MARKET INSIGHTS

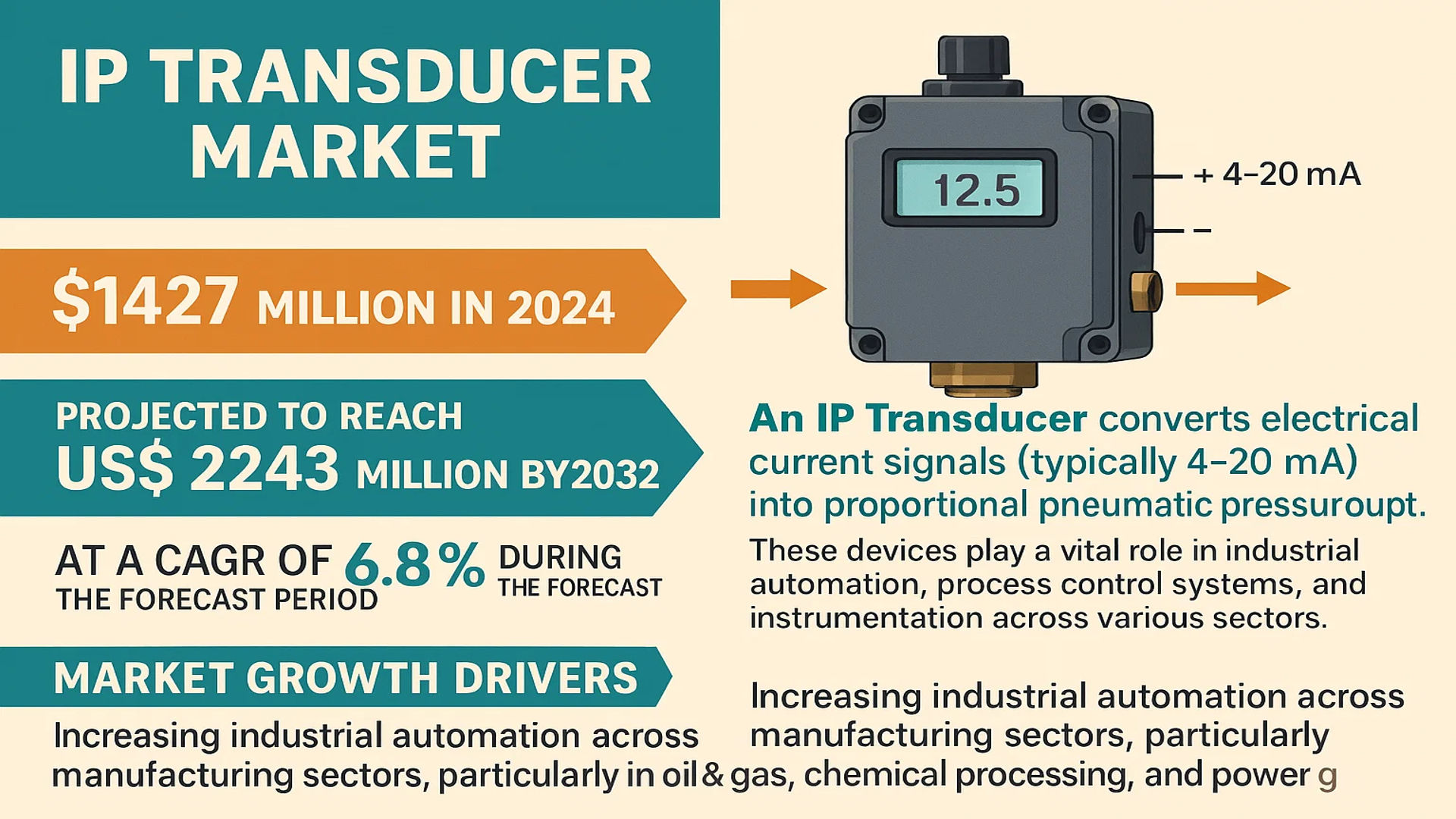

The global IP Transducer Market was valued at 1427 million in 2024 and is projected to reach US$ 2243 million by 2032, at a CAGR of 6.8% during the forecast period.

An IP Transducer (current-to-pressure transducer) is a critical industrial device that converts electrical current signals (typically 4-20 mA) into proportional pneumatic pressure output. These devices play a vital role in industrial automation, process control systems, and instrumentation across various sectors. The technology enables precise control of pneumatic actuators and valves by translating control signals from distributed control systems.

The market growth is primarily driven by increasing industrial automation across manufacturing sectors, particularly in oil & gas, chemical processing, and power generation. While the analog input segment currently dominates with over 70% market share, digital input transducers are gaining traction due to Industry 4.0 adoption. North America holds the largest market share at approximately 35%, followed by Europe and Asia-Pacific. Key players including ABB, Emerson, and Siemens are focusing on developing smart transducers with IoT capabilities to meet evolving industry demands.

MARKET DYNAMICS

MARKET DRIVERS

Growing Industrial Automation to Drive Adoption of IP Transducers

The global shift toward industrial automation continues to accelerate, with manufacturing and process industries increasingly adopting smart instrumentation for improved efficiency and control. This trend directly increases demand for IP transducers, which serve as critical components in converting electrical signals to pneumatic pressure outputs. The ability to precisely regulate mechanical actuators and control valves makes these devices indispensable in automated process control systems. Recent reports indicate that industries adopting automation solutions see productivity improvements of 20-30% while reducing operational costs by an estimated 15-25%, underscoring why IP transducers remain essential for modern industrial applications.

Stringent Process Control Requirements in Oil & Gas to Stimulate Market Growth

The oil and gas industry, one of the largest end-users of IP transducers, demands highly reliable pressure control systems for critical operations. With extraction and refining processes operating under extreme conditions, the need for robust signal conversion technology remains paramount. Major projects in LNG facilities, pipelines, and offshore platforms increasingly specify IP transducers for their proven reliability in hazardous environments. Investments in downstream infrastructure modernization, particularly in regions with aging facilities, are projected to maintain steady demand. For instance, refinery modernization projects across North America and Asia-Pacific collectively represent multi-billion dollar opportunities for process instrumentation suppliers.

Advancements in Smart Manufacturing Technologies to Accelerate Market Expansion

The integration of Industrial Internet of Things (IIoT) capabilities with process instrumentation presents significant growth opportunities for IP transducer manufacturers. Modern transducers with digital communication protocols enable real-time monitoring and predictive maintenance, reducing unplanned downtime in production facilities. Recent technological developments focus on enhancing device intelligence through embedded diagnostics and wireless connectivity options. Leading manufacturers have introduced IP65/67 rated transducers with HART and Foundation Fieldbus compatibility, meeting the evolving needs of Industry 4.0 implementations. This technological evolution positions IP transducers as vital components in the digital transformation of industrial operations.

MARKET RESTRAINTS

High Initial Costs and Installation Complexities Limit Market Penetration

While IP transducers offer substantial operational benefits, their adoption faces challenges due to significant upfront costs and installation requirements. The total cost of ownership extends beyond unit pricing to include specialized mounting hardware, calibration equipment, and skilled labor for proper integration into control systems. In price-sensitive markets, these financial considerations often lead plants to postpone upgrades or opt for lower-cost alternatives with reduced functionality. Additionally, retrofitting older facilities with modern transducers frequently requires structural modifications to accommodate new instrumentation standards, creating further implementation barriers.

Supply Chain Disruptions Impacting Manufacturing and Delivery Timelines

The global instrumentation market continues to experience supply chain volatility affecting critical components for IP transducer production. Semiconductor shortages and fluctuating raw material prices have led to extended lead times, with some manufacturers reporting 20-30% longer delivery periods compared to pre-pandemic levels. These disruptions particularly impact specialized transducers requiring custom configurations, where component availability becomes constrained. Customers in time-sensitive projects increasingly face difficult choices between waiting for preferred models or compromising with readily available alternatives that may not fully meet technical specifications.

Technical Limitations in Extreme Operating Conditions Present Challenges

While IP transducers demonstrate reliable performance across many industrial applications, certain extreme operating environments push the boundaries of current technology. Applications involving ultra-high pressures exceeding 10,000 psi or temperatures beyond standard operating ranges often require custom-engineered solutions with substantial cost premiums. The transducer’s pneumatic components remain vulnerable to contamination from process media containing particulates or corrosive elements, necessitating additional filtration and protection systems. These technical constraints continue to drive research into more robust materials and designs that can withstand increasingly demanding industrial processes.

MARKET OPPORTUNITIES

Emerging Markets Present Significant Growth Potential for Industrial Automation

Developing economies in Asia, Africa, and South America are investing heavily in industrial infrastructure, creating substantial opportunities for process instrumentation suppliers. Government initiatives promoting domestic manufacturing and Industry 4.0 adoption are driving new facility construction and process plant modernization across these regions. For IP transducer manufacturers, this translates to growing demand from sectors such as chemicals, water treatment, and food processing. Industry analyses suggest that automation adoption rates in emerging markets could grow 2-3 times faster than in mature economies over the next decade, representing a significant expansion opportunity for smart instrumentation providers.

Technological Convergence Creating New Application Areas

The integration of IP transducers with advanced control systems and analytics platforms opens new application possibilities beyond traditional process industries. Emerging sectors such as renewable energy systems, hydrogen production facilities, and carbon capture installations require precise pressure regulation and control. These technologies often operate at the intersection of mechanical and digital systems, where IP transducers serve as the crucial interface between electrical control signals and physical process adjustments. Manufacturers developing specialized transducers for these novel applications can establish early leadership positions in high-growth market segments.

Aftermarket Services and Retrofitting Offer Sustainable Revenue Streams

With installed bases of legacy transducers aging across industrial facilities worldwide, maintenance, calibration, and upgrading services represent a substantial business opportunity. Many plants face the challenge of maintaining obsolete transducer models while needing to improve control system performance. Smart retrofitting solutions that enable older transducers to integrate with modern digital control networks are gaining traction. Service-oriented business models that combine predictive maintenance technologies with transducer diagnostics create ongoing revenue opportunities while helping customers maximize the lifespan and performance of their existing instrumentation assets.

MARKET CHALLENGES

Intense Price Competition from Regional Manufacturers

The IP transducer market faces growing pricing pressures as regional manufacturers, particularly in Asia, offer competitively priced alternatives to established brands. These competitors often benefit from lower production costs and government support programs, enabling aggressive pricing strategies that challenge premium product positioning. While quality and reliability differences remain, the narrowing performance gap in standard applications forces all market participants to carefully balance pricing, features, and brand value. This dynamic creates particularly acute challenges for manufacturers serving price-sensitive market segments where technical differentiations become less pronounced.

Regulatory Compliance Across Multiple Jurisdictions Increases Complexity

Manufacturers must navigate an evolving landscape of regional and industry-specific certifications and standards for process instrumentation. Compliance requirements such as ATEX for hazardous locations, SIL ratings for safety systems, and various environmental regulations create development and certification burdens. The process of obtaining and maintaining these certifications across multiple markets significantly extends product development cycles and increases time-to-market. Furthermore, emerging sustainability reporting requirements are adding new dimensions to product compliance, requiring manufacturers to track and disclose environmental impacts throughout the product lifecycle.

Workforce Skill Gaps Impede Advanced Technology Adoption

The increasing sophistication of IP transducer technology and integrated control systems creates challenges in workforce readiness. Many industrial facilities report difficulties finding personnel with adequate skills to properly install, configure, and maintain advanced transducer systems. This skills gap becomes particularly acute in regions experiencing rapid industrial growth, where experienced technical talent remains scarce. Manufacturers face the dual challenge of simplifying device interfaces for broader usability while maintaining advanced capabilities that differentiate their products. Comprehensive training programs and enhanced documentation have become essential components of product offerings to address this persistent market challenge.

IP TRANSDUCER MARKET TRENDS

Industrial Automation and Digital Transformation Driving Market Expansion

The increasing adoption of Industry 4.0 technologies across manufacturing and process industries is significantly boosting the demand for IP transducers globally. These devices play a critical role in industrial automation by converting electrical current signals into pneumatic outputs, which are essential for precise control in systems such as valves and actuators. The rise of smart factories has accelerated deployment, with the oil & gas sector expected to account for over 28% of global transducer demand by 2032. Furthermore, the integration of IIoT (Industrial Internet of Things) solutions enables real-time monitoring, pushing manufacturers toward high-accuracy transducer solutions with digital interfaces.

Other Trends

Shift Toward Digital Input Transducers

While traditional analog input transducers still dominate the market with approximately 62% revenue share in 2024, digital input variants are experiencing rapid adoption due to their compatibility with modern control systems. These devices offer superior noise immunity, simplified calibration, and direct integration with programmable logic controllers (PLCs). The segment is projected to grow at over 8.3% CAGR through 2032, particularly in industries like aerospace where precision and reliability are non-negotiable.

Emerging Markets and Infrastructure Investments

The Asia-Pacific region is witnessing robust growth in IP transducer demand, primarily fueled by China’s industrial expansion and infrastructure projects. With increasing investments in petrochemical plants and water treatment facilities, the regional market is anticipated to capture 34% of global sales by 2028. Additionally, government initiatives promoting domestic manufacturing—such as India’s “Make in India” campaign—are encouraging local transducer production, though high-performance devices still rely on imports from key players like SMC Corporation and Azbil. This dual dynamic creates both competition and collaboration opportunities within the supply chain.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovations and Market Expansion Drive Competition in the IP Transducer Market

The global IP transducer market exhibits a moderately consolidated competitive landscape, dominated by established industrial automation giants alongside specialized manufacturers. ABB and Siemens collectively hold substantial market share, leveraging their extensive product portfolios and established distribution networks across critical regions including North America, Europe, and Asia-Pacific. These corporations continue to strengthen their positions through continuous R&D investment, with ABB reporting a 7.2% year-over-year increase in industrial automation R&D spending in its 2023 annual report.

Emerson Electric (through its Fisher and TopWorx brands) maintains a particularly strong position in the oil & gas segment, where IP transducers are extensively used for process control applications. Recent supply chain optimizations have enabled Emerson to improve delivery times by 18% in key markets, according to their latest quarterly earnings call. Meanwhile, Yokogawa Electric has been gaining traction through its focus on high-precision digital input transducers, capturing significant market share in the pharma and biotechnology sectors.

Smaller but technologically agile players like Dwyer Instruments and Proportion-Air are carving out specialized niches through innovations in miniaturization and IoT integration. Dwyer’s recent launch of its Series 600 smart transducer with Bluetooth connectivity exemplifies this trend, with preliminary reports indicating a 22% sales increase in the industrial HVAC segment.

The market also sees active participation from regional specialists, with Azbil Corporation (formerly Yamatake) dominating the Japanese market and SMC Corporation maintaining strong positions across Southeast Asian manufacturing hubs. These companies benefit from localized supply chains and tailored solutions for regional industry requirements.

List of Key IP Transducer Companies Profiled

- ABB Ltd. (Switzerland)

- Emerson Electric Co. (Fisher Controls, TopWorx) (U.S.)

- Siemens AG (Germany)

- Fairchild (Rotork Instruments) (U.K.)

- Marsh Bellofram (Bellofram PCD, TPC) (U.S.)

- Foxboro (Schneider Electric) (France)

- SMC Corporation (Japan)

- Yokogawa Electric Corporation (Japan)

- Azbil Corporation (Japan)

- Dwyer Instruments (U.S.)

- Proportion-Air (U.S.)

Segment Analysis:

By Type

Analog Input Segment Dominates Due to Widespread Industrial Automation Requirements

The market is segmented based on type into:

- Analog Input

- Subtypes: Current-to-pressure (4-20mA), Voltage-to-pressure (0-10V), and others

- Digital Input

- Subtypes: Fieldbus, HART, and others

- Smart Transducers

- Others

By Application

Oil and Gas Segment Leads Due to Critical Pressure Control Needs in Refineries

The market is segmented based on application into:

- Oil and Gas

- Chemical Processing

- Power Generation

- Water and Wastewater Treatment

- Others

By End User

Process Industries Hold Major Share Owing to Continuous Monitoring Needs

The market is segmented based on end user into:

- Process Industries

- Subtypes: Refineries, Chemical Plants, Pharmaceuticals

- Discrete Manufacturing

- Infrastructure

- Others

Regional Analysis: IP Transducer Market

Asia-Pacific

The Asia-Pacific region dominates the global IP transducer market, accounting for the highest revenue share, primarily driven by rapid industrialization in China, India, and Southeast Asia. Major manufacturing hubs and expansive process industries in these countries heavily rely on automation, creating consistent demand for IP transducers in control systems. China leads owing to its robust electronics and industrial automation sectors, with government initiatives like “Made in China 2025” accelerating adoption. While analog input transducers remain popular for legacy systems, digital input variants are gaining traction as smart factory initiatives expand. However, price sensitivity among small and medium enterprises slows the transition to advanced models despite the region’s high-volume consumption.

North America

North America represents a technologically advanced market, where IP transducers are widely deployed in oil & gas, aerospace, and precision manufacturing. The U.S. holds the largest share, with stringent industry standards pushing manufacturers toward high-accuracy, durable transducers. Recent investments in Industry 4.0 and IoT-integrated systems have spurred demand for digital IP transducers with diagnostic capabilities. Key players like Emerson and Dwyer Instruments focus on innovations such as corrosion-resistant models for harsh environments. However, market saturation in traditional industries and the shift toward wireless solutions pose challenges for conventional transducer suppliers in the region.

Europe

Europe’s mature industrial sector sustains steady demand for IP transducers, particularly in Germany, France, and the U.K., where process automation is integral to manufacturing competitiveness. The region favors energy-efficient and compact transducer designs to comply with EU sustainability directives. Siemens and ABB lead innovation, with digital transducers increasingly adopted in pharmaceutical and food processing applications requiring precise hygienic control. While Western Europe maintains stable growth, Eastern European markets show potential as automotive and chemical industries expand. Nonetheless, high production costs and competition from Asian manufacturers impact local supplier margins.

Middle East & Africa

The MEA region exhibits growing but uneven demand, concentrated in Gulf Cooperation Council (GCC) countries where oil, gas, and power generation sectors drive transducer applications. Saudi Arabia and the UAE lead deployments in refineries and water treatment plants, prioritizing explosion-proof and high-temperature-resistant models. Local players face challenges due to reliance on imports, though joint ventures with global brands are increasing. In Africa, mining and infrastructure projects create niche opportunities, but political instability and underdeveloped supply chains limit market penetration beyond South Africa and Egypt.

South America

South America’s market remains nascent, with Brazil and Argentina accounting for most IP transducer demand, primarily in mining and agricultural processing. Economic volatility and underinvestment in industrial automation restrict growth, though deferred maintenance in aging facilities generates replacement demand. Local manufacturers compete on price but struggle against multinational brands’ technological edge. Government initiatives to upgrade food processing and energy infrastructure, such as Brazil’s Novo Mercado Automático program, may stimulate future transducer adoption if funding stabilizes.

Report Scope

This market research report provides a comprehensive analysis of the global and regional IP Transducer markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global IP Transducer market was valued at USD 1,427 million in 2024 and is projected to reach USD 2,243 million by 2032, growing at a CAGR of 6.8%.

- Segmentation Analysis: Detailed breakdown by product type (Analog Input, Digital Input), application (Oil & Gas, Mining, Medical, Aerospace, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis of key markets like the U.S., China, Germany, and Japan.

- Competitive Landscape: Profiles of leading market participants including ABB, Emerson, Siemens, Foxboro (Schneider Electric), and Yokogawa Electric Corporation, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging trends in industrial automation, smart manufacturing integration, and advancements in transducer technology.

- Market Drivers & Restraints: Analysis of factors driving growth such as industrial automation adoption and process control demands, along with challenges like supply chain constraints and regulatory compliance.

- Stakeholder Analysis: Strategic insights for manufacturers, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs both primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global IP Transducer Market?

-> IP Transducer market was valued at 1427 million in 2024 and is projected to reach US$ 2243 million by 2032, at a CAGR of 6.8% during the forecast period.

Which key companies operate in Global IP Transducer Market?

-> Key players include ABB, Emerson (Fisher, TopWorx), Siemens, Foxboro (Schneider Electric), Yokogawa Electric Corporation, and SMC Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for process control systems, and expansion in oil & gas and chemical industries.

Which region dominates the market?

-> Asia-Pacific shows the highest growth potential, while North America and Europe remain significant markets due to established industrial sectors.

What are the emerging trends?

-> Emerging trends include integration with IIoT systems, development of smart transducers, and increasing demand for energy-efficient solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...