MARKET INSIGHTS

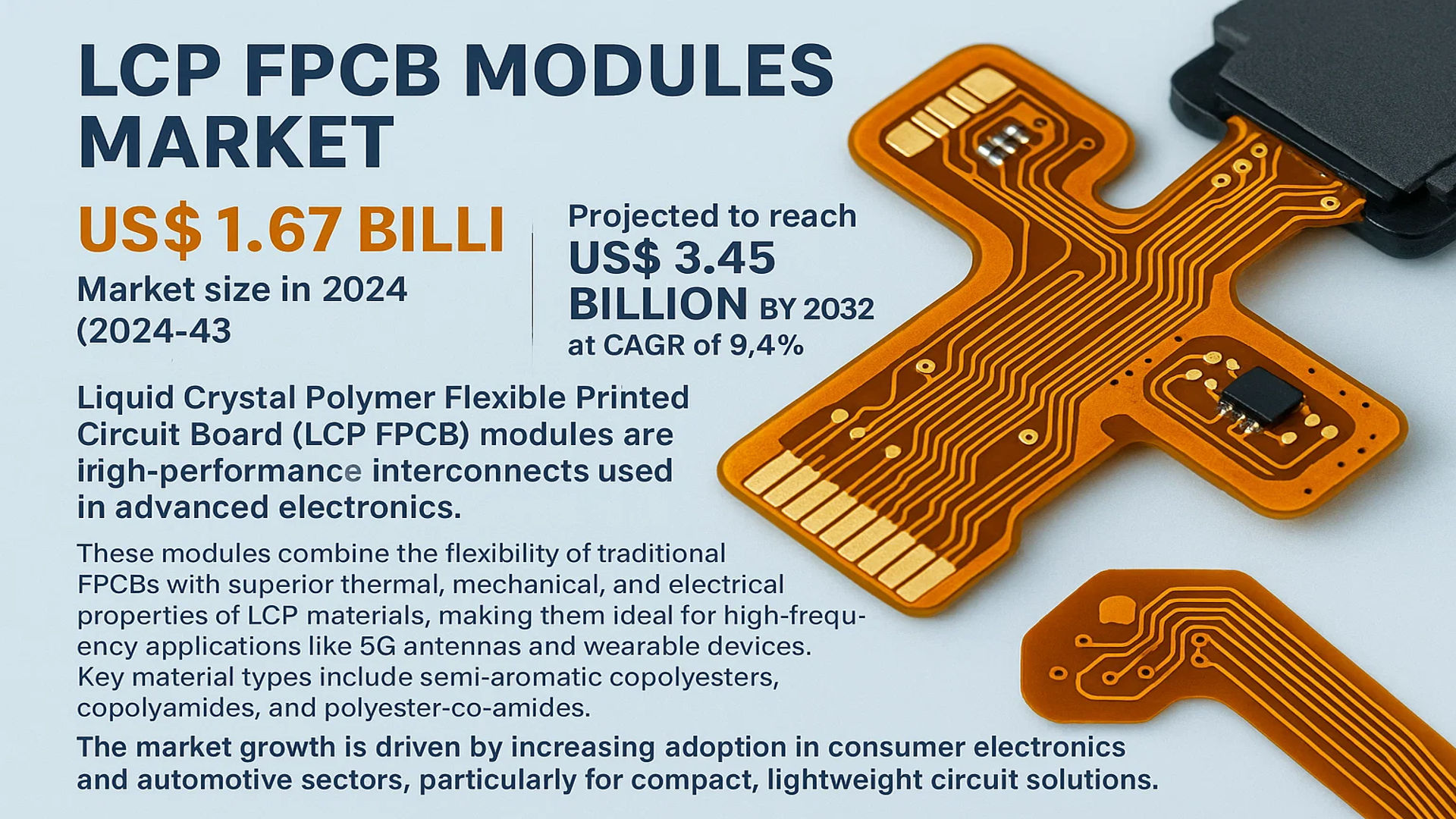

The global LCP FPCB Modules Market size was valued at US$ 1.67 billion in 2024 and is projected to reach US$ 3.45 billion by 2032, at a CAGR of 9.4% during the forecast period 2025-2032.

Liquid Crystal Polymer Flexible Printed Circuit Board (LCP FPCB) modules are high-performance interconnects used in advanced electronics. These modules combine the flexibility of traditional FPCBs with superior thermal, mechanical, and electrical properties of LCP materials, making them ideal for high-frequency applications like 5G antennas and wearable devices. Key material types include semi-aromatic copolyesters, copolyamides, and polyester-co-amides.

The market growth is driven by increasing adoption in consumer electronics and automotive sectors, particularly for compact, lightweight circuit solutions. While 5G expansion creates new opportunities, material costs remain a challenge. Leading manufacturers like Fujikura and Amphenol are investing in production scaling, with Asia-Pacific dominating over 65% of global supply.

MARKET DYNAMICS

MARKET DRIVERS

5G Technology Expansion Accelerates Demand for High-Frequency LCP FPCB Modules

The global rollout of 5G networks is creating unprecedented demand for Liquid Crystal Polymer Flexible Printed Circuit Boards (LCP FPCBs), which offer superior high-frequency signal integrity. With 5G requiring transmission frequencies up to 6GHz and beyond, LCP’s low dielectric constant (Dk ~2.9) and low dissipation factor (Df ~0.002) make it the material of choice for antenna modules and RF components. The mobile industry’s transition to millimeter-wave 5G bands (24-100GHz) particularly benefits LCP adoption, as traditional PI-based FPCBs struggle with signal loss at these frequencies.

Consumer Electronics Miniaturization Drives LCP FPCB Innovation

Smartphone manufacturers continue pushing the boundaries of device thinness while packing in more functionality, creating ideal conditions for LCP FPCB adoption. The material’s ability to support ultra-fine pitch traces (below 25μm) and withstand repeated bending cycles makes it critical for foldable displays and compact internal designs. Major OEMs now standardize LCP modules for antenna integration, with leading smartphone brands allocating 15-20% of their total PCB budget specifically for LCP solutions in flagship models. This trend extends to wearables and AR/VR devices where space constraints demand high-density interconnects.

Automotive Electrification Creates New Growth Vectors

The automotive industry’s transition to electric vehicles and advanced driver assistance systems (ADAS) presents significant opportunities for LCP FPCB manufacturers. Electric vehicles require high-reliability interconnects for battery management systems that can withstand temperature fluctuations from -40°C to 150°C – a range where LCP outperforms traditional materials. Furthermore, the proliferation of millimeter-wave radar and LiDAR sensors in autonomous vehicles benefits from LCP’s stable dielectric properties across operating frequencies. Premium automakers now specify LCP-based flexible circuits for critical safety systems, creating a market segment expected to grow at over 25% annually through 2030.

MARKET RESTRAINTS

High Material Costs and Complex Processing Limit Market Penetration

While LCP FPCB technology offers superior performance, its adoption faces significant cost barriers. LCP resin raw materials carry a 3-5x premium over conventional polyimide, and the specialized processing equipment required for LCP lamination and laser drilling adds substantial capital expenditure. These cost factors make LCP solutions economically prohibitive for mid-range and budget electronic devices, confining adoption primarily to premium segments. Additionally, the tight thermal control requirements during manufacturing (processing windows ±2°C) result in higher scrap rates compared to traditional FPCB materials.

Supply Chain Concentration Creates Vulnerability

The LCP FPCB market faces constraints from concentrated supply chains, with over 80% of high-grade LCP resin production controlled by a handful of chemical manufacturers primarily in Japan and the United States. This concentration creates potential bottlenecks during periods of strong demand growth. Furthermore, the specialized etching and plating processes for LCP circuits remain proprietary technologies at a limited number of FPCB fabricators, creating capacity constraints. The recent geopolitical tensions affecting advanced material exports have exacerbated these supply chain risks, causing some OEMs to maintain dual sourcing strategies that slow adoption timelines.

Design Complexity Challenges Widespread Engineering Adoption

LCP’s anisotropic thermal expansion properties present unique design challenges that require specialized engineering expertise. The material’s different coefficients of thermal expansion in X/Y versus Z axes (often 10-17 ppm/°C vs 80-200 ppm/°C) can cause reliability issues if not properly accounted for in the design phase. Many electronics manufacturers lack in-house expertise to redesign circuits for LCP’s unique characteristics, causing hesitation in adoption. Additionally, the limited availability of comprehensive design guidelines and simulation tools tailored for LCP FPCBs creates a knowledge gap that slows broader market acceptance.

MARKET OPPORTUNITIES

Emerging 6G Development Opens New Frontier for Ultra-High Frequency Applications

The nascent development of 6G wireless technology, targeting frequencies above 100GHz, presents substantial long-term opportunities for LCP FPCB solutions. Early research indicates LCP maintains stable dielectric properties even in terahertz ranges, positioning it as a critical enabler for future sub-THz wireless systems. Leading telecom equipment providers have already initiated partnerships with LCP material suppliers to develop next-generation antenna-in-package solutions. The anticipated performance requirements for 6G – including data rates exceeding 1Tbps and latency below 100μs – will likely mandate LCP’s use in both base station and device-side RF components.

Medical Electronics Innovations Drive High-Reliability Demand

The medical device industry’s increasing adoption of wearable diagnostics and implantable electronics creates promising opportunities for LCP FPCB manufacturers. LCP’s biocompatibility, moisture resistance (water absorption <0.02%), and sterilization compatibility (withstanding autoclave cycles) make it ideal for medical applications. Emerging uses include flexible neural interfaces where LPC’s stable impedance characteristics enable high-density electrode arrays, and ingestible sensors requiring reliable operation in harsh bodily environments. Regulatory approvals for several LCP-based medical devices in recent years have paved the way for broader adoption across therapeutic and diagnostic applications.

Advanced Packaging Trends Favor LCP Integration

The semiconductor industry’s shift toward heterogeneous integration and chiplet architectures benefits LCP FPCB technology. As package interconnects move to increasingly finer pitches below 10μm, LCP’s dimensional stability and low coefficient of thermal expansion (CTE) make it attractive for interposer and redistribution layer applications. Leading OSATs are evaluating LCP as a potential organic substrate alternative for high-performance computing packages, particularly where high-frequency operation is required. The material’s ability to support embedded passive components further enhances its value proposition for advanced packaging solutions targeting AI accelerators and high-bandwidth memory applications.

MARKET CHALLENGES

Material Alternatives Threaten Long-Term Technology Positioning

Emerging substrate materials pose competitive challenges to LCP’s dominance in high-frequency applications. Modified polyimides with fluoropolymer additives now achieve dielectric properties approaching LCP performance at lower costs, particularly for frequencies below 30GHz. Additionally, hydrocarbon-based laminates with liquid crystal filler technology demonstrate comparable RF performance with better mechanical stability in some applications. These alternatives benefit from established manufacturing infrastructures, potentially slowing LCP adoption in cost-sensitive market segments unless significant material cost reductions occur.

Recycling and Environmental Considerations Grow in Importance

Increasing environmental regulations regarding electronics manufacturing create challenges for LCP FPCB adoption. Unlike conventional FR-4 laminates, LCP materials cannot be easily recycled using standard PCB recycling processes, requiring specialized thermal decomposition methods. The European Union’s evolving regulations on persistent organic pollutants (POPs) and restrictions on halogenated flame retardants may necessitate reformulation of some LCP compounds. Furthermore, the energy-intensive LCP polymerization process conflicts with some OEMs’ carbon reduction targets, prompting evaluations of alternative sustainable high-performance materials.

Talent Shortage Limits Production Capacity Expansion

The specialized nature of LCP FPCB manufacturing creates significant workforce challenges. Processing LCP requires operators with expertise in precision thermal management and laser micromachining – skills in short supply globally. The average training period for LCP-specific process engineers exceeds 18 months, creating bottlenecks in production scaling. Furthermore, the concentration of expertise in specific geographic regions makes rapid global expansion difficult. Without substantial investment in workforce development programs, these talent constraints may limit the industry’s ability to meet projected demand growth through 2030.

LCP FPCB MODULES MARKET TRENDS

Expanding 5G and High-Frequency Applications Drive Market Growth

The global LCP FPCB modules market is experiencing significant growth due to expanding 5G networks and high-frequency applications in consumer electronics and automotive sectors. Liquid Crystal Polymer (LCP) Flexible Printed Circuit Boards (FPCB) are gaining traction for their exceptional electrical performance in high-frequency environments, low dielectric loss, and superior thermal stability. The proliferation of 5G technology, which operates at higher frequencies, has intensified demand for LCP FPCBs, as they minimize signal loss and interference. Additionally, the automotive industry’s shift towards advanced driver-assistance systems (ADAS) and in-vehicle infotainment further fuels adoption. In 2024, the market was valued at $X million, projected to reach $Y million by 2032, growing at a CAGR of Z%.

Other Trends

Miniaturization in Consumer Electronics

The trend towards slimmer, lighter, and more compact consumer electronics is accelerating the adoption of LCP FPCB modules. Smartphones, wearables, and foldable devices require flexible circuitry with high-density interconnects, a niche where LCP excels. Leading smartphone manufacturers are integrating these modules to enhance signal integrity while reducing space constraints. Meanwhile, wearables demand durability and flexibility, making LCP FPCBs a preferred choice. The rise of foldable display technology has further heightened demand, as these devices require flexible substrates capable of enduring repeated bending cycles without performance degradation.

Supply Chain Localization and Regional Manufacturing Shifts

Geopolitical tensions and supply chain disruptions have prompted a strategic shift towards localized manufacturing of LCP FPCBs, particularly in Asia. China dominates production, accounting for over 60% of global PCB output, with Taiwan, Japan, and South Korea also playing pivotal roles. Recent investments in domestic LCP material production aim to reduce reliance on imports, as seen in China’s push for self-sufficiency in high-performance substrates. Meanwhile, North American and European manufacturers are diversifying supply chains by partnering with regional suppliers, though material costs and technical barriers remain challenges. This localization trend is expected to reshape competitive dynamics and influence pricing strategies.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Innovation to Capture Growth in High-Tech Applications

The global LCP FPCB (Liquid Crystal Polymer Flexible Printed Circuit Board) modules market features a dynamic competitive landscape with both established multinational corporations and agile regional players. Fujikura Ltd., a Japanese leader in electronic components, has emerged as a dominant force in this space, leveraging its extensive R&D capabilities and strategic partnerships with major consumer electronics brands. The company’s focus on ultra-thin, high-frequency LCP solutions has given it a competitive edge in 5G and wearable applications.

Meanwhile, Amphenol Corporation has significantly expanded its market share through vertical integration and acquisitions in the advanced PCB sector. Their comprehensive product portfolio, spanning automotive, aerospace, and industrial applications, positions them strongly in the high-reliability segment of the LCP FPCB market.

Chinese manufacturers are rapidly catching up with technological advancements. Luxshare Precision and Shenzhen Sunway have made substantial investments in LCP production capacity, capitalizing on the growing domestic demand for premium flexible circuits in smartphones and IoT devices. These companies benefit from China’s robust electronics manufacturing ecosystem, though they face increasing competition from Japanese and South Korean counterparts.

With the market projected to grow significantly through 2032, companies are pursuing distinct strategies – while Japanese firms emphasize material science innovations, Chinese players compete on cost efficiency and rapid prototyping capabilities. This diversity in competitive approaches is driving overall market advancement while keeping downward pressure on prices.

List of Key LCP FPCB Module Companies Profiled

- Fujikura Ltd. (Japan)

- Amphenol Corporation (U.S.)

- Luxshare Precision Industry Co., Ltd. (China)

- Shenzhen Sunway Communication Co., Ltd. (China)

- Huizhou Speed Wireless Technology Co., Ltd. (China)

- Forewin Suzhou Electronics Technology Co., Ltd. (China)

- Holitech Technology Co., Ltd. (China)

- AAC Technologies (China)

- Electric Connector Technology Co., Ltd. (Taiwan)

Segment Analysis:

By Type

Semi-Aromatic Copolyesters Lead the Market Due to Superior Electrical Performance and Thermal Stability

The market is segmented based on type into:

- Semi-aromatic copolyesters

- Copolyamides

- Polyester-co-amides

- Others

By Application

Consumer Electronics Segment Dominates Due to Rising Demand for Miniaturized and High-Frequency Components

The market is segmented based on application into:

- Consumer electronics

- Subtypes: Smartphones, wearables, tablets and others

- Automotive

- Subtypes: ADAS, infotainment systems and others

- Aerospace and defense

- Medical devices

- Others

By End-User

OEMs Hold Largest Share Due to Direct Integration in Device Manufacturing

The market is segmented based on end-user into:

- Original equipment manufacturers (OEMs)

- Electronic manufacturing service providers

- Aftermarket suppliers

Regional Analysis: LCP FPCB Modules Market

Asia-Pacific

As the dominant force in the global LCP FPCB Modules market, Asia-Pacific accounts for over 60% of total production and consumption. China stands as the epicenter of manufacturing, propelled by its robust electronics ecosystem and government initiatives like Made in China 2025. Japan and South Korea contribute significantly through their advanced material science capabilities, particularly in high-frequency applications for 5G and automotive electronics. While cost-competitive manufacturing drives growth in Southeast Asia, regulatory pressures are gradually pushing manufacturers toward environmentally sustainable production methods. The region’s explosive demand for smartphones, wearables, and electric vehicles continues to fuel innovation in flexible circuit solutions.

North America

The North American market prioritizes high-performance LCP FPCB solutions for aerospace, defense, and premium consumer electronics applications. With major tech companies like Apple increasingly adopting LCP-based antennas, domestic manufacturers are investing in R&D to improve signal integrity and thermal stability. The CHIPS Act provisions have indirectly supported supply chain development for advanced PCB technologies, though the region faces challenges in scaling production capacity. Collaboration between material scientists and PCB fabricators is driving breakthroughs in multilayer LCP designs, particularly for millimeter-wave applications in next-generation communication systems.

Europe

European demand focuses on automotive and industrial applications where reliability under extreme conditions is paramount. German automakers are leading the adoption of LCP FPCBs for in-vehicle networking systems, while Nordic countries show strong uptake in medical device applications. Strict RoHS and REACH compliance requirements have pushed manufacturers toward halogen-free and recyclable material formulations. While the region lacks large-scale production facilities, it maintains technological leadership in niche high-value applications through companies like AT&S and Schweizer Electronic.

Middle East & Africa

This emerging market shows promising growth potential, particularly in the UAE and Israel, where increasing investments in telecommunications infrastructure are driving demand for high-frequency PCB solutions. The lack of local manufacturing capabilities currently makes the region dependent on imports, though several technology free zones are attracting foreign PCB manufacturers. Government initiatives to diversify economies away from oil dependence are creating opportunities for electronics manufacturing, with LCP FPCB adoption expected to grow alongside 5G network deployments.

South America

The market remains in early development stages, with Brazil showing the most activity through its aerospace and automotive sectors. Economic volatility and limited local expertise in advanced PCB technologies have constrained growth, though increasing smartphone penetration and the gradual rollout of 5G networks present long-term opportunities. The region currently serves as an importer of finished modules rather than a manufacturing hub, with most demand being met by Asian suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global LCP FPCB Modules market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LCP FPCB Modules Market?

-> LCP FPCB Modules Market size was valued at US$ 1.67 billion in 2024 and is projected to reach US$ 3.45 billion by 2032, at a CAGR of 9.4% during the forecast period 2025-2032.

Which key companies operate in Global LCP FPCB Modules Market?

-> Key players include Fujikura, Amphenol, Luxshare Precision, Shenzhen Sunway, Huizhou Speed Wireless, Forewin Suzhou Electronics, Holitech Technology, AAC Technologies, and Electric Connector Tech.

What are the key growth drivers?

-> Key growth drivers include rising demand for miniaturized electronic components, increasing adoption in 5G devices, and advancements in flexible printed circuit board (FPCB) technologies.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 65% of global demand, driven by strong electronics manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of ultra-thin LCP FPCB modules, integration with IoT devices, and increasing use in automotive electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...