Market Insights

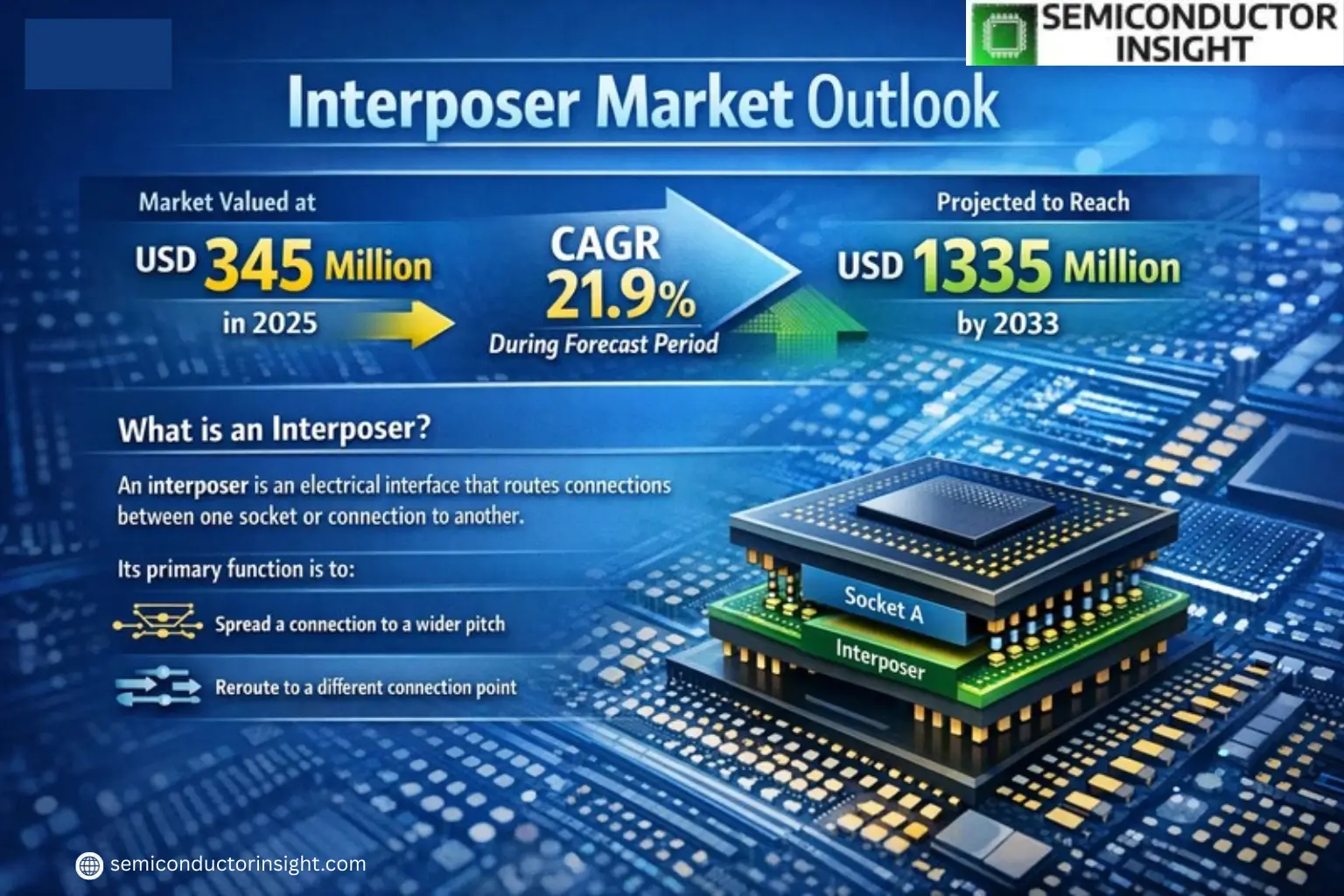

Global Interposer Market was valued at USD 345 million in 2025 and is projected to reach USD 1335 million by 2033, exhibiting a CAGR of 21.9% during the forecast period.

An interposer is an electrical interface that routes connections between one socket or connection to another. Its primary function is to spread a connection to a wider pitch or reroute it to a different connection point. These components are critical in advanced semiconductor packaging, enabling high-density integration and improved performance in applications such as ASICs, FPGAs, and CPUs/GPUs.

The market growth is driven by increasing demand for miniaturized electronic devices, advancements in semiconductor packaging technologies, and the rising adoption of high-performance computing (HPC) solutions. The 2.5D interposer segment dominates the market with a share of approximately 70%, owing to its widespread use in complex chip designs. Key players like TSMC, Murata, and Xilinx collectively hold around 60% of the global market share, leveraging their expertise in semiconductor manufacturing and packaging innovations.

MARKET DRIVERS

Growing Demand for High-Performance Computing

Interposer Market is experiencing significant growth due to increasing demand for high-performance computing solutions. Advanced packaging technologies, including 2.5D and 3D interposers, enable higher bandwidth and lower power consumption in data centers and AI applications. Semiconductor companies are heavily investing in interposer-based designs to meet the computational needs of modern workloads.

Rise of AI and Machine Learning Applications

The proliferation of AI and machine learning has accelerated adoption of interposer technology, as it enhances chip performance for neural network processing. Leading tech firms are increasingly adopting interposers to achieve faster data transfer between memory and processors in AI chipsets.

Additionally, the automotive sector’s shift towards advanced driver-assistance systems (ADAS) and autonomous vehicles is creating new opportunities for interposer applications in high-reliability electronic systems.

MARKET CHALLENGES

High Manufacturing Complexity and Costs

Interposer fabrication involves complex processes like through-silicon via (TSV) formation and fine-pitch bonding, leading to substantial production costs. Only a handful of foundries currently possess the capability to manufacture high-quality interposers at commercial scales.

Other Challenges

Thermal Management Issues

As interposer-based packages become more dense, managing heat dissipation becomes increasingly difficult, potentially affecting device reliability and longevity in high-temperature environments.

MARKET RESTRAINTS

Limited Adoption in Cost-Sensitive Applications

While interposer technology offers performance benefits, its high cost per unit restricts adoption in price-sensitive consumer electronics segments. Many mid-range device manufacturers continue to prefer traditional packaging solutions due to budget constraints.

MARKET OPPORTUNITIES

Emerging Applications in 5G and IoT Devices

Interposer Market stands to benefit from the global rollout of 5G networks and expansion of IoT ecosystems. System-in-Package (SiP) solutions utilizing interposers are becoming crucial for achieving the miniaturization and performance requirements of next-generation wireless devices.

Global Interposer Market Trends

Rapid Market Growth Driven by Advanced Packaging Needs

Global Interposer Market, valued at USD 345 million in 2025, is projected to reach USD 1,335 million by 2033, growing at a robust CAGR of 21.9%. This exponential growth is fueled by increasing demand for high-performance computing and advanced semiconductor packaging solutions. Interposers play a critical role in modern electronics by enabling efficient routing between different connection points, particularly in complex chip architectures.

Other Trends

Dominance of 2.5D Interposer Technology

2.5D interposers currently dominate the market with a 70% share, as they provide optimal balance between performance and cost for applications requiring high-density interconnects. This technology is particularly prevalent in ASIC/FPGA applications, which represent a significant portion of the Interposer Market demand.

Regional Market Concentration and Competitive Landscape

North America leads the global Interposer Market with a 40% share, followed closely by Taiwan and Japan which collectively account for 45% of the market. The competitive landscape is concentrated, with the top five players – including Murata, Tezzaron, and TSMC – holding approximately 60% of the market share. These established players are investing heavily in R&D to maintain technological leadership in interposer manufacturing.

Emerging Applications Fueling Demand

Beyond traditional applications in ASIC/FPGA and CPU/GPU markets, emerging uses in MEMS 3D capping, RF devices, and high-power LED applications are creating new growth opportunities. The Logic SoC segment in particular shows strong potential for interposer adoption as chip designs become more complex and performance requirements intensify.

COMPETITIVE LANDSCAPE

Key Industry Players

Consolidated Market Dominated by Top 5 Players Holding 60% Share

Global Interposer Market remains highly concentrated, with Murata, Tezzaron, Xilinx, AGC Electronics, and TSMC collectively controlling approximately 60% of market share. Murata leads through its advanced 2.5D interposer solutions for RF devices, while TSMC dominates semiconductor packaging applications through its CoWoS (Chip on Wafer on Substrate) technology. Xilinx maintains strong positioning through FPGA-focused interposer designs optimized for high-speed data transfer applications.

Niche players like Plan Optik AG specialize in glass interposers for MEMS applications, while UMC and Amkor provide foundry services for 3D IC packaging. Emerging participants such as IMT and ALLVIA are gaining traction through innovative through-silicon via (TSV) technologies for advanced packaging solutions. The market shows increasing competition in passive interposer segments as more players enter the high-growth automotive and AI processor markets.

List of Key Interposer Companies Profiled

- Murata

- Tezzaron Semiconductor

- Xilinx (AMD)

- AGC Electronics

- TSMC

- UMC

- Plan Optik AG

- Amkor Technology

- IMT

- ALLVIA, Inc

- GlobalFoundries

- ASE Group

- STATS ChipPAC

- SK Hynix

- Powertech Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

2.5D Interposer dominates the market due to:

|

| By Application |

|

ASIC/FPGA applications lead the market because:

|

| By End User |

|

Semiconductor Manufacturers represent the largest end-user segment due to:

|

| By Material Type |

|

Silicon Interposers maintain market leadership because:

|

| By Technology |

|

Through-Silicon Via (TSV) technology dominates due to:

|

Regional Analysis: Global Interposer Market

Asia-Pacific leads in silicon interposer adoption due to superior electrical performance requirements in high-end computing applications. TSMC’s CoWoS technology and Samsung’s interposer solutions demonstrate regional technical leadership in this segment.

The booming high-performance computing and AI sectors in China, Japan, and South Korea create sustained demand for advanced interposer solutions. Increasing adoption of chiplet architectures further drives the need for sophisticated interposer technologies.

Regional players benefit from vertically integrated semiconductor ecosystems, reducing time-to-market for interposer-based packages. Close collaboration between foundries, OSATs, and end-users enables rapid technology adoption and customization.

Beyond traditional computing, Asia-Pacific sees growing interposer adoption in automotive electronics, 5G infrastructure, and IoT devices. Japan leads in organic interposer development for cost-sensitive applications in consumer electronics.

North America

North America remains a key innovation center for interposer technologies, particularly in R&D and high-end applications. The region benefits from strong presence of fabless semiconductor companies and system designers requiring advanced packaging solutions. Silicon Valley-based companies drive demand for high-performance interposers used in AI accelerators and data center applications. The U.S. government’s focus on reshoring semiconductor manufacturing may boost local interposer production capabilities in coming years. Collaborative R&D between academia and industry continues to push the boundaries of interposer technology, particularly in areas like photonic interposers.

Europe

Europe maintains a specialized position in the Interposer Market, focusing on niche applications in automotive, industrial, and aerospace sectors. The region demonstrates strength in glass interposer technologies, supported by research institutions and specialized manufacturers. European semiconductor companies emphasize reliability and ruggedness in interposer designs suitable for harsh environments. While production volumes lag behind Asia-Pacific, European players compete through high-value, customized solutions. Recent initiatives under the European Chips Act aim to strengthen the regional semiconductor ecosystem, potentially boosting interposer innovation and manufacturing capabilities.

Middle East & Africa

The Middle East and Africa region shows emerging potential in the Interposer Market, primarily driven by increasing electronics manufacturing in countries like Israel and South Africa. Growing investments in data centers and telecom infrastructure create localized demand for interposer-based solutions. The region benefits from strategic partnerships with global semiconductor players establishing R&D centers. While current market size remains small compared to other regions, long-term growth prospects appear promising as regional technology ecosystems develop and local foundry capabilities expand.

South America

South America represents the smallest but gradually developing market for interposer technologies. Brazil leads regional adoption with its growing electronics manufacturing sector and increasing data center investments. The region primarily serves as an importer of interposer-based components rather than a manufacturing hub. However, partnerships with global semiconductor companies and technology transfer initiatives show potential for gradual capacity building in advanced packaging technologies over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Interposer Market, covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Interposer Market?

-> Interposer Market was valued at USD 345 million in 2025 and is projected to reach USD 1335 million by 2033, exhibiting a CAGR of 21.9% during the forecast period.

What is the growth rate of the Interposer Market?

-> The market is projected to grow at a CAGR of 21.9% during the forecast period (2025-2033).

Which key companies operate in the Interposer Market?

-> Key players include Murata, Tezzaron, Xilinx, AGC Electronics, TSMC, UMC, Plan Optik AG, Amkor, IMT, and ALLVIA, Inc, among others. Global top five players hold about 60% market share.

Which region dominates the Interposer Market?

-> North America is the largest market with a 40% share, followed by Taiwan, China, and Japan with a combined 45% share.

What are the major product segments in the Interposer Market?

-> The largest segment is 2.5D Interposer with a 70% market share, followed by 2D Interposer and 3D Interposer.

What are the key applications of Interposer?

-> The largest application is ASIC/FPGA, followed by CPU/GPU, MEMS 3D Capping Interposer, RF Devices, Logic SoC, CIS, and High Power LED.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...