MARKET INSIGHTS

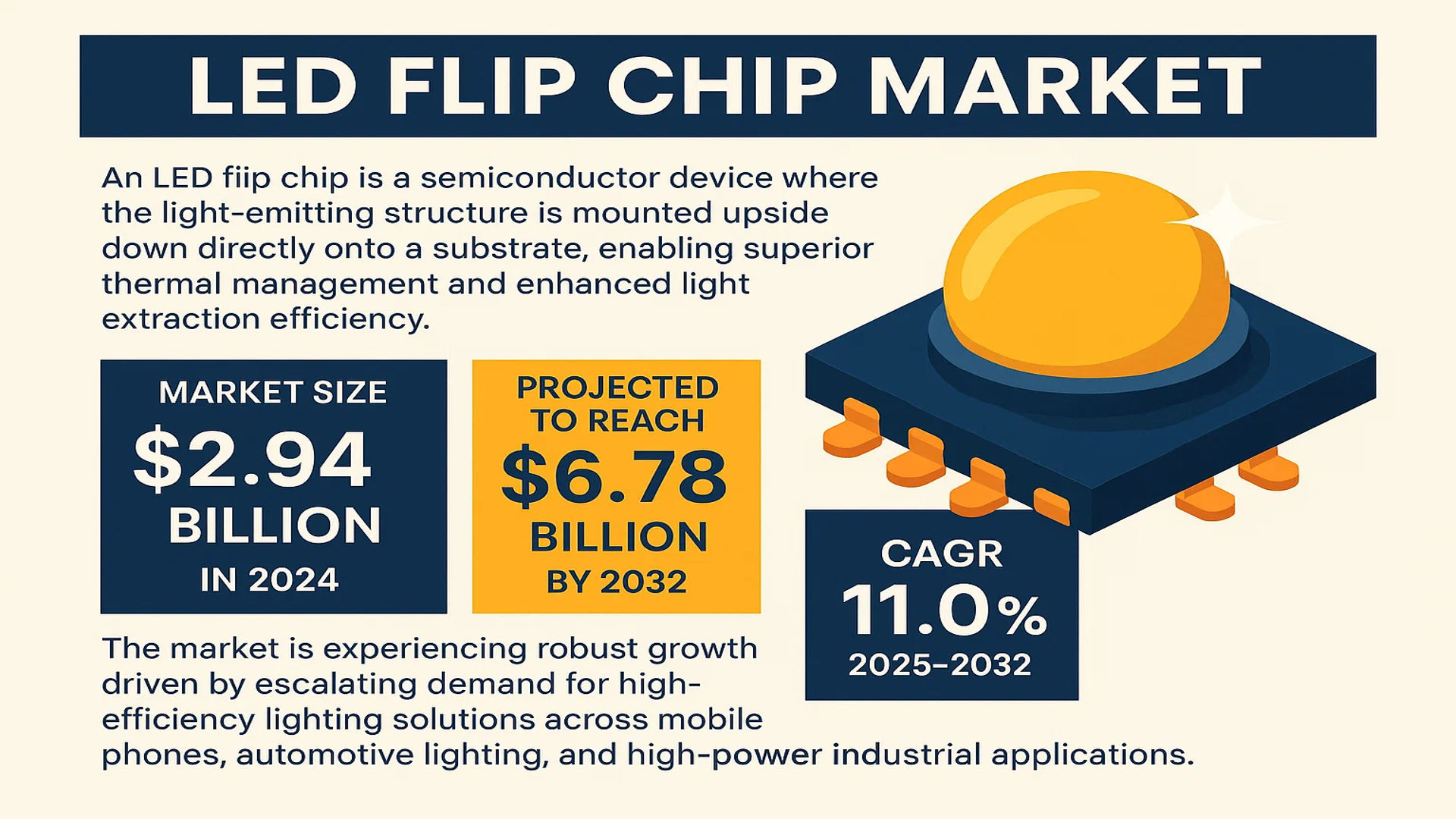

The global LED Flip Chip Market size was valued at US$ 2.94 billion in 2024 and is projected to reach US$ 6.78 billion by 2032, at a CAGR of 11.0% during the forecast period 2025-2032.

A Light Emitting Diode (LED) flip chip is a semiconductor device where the light-emitting structure is mounted upside down directly onto a substrate, enabling superior thermal management and enhanced light extraction efficiency. This advanced packaging technology is a core component of modern LED systems, leveraging the fundamental PN junction principle to convert electrical energy into light. Flip chip LEDs are categorized by structure alongside lateral and vertical chips, representing a significant evolution in solid-state lighting design.

The market is experiencing robust growth driven by escalating demand for high-efficiency lighting solutions across mobile phones, automotive lighting, and high-power industrial applications. Furthermore, the transition towards energy-efficient technologies and miniaturization of electronic components is accelerating adoption. Key industry players, including Lumileds, Nichia, and Epistar, are actively expanding their production capacities and investing in R&D to enhance product performance, thereby intensifying competition and fostering market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Efficiency Lighting Solutions to Propel Market Growth

The global LED flip chip market is experiencing robust growth driven by increasing demand for energy-efficient and high-performance lighting solutions across various sectors. LED flip chips offer superior thermal management, higher lumen output, and enhanced reliability compared to traditional lateral chips, making them ideal for applications requiring intense illumination and compact form factors. The transition towards smart cities and infrastructure modernization projects worldwide has accelerated the adoption of advanced lighting technologies. Governments and municipalities are implementing large-scale LED retrofitting programs to reduce energy consumption and carbon emissions. For instance, numerous urban development initiatives across Asia and Europe are mandating the use of high-efficiency LEDs for street lighting, public spaces, and commercial buildings, creating sustained demand for flip chip technology.

Expansion of Automotive Lighting Applications to Accelerate Adoption

Automotive lighting represents a significant growth avenue for LED flip chips, driven by the automotive industry’s shift towards advanced lighting systems and electric vehicles. Flip chip LEDs provide excellent thermal performance and design flexibility, enabling slimmer headlight designs and improved illumination patterns. The increasing consumer preference for premium lighting features, along with stringent safety regulations mandating brighter and more efficient automotive lighting, is pushing manufacturers to adopt flip chip technology. The electric vehicle revolution further amplifies this trend, as EVs require highly efficient lighting systems to optimize energy consumption and extend battery life. Major automotive manufacturers are integrating advanced LED lighting solutions across their vehicle portfolios, from economy models to luxury segments, ensuring sustained market expansion.

Technological Advancements in Miniaturization to Drive Market Penetration

Continuous innovation in semiconductor packaging and miniaturization technologies is creating new opportunities for LED flip chips across diverse applications. The development of smaller form factors, particularly 1.1mm chips, enables their integration into space-constrained devices such as mobile phones, wearables, and portable electronics. Flip chip technology’s ability to provide higher power density in smaller packages aligns perfectly with the electronics industry’s trend towards miniaturization and enhanced functionality. Recent manufacturing improvements have reduced production costs while maintaining high yield rates, making flip chip LEDs more accessible to mass-market applications. The proliferation of IoT devices and smart home systems further expands the addressable market, as these applications require reliable, efficient, and compact lighting solutions.

MARKET CHALLENGES

High Manufacturing Complexity and Costs to Constrain Market Expansion

The LED flip chip market faces significant challenges related to manufacturing complexity and associated costs. Flip chip production involves sophisticated processes including wafer-level processing, bumping, and precise placement techniques that require advanced equipment and specialized expertise. The capital investment for establishing flip chip manufacturing facilities is substantially higher than traditional LED production lines, creating barriers for smaller players and new entrants. Additionally, the yield rates for flip chip manufacturing, while improving, still present challenges compared to conventional LED chips. The need for stringent quality control and testing further adds to production costs, making flip chip LEDs more expensive than alternative technologies. These cost factors particularly impact price-sensitive markets and applications where budget constraints limit adoption.

Other Challenges

Thermal Management Issues

Despite advantages in thermal performance, flip chip LEDs still face challenges in heat dissipation at higher power densities. As applications demand brighter outputs and smaller form factors, managing heat generation becomes increasingly critical. Inadequate thermal management can lead to reduced lifespan, color shifting, and performance degradation, particularly in high-power lighting applications and automotive systems. Developing effective thermal interface materials and heat dissipation solutions remains an ongoing challenge for manufacturers.

Supply Chain Vulnerabilities

The global nature of semiconductor supply chains creates vulnerabilities for flip chip LED production. Dependencies on specific raw materials, specialized equipment, and geopolitical factors can disrupt manufacturing continuity. Recent global events have highlighted the fragility of semiconductor supply networks, affecting production timelines and cost structures. Ensuring stable material sourcing and manufacturing capacity while navigating trade regulations and geopolitical tensions presents ongoing operational challenges for market participants.

MARKET RESTRAINTS

Competition from Alternative Technologies to Limit Market Growth

While LED flip chips offer numerous advantages, they face strong competition from emerging lighting technologies and alternative LED configurations. Organic LEDs (OLEDs) and micro-LEDs are gaining traction in display and lighting applications, offering different performance characteristics that may better suit specific use cases. Additionally, improvements in traditional lateral LED technology continue to narrow the performance gap with flip chips, particularly in cost-sensitive applications. The development of hybrid approaches and intermediate technologies provides customers with multiple options, potentially fragmenting the market and limiting flip chip adoption. In price-sensitive segments such as general lighting and consumer electronics, the cost-performance trade-off often favors alternative solutions, restraining flip chip market penetration in these segments.

Technical Standardization Issues to Hinder Market Development

The lack of universal technical standards and interoperability specifications presents significant restraints for the LED flip chip market. Different manufacturers employ varying packaging approaches, materials, and interface technologies, creating compatibility issues for downstream integrators. This fragmentation increases development costs for lighting system manufacturers who must design specific solutions for different flip chip variants. The absence of standardized testing methodologies and performance metrics also makes comparative evaluation challenging for customers, potentially slowing adoption decisions. Furthermore, the rapid pace of technological innovation means that standards struggle to keep up with new developments, creating uncertainty and risk for both manufacturers and customers investing in flip chip technology.

Economic Uncertainty and Budget Constraints to Impact Market Momentum

Global economic fluctuations and budget constraints across key end-user industries pose significant restraints for LED flip chip market growth. The capital-intensive nature of lighting upgrades and infrastructure projects means that economic downturns can delay or cancel planned investments. Commercial and industrial customers often prioritize cost reduction over technology upgrades during challenging economic conditions, opting for conventional lighting solutions rather than premium flip chip-based systems. Public sector spending on smart city initiatives and infrastructure modernization, while growing, remains subject to budgetary pressures and changing political priorities. These economic factors create uncertainty in demand patterns and can temporarily slow market expansion during periods of economic volatility.

MARKET OPPORTUNITIES

Emerging Applications in Horticulture Lighting to Create New Growth Avenues

The rapidly expanding controlled environment agriculture sector presents substantial opportunities for LED flip chip technology. Horticulture lighting requires specific spectral outputs, high efficiency, and reliable performance under continuous operation conditions—characteristics where flip chip LEDs excel. The global shift towards sustainable food production and urban farming is driving investment in advanced horticulture lighting systems. Flip chip technology’s ability to provide precise spectral control and high photon efficacy makes it ideal for plant growth applications. The market for horticulture lighting is experiencing double-digit growth as vertical farming and greenhouse operations expand worldwide, creating sustained demand for advanced LED solutions.

Integration with Smart Lighting Systems to Unlock New Potential

The convergence of IoT technology with lighting systems creates significant opportunities for LED flip chip adoption in smart lighting applications. Flip chips’ compact size and excellent thermal characteristics enable the integration of sensors, controllers, and communication modules directly into lighting fixtures. The growing smart city infrastructure and building automation markets require intelligent lighting solutions that can adapt to environmental conditions and user preferences. Flip chip technology provides the foundation for these advanced systems, offering the reliability and performance needed for always-connected applications. The proliferation of 5G networks and edge computing further enhances the potential for smart lighting systems, creating new revenue streams and application possibilities for flip chip technology.

Advancements in Display Technologies to Drive Future Expansion

The display industry’s ongoing transition towards mini-LED and micro-LED technologies represents a substantial opportunity for LED flip chip manufacturers. These advanced display technologies require extremely small, high-performance LEDs with excellent thermal management and reliability—characteristics inherent to flip chip design. The consumer electronics market’s demand for brighter, more efficient, and higher-resolution displays is driving investment in next-generation display technologies. Flip chip LEDs are particularly suited for backlighting applications in premium televisions, monitors, and automotive displays where uniform illumination and high contrast ratios are critical. The display segment’s continuous innovation cycle and premium pricing structure provide favorable conditions for flip chip technology adoption and market growth.

LED FLIP CHIP MARKET TRENDS

Advancements in Miniaturization and High-Power Applications Drive Market Growth

The global LED Flip Chip market is experiencing robust growth, primarily fueled by the relentless drive towards miniaturization and enhanced performance in electronic devices. Unlike traditional lateral chips, flip-chip technology involves inverting the semiconductor die and connecting it directly to the substrate via solder bumps, which significantly improves thermal management and allows for a higher power density in a smaller footprint. This structural advantage is critical for applications demanding high luminosity and reliability, such as automotive headlights and high-power lighting devices, a segment projected to hold a substantial market share. The superior thermal dissipation capability of flip chips, which can be up to 30% more efficient than wire-bonded alternatives, directly translates to longer lifespans and higher lumen output, making them the preferred choice for next-generation lighting solutions. This trend is further amplified by the proliferation of ultra-high-definition displays in consumer electronics, where the compact size and superior performance of flip chips are indispensable.

Other Trends

Automotive Lighting Revolution

The automotive industry’s rapid transition towards advanced lighting systems is a paramount trend shaping the LED Flip Chip market. The adoption of Adaptive Driving Beams (ADB), matrix LED headlights, and interior ambient lighting in modern vehicles is creating immense demand for reliable, high-performance chips. Flip chips are uniquely suited for these applications because of their ability to handle high current densities and their exceptional resistance to thermal stress, a common challenge in automotive environments. Furthermore, the global push for vehicle electrification and autonomous driving features, which rely heavily on sophisticated sensor and lighting systems, is providing a sustained tailwind for market expansion. The automotive segment is anticipated to be one of the fastest-growing application areas, with its demand intricately linked to annual vehicle production volumes, which are steadily recovering and innovating post-global supply chain disruptions.

Geographic Shift and Supply Chain Consolidation in Asia-Pacific

The Asia-Pacific region continues to dominate the global LED Flip Chip market, accounting for over 70% of both production and consumption. This hegemony is underpinned by a powerful combination of factors: a concentrated presence of major manufacturers like Epistar, San’an Opto, and HC SemiTek; a vast electronics manufacturing ecosystem; and strong governmental support for semiconductor industries in countries like China and Taiwan. However, the market dynamic is not static. There is a noticeable trend towards supply chain consolidation and technological upgrading within the region. Leading players are aggressively investing in Metal Organic Chemical Vapor Deposition (MOCVD) reactor capacity and advanced packaging techniques to improve yields and reduce production costs. This internal competition is driving rapid innovation and efficiency gains, ensuring the region’s continued leadership. Meanwhile, geopolitical factors and a global emphasis on supply chain resilience are prompting some diversification of manufacturing bases, though Asia-Pacific’s entrenched advantages ensure its central role for the foreseeable future.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansions Drive Market Leadership

The global LED flip chip market exhibits a semi-consolidated competitive structure, characterized by a dynamic mix of established multinational corporations and agile regional specialists. This landscape is intensely competitive, with players vying for market share through technological superiority, manufacturing scale, and strategic partnerships. The market’s projected growth to US$ 6.78 billion by 2032 from a 2024 valuation of US$ 2.94 billion acts as a primary catalyst for these competitive strategies, driving significant investment in research and development.

Lumileds holds a commanding position as a market leader, a status reinforced by its extensive intellectual property portfolio and global manufacturing footprint. The company’s focus on high-performance flip chips for automotive lighting and premium general illumination applications has secured its dominance. Similarly, Epistar Corporation and San’an Opto are pivotal forces, particularly within the Asia-Pacific region. Their growth is largely fueled by massive production capacities and deep integration into the consumer electronics supply chain, serving major smartphone and television manufacturers. These companies benefit from economies of scale, allowing them to compete aggressively on both performance and price.

Furthermore, these leading entities are actively pursuing growth through geographical expansion and continuous product launches. For instance, companies are establishing new fabrication plants and forming joint ventures to tap into emerging markets and secure a stable supply of raw materials. New product developments are increasingly focused on enhancing luminous efficacy and thermal management, which are critical for next-generation applications like micro-LED displays and ultra-high-brightness automotive headlights.

Meanwhile, other significant players such as Genesis Photonics and Lextar (AU Optronics) are strengthening their market presence by carving out specialized niches. Genesis Photonics, for example, has made notable strides in flip chips designed for horticultural lighting and UV curing applications. They are achieving this through dedicated R&D investments and strategic partnerships with lighting module manufacturers, ensuring their technology is optimized for specific end-use requirements. This trend towards specialization and collaboration is expected to further intensify the competition and drive innovation across the entire market.

List of Key LED Flip Chip Companies Profiled

- Lumileds Holding B.V. (Netherlands)

- Epistar Corporation (Taiwan)

- San’an Optoelectronics Co., Ltd. (China)

- Nichia Corporation (Japan)

- Lextar Electronics Corporation (AU Optronics) (Taiwan)

- Genesis Photonics Inc. (Taiwan)

- HC SemiTek Corporation (China)

- Lattice Power Corporation (China)

- ETI Solid State Lighting Inc. (Taiwan)

Segment Analysis:

By Type

1.1mm Segment Leads the Market Due to Superior Thermal Management and Miniaturization Advantages

The market is segmented based on type into:

- 1.4mm

- 1.1mm

By Application

Automobiles Segment Dominates Owing to Surging Adoption in Advanced Automotive Lighting Systems

The market is segmented based on application into:

- Mobile Phones

- Automobiles

- Daylight Lamps

- High Power Lighting Devices

- Others

By End-User Industry

Consumer Electronics Holds Largest Share Driven by Demand for Energy-Efficient Display Solutions

The market is segmented based on end-user industry into:

- Consumer Electronics

- Automotive

- General Lighting

- Others

Regional Analysis: LED Flip Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global LED Flip Chip market, accounting for over 60% of the total market share in 2024. This leadership is driven by the massive manufacturing ecosystems in China, Taiwan, and South Korea, which serve as the global hub for semiconductor and LED production. China, in particular, is the epicenter, with companies like San’an Opto and HC SemiTek leading production volumes. The region benefits from strong government support for the semiconductor industry, extensive R&D investments, and a robust supply chain that reduces costs. High demand from the consumer electronics sector, especially for mobile phones and automotive lighting, further fuels growth. However, intense competition and price sensitivity remain significant challenges for manufacturers operating in this region.

North America

North America is a significant market characterized by high-value, innovation-driven demand. The region, particularly the United States, is home to key players like Lumileds, which focus on advanced applications such as high-power lighting devices for automotive and specialized industrial uses. Strict energy efficiency regulations, such as those from the U.S. Department of Energy, and a strong emphasis on R&D foster the adoption of high-performance flip chips. The market is further supported by investments in smart infrastructure and the automotive industry’s shift toward energy-efficient lighting solutions. While manufacturing volume is lower compared to Asia-Pacific, the focus on quality and technological advancement ensures strong revenue generation.

Europe

Europe’s market is shaped by stringent environmental and energy efficiency regulations, such as the EU’s Ecodesign Directive, which promotes the use of advanced LED technologies. The automotive sector is a major driver, with leading manufacturers incorporating flip chip LEDs for enhanced reliability and performance in vehicle lighting. Countries like Germany and France are at the forefront, supported by a strong industrial base and emphasis on sustainability. While the region has limited local manufacturing capacity compared to Asia, it relies on imports and partnerships with global suppliers. Innovation in applications such as horticultural lighting and professional daylight lamps also contributes to steady market growth.

South America

The South American market for LED flip chips is emerging but faces challenges due to economic volatility and limited local manufacturing infrastructure. Brazil and Argentina are the primary markets, driven by gradual urbanization and increasing adoption of energy-efficient lighting solutions. Demand is largely met through imports, as there are few regional manufacturers. The automotive sector shows potential for growth, but high costs and economic instability slow down the adoption of advanced flip chip technology. Nonetheless, government initiatives promoting energy efficiency and urban development projects offer long-term opportunities for market expansion.

Middle East & Africa

This region represents a nascent market with growing potential, particularly in countries like the UAE, Saudi Arabia, and Israel, where urbanization and infrastructure development are priorities. The demand for LED flip chips is primarily driven by high-power lighting devices used in commercial and municipal projects. However, the market is constrained by limited local production, reliance on imports, and a focus on cost-effective solutions rather than advanced technologies. While the adoption rate is slower compared to other regions, increasing investments in smart city projects and energy-efficient infrastructure are expected to drive gradual growth in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the global LED Flip Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Flip Chip Market?

-> LED Flip Chip Market size was valued at US$ 2.94 billion in 2024 and is projected to reach US$ 6.78 billion by 2032, at a CAGR of 11.0% during the forecast period 2025-2032.

Which key companies operate in Global LED Flip Chip Market?

-> Key players include Lumileds, NiChia, Lextar (AU Optronics), Genesis Photonics, Epistar, San’an Opto, ETI, Lattice Power, and HC SemiTek, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for energy-efficient lighting, adoption in automotive lighting systems, and growth in consumer electronics.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 65% of global revenue in 2024, driven by strong manufacturing presence in China and Taiwan.

What are the emerging trends?

-> Emerging trends include miniaturization of chips, development of micro-LED technology, and integration with IoT-enabled smart lighting systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...