MARKET INSIGHTS

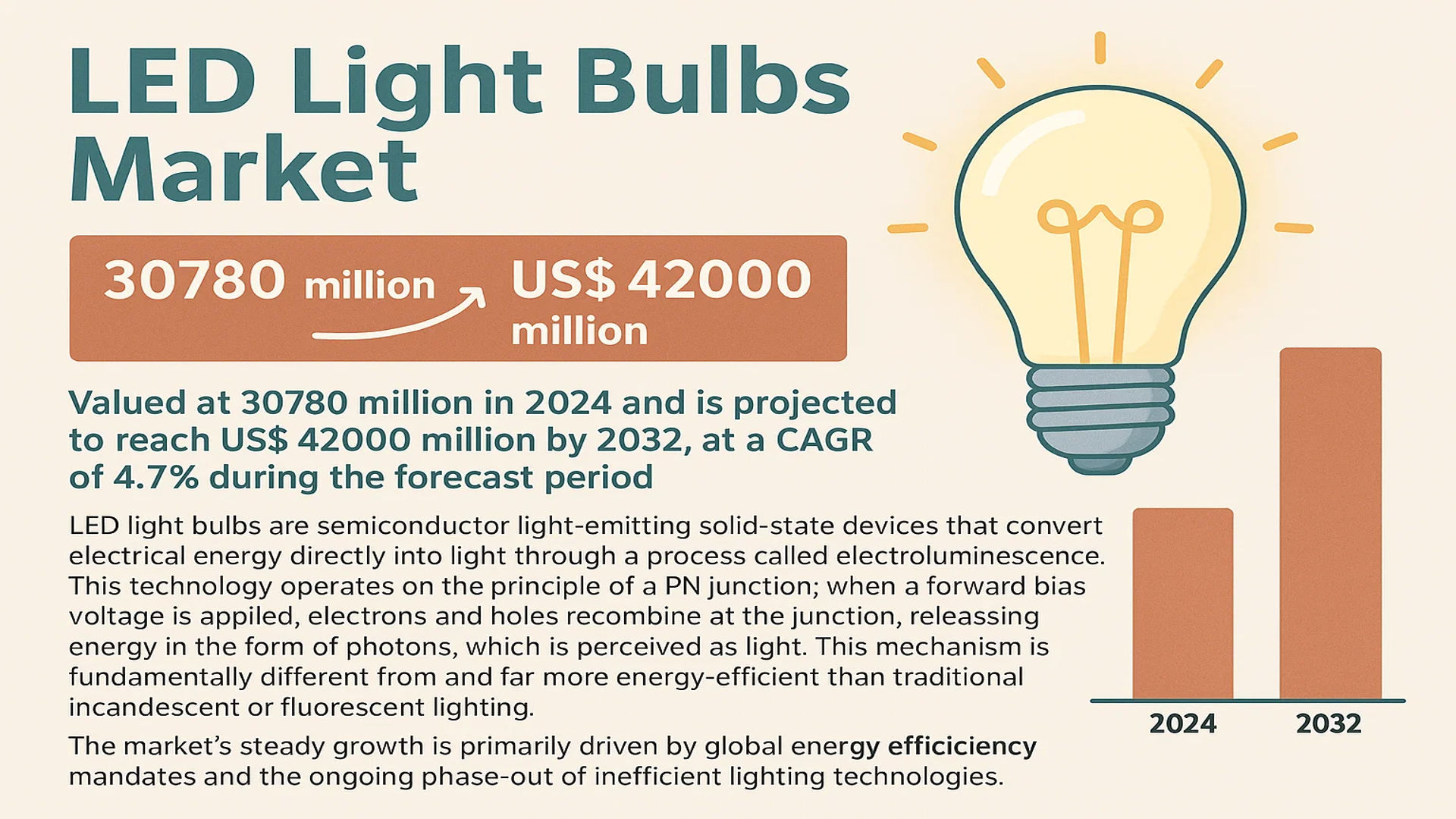

The global LED Light Bulbs Market was valued at 30780 million in 2024 and is projected to reach US$ 42000 million by 2032, at a CAGR of 4.7% during the forecast period.

LED light bulbs are semiconductor light-emitting solid-state devices that convert electrical energy directly into light through a process called electroluminescence. This technology operates on the principle of a PN junction; when a forward bias voltage is applied, electrons and holes recombine at the junction, releasing energy in the form of photons, which is perceived as light. This mechanism is fundamentally different from and far more energy-efficient than traditional incandescent or fluorescent lighting.

The market’s steady growth is primarily driven by global energy efficiency mandates and the ongoing phase-out of inefficient lighting technologies. Furthermore, declining average selling prices and continuous improvements in luminous efficacy, color rendering index (CRI), and smart connectivity features are accelerating adoption. The Asia Pacific region dominates the market, holding a 48% revenue share in 2024, largely due to massive manufacturing hubs in China and supportive government policies. Key players such as Philips (Signify), MLS, and Savant Systems Inc. (including GE Lighting) lead the market with extensive product portfolios and significant investments in smart lighting and human-centric lighting solutions.

MARKET DYNAMICS

MARKET DRIVERS

Global Energy Efficiency Mandates Accelerating LED Adoption

Governments worldwide are implementing stringent energy efficiency regulations to reduce carbon emissions and combat climate change, which serves as a primary catalyst for LED light bulb market expansion. Over 40 countries have now phased out or restricted the sale of inefficient incandescent and halogen bulbs, creating a regulatory environment that favors LED technology. The European Union’s Ecodesign Directive and the United States’ Energy Independence and Security Act have been particularly influential in driving market transformation. These policies mandate minimum efficiency standards that traditional lighting technologies cannot meet, effectively forcing consumers and businesses toward LED alternatives. The global push toward net-zero emissions targets by 2050 has further intensified these efforts, with many nations implementing additional incentives such as rebate programs and tax credits for energy-efficient lighting upgrades.

Rapid Declines in LED Pricing Driving Mass Market Adoption

The manufacturing cost of LED bulbs has decreased dramatically over the past decade, making them increasingly accessible to consumers across all economic segments. While an LED bulb cost approximately 40 dollars in 2010, today’s prices have fallen to just 2-5 dollars for equivalent products, representing a price reduction of over 90%. This dramatic cost reduction stems from improvements in manufacturing processes, economies of scale, and technological advancements in LED chip production. The development of more efficient manufacturing techniques for LED components, particularly in Asia where approximately 80% of global production occurs, has been instrumental in driving down costs. This price compression has effectively eliminated the primary barrier to adoption, transforming LED lighting from a premium product into a mainstream commodity available across all retail channels.

Growing Smart City Infrastructure Investments Boosting Commercial Demand

Urbanization trends and smart city initiatives worldwide are driving significant demand for LED lighting in municipal and commercial applications. Cities are increasingly adopting LED technology for street lighting, public buildings, and infrastructure projects due to its superior energy efficiency, longer lifespan, and compatibility with smart control systems. The global smart city market is projected to exceed 2.5 trillion dollars by 2025, with intelligent lighting representing a substantial component of this investment. LED systems enable cities to implement adaptive lighting that adjusts based on traffic patterns, weather conditions, and time of day, delivering additional energy savings of 20-30% beyond basic LED conversion. This technological capability, combined with the potential for integration with broader smart city networks for data collection and monitoring, makes LED lighting an essential infrastructure component for modern urban development.

MARKET RESTRAINTS

Market Saturation in Developed Regions Limiting Growth Potential

The LED light bulb market in developed economies is approaching saturation, creating significant headwinds for future growth. In regions such as North America and Europe, household penetration rates have exceeded 70%, leaving limited room for expansion in the residential replacement market. This high penetration rate means that most future sales will come from replacement purchases rather than new adopters, fundamentally changing the market dynamics and growth trajectory. The exceptional longevity of LED products, with lifespans ranging from 15,000 to 50,000 hours, further exacerbates this challenge by extending replacement cycles significantly beyond those of traditional lighting technologies. This market maturation is particularly evident in countries that implemented early transition programs, where the initial wave of replacements has largely been completed, leaving manufacturers to compete primarily for market share rather than market expansion.

Intense Price Competition Squeezing Manufacturer Margins

The LED lighting industry faces severe margin pressure due to commoditization and intense competition, particularly from manufacturers in Asia. With hundreds of companies producing similar products, differentiation has become increasingly difficult, leading to price wars that erode profitability across the sector. The average selling price for LED bulbs has declined by approximately 15-20% annually over the past five years, while material and labor costs have remained relatively stable or increased. This pricing environment makes it challenging for manufacturers to maintain research and development investments necessary for innovation, potentially slowing the pace of technological advancement. The situation is particularly acute for smaller manufacturers who lack the economies of scale enjoyed by market leaders, forcing consolidation within the industry as smaller players struggle to remain competitive.

Complex Global Supply Chain Vulnerabilities Impacting Production

The LED lighting industry’s reliance on complex global supply chains creates significant operational challenges and vulnerabilities. Most manufacturers depend on components sourced from multiple countries, particularly semiconductors from Taiwan and South Korea, phosphors from Japan, and various materials from China. This geographic dispersion makes the industry susceptible to disruptions from trade tensions, logistical challenges, and regional instability. The recent global semiconductor shortage demonstrated how vulnerable the industry is to supply chain disruptions, with lead times for certain components extending from weeks to months. These challenges are compounded by fluctuating raw material prices and transportation costs, which create additional uncertainty in production planning and cost management. Manufacturers must maintain higher inventory levels to buffer against these uncertainties, increasing working capital requirements and reducing operational efficiency.

MARKET CHALLENGES

Technical Standardization Issues Creating Consumer Confusion

The lack of universal technical standards across the LED lighting industry creates significant challenges for both consumers and manufacturers. Unlike traditional incandescent bulbs that had relatively straightforward specifications, LED products vary widely in terms of color temperature, color rendering index, dimming compatibility, and connectivity protocols. This variability leads to consumer confusion and dissatisfaction when products don’t perform as expected or aren’t compatible with existing infrastructure. The problem is particularly acute with smart LED products, where multiple wireless protocols including Zigbee, Z-Wave, Bluetooth, and Wi-Fi create interoperability challenges. Industry efforts to establish common standards have progressed slowly, with different regions and major manufacturers often promoting proprietary solutions that fragment the market. This lack of standardization increases product development costs, complicates inventory management, and creates barriers to widespread smart lighting adoption.

Other Challenges

Environmental Concerns Regarding Electronic Waste

The rapid adoption of LED lighting creates emerging environmental challenges related to electronic waste management. While LED bulbs are more energy-efficient than traditional lighting, they contain electronic components and materials that require proper disposal and recycling. The relatively short product life compared to manufacturer claims in some cases, particularly with cheaper products, exacerbates this issue by increasing replacement frequency. Many regions lack adequate recycling infrastructure for LED products, leading to improper disposal that can release heavy metals and other contaminants into the environment. These environmental considerations are becoming increasingly important to regulators and consumers, potentially leading to additional compliance requirements and costs for manufacturers.

Consumer Perception and Education Gaps

Despite significant market penetration, many consumers still maintain misconceptions about LED technology that hinder broader adoption. Common concerns include perceived poor light quality, higher upfront costs despite long-term savings, and uncertainty about product claims. Educational gaps are particularly pronounced in emerging markets and among older demographic segments where resistance to new technology remains stronger. Manufacturers face the ongoing challenge of communicating the benefits and proper usage of LED lighting while overcoming negative perceptions from early-generation products that suffered from quality issues. This educational burden increases marketing costs and extends the adoption cycle, particularly in price-sensitive market segments.

MARKET OPPORTUNITIES

Emerging Markets Present Substantial Untapped Potential

Developing economies represent the most significant growth opportunity for the LED lighting industry, with current penetration rates substantially below those in developed markets. In many Asian, African, and Latin American countries, LED adoption remains below 30% of households, creating a substantial addressable market for future expansion. Rapid urbanization, growing middle-class populations, and increasing electrification rates in these regions are driving demand for modern lighting solutions. Government initiatives in many emerging markets are also promoting LED adoption through energy efficiency programs and subsidies, particularly as these nations seek to reduce energy imports and improve electrical grid stability. The combination of economic development, infrastructure investment, and policy support creates a favorable environment for market expansion that could drive growth for the next decade.

Integration with IoT and Smart Building Systems Creating New Value Propositions

The convergence of LED lighting with Internet of Things technology and smart building systems is creating innovative applications that extend far beyond basic illumination. Modern LED systems can incorporate sensors, connectivity, and data analytics capabilities that transform lighting infrastructure into intelligent networks capable of monitoring occupancy, tracking assets, collecting environmental data, and enhancing security. This technological evolution enables lighting to become a platform for building automation and smart city applications, creating additional revenue streams beyond the sale of light bulbs. The integration of Li-Fi technology, which uses light waves for data transmission, represents another emerging opportunity that could fundamentally expand the functionality of lighting systems. These advanced applications command premium pricing and create opportunities for differentiation in an otherwise commoditized market.

Human-Centric Lighting Driving Premium Market Segment Growth

Growing awareness of the biological effects of light on human health and productivity is creating new market opportunities for advanced LED solutions. Human-centric lighting systems that adjust color temperature and intensity throughout the day to align with natural circadian rhythms are gaining traction in healthcare, education, and corporate environments. Research demonstrating the positive impact of tunable lighting on patient outcomes, student performance, and workplace productivity is driving investment in these specialized systems. This segment commands significantly higher prices than standard LED products, with premium solutions often costing 3-5 times more than basic alternatives. The emphasis on health and wellness in building design, particularly in post-pandemic environments, is accelerating adoption of these advanced lighting solutions and creating a high-value market segment less susceptible to price competition.

LED LIGHT BULBS MARKET TRENDS

Smart Connectivity and IoT Integration to Emerge as a Dominant Trend

The integration of smart technology and Internet of Things (IoT) capabilities is fundamentally reshaping the LED light bulbs market, moving beyond simple illumination to become a core component of connected home and building automation systems. This evolution is driven by consumer demand for energy management, convenience, and personalized lighting experiences. Smart LED bulbs, which can be controlled via smartphones, voice assistants, or automated schedules, now represent one of the fastest-growing segments, with adoption rates increasing by over 20% annually in key markets. This trend is further accelerated by the rollout of 5G networks and improved wireless protocols like Matter, which enhance device interoperability and reliability. Manufacturers are responding by embedding advanced sensors for occupancy detection, ambient light monitoring, and even health metrics, transforming light fixtures into data collection points that contribute to overall energy efficiency and user well-being.

Other Trends

Sustainability and Regulatory Drivers

Global sustainability initiatives and stringent government regulations continue to be powerful drivers for LED adoption, as nations aim to reduce carbon footprints and achieve energy independence. The ongoing global phase-out of inefficient incandescent and halogen bulbs has created a massive replacement market, with LEDs now accounting for over 60% of the global general illumination market. Energy efficiency standards, such as the U.S. Department of Energy’s new rules that require bulbs to produce over 45 lumens per watt, effectively mandate the use of LED technology. Furthermore, corporate sustainability pledges and green building certifications like LEED and BREEAM are accelerating the retrofitting of commercial and industrial spaces with intelligent LED systems that can reduce lighting energy consumption by up to 80% compared to traditional solutions.

Human-Centric Lighting and Advanced Materials

Advancements in phosphor technology and chip design are enabling a new wave of human-centric lighting (HCL) solutions that dynamically adjust color temperature and intensity to align with natural circadian rhythms. This focus on health and wellness is particularly influential in the corporate, healthcare, and educational sectors, where studies have shown that tunable white LED lighting can improve productivity, patient recovery times, and student concentration. Concurrently, material science innovations are addressing key industry challenges. The development of more efficient heat sink materials and robust driver components is significantly extending product lifespans, with many premium bulbs now rated for over 50,000 hours of use. Research into organic LEDs (OLEDs) and micro-LEDs is also progressing, promising even greater efficiency, flexibility in design, and new form factors that could unlock novel applications in the future.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Leverage Innovation and Strategic Acquisitions to Maintain Dominance

The global LED light bulbs market exhibits a semi-consolidated structure, characterized by the presence of a few dominant multinational corporations alongside numerous regional and specialized manufacturers. Philips (Signify) stands as the unequivocal market leader, a position solidified by its extensive brand recognition, comprehensive product portfolio spanning residential, commercial, and industrial applications, and a deeply entrenched global distribution network. The company’s strategic pivot towards smart, connected lighting solutions and sustainability initiatives has been a primary driver of its sustained market share.

MLS Co., Ltd. (which includes the Ledvance brand, formerly part of OSRAM) and Savant Systems Inc. (now encompassing the iconic GE Lighting portfolio) also command significant portions of the global market. Their strength is largely derived from robust manufacturing capabilities, particularly in the Asia-Pacific region, and a strong foothold in the replacement bulb segment across North America and Europe. The integration of GE Lighting into Savant has created a powerful entity focused on the high-growth smart home and connected lighting space.

Furthermore, these established players are actively expanding their market influence through continuous research and development in areas like human-centric lighting (HCL), increased lumens-per-watt efficiency, and IoT integration. New product launches featuring enhanced connectivity protocols like Matter, along with geographical expansions into emerging economies in Asia and South America, are expected to be critical for future growth.

Meanwhile, other key competitors like Panasonic and Opple Lighting are strengthening their positions through aggressive pricing strategies, significant investments in automated manufacturing to reduce costs, and the development of innovative product lines tailored to specific regional preferences and regulatory standards. Companies such as NVC Lighting and Yankon Lighting compete effectively by dominating value-oriented market segments and leveraging their massive scale in production.

List of Key LED Light Bulb Companies Profiled

- Philips (Signify) (Netherlands)

- MLS Co., Ltd. (including Ledvance) (China)

- Savant Systems Inc. (including GE Lighting) (U.S.)

- Panasonic Corporation (Japan)

- Toshiba Corporation (Japan)

- FSL (Foshan Lighting) (China)

- Opple Lighting (China)

- Yankon Lighting (China)

- NVC Lighting (ETI) (China)

- Ideal Industries Inc. (including Cree Lighting) (U.S.)

- Technical Consumer Products, Inc. (U.S.)

- Shanghai Feilo Acoustics Co., Ltd. (China)

Segment Analysis:

By Type

A-Lamp Bulb Segment Dominates the Market Due to its Widespread Adoption in Residential Retrofit Applications

The market is segmented based on type into:

- A-Lamp Bulb

- Spot Light

- Street Light

- Tube Light

- Wall Washer Light

- Others

By Application

Residential Segment Leads Due to Global Energy Efficiency Initiatives and Consumer Shift Towards Sustainable Lighting

The market is segmented based on application into:

- Residential

- Office

- Shop

- Hospitality

- Others

By End User

Consumer Segment Leads the Market Owing to High Volume Demand for Household and Personal Use Lighting Solutions

The market is segmented based on end user into:

- Consumer

- Industrial

- Commercial

- Government & Municipalities

Regional Analysis: LED Light Bulbs Market

Asia-Pacific

As the dominant global market, Asia-Pacific holds approximately 48% of the worldwide LED light bulb market share, driven by massive manufacturing capabilities and widespread adoption. China is the undisputed leader in both production and consumption, supported by strong government initiatives promoting energy efficiency and a well-established electronics supply chain. India is experiencing explosive growth, fueled by ambitious smart city projects, rising disposable incomes, and large-scale rural electrification programs that prioritize LED technology for its energy savings. While cost-competitiveness remains a primary driver, there is a noticeable and accelerating shift towards smart, connected LED solutions and higher-quality products, particularly in urban centers across Japan, South Korea, and Southeast Asia.

Europe

Europe is a mature and highly regulated market, accounting for roughly 23% of global sales. The region’s growth is heavily influenced by stringent EU energy efficiency directives, such as the Ecodesign regulations, which have effectively phased out most incandescent and halogen lighting. Consumer demand is increasingly skewed towards smart home-integrated bulbs, human-centric lighting that supports well-being, and products with circular economy principles, including reparability and recyclability. Western European nations like Germany, France, and the U.K. lead in the adoption of advanced, connected lighting systems, while Eastern European markets are experiencing robust growth as they modernize their infrastructure.

North America

Accounting for an estimated 19% of the global market, North America is characterized by high consumer awareness and a strong preference for smart, connected lighting ecosystems that integrate with platforms like Amazon Alexa, Google Home, and Apple HomeKit. Energy Star certification and utility rebate programs significantly influence purchasing decisions, driving the replacement of older lighting technologies. The market is highly competitive, with major players continuously innovating in terms of connectivity, light quality, and design aesthetics. While the residential retrofit segment is substantial, there is also consistent demand from the commercial and industrial sectors seeking operational cost savings through energy efficiency.

South America

The South American market is in a growth phase, though it is challenged by economic volatility and fluctuating currency values, which can impact import costs and consumer spending power. Brazil and Argentina are the largest markets, with growth primarily driven by rising energy costs that make LED savings more attractive and gradual infrastructure modernization efforts. Government energy efficiency programs are emerging but are not yet as comprehensive or enforced as in other regions. The market currently favors more basic, cost-effective LED bulbs, with the adoption of smart and premium features limited to higher-income urban segments.

Middle East & Africa

This is an emerging region with significant long-term potential, largely driven by rapid urbanization, massive infrastructure development, and the pressing need for energy conservation, particularly in Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia. Large-scale government projects, smart city initiatives, and the construction of new commercial and hospitality spaces are key demand drivers. However, market development is uneven; while affluent Gulf states are adopting high-end and smart lighting solutions, price sensitivity remains a major factor in other parts of the region. The lack of strong, unified regulatory standards also slows the widespread transition to higher-quality LED products.

Report Scope

This market research report provides a comprehensive analysis of the global and regional LED Light Bulbs markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Light Bulbs Market?

-> LED Light Bulbs Market was valued at 30780 million in 2024 and is projected to reach US$ 42000 million by 2032, at a CAGR of 4.7% during the forecast period.

Which key companies operate in Global LED Light Bulbs Market?

-> Key players include Philips (Signify), MLS (including Ledvance), Savant Systems Inc. (including GE Lighting), Panasonic, Toshiba, FSL, Opple, Yankon Lighting, NVC (ETI), Ideal Industries Inc. (including Cree Lighting), Technical Consumer Products, Inc., and Shanghai Feilo Acoustics, among others.

What are the key growth drivers?

-> Key growth drivers include global energy efficiency regulations, declining LED prices, rising consumer awareness of energy savings, and government initiatives promoting sustainable lighting solutions.

Which region dominates the market?

-> Asia-Pacific is the largest market with approximately 48% market share, followed by Europe and North America with shares of about 23% and 19% respectively.

What are the emerging trends?

-> Emerging trends include smart connected lighting systems, human-centric lighting, increased adoption of Li-Fi technology, and development of organic LEDs (OLEDs).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...