MARKET INSIGHTS

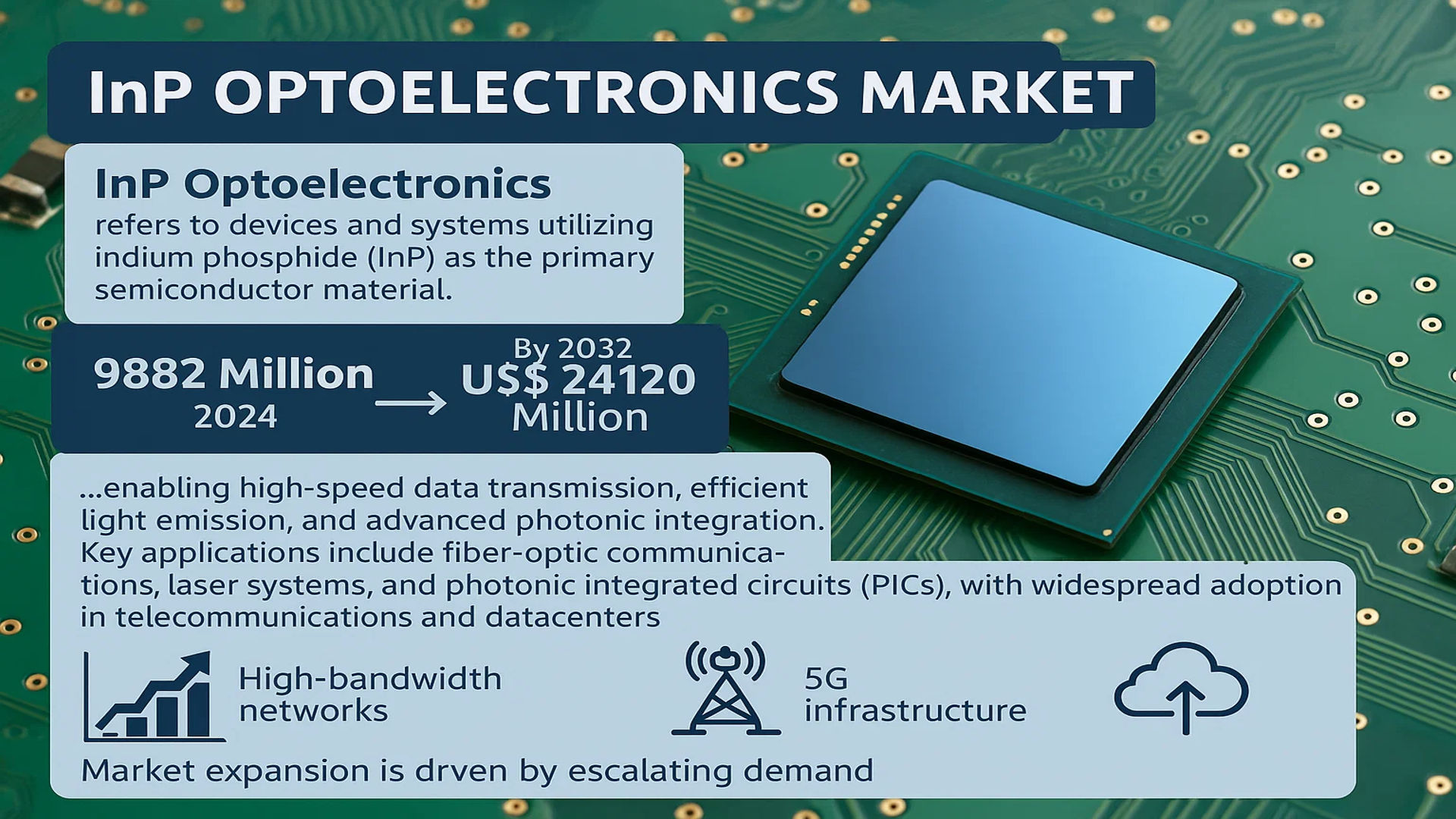

The global InP Optoelectronics Market was valued at 9882 million in 2024 and is projected to reach US$ 24120 million by 2032, at a CAGR of 9.7% during the forecast period.

InP Optoelectronics refers to devices and systems utilizing indium phosphide (InP) as the primary semiconductor material. These components leverage InP’s superior electronic and optical properties, enabling high-speed data transmission, efficient light emission, and advanced photonic integration. Key applications include fiber-optic communications, laser systems, and photonic integrated circuits (PICs), with widespread adoption in telecommunications and datacenters.

Market expansion is driven by escalating demand for high-bandwidth networks, the proliferation of 5G infrastructure, and advancements in cloud computing. The U.S. currently dominates the market, while China is emerging as a high-growth region due to accelerated digital transformation. Leading players like Lumentum, Broadcom, and Coherent (II-VI) are investing in R&D to develop next-generation InP-based solutions, further propelling market growth. The Fabry-Perot Laser Diode segment remains a key revenue contributor, though emerging technologies like Electro-Absorption Modulated Lasers (EMLs) are gaining traction.

MARKET DRIVERS

Exponential Growth in Data Center and Telecommunications Demand Fuels InP Optoelectronics Adoption

The rapid expansion of cloud computing, 5G networks, and hyperscale data centers is creating unprecedented demand for high-speed optical communication systems. InP-based optoelectronic components, particularly distributed feedback (DFB) lasers and electro-absorption modulated lasers (EMLs), are becoming essential for 100G, 400G, and emerging 800G optical transceivers. With global IP traffic projected to grow at 23% CAGR through 2027, network operators are increasingly adopting InP solutions to meet bandwidth requirements while maintaining power efficiency. The superior performance of InP at high frequencies makes it the material of choice for next-generation optical networks.

Advancements in Photonic Integrated Circuits Accelerate Market Penetration

Recent breakthroughs in photonic integrated circuit (PIC) technology utilizing InP substrates are transforming optical system design. Leading manufacturers have demonstrated monolithic integration of lasers, modulators, and detectors on single InP chips, enabling more compact and power-efficient devices. This integration is critical for applications ranging from co-packaged optics in data centers to miniaturized sensing systems. The capability to combine multiple optical functions on a single InP die reduces assembly complexity and improves yield – factors that directly impact production costs and time-to-market.

Furthermore, investments in PIC foundries and design automation tools are lowering barriers to entry for innovative startups and established players alike. The growing ecosystem of InP-based PIC solutions is expected to drive adoption across new verticals including aerospace, medical diagnostics, and automotive LiDAR.

MARKET RESTRAINTS

High Manufacturing Costs and Yield Challenges Impede Mass Adoption

Despite superior performance characteristics, InP optoelectronics face significant production challenges that constrain market expansion. The compound semiconductor’s inherent material properties, including fragility and sensitivity to defects, result in lower wafer yields compared to silicon-based alternatives. Epitaxial growth of InP layers requires precise control over temperature and gas flows, with even minor deviations causing substantial performance variations. These manufacturing complexities contribute to unit costs that are typically 20-30% higher than competing technologies.

Supply Chain Vulnerabilities

The InP optoelectronics market remains vulnerable to supply chain disruptions for critical raw materials. Indium, a key component, has faced periodic shortages due to limited global production capacity and competing demands from display manufacturers. The specialized equipment required for InP fabrication represents another bottleneck, with lead times for key tools extending beyond 12 months during peak demand periods.

MARKET CHALLENGES

Technological Complexity Creates Barriers to Market Entry

Designing and manufacturing InP-based optoelectronic devices requires deep domain expertise across multiple technical disciplines. The physics of III-V semiconductor behavior, optical waveguide design principles, and thermomechanical packaging considerations create steep learning curves for new entrants. Many established industry players protect their intellectual property through extensive patent portfolios, further increasing barriers to competition.

Skilled Labor Shortage

The industry faces an acute shortage of engineers with specialized InP processing experience. Universities produce relatively few graduates with hands-on III-V semiconductor training, forcing companies to invest heavily in internal development programs. This talent gap is particularly problematic for startups attempting to commercialize innovative InP technologies.

MARKET OPPORTUNITIES

Emerging Applications in Sensing and Quantum Technologies Present New Growth Frontiers

Beyond traditional communications applications, InP optoelectronics are finding growing adoption in cutting-edge fields requiring high-performance photonic solutions. Quantum computing developers increasingly utilize InP-based single-photon sources and detectors for their superior performance at telecommunications wavelengths. The emerging quantum communications sector presents a particularly promising opportunity, with secure quantum key distribution systems relying heavily on InP components.

The medical diagnostics field represents another high-growth area, where InP’s tunable emission characteristics enable advanced spectroscopy and imaging systems. Recent clinical trials have demonstrated the effectiveness of InP quantum dot biomarkers for early cancer detection, opening potential applications in point-of-care diagnostics.

Automotive LiDAR manufacturers are also turning to InP lasers and receivers to meet the demanding performance requirements of autonomous vehicle systems. The material’s ability to operate at eye-safe wavelengths while delivering high peak power makes it ideal for next-generation ranging and 3D sensing applications.

InP OPTOELECTRONICS MARKET TRENDS

Growth in High-Speed Data Transmission Applications Driving Market Expansion

The global InP optoelectronics market is witnessing accelerated growth, primarily fueled by the rising demand for high-speed data transmission in telecommunications and datacenters. Indium Phosphide (InP) based devices are increasingly favored due to their superior efficiency in handling high-frequency signals and compatibility with optical communication networks. With data traffic expected to grow at a compound annual growth rate (CAGR) of over 25% in the next five years, there is a pressing need for high-performance optoelectronic components. The deployment of 5G networks and expansion of fiber-optic infrastructure are further reinforcing this trend. Leading market players are ramping up production capacities to meet the escalating demand for InP-based laser diodes and photodetectors, which are critical in enabling next-generation optical communication systems.

Other Trends

Advancements in Photonic Integrated Circuits (PICs)

The integration of InP in photonic integrated circuits (PICs) is revolutionizing the semiconductor industry, facilitating the development of compact, energy-efficient devices for telecommunications and sensing applications. PICs leverage the high electron mobility and direct bandgap properties of InP, enabling faster data processing and reduced power consumption compared to traditional silicon-based solutions. The adoption of these circuits is particularly notable in datacenters, where minimizing latency and energy usage is crucial. Furthermore, advancements in quantum dot lasers built on InP substrates are enhancing the performance and scalability of optoelectronic components, paving the way for innovations in high-speed computing and secure quantum communication.

Expansion of Datacenters and Cloud Services

The proliferation of cloud computing and hyperscale data centers is significantly contributing to the demand for InP optoelectronics. With enterprises increasingly migrating to cloud-based solutions, there is a heightened need for ultra-fast and reliable optical interconnects. InP-based electro-absorption modulated lasers (EMLs) and distributed feedback lasers (DFBs) are central to this transition, offering superior modulation speeds and signal integrity. Datacenter operators are investing heavily in upgrading their infrastructure to support bandwidth-intensive applications like artificial intelligence (AI) and machine learning (ML), which require seamless data transfer rates exceeding 400G and beyond. This shift is propelling market revenues, with the datacenter segment projected to grow at a CAGR of approximately 11% over the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global InP Optoelectronics market is characterized by intense competition, with major players leveraging technological advancements and strategic acquisitions to strengthen their market positions. Lumentum currently holds a dominant position, owing to its comprehensive product portfolio in optical communication components and strong R&D capabilities. The company’s expertise in high-power lasers and photonic solutions has solidified its leadership, especially in North America and Asia-Pacific markets.

Coherent (II-VI) and Broadcom follow closely, capturing significant market shares through their vertically integrated manufacturing processes and diverse applications in telecommunications and datacenters. These companies have demonstrated remarkable resilience despite supply chain challenges, focusing on meeting the growing demand for high-speed optical networking solutions.

Furthermore, Japanese players like Sumitomo Electric and Furukawa Electric continue to expand their global footprint through joint ventures and capacity expansions in the Asia-Pacific region. Their expertise in indium phosphide-based laser diodes positions them strongly in emerging 5G and cloud computing applications.

Meanwhile, mid-sized innovators such as AdTech Optics and Inphenix are carving niche segments through specialized product offerings, particularly in medical and defense applications. Their agile approach to development allows faster adaptation to evolving industry requirements compared to larger competitors.

List of Key InP Optoelectronics Companies Profiled

- Lumentum Holdings Inc. (U.S.)

- Coherent (II-VI Incorporated) (U.S.)

- Broadcom Inc. (U.S.)

- Sumitomo Electric Industries (Japan)

- Applied Optoelectronics (U.S.)

- Furukawa Electric Co. (Japan)

- MACOM Technology Solutions (U.S.)

- AdTech Optics (U.S.)

- Inphenix (U.S.)

- Nanoplus GmbH (Germany)

- RPMC Lasers (U.S.)

- Frankfurt Laser Company (Germany)

- Advanced Imaging (U.S.)

- Innolume GmbH (Germany)

- OPTICA Photonics (Germany)

- VIAVI Solutions Inc. (U.S.)

Segment Analysis:

By Type

Fabry-Perot Laser Diode (FP) Segment Leads Due to High Demand in Optical Communication

The market is segmented based on type into:

- Fabry-Perot Laser Diode (FP)

- Distributed Feedback Laser (DFB)

- Electro-Absorption Modulated Laser (EML)

- Others

By Application

Telecommunications Segment Dominates Owing to Rising Demand for High-Speed Data Transmission

The market is segmented based on application into:

- Telecommunications

- Datacenters

- Others

By Component

Laser Diodes Hold Major Share Due to Expanding Fiber Optic Network Deployments

The market is segmented based on component into:

- Laser Diodes

- Photodetectors

- Optical Modulators

- Others

By Wavelength

1310 nm Wavelength Segment Grows Rapidly for Metro Network Applications

The market is segmented based on wavelength into:

- 1310 nm

- 1550 nm

- Others

Regional Analysis: InP Optoelectronics Market

The Asia-Pacific region dominates the global InP optoelectronics market, accounting for over 40% of revenue share in 2024. This leadership position stems from massive telecommunications infrastructure expansion, particularly in China, Japan, and South Korea. China’s “Digital Silk Road” initiative and Japan’s focus on 6G technology development are driving substantial demand for high-speed optical components. India’s rapidly growing datacenter market, projected to reach 1,318 MW capacity by 2025, further fuels adoption of InP-based devices. While cost sensitivity remains a challenge, regional manufacturers are increasingly investing in research to develop more affordable fabrication techniques without compromising performance.

North America

North America represents the second-largest market for InP optoelectronics, driven by advanced defense applications and quantum computing research. The U.S. Department of Defense’s increased funding for photonic integrated circuits and the commercial rollout of 800G transceivers in major datacenters are key growth factors. Silicon Valley’s tech ecosystem continues to push innovation boundaries, with companies like Lumentum and Coherent leading in tunable laser development. However, export restrictions on certain InP technologies to China have created both challenges and opportunities for domestic suppliers.

Europe

Europe maintains a strong position in specialty InP applications, particularly in automotive LiDAR and biomedical sensing. Strict data privacy regulations (GDPR) are accelerating the adoption of secure optical communication systems based on InP components. Germany’s Fraunhofer Institute and other research centers have made significant breakthroughs in quantum dot lasers on InP substrates. The European Commission’s Horizon Europe program has allocated substantial funding for photonics research, supporting the region’s transition from traditional manufacturing to high-value optoelectronic solutions.

Middle East & Africa

This emerging market shows promising growth potential, particularly in telecommunications infrastructure modernization. Saudi Arabia’s Vision 2030 and UAE’s Smart City initiatives are driving investments in optical networks. While adoption rates remain low compared to other regions, strategic partnerships between global InP manufacturers and local telecom providers are beginning to bear fruit. The lack of domestic manufacturing capabilities currently makes the region dependent on imports, creating opportunities for established suppliers to expand their distribution networks.

South America

South America represents the smallest but gradually expanding market for InP optoelectronics. Brazil leads regional adoption, mainly in fiber optic network expansion projects across major urban centers. Economic volatility and currency fluctuations pose challenges for consistent technology investment, though the growing demand for high-speed internet in Argentina and Chile is creating new opportunities. Partnerships with Asian manufacturers help mitigate cost barriers, enabling gradual market penetration of InP-based optical solutions.

Report Scope

This market research report provides a comprehensive analysis of the global InP Optoelectronics market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global InP Optoelectronics market was valued at USD 9,882 million in 2024 and is projected to reach USD 24,120 million by 2032, growing at a CAGR of 9.7%.

- Segmentation Analysis: Detailed breakdown by product type (FP Laser Diode, DFB Laser, EML), application (Telecommunications, Datacenters, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key markets driving growth.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Top players include Lumentum, Coherent (II-VI), Broadcom, Sumitomo, and Applied Optoelectronics.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of photonic integrated circuits, high-bitrate communication systems, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global InP Optoelectronics Market?

-> InP Optoelectronics Market was valued at 9882 million in 2024 and is projected to reach US$ 24120 million by 2032, at a CAGR of 9.7% during the forecast period.

Which key companies operate in Global InP Optoelectronics Market?

-> Key players include Lumentum, Coherent (II-VI), Broadcom, Sumitomo, Applied Optoelectronics, Furukawa Electric, and Macom, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-speed data transmission, expansion of 5G networks, increasing adoption in datacenters, and advancements in photonic integrated circuits.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market due to technological advancements and high adoption rates.

What are the emerging trends?

-> Emerging trends include development of ultra-high-speed optoelectronic devices, integration with AI-driven networks, and increased focus on energy-efficient solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...