Mounting Type

Top-Mounted Lights Hold Significant Share Due to Their Critical Role in Marking the Highest Points of Obstructions

The market is segmented based on mounting type into:

- Top-Mounted Lights

- Side-Mounted Lights

- In-Pavement Lights

Regional Analysis: LED Obstruct Lighting Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global LED obstruct lighting market, accounting for approximately 29% of total global consumption, with China being the single largest national market. This dominance is fueled by an unprecedented scale of infrastructure development. China’s Belt and Road Initiative (BRI) and its extensive domestic urbanization projects require the marking of countless new high-rise buildings, communication towers, and wind farms. Similarly, India’s ambitious targets for renewable energy, aiming for 500 GW of capacity by 2030, are driving the installation of new wind turbines that require compliant obstruction lighting. While the market is volume-driven and historically cost-sensitive, leading to strong competition from local manufacturers like Shanghai Nanhua and Shenzhen Ruibu, there is a noticeable and growing shift toward higher-quality, more reliable systems. This is propelled by increasing regulatory scrutiny, the need for lower long-term maintenance costs, and heightened aviation safety awareness. The region is not just a consumption hub but also a major manufacturing center, supplying products globally.

North America

North America represents a highly mature and technologically advanced market, holding an estimated 25% share of global consumption. The market is characterized by stringent regulatory enforcement by the Federal Aviation Administration (FAA) in the U.S. and Transport Canada, which mandates strict compliance with technical standards for obstruction lighting on structures exceeding certain heights. This regulatory environment creates a consistent demand for high-performance, FAA-certified products from established players like Hughey & Phillips and Dialight. Market growth is further supported by the modernization and expansion of critical infrastructure, including the build-out of 5G telecommunications networks requiring new tower arrays, the ongoing development of wind energy projects, and the revitalization of aging bridges and buildings. A key trend is the rapid adoption of smart lighting systems that feature remote monitoring, diagnostics, and control, enhancing operational efficiency and safety while reducing the need for physical inspections.

Europe

Europe is a significant and stable market, comprising about 17% of the global total. The region’s growth is underpinned by a dual focus: the rigorous upgrade of aging infrastructure and the strong push toward sustainability and energy efficiency. European Aviation Safety Agency (EASA) regulations ensure high standards for aviation safety, driving demand for reliable LED systems. A major market driver is the continent’s commitment to renewable energy, particularly offshore wind farms in the North Sea, which represent massive projects requiring robust and durable obstruction lighting solutions capable of withstanding harsh marine environments. Furthermore, the European Union’s energy efficiency directives encourage the replacement of older, power-intensive incandescent lighting with modern LED systems across buildings and industrial structures. This replacement cycle, coupled with new construction adhering to strict environmental and safety codes, ensures steady demand. Innovation in low-power consumption and long-life products is a key competitive differentiator here.

South America

The South American market for LED obstruction lighting is in a developing phase, presenting a landscape of significant potential tempered by economic challenges. Countries like Brazil and Argentina are undertaking infrastructure projects, including urban high-rises and renewable energy installations, which generate demand for these safety systems. However, the market’s growth is often constrained by economic volatility, which can delay large-scale projects and limit capital expenditure. Furthermore, while aviation safety regulations exist, their enforcement can be inconsistent across the region, sometimes hindering the widespread adoption of the latest certified technologies. Price sensitivity remains a considerable factor, often favoring more cost-competitive solutions. Nevertheless, as economies stabilize and urban development continues, the long-term outlook for the market is positive, with growth expected to gradually accelerate.

Middle East & Africa

The Middle East and Africa region is an emerging market with distinct growth patterns. In the Middle East, particularly in Gulf Cooperation Council (GCC) nations like the UAE and Saudi Arabia, ambitious urban development projects, such as smart cities and mega-tall structures, are creating strong demand for high-quality LED obstruction lighting. These projects often specify advanced, technologically sophisticated systems. Conversely, in many parts of Africa, market development is more nascent and uneven. Growth is primarily driven by investments in telecommunications infrastructure and renewable energy, but it can be hampered by funding limitations and less developed regulatory frameworks for aviation safety. Despite these hurdles, the overall long-term potential is substantial, as ongoing urbanization and economic diversification across the region will necessitate increased investment in infrastructure and its associated safety markings.

Report Scope

This market research report provides a comprehensive analysis of the global and regional LED Obstruct Lighting markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Obstruct Lighting Market?

-> The global LED obstruct lighting market was valued at USD 265 million in 2024 and is projected to reach USD 388 million by 2032.

Which key companies operate in Global LED Obstruct Lighting Market?

-> Key players include Hughey & Phillips, Dialight, Orga Aviation, Carmanah Technologies, and Avlite, among others.

What are the key growth drivers?

-> Key growth drivers include increasing aviation safety regulations, growing renewable energy infrastructure, and urbanization driving tall construction projects.

Which region dominates the market?

-> China is the largest consumption market with 29% global share, while North America follows with 25% market share.

What are the emerging trends?

-> Emerging trends include solar-powered LED systems, smart lighting with remote monitoring, and integration with IoT for predictive maintenance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...