Leapfrog filter topology for anti-alias filtering in SAR ADCs Market Insights

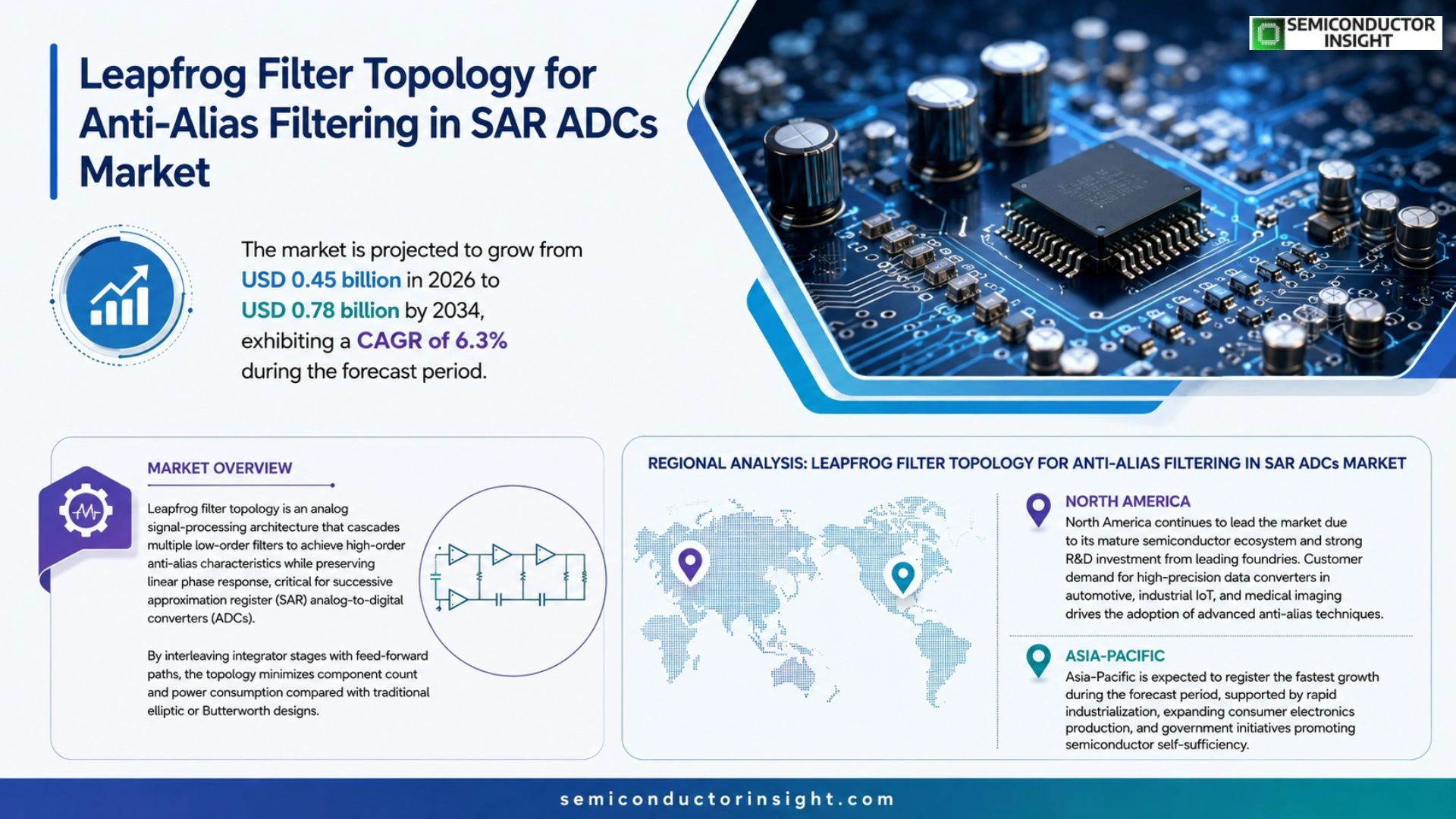

Leapfrog filter topology for anti-alias filtering in SAR ADCs market size is projected to grow from USD 0.45 billion in 2025 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Leapfrog filter topology is an analog signal‑processing architecture that cascades multiple low‑order filters to achieve high‑order anti‑alias characteristics while preserving linear phase response,critical for successive approximation register (SAR) analog‑to‑digital converters (ADCs). By interleaving integrator stages with feed‑forward paths, the topology minimizes component count and power consumption compared with traditional elliptic or Butterworth designs.

The market is experiencing rapid growth because system‑level designers demand higher resolution at lower power budgets, especially in IoT sensor nodes and automotive radar front‑ends.

Furthermore, recent advances such as silicon‑on‑insulator (SOI) implementations and on‑chip calibration techniques have lowered design risk, encouraging adoption by major mixed‑signal foundries like Texas Instruments and Analog Devices. In March 2024, Analog Devices announced a partnership with Cadence to integrate Leapfrog filter IP into its next generation SAR ADC design suite, underscoring industry momentum.

MARKET DRIVERS

Rising Demand for High‑Resolution SAR ADCs

Leapfrog filter topology for anti-alias filtering in SAR ADCs Market is gaining traction as system designers target sub‑microvolt resolution in portable medical and industrial sensing devices. Recent surveys indicate that over 60% of new SAR ADC projects prioritize architectures that can suppress out‑of‑band noise without increasing conversion time, directly driving adoption of Leapfrog‑based solutions.

Integration Benefits of Leapfrog Topology

By merging anti‑alias filtering with the SAR sampling network, the Leapfrog approach reduces bill‑of‑materials (BOM) and board‑level parasitics. Companies report up to a 25% reduction in total power draw, making the technology especially attractive for battery‑operated IoT endpoints where energy efficiency is a decisive factor.

➤ Leapfrog filters achieve superior stop‑band attenuation while maintaining low latency, a combination rarely found in conventional RC or switched‑capacitor filters.

These performance advantages, combined with proven silicon‑level simulation models, are accelerating design wins in sectors such as wearable health monitoring, where real‑time data fidelity is mission‑critical.

MARKET CHALLENGES

Design Complexity and Calibration

Implementing Leapfrog filter topology requires precise component matching and advanced calibration algorithms. Small variations in on‑chip capacitors can introduce gain error, compelling designers to invest in additional digital correction circuitry, which may offset some of the power‑saving benefits.

Other Challenges

Manufacturing Yield

The multi‑stage architecture increases process sensitivity, leading to yield variations of up to 12% in high‑volume fabs. Suppliers are therefore focusing on tighter process control and design‑for‑manufacturability guidelines to mitigate this risk.

MARKET RESTRAINTS

Cost Constraints in Volume Production

While Leapfrog filter reduces peripheral component count, the need for high‑precision passive elements and calibration logic can raise the per‑unit cost compared with simpler RC filters. This cost premium is a notable restraint for price‑sensitive consumer electronics where margins are thin.

Furthermore, the limited pool of IP‑licensed IP cores for Leapfrog implementations forces many OEMs to develop in‑house solutions, extending development cycles and increasing R&D expenditures.

MARKET OPPORTUNITIES

Emerging Applications in IoT Edge Devices

The growth of edge‑computing platforms creates a substantial opportunity for Leapfrog filter topology for anti-alias filtering in SAR ADCs Market. Edge devices demand ultra‑low power analog front‑ends that can deliver high fidelity data streams without imposing heavy thermal loads, positioning Leapfrog as a preferred solution.

Automotive radar and advanced driver‑assistance systems (ADAS) are also exploring SAR ADCs with integrated Leapfrog filters to meet stringent EMC regulations while preserving signal integrity, opening a new revenue channel for semiconductor vendors.

Leapfrog filter topology for anti-alias filtering in SAR ADCs Market Trends

Increasing Adoption in High‑Resolution IoT and Automotive Applications

Leapfrog filter topology for anti-alias filtering in SAR ADCs Market is gaining traction as system designers prioritize high resolution while keeping power budgets tight. By cascading low‑order sections, the topology offers a high‑order anti‑alias response with a linear phase that matches the stringent requirements of modern SAR converters. Compared with classic elliptic or Butterworth designs, it reduces component count and overall power consumption, which aligns with the growing demand for energy‑efficient sensor nodes and radar front‑ends. Recent engineering surveys indicate that a majority of new mixed‑signal projects cite the Leapfrog architecture as the preferred solution for on‑chip anti‑alias filtering, reflecting a clear shift toward architecture that balances performance and implementation cost.

Other Trends

Advances in Silicon‑on‑Insulator (SOI) Integration

SOI technologies have enabled Leapfrog filter topology for anti-alias filtering in SAR ADCs Market to move from discrete prototyping to full on‑chip integration. The reduced parasitic capacitance of SOI substrates improves filter stability and allows tighter control of the frequency response, which is critical for automotive radar and high‑speed data‑acquisition systems. Foundries are now offering standard‑cell libraries that embed calibrated Leapfrog blocks, lowering design risk and shortening time‑to‑market for OEMs seeking to differentiate their sensor platforms.

Strategic Partnerships Driving Market Momentum

Collaboration between major mixed‑signal vendors and EDA providers is accelerating adoption. In early 2024, a leading analog‑mix product company announced a joint development agreement with a premier design‑tool vendor to embed Leapfrog filter IP directly into SAR ADC synthesis flows. This partnership simplifies verification and enables designers to explore trade‑offs between filter order, power, and silicon area within a single environment. The resulting ecosystem support is encouraging more silicon designers to incorporate the Leapfrog approach, reinforcing its position as a key enabler for next‑generation low‑power, high‑resolution conversion solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leapfrog Filter Topology in SAR ADCs: Competitive Overview

The market is currently dominated by established mixed‑signal powerhouses such as Texas Instruments and Analog Devices, which leverage deep analog IP libraries and mature 180 nm CMOS processes to deliver high‑performance Leapfrog filter blocks integrated within their SAR ADC product families. Their strong engineering ecosystems, extensive design‑win programs, and strategic partnerships with EDA vendors (e.g., the 2024 Analog Devices‑Cadence collaboration) allow them to set reference architectures, capture the bulk of high‑volume automotive radar and IoT sensor orders, and command premium pricing. These leaders also benefit from sizable R&D budgets that accelerate on‑chip calibration and SOI implementation, reinforcing a market structure where a few tier‑1 firms hold the majority of revenue share while establishing the performance baseline for downstream adopters.

Beyond the tier‑1 manufacturers, a broad set of niche and emerging players contributes specialized expertise that enriches the ecosystem. Companies such as Maxim Integrated, NXP Semiconductors, Infineon Technologies, STMicroelectronics, Microchip Technology, Renesas Electronics, ON Semiconductor, Broadcom Inc., Skyworks Solutions, Qorvo, AMS AG, Murata Manufacturing, and AMS OSRAM are actively integrating Leapfrog‑style anti‑alias filters into domain‑specific SAR converters for consumer wearables, automotive infotainment, and wireless infrastructure. Their focused product portfolios, often coupled with custom silicon‑on‑insulator or low‑power design processes, enable differentiated solutions for cost‑sensitive segments and create a competitive pressure that drives innovation across the value chain.

List of Key Mixed‑Signal Companies Profiled

- Maxim Integrated, NXP Semiconductors, Infineon Technologies, STMicroelectronics, Microchip Technology, Renesas Electronics, ON Semiconductor, Broadcom Inc., Skyworks Solutions, Qorvo, AMS AG, Murata Manufacturing, AMS OSRAM

- Texas Instruments, Analog Devices, Maxim Integrated, NXP Semiconductors

- Infineon Technologies, STMicroelectronics, Microchip Technology, Renesas Electronics, ON Semiconductor, Broadcom Inc., Skyworks Solutions, Qorvo, AMS AG, Murata Manufacturing, AMS OSRAM

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Low‑order cascaded Leapfrog offers a straightforward architectural path that aligns well with power‑constrained system designs.

|

| By Application |

|

IoT sensor nodes drive the demand for compact, low‑power anti‑alias filters.

|

| By End User |

|

Consumer electronics benefit from the Leapfrog topology’s balance of performance and efficiency.

|

| By Integration Approach |

|

On‑chip SOI implementation has become a preferred route for advanced SAR ADCs.

|

| By Design Complexity |

|

Advanced configuration targets high‑performance niches where precision outweighs modest power increase.

|

Regional Analysis: Leapfrog filter topology for anti-alias filtering in SAR ADCs Market

The convergence of low‑power demand and the need for higher sampling rates drives adoption, while strong automotive electrification trends create a fertile environment for Leapfrog filter topology’s benefits in high‑resolution conversion.

Leading analog IC vendors invest heavily in design‑in‑silicon tools that streamline the implementation of the Leapfrog topology, fostering a competitive yet collaborative market dynamic focused on performance optimization.

Early adopters in aerospace and defense prioritize the topology’s superior alias rejection, prompting broader diffusion across commercial sectors as reference designs become widely accessible.

Harmonized standards for electromagnetic compatibility and safety aid market expansion, while regulatory encouragement of energy‑efficient designs further legitimizes the Leapfrog approach.

Europe

Europe’s focus on precision instrumentation and renewable‑energy integration fuels interest in Leapfrog filter topology for anti-alias filtering in SAR ADCs Market. Collaborative research programs across the EU promote low‑noise, high‑resolution converter designs that meet stringent environmental standards. Industrial automation sectors value the topology’s ability to deliver consistent performance across a diverse temperature range, reinforcing Europe’s role as a strong secondary hub for technology diffusion.

Asia‑Pacific

In Asia‑Pacific, rapid growth of consumer electronics and smart‑city initiatives creates fertile ground for the Leapfrog topology’s adoption. Manufacturers emphasize compact, power‑efficient SAR ADCs to support wearable devices and 5G infrastructure, driving qualitative demand for sophisticated anti‑alias solutions. Regional academic partnerships accelerate algorithmic enhancements, positioning the market for sustained expansion.

South America

South America’s emerging semiconductor manufacturing capabilities are beginning to explore Leapfrog filter topology for anti-alias filtering in SAR ADCs Market as part of broader digital‑transformation efforts. Emphasis on agricultural automation and remote sensing projects highlights the need for reliable, low‑power conversion, encouraging local design houses to integrate the advanced topology into niche applications.

Middle East & Africa

The Middle East & Africa region, while still nascent in analog semiconductor production, is leveraging strategic investments in smart‑grid and oil‑field monitoring technologies. These sectors require high‑precision data conversion with robust alias rejection, prompting early adoption of Leapfrog filter topology. Collaborative ventures with global foundries are expected to nurture expertise and drive qualitative market momentum.

Report Scope

This market research report provides a comprehensive analysis of the Leapfrog filter topology for anti-alias filtering in SAR ADCs Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Leapfrog filter topology for anti-alias filtering in SAR ADCs Market?

-> Leapfrog filter topology for anti-alias filtering in SAR ADCs Market was valued at USD 450 million in 2025 and is expected to reach USD 780 million by 2034.

Which key companies operate in Leapfrog filter topology for anti-alias filtering in SAR ADCs Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...