MARKET INSIGHTS

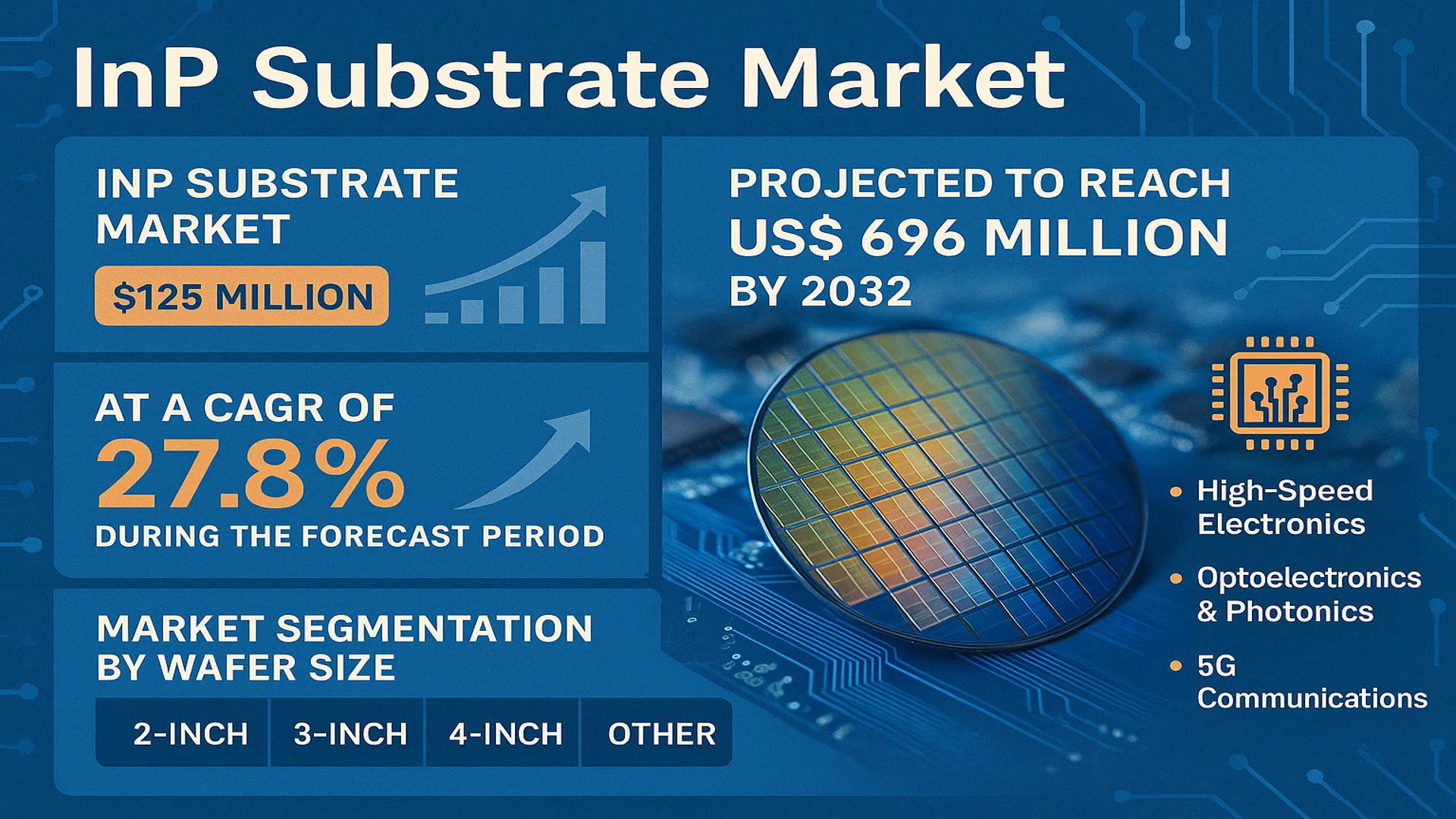

The global InP Substrate Market was valued at 125 million in 2024 and is projected to reach US$ 696 million by 2032, at a CAGR of 27.8% during the forecast period.

An InP (Indium Phosphide) substrate is a semiconductor wafer composed of indium phosphide material, prized for its superior electron mobility and high light emission efficiency. These substrates are critical components in high-speed electronics, optoelectronics, and photonics applications, particularly in 5G communications, data centers, and advanced sensor technologies. The market is segmented by wafer size, including 2-inch, 3-inch, 4-inch, 6-inch, and other diameters, with the 2-inch segment showing notable growth potential.

The market expansion is driven by increasing demand for high-performance semiconductors in telecommunication and defense sectors, coupled with advancements in compound semiconductor technologies. North America and Asia-Pacific dominate the market share, with the U.S. and China being key revenue contributors. Leading manufacturers such as Sumitomo Electric and AXT hold significant market positions, leveraging technological innovations to meet growing industry demands.

MARKET DYNAMICS

MARKET DRIVERS

Expanding 5G and Optical Communication Infrastructure to Boost Demand for InP Substrates

The global rollout of 5G networks and the continuous expansion of optical communication systems form a key driver for the InP substrates market. Indium Phosphide (InP) substrates are preferred for high-frequency applications due to their superior electron mobility and thermal stability. With 5G infrastructure demanding high-speed data transmission capabilities, the adoption of InP-based RF devices such as power amplifiers and switches has surged. Similarly, in fiber optic communication networks, InP substrates are critical components for laser diodes and photodetectors, enhancing bandwidth and efficiency. The anticipated increase in data traffic volumes due to IoT implementations and cloud computing further reinforces this demand trajectory.

Growth in Photonics and Optoelectronics Applications to Accelerate Market Expansion

Photonics and optoelectronics sectors are witnessing substantial R&D investments, contributing to the growing adoption of InP substrates. These substrates enable high-performance semiconductor lasers, LEDs, and sensors essential for applications ranging from medical imaging to autonomous vehicles. Notably, InP’s efficiency in converting electrical signals into light makes it indispensable for lidar systems—a technology critical for advanced driver-assistance systems (ADAS) and robotic automation. Furthermore, governmental initiatives supporting photonics research, such as those in Europe and North America, have accelerated commercialization, reinforcing market growth for InP substrates globally.

Increasing Demand for High-Speed Data Centers to Propel Market Growth

The exponential rise in hyperscale data centers, driven by cloud computing, AI, and big data analytics, is a significant factor compelling the need for InP substrates. These substrates enhance the efficiency of optical transceivers used in high-bandwidth interconnects, enabling faster data transfer rates while reducing power consumption—a critical requirement for sustainable data center operations. Investments in next-gen data centers, particularly in North America and Asia-Pacific, highlight the growing reliance on InP-based solutions to meet evolving technological demands.

MARKET RESTRAINTS

High Manufacturing Costs and Limited Indium Supply to Impede Market Growth

Despite their advantageous properties, InP substrates face constraints due to high production costs linked to raw material procurement and complex fabrication processes. Indium, a rare metal essential for manufacturing InP wafers, has limited global reserves, leading to price volatility and supply chain vulnerabilities. Additionally, stringent purity requirements for semiconductor-grade InP further escalate production expenses. These cost barriers may deter adoption, particularly for price-sensitive applications, and compel manufacturers to explore alternative materials despite performance trade-offs.

Technical Challenges in Large-Diameter Wafer Production to Limit Scalability

The InP substrate market is constrained by difficulties in scaling up wafer sizes beyond 6 inches while maintaining crystal quality—a critical factor for cost-efficient mass production. Current manufacturing techniques often result in defects like dislocations and micro-cracks, compromising yield rates. While the industry aims to transition toward larger wafer formats to align with silicon-based semiconductor standards, achieving defect-free InP wafers at scale remains a persistent challenge, potentially slowing market expansion.

MARKET CHALLENGES

Intense Competition from Alternative Semiconductor Materials to Pose Market Challenges

InP substrates face competition from silicon-based technologies and other III-V compounds like GaAs (Gallium Arsenide), which offer cost efficiencies for certain applications. Silicon photonics is gaining traction in data centers and telecommunications due to its compatibility with existing CMOS fabrication infrastructure. Additionally, emerging 2D materials such as graphene and transition metal dichalcogenides (TMDs) are being researched for optoelectronic uses, potentially challenging InP’s dominance. Market players must emphasize unique performance advantages to maintain competitiveness amid these alternatives.

Complexity in Heterogeneous Integration to Hinder Adoption

The integration of InP-based devices with silicon platforms—crucial for hybrid photonic-electronic systems—introduces technical complexities. Mismatches in thermal expansion coefficients and lattice structures between InP and silicon require advanced bonding techniques, increasing fabrication costs and limiting production scalability. Addressing these integration hurdles through innovations like wafer bonding and epitaxial growth technologies will be pivotal for broader market penetration.

MARKET OPPORTUNITIES

Advancements in Quantum Computing to Unlock New Growth Avenues

Quantum computing represents a transformative opportunity for InP substrates, which are integral to developing qubit technologies and photonic quantum circuits. Their ability to operate at telecom wavelengths aligns with quantum communication needs, positioning InP as a strategic material for next-gen quantum devices. With governments and tech giants investing heavily in quantum R&D, collaborations between semiconductor manufacturers and research institutions could accelerate commercialization efforts in this niche.

Rising Demand for Satellite Communication Systems to Drive Future Adoption

The surge in low-earth orbit (LEO) satellite deployments for global broadband coverage underscores opportunities for InP-based RF components. These substrates enable high-efficiency power amplifiers and transceivers capable of operating in extreme conditions—a prerequisite for satellite communications. As private and public sectors expand satellite constellations, InP substrates are poised to play a vital role in meeting the technical demands of this high-growth sector.

InP SUBSTRATE MARKET TRENDS

Expanding Demand for High-Speed Optoelectronic Devices Drives Market Growth

The InP (Indium Phosphide) substrate market is experiencing robust growth, primarily driven by increasing demand for high-speed optoelectronic and photonic devices. As industries shift toward next-generation communication technologies such as 5G and fiber-optic networks, the superior electron mobility and light emission efficiency of InP make it indispensable. In 2024, the market was valued at $125 million, and projections indicate a compound annual growth rate (CAGR) of 27.8%, pushing the market value to $696 million by 2032. Key applications in optical module devices, RF components, and sensor technologies further contribute to this expansion, with the U.S. and China emerging as dominant regions investing heavily in semiconductor advancements.

Other Trends

Innovations in Wafer Technology

Technological advancements in wafer fabrication are significantly improving InP substrate efficiency and cost-effectiveness. The increasing adoption of 6-inch InP wafers—compared to traditional 2-inch and 4-inch variants—enhances yield and reduces production costs for manufacturers. Innovations like epitaxial growth techniques and defect-reduction methods are further refining substrate quality, making them highly suitable for high-performance semiconductor applications. The 2-inch segment, though smaller, remains critical for niche applications, while larger wafers gain traction in mass production for telecommunications and data centers.

Growing Investments in Semiconductor Infrastructure

Government initiatives and private sector investments in semiconductor manufacturing are accelerating the InP substrate market’s expansion. Countries like the U.S., China, Japan, and South Korea are actively funding R&D and domestic production capabilities to reduce reliance on imports. In China, for instance, semiconductor self-sufficiency policies have spurred local players like Beijing Tongmei Xtal Technology and Zhuhai Dingtai Xinyuan to scale production. Meanwhile, collaborations between leading manufacturers—such as Sumitomo Electric and JX Advanced Metals Corporation—are fostering advancements in InP wafer purity and uniformity, meeting the stringent requirements of advanced photonics and quantum computing applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Leaders Drive Innovation in InP Substrate Manufacturing

The global InP substrate market features a moderately consolidated competitive landscape, dominated by established semiconductor material manufacturers and emerging specialty players. Leading companies are investing heavily in wafer diameter expansion and crystal growth technologies to meet the growing demand for high-performance semiconductor applications.

Sumitomo Electric Industries maintains a dominant position with approximately 30% market share in 2024, owing to its advanced crystal growth techniques and extensive distribution network across Asia and North America. The company recently announced plans to expand its 6-inch InP wafer production capacity by 40% by 2026 to address the booming demand for photonic integrated circuits.

Meanwhile, JX Advanced Metals Corporation (formerly JX Nippon Mining & Metals) and Beijing Tongmei Xtal Technology (AXT) are strengthening their positions through vertical integration strategies. These companies have developed proprietary manufacturing processes that significantly reduce defect densities while improving wafer uniformity – critical factors for high-yield device fabrication.

The competitive intensity is further heightened by Chinese players like Zhuhai Dingtai Xinyuan and Guangdong Tianding Sike New Materials, who are aggressively expanding their production capabilities. These companies benefit from strong domestic demand and government support for semiconductor material independence, though they currently focus primarily on smaller diameter substrates (2-4 inches).

Market leaders are pursuing several strategic initiatives to maintain their competitive edge:

- R&D investments in defect reduction and large-diameter wafer production

- Long-term supply agreements with major compound semiconductor foundries

- Geographic expansion into emerging manufacturing hubs

List of Key InP Substrate Manufacturers

- Sumitomo Electric Industries (Japan)

- JX Advanced Metals Corporation (Japan)

- Beijing Tongmei Xtal Technology (AXT) (China/US)

- Zhuhai Dingtai Xinyuan (China)

- FanMei Strategic Metal Resources (China)

- Guangdong Tianding Sike New Materials (China)

- Yunnan Xinyao Semiconductor Materials (China)

Looking ahead, competition is expected to intensify as demand grows for larger diameter substrates (6-inch and above) and higher quality specifications. Companies with strong intellectual property portfolios in crystal growth technologies and the ability to scale production efficiently will likely gain market share in this high-growth semiconductor material segment.

Segment Analysis:

By Type

6-Inch Substrates Dominates the Market Due to High Demand in High-Performance Applications

The market is segmented based on type into:

- 2 inches

- 3 inches

- 4 inches

- 6 inches

- Other

By Application

Optical Module Devices Segment Leads Due to Expanding Fiber Optic Networks and Data Communication Needs

The market is segmented based on application into:

- Optical Module Devices

- RF Devices

- Sensor Devices

- Other Applications

By End-Use Industry

Telecommunications Segment Leads with Accelerating 5G Implementation

The market is segmented based on end-use industry into:

- Telecommunications

- Aerospace & Defense

- Healthcare

- Consumer Electronics

- Industrial

Regional Analysis: InP Substrate Market

Asia-Pacific

The Asia-Pacific region dominates the global InP substrate market, accounting for the largest revenue share due to rapid advancements in semiconductor manufacturing and strong demand for optoelectronic components. Countries like China, Japan, and South Korea are at the forefront, leveraging government initiatives to strengthen domestic semiconductor supply chains. For instance, China’s semiconductor self-sufficiency push has accelerated investments in compound semiconductor materials, including InP substrates. Meanwhile, Japan benefits from the presence of key players like Sumitomo Electric, which specializes in high-quality InP wafer production for 5G and photonics applications. South Korea’s robust ecosystem for RF and optical devices further drives market expansion, with companies integrating InP substrates into next-generation communication systems.

North America

North America remains a critical market, driven by heavy investments in telecommunications, defense, and aerospace applications requiring high-frequency InP-based components. The U.S. leads with significant R&D spending in photonics and quantum computing, where InP substrates play a pivotal role. Federal programs like the CHIPS Act and collaborations between research institutions and manufacturers are fostering innovation. However, the region faces challenges in scaling production capacity compared to Asia, relying partially on imports for high-volume requirements. Companies are focusing on specialized, high-margin applications such as LiDAR and advanced sensors to maintain competitiveness.

Europe

Europe’s market growth is fueled by strong academic-industry partnerships and demand for energy-efficient photonic devices. Countries like Germany, the UK, and France are investing in InP-based solutions for data centers and automotive LiDAR systems under the broader EU digital transformation agenda. The region emphasizes sustainability, pushing for advancements in substrate recycling and lower-defect crystal growth techniques. However, limited local production capacity and dependence on Asian suppliers for raw materials pose supply chain risks. Collaborative projects between universities and manufacturers aim to address these gaps while maintaining Europe’s edge in high-precision applications.

Middle East & Africa

This emerging market shows promising growth potential, particularly in GCC countries investing in telecom infrastructure and smart city initiatives. While current demand is modest compared to other regions, partnerships with global InP substrate manufacturers are enabling technology transfer for niche applications like satellite communication. Substrate adoption remains constrained by high costs and limited local expertise, but increasing foreign direct investment in semiconductor-related projects signals long-term opportunities. South Africa and the UAE are emerging as focal points for research collaborations in photonics.

South America

The region exhibits slower growth due to economic volatility and fragmented industrial base, though Brazil and Argentina show increasing interest in InP substrates for specialized defense and aerospace applications. Local manufacturing is virtually nonexistent, creating dependence on imports. However, rising awareness of InP’s advantages in harsh-environment electronics and prospective government support for technology parks could stimulate future market development. The lack of regulatory frameworks for advanced materials remains a bottleneck for widespread adoption.

Key Regional Trends

- Asia-Pacific’s manufacturing scale and government backing cement its leadership position

- North America and Europe prioritize high-value applications over volume production

- Emerging markets face adoption barriers but present untapped potential via strategic partnerships

- Global supply chain rebalancing efforts may redistribute some production capacity across regions

Report Scope

This market research report provides a comprehensive analysis of the global and regional InP Substrate markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global InP Substrate market was valued at USD 125 million in 2024 and is projected to reach USD 696 million by 2032, at a CAGR of 27.8% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (2 inches, 3 inches, 4 inches, 6 inches, others), application (Optical Module Devices, RF Devices, Sensor Devices), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Sumitomo Electric, JX Advanced Metals Corporation, Beijing Tongmei Xtal Technology (AXT), and Zhuhai Dingtai Xinyuan.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in semiconductor manufacturing, advancements in fabrication techniques, and evolving industry standards for InP substrates.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing demand for high-speed electronics and optoelectronics) along with challenges (supply chain constraints, regulatory issues, and material costs).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the InP Substrate market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global InP Substrate Market?

-> InP Substrate Market was valued at 125 million in 2024 and is projected to reach US$ 696 million by 2032, at a CAGR of 27.8% during the forecast period.

Which key companies operate in Global InP Substrate Market?

-> Key players include Sumitomo Electric, JX Advanced Metals Corporation, Beijing Tongmei Xtal Technology (AXT), Zhuhai Dingtai Xinyuan, FanMei Strategic Metal Resources, Guangdong Tianding Sike New Materials, and Yunnan Xinyao Semiconductor Materials.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-speed electronics, increasing adoption in optoelectronic applications, and advancements in semiconductor fabrication technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by semiconductor manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of larger wafer sizes (6 inches and above), integration with AI-powered manufacturing processes, and increasing R&D in photonics applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...