MARKET INSIGHTS

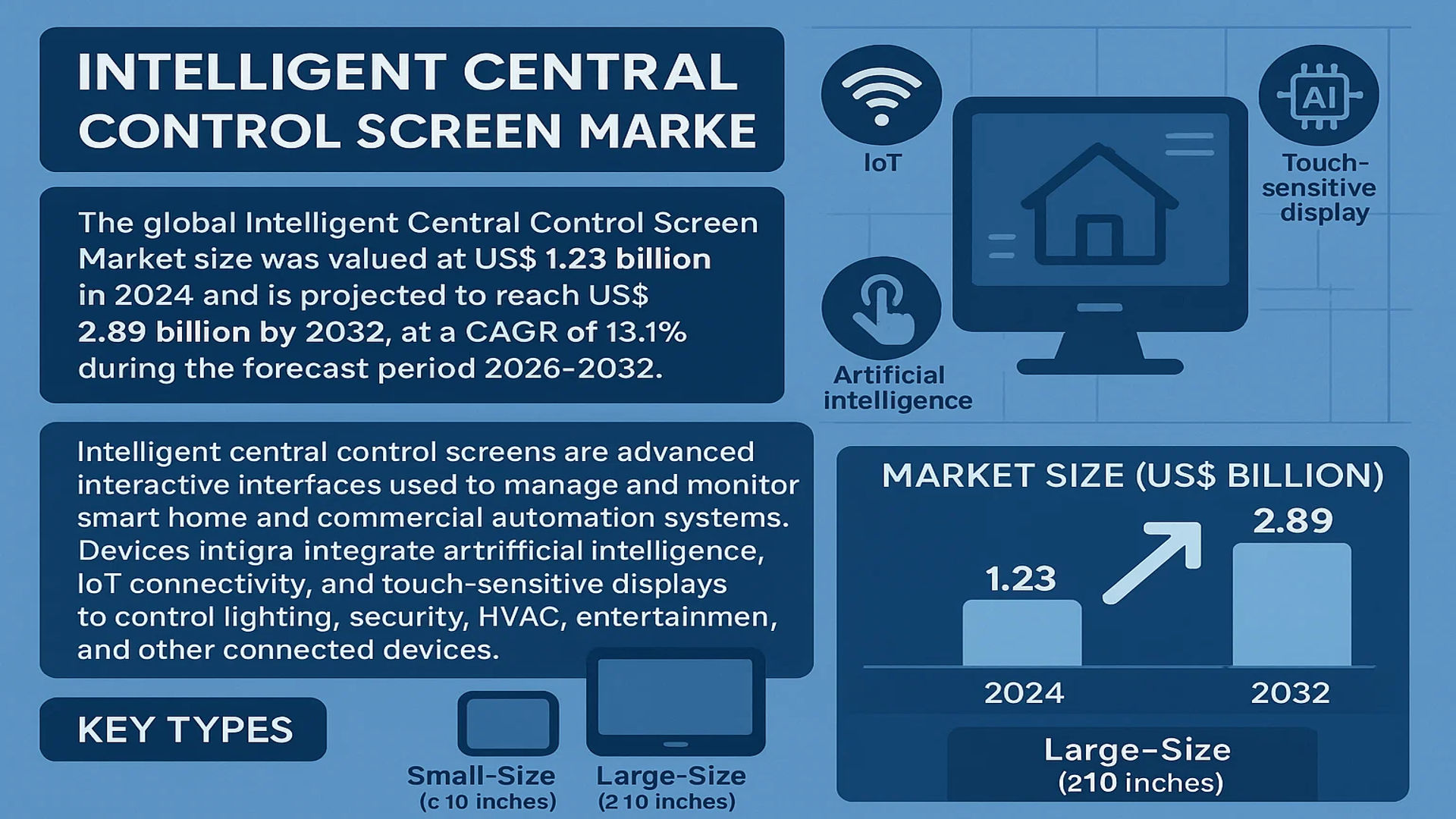

The global Intelligent Central Control Screen Market size was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 13.1% during the forecast period 2025-2032.

Intelligent central control screens are advanced interactive interfaces used to manage and monitor smart home and commercial automation systems. These devices integrate artificial intelligence, IoT connectivity, and touch-sensitive displays to control lighting, security, HVAC, entertainment, and other connected devices. Key types include small-size (under 10 inches) and large-size (above 10 inches) screens, catering to diverse residential and commercial applications.

The market growth is driven by rising demand for smart home automation, increasing adoption of IoT-enabled devices, and advancements in AI-based voice and gesture recognition technologies. While North America currently leads in market share, Asia-Pacific is witnessing accelerated growth due to rapid urbanization and government smart city initiatives. Major players such as Hisense, HUAWEI, and Xiaomi are expanding their portfolios with energy-efficient and user-friendly solutions, further fueling industry expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Adoption of Smart Home Automation to Accelerate Demand

The global intelligent central control screen market is experiencing strong growth driven by the increasing adoption of smart home automation systems. These centralized control interfaces serve as the brain of connected homes, allowing seamless management of lighting, security, climate, and entertainment through unified dashboards. The market for smart home devices is projected to grow significantly, with connected home technology becoming mainstream across residential and commercial sectors. As consumers seek convenience and energy efficiency, intelligent control screens have emerged as pivotal components in modern automation ecosystems. Recent advancements in voice recognition and AI-powered predictive controls are further enhancing user experience, making these systems indispensable for tech-savvy homeowners.

Commercial Sector Digitization Creating New Growth Avenues

Commercial establishments are increasingly deploying intelligent control screens to optimize building management systems and improve operational efficiency. Hotels, corporate offices, and retail spaces are implementing centralized control solutions to monitor and regulate multiple subsystems including HVAC, lighting, and security from single touchpoints. The hospitality industry in particular has seen significant adoption, with smart room management systems becoming standard in premium hotels worldwide. This trend is supported by growing investments in commercial IoT infrastructure and the need for energy-efficient building operations. As businesses prioritize digital transformation, the demand for sophisticated control interfaces is expected to rise substantially during the forecast period.

Technological Convergence Expanding Market Potential

The integration of intelligent control screens with emerging technologies is creating new opportunities across multiple sectors. Cloud computing enables remote monitoring and control capabilities, while 5G networks facilitate real-time data processing and faster response times. Artificial intelligence algorithms are being incorporated to provide predictive maintenance alerts and personalized automation scenarios. Furthermore, the development of interoperable ecosystems allows these screens to serve as hubs for diverse smart devices from different manufacturers. This technological convergence is driving system sophistication while improving cost-effectiveness through standardized communication protocols.

MARKET RESTRAINTS

High Implementation Costs Impeding Mass Market Adoption

While intelligent central control screens offer significant benefits, their widespread adoption faces challenges due to relatively high implementation costs. The sophisticated technology requires substantial upfront investment in both hardware and software components, making it currently more accessible to premium residential and commercial segments. Installation complexities often demand professional setup and configuration, adding to the total cost of ownership. This pricing barrier limits market penetration in cost-sensitive regions and budget-conscious consumer segments. While prices are gradually decreasing as technology matures, the premium positioning of these systems continues to restrict mass market appeal.

Interoperability Issues Creating Integration Challenges

The lack of universal standards in smart home ecosystems presents significant hurdles for intelligent control screen manufacturers. Different brands often utilize proprietary protocols, forcing consumers to choose between limited device compatibility or complex workaround solutions. This fragmentation in the IoT landscape leads to integration challenges that can diminish user experience. While industry alliances are working towards common communication standards, the current market reality requires control screen providers to support multiple protocols, increasing development costs and potentially delaying new feature rollouts.

Privacy and Security Concerns Affecting Consumer Confidence

As central control screens collect and process vast amounts of personal and operational data, cybersecurity risks have emerged as a significant market restraint. High-profile incidents of smart home vulnerabilities have made consumers cautious about adopting centralized control systems. The need for robust encryption, regular firmware updates, and secure cloud infrastructure adds development overhead for manufacturers. Regulatory compliance with evolving data protection laws also increases operational complexity. These security considerations must be adequately addressed to maintain consumer trust and ensure sustainable market growth.

MARKET OPPORTUNITIES

Emerging Markets Present Untapped Growth Potential

Developing economies represent significant opportunities as rising disposable incomes and urbanization drive demand for smart home technologies. Countries with growing middle-class populations are increasingly investing in home automation solutions, creating new markets for intelligent control systems. Government initiatives promoting smart city development and energy-efficient infrastructure further support this trend. Manufacturers can capitalize on this opportunity by developing cost-optimized products tailored to regional preferences and connectivity landscapes.

Integration with Renewable Energy Systems

The global shift towards sustainable energy solutions opens new possibilities for intelligent control screen applications. These systems are increasingly being integrated with solar power management and energy storage solutions, allowing users to monitor and optimize power consumption effectively. As renewable energy adoption grows, demand for comprehensive energy management interfaces will rise, presenting manufacturers with opportunities to develop specialized control solutions for this emerging market segment.

Healthcare and Assisted Living Applications

The healthcare sector offers promising growth avenues as intelligent control screens find applications in assisted living environments. These systems can integrate medical alert features, medication reminders, and health monitoring capabilities while maintaining the familiar home automation functions. With aging populations in developed nations and growing focus on independent living solutions, healthcare-oriented control interfaces represent a specialized but lucrative market opportunity.

MARKET CHALLENGES

Short Product Lifecycles Requiring Continuous Innovation

The intelligent control screen market faces intense competition and rapid technological obsolescence. Manufacturers must contend with short product lifecycles as new features and capabilities emerge continuously. This environment demands significant R&D investment to maintain competitiveness while managing profitability. Consumer expectations for regular software updates and new functionalities further strain development resources, particularly for smaller market players.

Supply Chain Vulnerabilities Impacting Production

The global semiconductor shortage and other supply chain disruptions have affected intelligent control screen manufacturers, leading to production delays and increased component costs. The industry’s reliance on specialized displays, processors, and connectivity modules makes it particularly susceptible to supply chain fluctuations. Developing resilient sourcing strategies and alternative component options has become critical for stable operations and consistent product availability.

User Experience and Interface Design Complexities

As control screens incorporate more features and functionalities, maintaining intuitive user interfaces becomes increasingly challenging. The balance between offering comprehensive control and simplicity requires careful design consideration. Poor user experience can lead to reduced satisfaction and slower adoption rates. Manufacturers must invest in human-centered design principles while accommodating the diverse needs of residential and commercial users across different demographic groups.

INTELLIGENT CENTRAL CONTROL SCREEN MARKET TRENDS

IoT Integration Driving Smart Home and Commercial Automation

The increasing adoption of Internet of Things (IoT) technology is significantly shaping the intelligent central control screen market. These centralized interfaces, which consolidate control for lighting, security, HVAC, and entertainment systems, are evolving beyond standalone devices into integrated smart ecosystems. Recent market trends show that over 85% of high-end residential projects now incorporate central control panels as part of their core automation infrastructure. The ability to manage multiple subsystems through a single touchpoint has become particularly valuable in commercial applications, where facilities management efficiency gains can reach up to 30% according to industry benchmarks. Importantly, the standard 7-inch control panel still dominates with 42% market share, while larger 10-inch and 12-inch displays are showing the fastest growth rates at 18% annually.

Other Trends

Voice Control and AI-assisted Interfaces

The integration of advanced voice recognition and artificial intelligence is transforming user interaction paradigms in the intelligent central control screen sector. Manufacturers are increasingly incorporating natural language processing capabilities, allowing users to manage their environments through conversational commands rather than traditional touch inputs. This shift has been accelerated by consumer preference – recent usage data indicates that 63% of smart home control operations now initiate through voice rather than touchscreen interaction. AI-driven predictive controls that learn user behaviors and adjust settings automatically are proving particularly popular in luxury residential markets, where they command a 35% price premium over standard control units.

Regional Growth Patterns and Competitive Landscape

Geographically, the Asia-Pacific region represents the most dynamic market for intelligent central control screens, projected to account for over 47% of global sales by 2026. This growth is being fueled by massive smart city initiatives across China and rapid urbanization in Southeast Asia. Notably, Chinese manufacturers have captured nearly 60% of the residential segment through aggressive pricing strategies and localization of features. Elsewhere, North American adoption is being driven primarily by commercial retrofits and high-end residential construction, where integration with existing security systems has become a key purchase consideration. The competitive landscape remains fragmented, with the top five manufacturers holding approximately 28% collective market share, suggesting significant room for consolidation as the industry matures.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Brands Drive Market Expansion Through Innovation and Strategic Partnerships

The global Intelligent Central Control Screen market features a dynamic competitive landscape where established electronics giants and emerging smart home specialists vie for dominance. Hisense and HUAWEI currently lead the sector, collectively holding over 25% market share in 2024, owing to their strong R&D capabilities and vertically integrated supply chains. These industry frontrunners are particularly dominant in the Asia-Pacific region, where smart home adoption rates are growing at 18% annually.

Chinese manufacturers Xiaomi and Haier have made significant inroads through competitive pricing strategies, capturing nearly 15% of the global market combined. Their success stems from affordable yet feature-rich product lines tailored for price-sensitive consumers, particularly in developing economies. These companies continue to expand their IoT ecosystems, seamlessly integrating central control screens with other smart devices.

Among Western players, ADT Control maintains a strong position in the North American market through strategic partnerships with security system providers. The company’s focus on interoperability with existing home automation systems gives it a distinctive competitive edge. Similarly, ORVIBO has gained traction in Europe by specializing in energy management features, appealing to sustainability-conscious consumers.

Recent market developments include Midea‘s launch of their AI-powered central control system featuring voice recognition in 12 languages, while Hangzhou Lifesmart Technology partnered with multiple real estate developers to pre-install control screens in smart buildings. Such differentiation strategies are becoming increasingly crucial as the market matures.

List of Key Intelligent Central Control Screen Manufacturers

- Hisense (China)

- ADT Control (U.S.)

- HUAWEI (China)

- Midea (China)

- Haier (China)

- Xiaomi (China)

- ORVIBO (China)

- Hangzhou Lifesmart Technology (China)

- Fujian Aurine Technology (China)

- Hangzhou Ezviz Networ (China)

Segment Analysis:

By Type

Small-Size Displays Gain Traction Due to Increasing Smart Home Integration and Space Efficiency

The market is segmented based on type into:

- Small Size

- Subtypes: Touchscreen, Non-touchscreen

- Large Size

- Subtypes: Wall-mounted, Standalone

By Application

Household Segment Dominates Owing to Rising Adoption of Smart Home Ecosystems

The market is segmented based on application into:

- Household

- Commercial

By Connectivity

Wi-Fi Enabled Devices Lead the Market with Seamless IoT Integration Capabilities

The market is segmented based on connectivity into:

- Wi-Fi

- Bluetooth

- Wired

- Hybrid

By End User

Residential Users Drive Demand Through Smart Home Automation Investments

The market is segmented based on end user into:

- Residential

- Enterprise

- Government

Regional Analysis: Intelligent Central Control Screen Market

North America

The North American Intelligent Central Control Screen market is experiencing robust growth, driven by the increasing adoption of smart home automation and commercial building management systems. The U.S. dominates this region, with significant investments in connected infrastructure and IoT-enabled solutions propelling demand. However, stringent data security regulations, such as the California Consumer Privacy Act (CCPA), create compliance challenges for manufacturers. The market also benefits from strong consumer preference for energy-efficient and voice-controlled smart home ecosystems. Notably, leading technology firms are innovating with AI-powered interfaces for commercial applications, particularly in retail and hospitality sectors.

Europe

Europe remains a key market for Intelligent Central Control Screens, with Germany and the U.K. accounting for the largest shares. Strict EU data protection laws (GDPR) and emphasis on sustainable technologies influence product development cycles, favoring solutions with low energy consumption. Residential adoption rates vary significantly between Western and Eastern Europe due to economic disparities. The commercial sector, especially in smart office applications, is showing accelerated growth, though concerns about interoperability between different smart device ecosystems continue to challenge widespread implementation. Manufacturers are responding with more standardized, cross-platform compatible solutions.

Asia-Pacific

Asia-Pacific represents the fastest-growing market, with China commanding over 40% of regional demand according to recent industry estimates. Rapid urbanization, government smart city initiatives, and increasing disposable income drive adoption across both household and commercial segments. While Japan and South Korea favor high-end, feature-rich systems, Southeast Asian markets demonstrate strong price sensitivity, creating opportunities for budget-conscious solutions. The competitive landscape is intense, with domestic brands leveraging localized ecosystems to outperform global players in several markets. However, concerns about data privacy and security standards continue to restrain growth potential in some developing nations.

South America

The South American market remains in a growth phase, with Brazil and Argentina showing the most promising developments. Economic volatility affects consumer purchasing power, limiting market penetration compared to other regions. Commercial applications, particularly in hospitality and retail, are driving adoption as businesses invest in automation to improve operational efficiency. Infrastructure limitations, including inconsistent internet connectivity in some areas, create barriers for full functionality. Manufacturers are adapting by offering more offline capabilities and simplified user interfaces to address these market-specific challenges.

Middle East & Africa

This emerging market demonstrates uneven growth patterns, with the UAE and Saudi Arabia leading in adoption rates due to ambitious smart city projects and high disposable incomes. Luxury residential developments and five-star hospitality establishments represent key application areas. However, the broader regional market faces challenges including limited technical awareness and infrastructure gaps in some countries. Recent economic diversification efforts in oil-dependent nations are creating new opportunities, with governments increasingly prioritizing technology-driven urban development. While the market is currently niche compared to other regions, long-term growth potential is significant as digital transformation initiatives gain momentum.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Intelligent Central Control Screen markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Intelligent Central Control Screen market was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 2.89 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Small Size, Large Size), application (Household, Commercial), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. market estimated at USD 350 million in 2024 and China projected to reach USD 820 million by 2032.

- Competitive Landscape: Profiles of leading market participants including Hisense, HUAWEI, Xiaomi, Midea, and Haier, with the global top five players holding approximately 45% market share in 2024.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, voice recognition capabilities, and evolving smart home ecosystem standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth including smart home adoption and urbanization, along with challenges such as high implementation costs and data security concerns.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Intelligent Central Control Screen Market?

-> Intelligent Central Control Screen Market size was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 13.1% during the forecast period 2025-2032.

Which key companies operate in Global Intelligent Central Control Screen Market?

-> Key players include Hisense, HUAWEI, Xiaomi, Midea, Haier, ADT Control, ORVIBO, and Hangzhou Lifesmart Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing smart home adoption, technological advancements in IoT, and rising demand for centralized home automation solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a technologically advanced market with high adoption rates.

What are the emerging trends?

-> Emerging trends include integration with voice assistants, AI-powered predictive controls, and multi-ecosystem compatibility.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...