Lab-on-Chip Semiconductor Market Insights

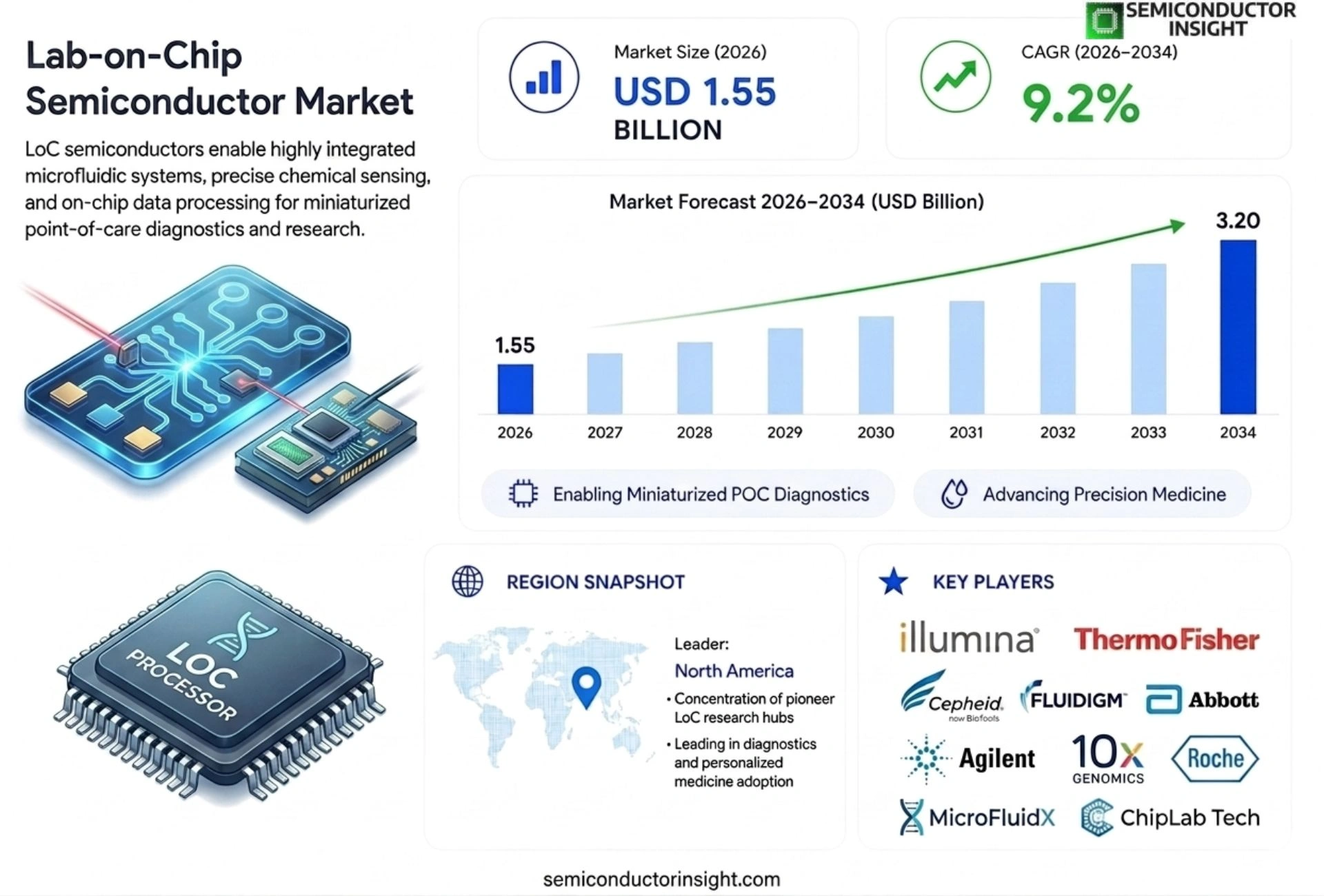

Global Lab-on-Chip Semiconductor market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 3.20 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period.

Lab‑on‑Chip semiconductors are highly integrated silicon‑based platforms that combine microfluidic channels, sensors, and electronic circuitry on a single chip to perform complex biochemical assays, point‑of‑care diagnostics, and drug discovery workflows with reduced sample volumes and faster turnaround times.

The market is experiencing rapid expansion because investment in precision medicine is accelerating, manufacturing advances such as CMOS scaling are lowering production costs, and regulatory support for decentralized testing is increasing adoption across hospitals and research labs. Furthermore, collaborations between semiconductor foundries and biotech firms,exemplified by the 2023 partnership between Intel’s Foundry Services and Thermo Fisher Scientific,are driving innovation and widening the addressable market.

MARKET DRIVERS

Increasing Demand for Point‑of‑Care Diagnostics

Lab-on-Chip Semiconductor Market is being propelled by a surge in point‑of‑care diagnostic devices, driven by aging populations and the need for rapid testing in remote settings. Healthcare providers are seeking compact, low‑cost platforms that deliver laboratory‑grade results at the bedside, creating a strong growth engine for semiconductor‑based micro‑fluidic solutions.

Advancements in Semiconductor Fabrication

Recent breakthroughs in advanced lithography and 3D stacking enable higher integration density for Lab‑on‑Chip platforms, reducing power consumption while increasing assay throughput. These technology gains make it feasible to embed complex fluidic networks on a single silicon die, reinforcing the market’s expansion prospects.

➤ Integration of microfluidics with CMOS technology accelerates assay speed, positioning Lab‑on‑Chip semiconductor Market for rapid adoption across clinical and industrial domains.

Overall, the convergence of healthcare imperatives and semiconductor innovation establishes a robust foundation for sustained market momentum, with manufacturers focusing on scalable production to meet global demand.

MARKET CHALLENGES

High Development Costs

Designing and qualifying Lab‑on‑Chip devices requires significant investment in both R&D and specialized fabrication equipment. The capital intensity of creating custom CMOS‑based fluidic architectures often limits entry to well‑funded players, creating a barrier for smaller innovators.

Other Challenges

Regulatory Hurdles

Achieving compliance with medical device regulations across multiple jurisdictions adds complexity and time to product launch cycles, slowing market entry for new solutions.

Additionally, aligning semiconductor supply chain reliability with the precise material requirements of micro‑fluidic components remains an operational challenge that can affect delivery schedules.

MARKET RESTRAINTS

Limited Material Compatibility

Many semiconductor processes rely on materials that are not inherently compatible with biological fluids, necessitating additional surface treatments or encapsulation steps. These extra processes increase manufacturing complexity and can constrain the range of applications for Lab‑on‑Chip semiconductor Market.

MARKET OPPORTUNITIES

Emerging Applications in Environmental Monitoring

Beyond healthcare, there is growing interest in deploying Lab‑on‑Chip sensors for real‑time detection of pollutants and pathogens in water and air. The combination of semiconductor robustness and micro‑fluidic precision offers a compelling value proposition for governments and utilities seeking automated monitoring solutions.

Investment in scalable manufacturing lines and strategic partnerships with biotech firms are expected to unlock new revenue streams, positioning Lab‑on‑Chip semiconductor Market at the forefront of next‑generation analytical technologies.

Lab-on-Chip Semiconductor Market Trends

CMOS Scaling Enables Lower‑Cost, High‑Volume Production

Lab-on-Chip Semiconductor Market is being reshaped by the adoption of advanced CMOS scaling techniques, which allow manufacturers to place more functional elements on a single silicon die without proportional cost increases. This integration of micro‑fluidic channels, sensors, and electronic circuitry on the same substrate improves assay throughput while cutting material waste. As production lines transition from specialized MEMS processes to mainstream semiconductor fabs, component yields rise and per‑unit pricing drops, making point‑of‑care diagnostics financially viable for a broader range of healthcare providers. The resulting economic advantage also encourages start‑ups to adopt Lab‑on‑Chip solutions for drug discovery and environmental monitoring.

Other Trends

Strategic Partnerships Accelerate Innovation

Collaboration between established semiconductor foundries and biotech firms is a defining feature of Lab‑on‑Chip semiconductor Market. The 2023 alliance between Intel’s Foundry Services and Thermo Fisher Scientific exemplifies how shared R&D resources accelerate the rollout of next‑generation assay platforms. Such partnerships combine deep expertise in high‑density transistor design with domain knowledge of biochemical workflows, shortening development cycles and expanding product portfolios. Participants benefit from joint access to silicon‑photonic design kits, enabling the integration of optical detection methods directly onto chips, a capability previously limited to niche research labs. These co‑development models are attracting additional venture capital, further reinforcing the market’s growth trajectory.

Regulatory Support Expands Decentralized Testing

Regulators worldwide are updating guidelines to accommodate decentralized diagnostic formats, recognizing the public‑health benefits of rapid, on‑site testing. Policies that streamline approval pathways for Lab‑on‑Chip devices reduce time‑to‑market, encouraging manufacturers to invest in scalable production. At the same time, reimbursement frameworks are evolving to cover point‑of‑care assays, providing financial incentives for hospitals and clinics to replace centralized laboratory workflows. This regulatory momentum, coupled with the demonstrated reliability of silicon‑based platforms, is driving broader adoption across both urban and rural healthcare settings, reinforcing the overall resilience of Lab‑on‑Chip semiconductor Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Lab-on-Chip Semiconductor Market Competitive Landscape

Lab‑on‑Chip semiconductor sector is anchored by a handful of large integrated‑device manufacturers that combine advanced CMOS foundry capabilities with biotech expertise. Intel’s Foundry Services, through its strategic alliance with Thermo Fisher Scientific, leads the market by leveraging 7‑nm silicon‑on‑insulator processes to deliver high‑density sensor arrays on a single die. This partnership has accelerated time‑to‑market for point‑of‑care diagnostics and solidified a vertically integrated supply chain that pressures smaller rivals to pursue niche applications. Meanwhile, Applied Materials and STMicroelectronics provide essential wafer‑scale fabrication equipment and design‑for‑manufacturing services, reinforcing a consolidated ecosystem where scale and process standardization dictate market share.

Beyond the tier‑one giants, a vibrant cohort of specialized firms drives product differentiation in niche verticals such as personalized drug screening and environmental monitoring. Companies like Silicon Biosystems, Illumina, Roche Diagnostics, and Agilent Technologies focus on ultra‑low‑volume fluidic integration, while Texas Instruments and Analog Devices contribute analog front‑end expertise for electrochemical sensing. Emerging players such as Qorvo, NXP Semiconductors, and Micron Technology are expanding into heterogeneous integration to embed memory and RF capabilities directly onto Lab‑on‑Chip platforms, thereby broadening functional scope without sacrificing form‑factor. This diversified landscape creates a competitive pressure matrix where innovation speed, foundry access, and cross‑industry collaborations are the primary differentiators.

List of Key Lab-on-Chip Semiconductor Companies Profiled

- Intel Corporation

- Thermo Fisher Scientific

- Applied Materials, Inc.

- Illumina, Inc.

- Silicon Biosystems

- Roche Diagnostics

- Agilent Technologies

- Texas Instruments

- Analog Devices

- Qorvo, Inc.

- NXP Semiconductors

- STMicroelectronics

- Micron Technology

- Bio‑Rad Laboratories

- Qualcomm Incorporated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CMOS‑based Lab‑on‑Chip is emerging as the leading segment because:

|

| By Application |

|

Point‑of‑Care Diagnostics dominates this dimension owing to:

|

| By End User |

|

Hospitals & Clinical Laboratories are the primary end‑users because:

|

| By Integration Level |

|

Fully Integrated Systems lead this category due to:

|

| By Device Form Factor |

|

Handheld Portable Devices are gaining traction because:

|

Regional Analysis: North America

The primary drivers for Lab-on-Chip Semiconductor Market in the US include increasing demand for point-of-care diagnostics, advancements in microfluidic technology, and growing healthcare expenditure.

The integration of advanced semiconductor components allows for more sophisticated and accurate testing, contributing to faster diagnosis and improved patient outcomes.

Continual advancements in chip design, fabrication processes, and sensor integration are crucial for enhancing the performance and functionality of Lab-on-Chip devices. Research into novel materials and architectures is leading to smaller, more energy-efficient, and cost-effective solutions.

The development of bio-compatible materials for enhanced device performance and safety is also a key area of focus.

The US market is characterized by a mix of established players and emerging companies vying for market share. Key competitive strategies involve product innovation, strategic partnerships, and expansion into new applications. Many companies are focusing on developing customized solutions tailored to specific diagnostic needs.

Lab-on-Chip Semiconductor Market in the US is subject to stringent regulatory requirements from bodies like the FDA. Compliance with these regulations is essential for market entry and product commercialization. The regulatory landscape is constantly evolving, requiring companies to stay abreast of the latest guidelines.

Europe

Europe represents a significant market for Lab-on-Chip Semiconductor technology, with countries like Germany, the UK, and France leading the way. The region benefits from a strong emphasis on precision medicine and a well-established healthcare system. Focus on sustainability and environmentally friendly medical devices is also a major trend. The collaborative nature of European research institutions facilitates rapid innovation and technology transfer. The growing elderly population and increasing prevalence of age-related diseases further drive demand. Investment in smart healthcare solutions is also bolstering market growth throughout Europe.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing market for Lab-on-Chip Semiconductor solutions, driven by rapid economic growth, increasing healthcare spending, and rising awareness of preventive healthcare measures. China, Japan, and South Korea are key markets in the region. The availability of low-cost manufacturing capabilities in countries like China provides a competitive advantage. Government initiatives promoting domestic semiconductor manufacturing are also fueling market expansion. Increasing urbanization and a growing middle class are further contributing to the demand for advanced diagnostic tools.

South America

South America presents a moderate growth opportunity for Lab-on-Chip Semiconductor Market. Brazil and Argentina are the largest markets in the region. Increasing healthcare infrastructure development and growing disposable incomes are key drivers. The rising prevalence of infectious diseases and chronic conditions is also fueling demand for rapid and accurate diagnostic tests. However, challenges such as limited access to healthcare and economic instability can hinder market growth.

Middle East & Africa

The Middle East & Africa region offers potential for growth Lab-on-Chip Semiconductor Market, particularly in countries with expanding healthcare systems and increasing investments in medical technology. Saudi Arabia and South Africa are key markets. The rising prevalence of diabetes and cardiovascular diseases is driving demand for diagnostic tools. Government initiatives to improve healthcare infrastructure and promote local manufacturing are also contributing to market expansion.

Report Scope

This market research report provides a comprehensive analysis of the Lab-on-Chip Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Lab-on-Chip Semiconductor Market?

-> Lab-on-Chip Semiconductor market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 3.20 billion by 2034, exhibiting a CAGR of 9.2%

Which key companies operate Lab-on-Chip Semiconductor Market?

-> Key players include Intel (Foundry Services) and Thermo Fisher Scientific, representing leading semiconductor and biotech collaborations in this space.

What are the key growth drivers?

-> Key growth drivers include investment in precision medicine, manufacturing advances such as CMOS scaling, and regulatory support for decentralized testing.

Which region dominates the market?

-> The reference does not specify a dominant region; market adoption is being driven globally by collaborations across major semiconductor hubs.

What are the emerging trends?

-> Emerging trends include partnerships between semiconductor foundries and biotech firms, integration of silicon‑based microfluidic platforms, and AI‑enabled diagnostic solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...