Integrated AMOLED Display Driver Chip Market Insights

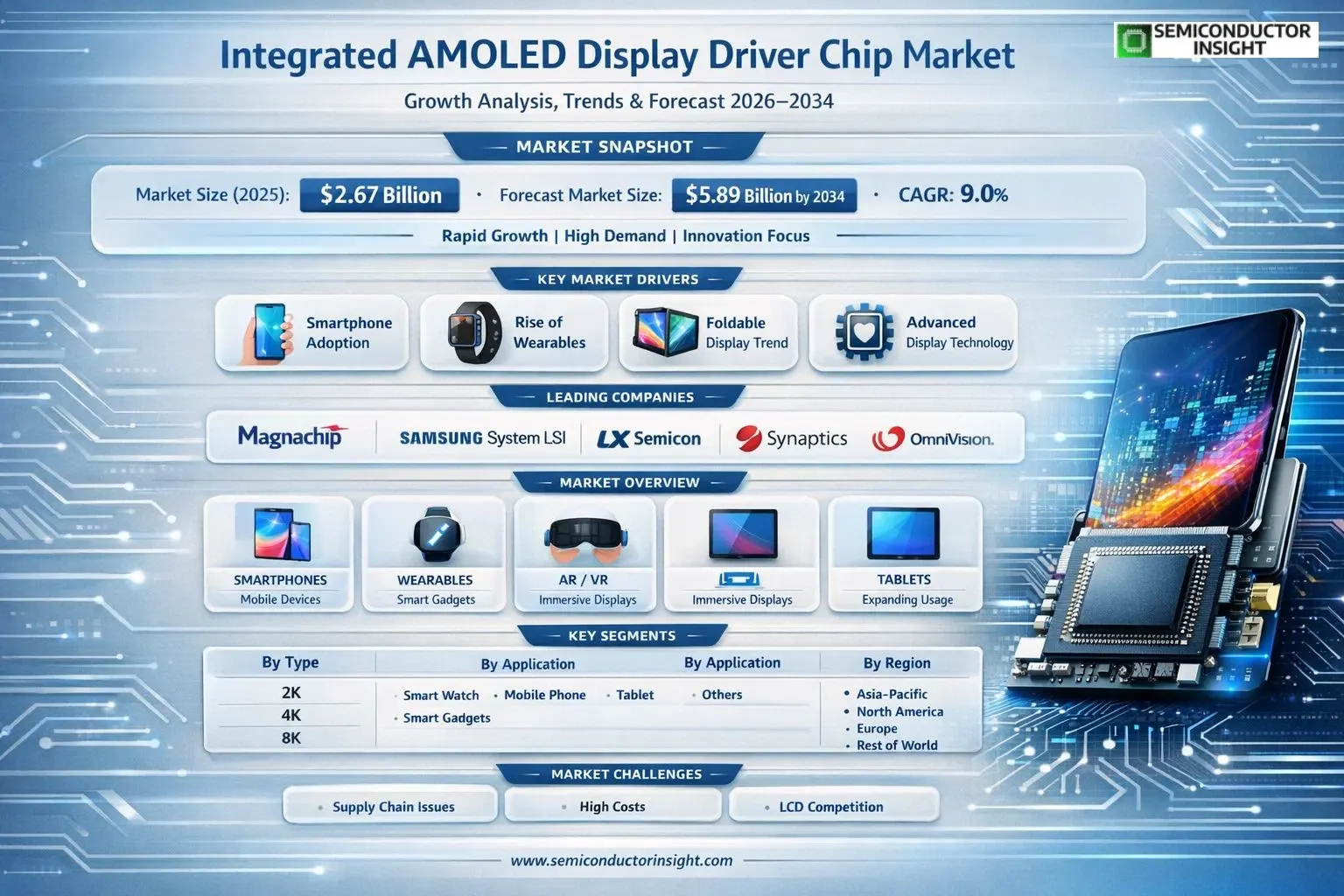

Global Integrated AMOLED Display Driver Chip market size was valued at USD 2.67 billion in 2025. The market is projected to grow from USD 2.95 billion in 2026 to USD 5.89 billion by 2034, exhibiting a CAGR of 9.0% during the forecast period.

The integrated AMOLED display driver chip is an integrated circuit designed specifically for AMOLED displays, which is used to control and drive each pixel on the display. It integrates multiple functional modules into one chip, optimizes display performance, and simplifies system design.

The market is experiencing rapid growth due to several factors, including surging demand for vibrant, energy-efficient AMOLED screens in smartphones and wearables, the rise of foldable devices, and advancements in high-resolution display technologies. Furthermore, expanding applications in tablets and emerging AR/VR sectors are driving expansion. Key players continue to innovate; for instance, Himax Technologies enhanced its AMOLED driver solutions for smartwatches in 2024. Magnachip Semiconductor, Samsung System LSI, LX Semicon, Synaptics, OmniVision, Raydium Semiconductor, Himax Technologies, Novatek Microelectronics, and Fitipower Integrated are prominent companies with robust portfolios in this space.

MARKET DRIVERS

Rising Demand for High-Resolution Displays

Integrated AMOLED Display Driver Chip Market is propelled by the surging adoption of premium smartphones and tablets featuring vibrant, high-contrast AMOLED screens. With global smartphone shipments exceeding 1.2 billion units annually, manufacturers prioritize integrated chips that enhance power efficiency and support resolutions up to 4K, reducing bezels and enabling immersive viewing experiences.

Expansion in Wearables and Automotive

Growth in smartwatches and fitness trackers, projected to reach 500 million units by 2025, drives demand for compact, low-power integrated AMOLED driver chips. In automotive displays, the shift toward advanced driver-assistance systems (ADAS) integrates larger AMOLED panels, necessitating chips with superior refresh rates and touch integration for enhanced user interfaces.

➤ Key players like Samsung and Synaptics report 15% year-over-year revenue growth from AMOLED driver ICs, underscoring market momentum.

Foldable and flexible display innovations further accelerate adoption, as integrated chips handle dynamic pixel driving, boosting the overall Integrated AMOLED Display Driver Chip Market at a CAGR of approximately 11% through 2030.

MARKET CHALLENGES

Supply Chain Vulnerabilities

Integrated AMOLED Display Driver Chip Market faces disruptions from semiconductor shortages, with production delays impacting 20% of OEM orders in recent years. Reliance on Asian foundries exposes the sector to geopolitical tensions and raw material fluctuations, complicating timely delivery for high-volume consumer electronics.

Other Challenges

High Development Costs

R&D expenses for next-gen chips exceed $500 million per design cycle, straining smaller fabless firms and favoring incumbents with scale advantages. Yield rates hover around 85% for advanced nodes, increasing per-unit costs and hindering market penetration in mid-range devices.

Competition from LCD alternatives persists in cost-sensitive segments, where AMOLED integration premiums deter mass adoption despite superior image quality.

MARKET RESTRAINTS

Manufacturing Complexity and Costs

Elevated fabrication costs for nanoscale processes limit scalability in Integrated AMOLED Display Driver Chip Market. Advanced nodes below 8nm demand specialized equipment, pushing chip prices 30-40% higher than legacy silicon, which restricts deployment in budget devices comprising 60% of shipments.

Power consumption remains a bottleneck for always-on displays, with current integrations struggling to achieve sub-1mW metrics without compromising brightness uniformity across large panels.

Intellectual property barriers and patent thickets slow innovation, as leading vendors control core algorithms for pixel compensation, deterring new entrants and consolidating market share among top suppliers.

MARKET OPPORTUNITIES

Emerging Applications in AR/VR and IoT

Integrated AMOLED Display Driver Chip Market holds promise in augmented reality headsets, where micro-AMOLED panels require high-PPI drivers supporting 120Hz refresh for seamless experiences, with shipments forecasted to grow 25% annually.

IoT devices like smart home hubs and medical wearables offer untapped potential, as low-power integrated chips enable always-on functionality with extended battery life.

Strategic partnerships for 8K TV panels and automotive HUDs could capture 15% additional market share, leveraging AI-enhanced driving for superior contrast and response times.

Integrated AMOLED Display Driver Chip Market Trends

Shift Towards Higher Resolution Support

Integrated AMOLED Display Driver Chip Market is experiencing a significant shift towards chips capable of supporting advanced resolutions including 2K, 4K, and 8K. These integrated circuits are engineered to precisely control and drive individual pixels in AMOLED displays, incorporating multiple functional modules that optimize performance and streamline system designs. This trend is fueled by escalating consumer expectations for superior visual quality across various devices, prompting manufacturers to prioritize enhanced resolution capabilities in their chip architectures.

Other Trends

Diversification Across Applications

Another notable development in Integrated AMOLED Display Driver Chip Market involves broader adoption in diverse applications such as smartwatches, mobile phones, tablets, and other emerging devices. Mobile phones continue to represent a dominant segment due to the widespread integration of AMOLED panels requiring efficient driver solutions, while smartwatches are seeing rapid uptake for their compact, power-efficient designs. This diversification underscores the chips’ versatility in enhancing display responsiveness and image quality in portable electronics.

Intensified Competition and Regional Dynamics

Competition within Integrated AMOLED Display Driver Chip Market is intensifying among leading manufacturers like Magnachip Semiconductor, Samsung System LSI, LX Semicon, Synaptics, Himax Technologies, Novatek Microelectronics, and others, who collectively hold substantial market influence. These players are focusing on innovations in power management, integration density, and compatibility with next-generation AMOLED panels. Regionally, Asia-Pacific leads, driven by production hubs in China, Japan, and South Korea, where proximity to display panel fabricators accelerates development cycles. North America and Europe are witnessing steady growth through premium device integrations, with ongoing surveys of industry experts highlighting drivers like technological miniaturization and challenges such as supply chain dependencies.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers in Integrated AMOLED Display Driver Chip Market

Integrated AMOLED Display Driver Chip Market is dominated by a handful of established semiconductor firms, with the global top five players holding a substantial revenue share as of 2025. Samsung System LSI emerges as a frontrunner, leveraging its vertical integration within the Samsung ecosystem to supply advanced driver chips optimized for high-resolution AMOLED panels in mobile devices and wearables. Magnachip Semiconductor and LX Semicon follow closely, focusing on power-efficient solutions that support 2K, 4K, and emerging 8K resolutions. This oligopolistic structure fosters intense innovation in integration density and display performance, driven by demand from smartphones, smartwatches, and tablets, where cost reduction and yield improvements are critical competitive edges.

Beyond the leaders, a cadre of niche players contributes specialized expertise, particularly in cost-sensitive applications and regional markets. Companies like Synaptics and OmniVision excel in touch-integrated drivers for premium devices, while Raydium Semiconductor and Himax Technologies target mid-range segments with compact, low-power ICs. Novatek Microelectronics and Fitipower Integrated emphasize high-volume production for Asian OEMs, addressing challenges in supply chain scalability. Emerging firms such as Jadard Technology and Geke Microelectronics are gaining traction through customized solutions for wearables and automotive displays, intensifying competition and spurring advancements in AMOLED driving efficiency amid rising global demand.

List of Key Integrated AMOLED Display Driver Chip Companies Profiled

- Magnachip Semiconductor

- Samsung System LSI

- LX Semicon

- Synaptics

- OmniVision

- Raydium Semiconductor

- New Vision Microelectronics

- Himax Technologies

- Novatek Microelectronics

- Fitipower Integrated

- Jadard Technology

- Geke Microelectronics

- Jichuang North Technology

- Sino Wealth Electronic

- Viewtrix Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

2K leads the segment by offering an ideal equilibrium of resolution and performance tailored for AMOLED displays in mainstream applications.

|

| By Application |

|

Mobile Phone commands the forefront, propelled by its central role in driving AMOLED innovation and consumer expectations for superior displays.

|

| By End User |

|

Smartphone OEMs dominate as primary adopters, leveraging these chips to differentiate products in a competitive landscape.

|

| By Panel Type |

|

Flexible Panels spearheads growth, capitalizing on the shift toward innovative form factors in premium devices.

|

| By Packaging |

|

Chip on Film (COF) prevails due to its versatility in high-density AMOLED implementations.

|

Regional Analysis: Integrated AMOLED Display Driver Chip Market

Asia-Pacific

Asia-Pacific leads in pioneering compact, high-speed Integrated AMOLED Display Driver Chips with embedded gamma correction and timing controllers. Firms leverage mature foundries to achieve superior yield rates, enabling brighter displays with lower power draw for mobile devices.

Explosive growth in smartphones and wearables drives adoption of these chips, where integrated designs optimize resolution and color accuracy. Local assembly lines ensure quick adaptation to market trends like curved screens.

Vertical integration among key players minimizes disruptions, fostering reliable delivery of driver ICs for large-area AMOLED panels used in TVs and monitors, enhancing regional market stability.

Rising electric vehicle production spurs demand for rugged Integrated AMOLED Display Driver Chips, supporting dashboard and infotainment systems with high refresh rates and wide viewing angles.

North America

North America plays a pivotal role in Integrated AMOLED Display Driver Chip Market through innovation-driven design centers and strong IP portfolios. Tech giants focus on custom solutions for premium smartphones and AR/VR devices, emphasizing low-latency drivers for immersive experiences. Collaborative ecosystems between fabless chip firms and U.S.-based foundries accelerate prototyping. Adoption in medical displays and aviation highlights the region’s push for high-reliability chips. While manufacturing lags behind Asia, strategic partnerships bridge gaps, positioning North America for growth in niche, high-margin segments amid evolving consumer preferences for vibrant visuals.

Europe

Europe’s Integrated AMOLED Display Driver Chip Market thrives on stringent quality standards and automotive applications. Chip developers prioritize energy-efficient designs compliant with EU regulations, targeting dashboard clusters and heads-up displays. Research institutions drive advancements in flexible substrates, enhancing durability for wearables. A balanced mix of local startups and established players fosters competition, with focus on sustainable manufacturing. Growing smart home integration further propels demand, as integrated drivers enable seamless connectivity in appliances, solidifying Europe’s reputation for precision-engineered solutions.

South America

In South America, Integrated AMOLED Display Driver Chip Market is emerging, driven by expanding middle-class consumption of affordable electronics. Import reliance shapes dynamics, with local assemblers adapting imported chips for budget smartphones and TVs. Urbanization spurs investments in distribution networks, while government tech initiatives promote domestic R&D for cost-optimized drivers. Challenges like infrastructure limitations are offset by partnerships with Asian suppliers, gradually building regional capabilities for mid-range AMOLED applications in consumer devices.

Middle East & Africa

The Middle East & Africa region witnesses gradual uptake in Integrated AMOLED Display Driver Chip Market, centered on digital transformation in consumer and public sectors. Oil-rich economies fund smart city projects incorporating high-quality displays, favoring durable chips for outdoor signage. Africa’s mobile-first market boosts demand for power-thrifty drivers in feature-rich phones. Infrastructure investments and rising e-commerce accelerate penetration, though fragmented supply chains pose hurdles. Strategic alliances with global leaders pave the way for localized adaptations, unlocking potential in diverse applications.

Report Scope

This market research report provides a comprehensive analysis of Integrated AMOLED Display Driver Chip Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Integrated AMOLED Display Driver Chip Market?

-> Global Integrated AMOLED Display Driver Chip market was valued at USD 2.67 billion in 2025 and is projected to reach USD 5.89 billion by 2034, at a CAGR of 9.0% during the forecast period.

Which key companies operate in Integrated AMOLED Display Driver Chip Market?

-> Key players include Magnachip Semiconductor, Samsung System LSI, LX Semicon, Synaptics, OmniVision, Raydium Semiconductor, New Vision Microelectronics, Himax Technologies, Novatek Microelectronics, Fitipower Integrated, among others. In 2025, the global top five players had a share approximately % in terms of revenue.

What are the key growth drivers?

-> Key growth drivers include demand from Smart Watch, Mobile Phone, Tablet applications, industry trends, recent developments, and integration of multiple functional modules to optimize display performance.

Which region dominates the market?

-> The U.S. market size is estimated at USD million in 2025 while China is projected to reach USD million. Asia, including China, Japan, and South Korea, holds significant market share.

What are the emerging trends?

-> Emerging trends include 2K segment projected to reach USD million by 2034 at a % CAGR in the next six years, along with growth in 4K and 8K product types, and expansion in applications like Tablets and Others.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...