MARKET INSIGHTS

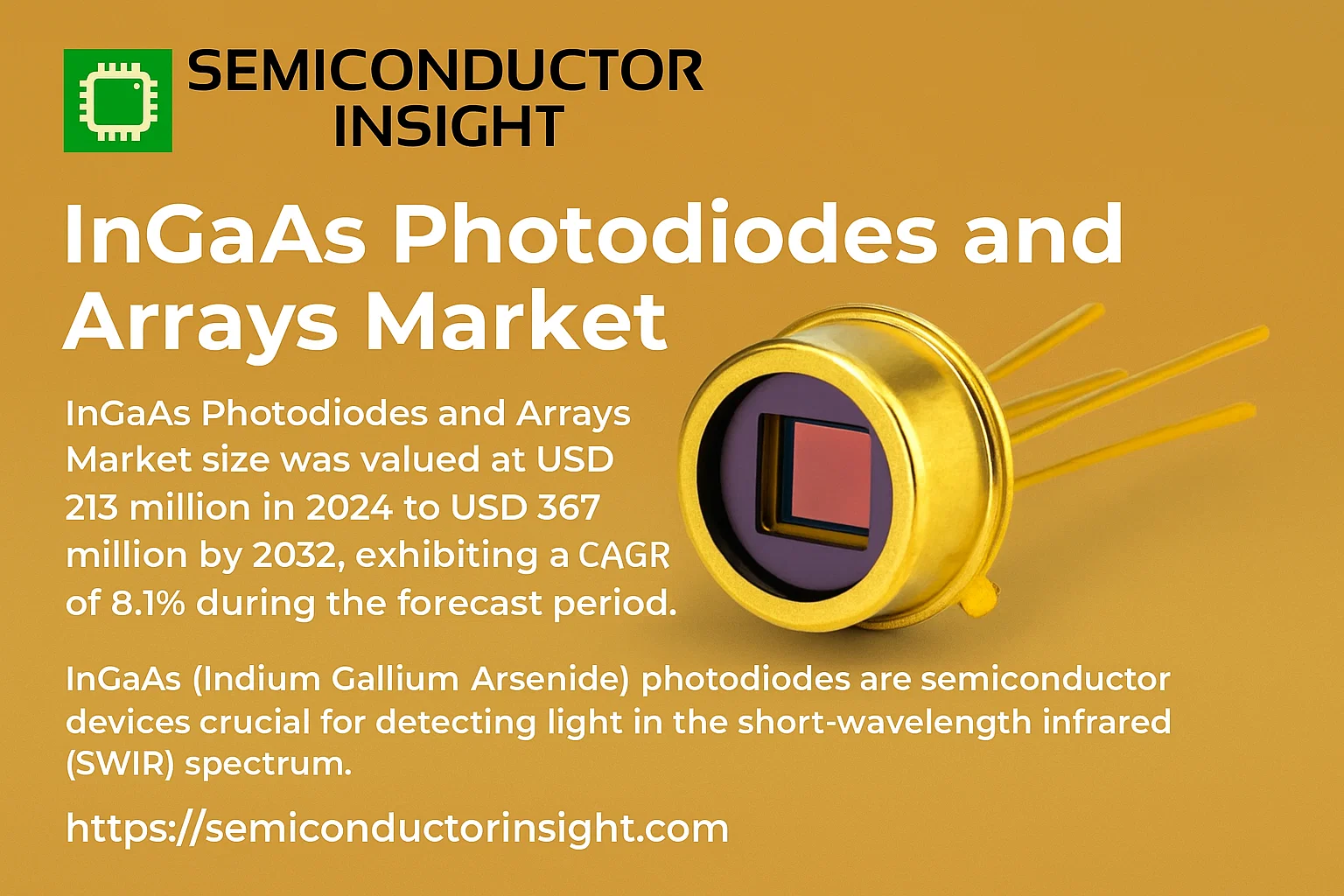

Global InGaAs Photodiodes and Arrays Market size was valued at USD 213 million in 2024 to USD 367 million by 2032, exhibiting a CAGR of 8.1% during the forecast period.

InGaAs (Indium Gallium Arsenide) photodiodes are semiconductor devices crucial for detecting light in the short-wavelength infrared (SWIR) spectrum. These components are sensitive to wavelengths over a wide spectral range, typically from 0.9 to 2.6 micrometers, and are available as image sensors, linear/area arrays, and photodiode/amplifier combination devices.

The market is experiencing robust growth due to several factors, including rising demand for high-performance sensing in security and surveillance, expanding fiber optic communication networks, and increasing adoption in industrial process control. Furthermore, advancements in spectroscopy and scientific research are contributing significantly to market expansion. The competitive landscape is concentrated; the top three players—OSI Optoelectronics, Hamamatsu Photonics, and Kyosemi Corporation—collectively hold a share of over 43%. Geographically, Asia-Pacific dominates as the largest market with a share of about 45%, driven by strong manufacturing and telecommunications sectors.

MARKET DRIVERS

Expanding Applications in Fiber Optic Communication

The relentless global demand for higher data transmission rates is a primary driver for InGaAs photodiodes. Their sensitivity in the short-wavelength infrared (SWIR) range, particularly around 1310 nm and 1550 nm, makes them the detector of choice for modern fiber optic communication systems. The deployment of 5G infrastructure and the ongoing expansion of data centers are fueling significant demand for high-speed receivers that utilize these components.

Growth in Industrial and Scientific Imaging

Beyond telecommunications, InGaAs arrays are experiencing strong growth in industrial process control and scientific research. Applications such as semiconductor wafer inspection, hyperspectral imaging for agriculture and food sorting, and astronomy benefit from the ability of InGaAs detectors to see through certain materials and identify chemical compositions based on their unique SWIR signatures. This diversification is creating new, sustained revenue streams for manufacturers.

Advancements in material science and fabrication techniques are also acting as a key driver. The development of extended InGaAs detectors with sensitivity beyond 2.2 μm is opening up new possibilities in spectroscopy and gas sensing, while improvements in reducing dark current are enhancing performance for low-light applications.

MARKET CHALLENGES

High Cost and Complex Manufacturing

The epitaxial growth of high-quality InGaAs material on indium phosphide substrates is a complex and expensive process. This inherent cost of raw materials and fabrication presents a significant challenge for widespread adoption, particularly in price-sensitive consumer markets. Achieving high yield and uniformity across arrays further adds to the manufacturing complexity and cost.

Other Challenges

Competition from Alternative Technologies

In some application segments, such as low-cost proximity sensing or consumer electronics, InGaAs photodiodes face stiff competition from silicon-based detectors and emerging technologies like organic photodiodes, which offer lower costs albeit with different performance characteristics.

Thermal Management and Performance Limitations

Managing dark current, which increases with temperature, remains a technical challenge. For high-performance applications, cooling is often required, which adds to the system’s cost, size, and power consumption, limiting use in portable or resource-constrained environments.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Geopolitical Factors

The market is susceptible to disruptions in the supply of critical raw materials, such as indium and gallium. These elements are subject to price volatility and geopolitical tensions, as their mining and refining are concentrated in a few countries. Any significant disruption can lead to increased costs and delayed production for InGaAs device manufacturers.

High Initial Investment for End-Users

The total cost of ownership for systems utilizing InGaAs detectors is often high. This includes not just the photodiodes or arrays themselves, but also the associated electronics for signal readout and, frequently, thermoelectric coolers. This high capital expenditure can restrain adoption, especially among small and medium-sized enterprises or in new, unproven application areas.

MARKET OPPORTUNITIES

Emergence of Autonomous Vehicles and LiDAR

The rapid development of autonomous vehicles and Advanced Driver-Assistance Systems (ADAS) presents a major growth opportunity. InGaAs-based LiDAR systems offer superior performance in adverse weather conditions like fog and rain compared to traditional silicon-based sensors, as SWIR light is less scattered. This key advantage is driving R&D investments and pilot deployments.

Advancements in Healthcare and Life Sciences

There is significant potential for InGaAs detectors in non-invasive medical diagnostics and bio-imaging. Techniques like optical coherence tomography (OCT) and diffuse optical tomography can be enhanced using SWIR light for deeper tissue penetration. This opens up new frontiers for disease detection and biological research, representing a high-value market segment.

Miniaturization and Integration

The trend towards smaller, more integrated photonic systems creates opportunities for developing compact InGaAs sensors. Integration with readout integrated circuits (ROICs) on a chip-level scale can lead to smaller form factors, lower power consumption, and reduced costs, making the technology accessible for a broader range of portable and embedded applications.

InGaAs Photodiodes and Arrays Market Trends

Significant Market Growth Driven by Technological Advancements

Global InGaAs Photodiodes and Arrays Market is on a robust growth trajectory, projected to expand from a valuation of USD 213 million in 2024 to USD 367 million by 2032, reflecting a compound annual growth rate (CAGR) of 8.1%. This sustained growth is primarily fueled by continuous technological advancements in photodetection. The unique sensitivity of InGaAs photodiodes over a broad spectral range, particularly in the short-wavelength infrared (SWIR) region, makes them indispensable. These components are increasingly integrated into more sophisticated formats such as linear and area arrays, as well as photodiode/amplifier combination devices, enhancing their utility across various high-tech applications.

Other Trends

Dominance of Single-Element Devices

A key trend is the clear market dominance of Single-Element InGaAs PIN photodiodes, which currently hold a substantial 73% market share by product type. This prevalence is due to their reliability, cost-effectiveness, and widespread suitability for a vast array of standard sensing applications. In contrast, Multi-Element Arrays, while holding a smaller share, are experiencing growth driven by demands in imaging and multi-channel spectroscopy applications that require simultaneous detection at multiple points.

Analytical Instruments as the Primary Application

The application landscape is firmly led by Analytical Instruments, which accounts for approximately 64% of the market. This dominance is attributed to the critical role of precise light detection in spectroscopy, chemical analysis, and environmental monitoring. The consistent demand from research institutions, pharmaceutical companies, and industrial quality control labs ensures a stable and growing end-market for these high-performance photodetectors.

Asia-Pacific: Global Market Leader

Regionally, the Asia-Pacific market is the largest, commanding about 45% of Global share. This leadership is driven by strong manufacturing bases, significant investments in research and development, and the rapid adoption of new technologies in countries like China, Japan, and South Korea. North America and Europe follow with shares of 27% and 22%, respectively, supported by well-established technological sectors and high investment in defense and scientific research.

Consolidated Competitive Landscape

The market features a consolidated competitive landscape, with the top three players—OSI Optoelectronics, Hamamatsu Photonics, and Kyosemi Corporation—collectively holding over 43% of the market share. This concentration highlights the importance of technological expertise, manufacturing scale, and strong distribution networks. Competition among these and other key players is intense, focusing on product innovation, performance enhancement, and strategic expansions to capture greater market share in this growing sector.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Characterized by Technological Specialization and Global Reach

Global market for InGaAs photodiodes and arrays is led by a few dominant players with significant technological expertise and manufacturing scale. OSI Optoelectronics and Hamamatsu Photonics are among the foremost leaders, collectively holding a substantial market share along with Kyosemi Corporation; the top three players command over 43% of Global market. This concentration is driven by the high technical barriers to entry, including the need for advanced compound semiconductor fabrication capabilities and deep knowledge of optoelectronic device physics. These leading companies offer a comprehensive portfolio, from single-element photodiodes to complex linear and area arrays, catering primarily to the demanding analytical instruments segment, which accounts for approximately 64% of the application market. Their global presence, particularly strong in the Asia-Pacific region (the largest market with a 45% share), allows them to serve a diverse customer base across various high-tech industries.

Beyond the top-tier leaders, the market includes a number of specialized and technologically adept companies that compete effectively in niche segments. Firms such as First Sensor (now part of TE Connectivity), Teledyne Judson, and Sensors Unlimited (a Collins Aerospace company) have established strong positions by focusing on high-reliability applications in communications, defense, and scientific measurement equipment. Other significant participants like Laser Components, Voxtel (Allegro MicroSystems), and Albis Optoelectronics offer specialized products and custom solutions, often competing on performance specifications, customization capability, and customer support. This secondary tier of players is crucial for driving innovation and providing alternatives in applications where the standard offerings from the largest suppliers may not suffice, ensuring a dynamic and competitive marketplace.

List of Key InGaAs Photodiodes and Arrays Companies Profiled

- Hamamatsu Photonics

- OSI Optoelectronics

- Kyosemi Corporation

- Teledyne Judson

- Sensors Unlimited (Collins Aerospace)

- First Sensor (TE Connectivity)

- Laser Components

- Voxtel (Allegro MicroSystems)

- Albis Optoelectronics

- QPhotonics

- AC Photonics Inc

- Fermionics Opto-Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single-Element InGaAs PIN photodiodes dominate the market due to their superior cost-effectiveness and broad applicability across numerous standard sensing and detection tasks. Their simpler fabrication process translates to higher reliability and lower unit costs for high-volume applications. Conversely, multi-element arrays are critical for specialized applications requiring imaging or multi-point sensing, driving development in high-performance niche sectors, while combination devices offer integrated solutions that reduce system complexity for end-users. |

| By Application |

|

Analytical Instruments represent the most significant application segment, fueled by the indispensable role of InGaAs detectors in spectroscopy for material analysis, pharmaceutical quality control, and environmental monitoring. Their high sensitivity in the near-infrared spectrum is unmatched for these precise measurements. The communications sector is a key growth area, leveraging these photodiodes for high-speed data transmission in fiber optics. Measurement equipment relies on them for accurate light detection, with the ‘Others’ category encompassing emerging uses in fields like biomedical imaging and defense. |

| By End User |

|

Industrial Manufacturing is the leading end-user segment, utilizing these components for process control, quality assurance, and non-destructive testing in various production environments. The telecommunications industry is a major consumer, driven by Global expansion of fiber-optic networks requiring reliable high-speed receivers. Research and academic institutions form a stable demand base for advanced experimental setups, while the healthcare and life sciences sector is an emerging adopter, exploring applications in medical diagnostics and laboratory instrumentation, indicating strong future growth potential. |

| By Wavelength Range |

|

Short-Wavelength Infrared (SWIR) capabilities are the most commercially significant, as the primary advantage of InGaAs technology is its excellent performance in this spectral band, which is invisible to silicon-based detectors. This makes it crucial for see-through imaging, spectroscopy, and sorting applications. The standard range covers the core telecom wavelengths, ensuring steady demand. Extended wavelength variants, while serving more specialized scientific and defense applications, drive technological innovation at the frontier of detector performance, pushing the limits of sensitivity. |

| By Packaging Type |

|

Hermetic Packages lead the segment due to their critical role in ensuring long-term reliability and performance stability, especially in harsh environmental conditions encountered in industrial, aerospace, and defense applications. They protect the sensitive semiconductor material from moisture and contaminants. Non-hermetic packages offer a cost-effective solution for less demanding commercial electronics. The trend towards miniaturization is fueling innovation in ceramic and chip-scale packaging, which is essential for integrating photodiodes into compact consumer electronics and advanced medical devices, representing a key area for future development. |

Regional Analysis: InGaAs Photodiodes and Arrays Market

The region benefits from a deeply integrated supply chain for semiconductor components, which is critical for the sophisticated fabrication processes of InGaAs devices. This ecosystem reduces production costs and accelerates time-to-market for manufacturers, attracting significant investment from global players seeking efficient production capabilities and access to a large, skilled technical workforce.

Explosive growth in data consumption is driving massive deployments of fiber optic networks. InGaAs photodiodes are essential for high-bandwidth receivers in these systems. The ongoing rollout of 5G infrastructure across major economies in the region further amplifies the need for these high-speed optical components, creating a powerful, long-term demand driver.

There is strong and growing adoption of InGaAs arrays in non-telecom sectors. Industries are increasingly using near-infrared spectroscopy for quality control in agriculture, pharmaceuticals, and food processing. Furthermore, significant government and private funding for scientific research institutes fuels demand for advanced photodiode arrays in analytical instrumentation and astronomy.

National policies in key countries actively promote the development of advanced photonics and semiconductor industries. These initiatives include funding for R&D, tax incentives for high-tech manufacturers, and programs aimed at achieving technological self-sufficiency, all of which create a highly favorable environment for the growth of the InGaAs photodiodes market.

North America

North America remains a critical and technologically advanced market for InGaAs photodiodes, characterized by strong demand from defense, aerospace, and leading-edge telecommunications sectors. The presence of major technology companies and defense contractors drives the need for high-reliability, high-performance detectors for applications such as LIDAR, free-space optical communication, and surveillance systems. The region’s robust R&D infrastructure, supported by universities and corporate labs, fosters innovation in extending the wavelength range and improving the sensitivity of these devices. A mature but continually evolving fiber optic network also contributes to steady demand for components, particularly for network upgrades to support cloud computing and increasing bandwidth requirements.

Europe

The European market is defined by a strong emphasis on high-quality manufacturing and research, with significant activity in scientific instrumentation, industrial process control, and environmental monitoring. Germany, the UK, and France are key contributors, hosting numerous companies that specialize in precision optics and sensors. The region’s market benefits from stringent industrial standards and a focus on applications requiring high accuracy, such as gas sensing for emissions monitoring and quality assurance in manufacturing. Collaborations between academic institutions and industry players are common, driving advancements in hyperspectral imaging and other specialized applications that utilize InGaAs arrays.

South America

The market in South America is in a developing phase, with growth primarily driven by the gradual modernization of telecommunications infrastructure in countries like Brazil and Chile. The deployment of fiber-to-the-home projects and expansion of mobile networks are creating initial demand for optical components. The mining and agricultural sectors also present niche opportunities for InGaAs-based spectroscopy for material analysis and quality assessment. However, market growth is moderated compared to other regions due to economic volatility and more limited local manufacturing capabilities, often relying on imports to meet demand.

Middle East & Africa Middle East & Africa

This region shows nascent but promising growth potential, largely tied to major infrastructure investments, particularly in the Gulf Cooperation Council (GCC) countries. Investments in smart city projects, security and surveillance systems, and telecommunications infrastructure are key drivers. There is also growing interest in using InGaAs detectors for oil and gas pipeline monitoring and resource exploration. The market across Africa is less developed, with demand primarily concentrated in telecommunications network expansion projects and select academic research institutions, though growth is expected to accelerate as digital infrastructure investments increase.

Report Scope

This market research report provides a comprehensive analysis of the InGaAs Photodiodes and Arrays Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of InGaAs Photodiodes and Arrays Market?

-> Global InGaAs Photodiodes and Arrays Market was valued at USD 213 million in 2024 and is projected to reach USD 367 million by 2032, growing at a CAGR of 8.1% during the forecast period.

Which key companies operate in InGaAs Photodiodes and Arrays Market?

-> Key players include OSI Optoelectronics, Hamamatsu Photonics, and Kyosemi Corporation, among others. The top three players hold a market share of over 43%.

What are the key growth drivers?

-> Key growth drivers include the wide spectral sensitivity of InGaAs photodiodes, their availability as image sensors and linear/area arrays, and strong demand from key applications.

Which region dominates the market?

-> Asia-Pacific is the largest market, holding a share of about 45%, followed by North America with a 27% share and Europe with a 22% share.

What are the emerging trends?

-> Emerging trends include the dominant market position of Single-Element InGaAs PIN products, which hold a 73% share, and the significant application of these components in Analytical Instruments, which accounts for about 64% of the market.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...