MARKET INSIGHTS

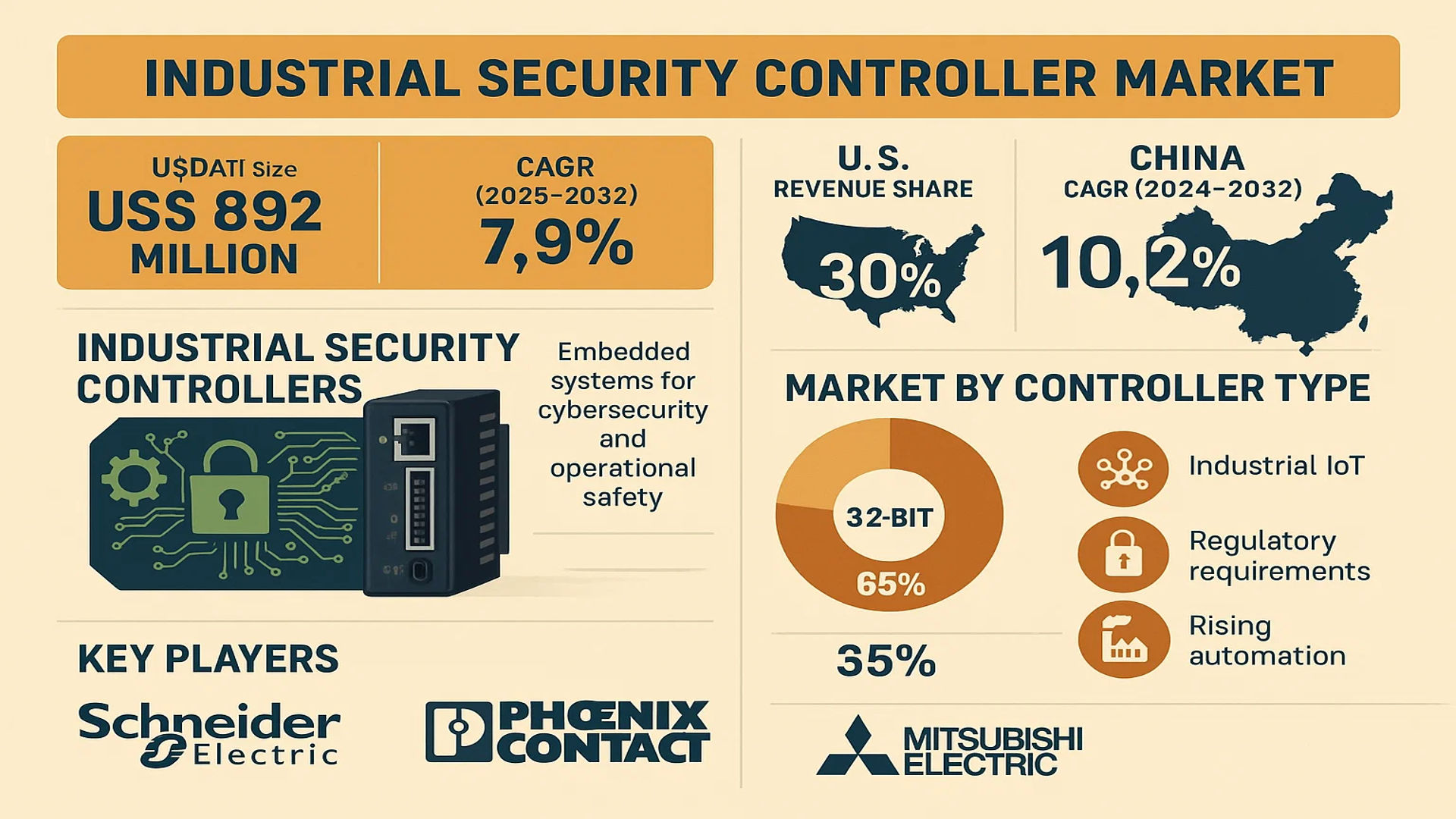

The global Industrial Security Controller Market size was valued at US$ 892 million in 2024 and is projected to reach US$ 1,520 million by 2032, at a CAGR of 7.9% during the forecast period 2025-2032. The U.S. market accounted for 30% of global revenue share in 2024, while China is expected to witness the fastest growth with a projected CAGR of 10.2% from 2024 to 2032.

Industrial Security Controllers are specialized embedded systems designed to provide robust cybersecurity and operational safety for industrial automation environments. These controllers integrate advanced security features such as cryptographic acceleration, secure boot, tamper detection, and secure communication protocols to protect critical infrastructure against cyber threats. The market primarily consists of 32-bit and 16-bit controller variants, with the 32-bit segment dominating over 65% of market share in 2024.

Market growth is being driven by increasing industrial IoT adoption, stringent regulatory requirements for industrial cybersecurity, and rising automation across manufacturing facilities. The emergence of Industry 4.0 technologies has particularly accelerated demand, as evidenced by recent partnerships like Siemens’ collaboration with Infineon Technologies to develop next-generation secure controllers for smart factories. Other key players include Schneider Electric, Phoenix Contact, and Mitsubishi Electric, which collectively hold over 45% of the global market share.

MARKET DYNAMICS

MARKET DRIVERS

Growing Industrial IoT Adoption Accelerates Demand for Security Controllers

The rapid expansion of Industrial Internet of Things (IIoT) applications is fundamentally transforming manufacturing and industrial processes, creating unprecedented demand for robust security controllers. With industrial environments increasingly connecting equipment to networks for data monitoring and automation, the attack surface for cyber threats has expanded significantly. Industrial security controllers provide critical protection against unauthorized access, data breaches, and operational disruptions. Recent studies indicate that IIoT connections in manufacturing environments are growing at over 25% annually, directly correlating with increased security controller deployments. Modern industrial security controllers now incorporate advanced features like secure boot, cryptographic acceleration, and tamper detection to safeguard sensitive operational technology networks.

Stringent Industrial Cybersecurity Regulations Compel Technology Upgrades

Governments worldwide are implementing rigorous cybersecurity standards for critical infrastructure and industrial facilities, driving mandatory security controller adoption. Regulations such as the NIST Cybersecurity Framework in the U.S. and IEC 62443 standards internationally specify requirements for industrial control system protection that often necessitate embedded security controllers. Facilities handling sensitive operations face compliance deadlines that are accelerating technology refreshes, with recent estimates showing over 60% of industrial operators planning security infrastructure upgrades within two years. These regulatory pressures are particularly impactful in energy, utilities, and transportation sectors where security breaches could have catastrophic consequences.

➤ Recent legislation in multiple regions now mandates security-by-design principles for industrial equipment, requiring manufacturers to integrate security controllers at the hardware level rather than as afterthought add-ons.

Furthermore, the convergence of operational technology (OT) and information technology (IT) networks in industrial environments creates additional security complexities that specialized controllers are uniquely positioned to address, further propelling market growth.

MARKET CHALLENGES

Legacy System Integration Poses Significant Technical Hurdles

While industrial security controllers offer advanced protection capabilities, their implementation in existing facilities faces substantial technical challenges. Many industrial sites operate equipment with lifespans measured in decades, containing proprietary control systems that were never designed with modern security in mind. Retrofitting these environments with security controllers requires careful planning to avoid operational disruptions, with integration projects often taking 12-18 months for complex facilities. The specialized nature of industrial protocols like Modbus, Profibus, and DNP3 requires security controllers to incorporate protocol-specific protection mechanisms that maintain compatibility while adding security layers.

Other Challenges

Cost Sensitivity in Industrial Sectors

The capital-intensive nature of industrial operations creates intense pressure to minimize equipment costs. High-performance security controllers with advanced features can represent significant investments, particularly for small and medium manufacturers operating with tight margins. This financial reality leads many operators to delay security upgrades until absolutely necessary or opt for basic solutions that may not provide adequate protection.

Performance vs Security Trade-offs

Industrial processes often require deterministic, real-time operation where added security processing can introduce latency concerns. Engineering teams must carefully balance security measures with performance requirements, sometimes resulting in compromised protection to maintain operational efficiency. This challenge is particularly acute in high-speed manufacturing and process control applications where microseconds matter.

MARKET RESTRAINTS

Limited Cybersecurity Awareness Hinders Adoption in Traditional Industries

Despite growing threats, many industrial operators underestimate their vulnerability to cyber attacks, particularly in sectors that have traditionally been physically isolated. This complacency stems from outdated perceptions of industrial control systems being “air-gapped” when in reality, increasing connectivity has eliminated this separation. Surveys indicate that less than 40% of industrial companies have comprehensive cybersecurity training programs for operational staff, creating knowledge gaps that delay security investments. The situation is further complicated by organizational silos where IT and OT teams have different priorities and risk assessments regarding security controller implementations.

Additionally, the shortage of professionals with both industrial operations experience and cybersecurity expertise makes proper security controller selection and deployment challenging. Many organizations struggle to find personnel qualified to evaluate the increasingly sophisticated features offered by modern security controllers, from secure element integration to advanced anomaly detection capabilities.

MARKET OPPORTUNITIES

Emerging IIoT Security Standards Create New Implementation Opportunities

The development of specialized IIoT security frameworks presents significant growth potential for industrial security controller providers. New standards like ISA/IEC 62443 and industrial adaptations of NIST guidelines are driving requirements for hardware-based security in connected devices. This standards evolution creates opportunities for security controller vendors to develop tailored solutions for specific vertical applications, from smart manufacturing to critical infrastructure protection. The increasing integration of artificial intelligence capabilities into security controllers also allows for predictive threat detection that can command premium pricing in sensitive applications.

Furthermore, the rise of edge computing in industrial environments necessitates localized security processing that security controllers are ideally positioned to provide. As more analytics and control functions move to the network edge, the demand for compact, power-efficient security controllers with robust cryptographic capabilities is expected to grow substantially. Industry projections suggest edge security applications could represent over 30% of the industrial security controller market within five years as distributed architectures become mainstream.

INDUSTRIAL SECURITY CONTROLLER MARKET TRENDS

Industrial IoT (IIoT) Adoption Driving Demand for Secure Controllers

The rapid adoption of Industrial Internet of Things (IIoT) is transforming industrial automation, creating unprecedented demand for security controllers with advanced encryption and authentication capabilities. These controllers act as the first line of defense against cyber-physical threats in smart factories, with their market projected to grow at a CAGR of 8-10% through 2032. Modern industrial security controllers now integrate hardware-based secure boot mechanisms and tamper-resistant designs to withstand sophisticated attacks. The need for real-time threat detection has further accelerated the deployment of 32-bit security controllers, which accounted for over 60% of 2024 market revenue due to their superior processing power for cryptographic operations.

Other Trends

Convergence of Operational Technology (OT) and IT Security

As industrial networks increasingly connect with enterprise IT systems, security controllers are evolving to bridge the gap between OT reliability and IT cybersecurity standards. This convergence has led to innovations like Trusted Platform Modules (TPMs) embedded within industrial controllers, providing secure cryptographic key storage and hardware-based authentication. Major manufacturers are now offering controllers compliant with IEC 62443 standards, capable of detecting anomalous network traffic patterns in real-time while maintaining deterministic performance for critical control functions.

Smart Manufacturing Expansion Accelerating Market Growth

The global push toward Industry 4.0 implementations is creating significant opportunities in the factory automation segment, which currently represents approximately 45% of industrial security controller applications. Modern automotive production lines now deploy layered security architectures where controllers authenticate every connected device while enforcing role-based access controls. The AGV (Automated Guided Vehicle) sector is emerging as another high-growth area, with security controller shipments for mobile robotics expected to double by 2028 as warehouses implement fleet management systems requiring secure wireless communications.

COMPETITIVE LANDSCAPE

Key Industry Players

Industrial Security Vendors Accelerate Innovation to Meet Rising Demand for IoT and Automation Protection

The global industrial security controller market features a semi-consolidated competitive environment, with established industrial automation giants competing alongside specialized security solution providers. Infineon Technologies leads the market, commanding a significant revenue share due to its comprehensive security IC portfolio and robust presence across manufacturing hubs in Europe and Asia-Pacific.

Siemens and Schneider Electric have emerged as formidable competitors, leveraging their established industrial automation ecosystems to integrate security controllers into broader Industry 4.0 solutions. In 2024, these players collectively accounted for over 30% of the industrial security controller market through their embedded security offerings for smart factories and critical infrastructure.

Meanwhile, specialized players like Banner Engineering and SICK AG are gaining traction with application-specific security controllers for harsh industrial environments. Their focus on ruggedized designs (-40 to 105°C operating range) and compliance with industrial safety standards has positioned them strongly in material handling and automated guided vehicle (AGV) segments.

The competitive landscape continues to evolve with strategic movements – Phoenix Contact recently expanded its security controller line with IIoT-ready models, while Mitsubishi Electric has been investing heavily in cyber-physical system security through R&D partnerships. Such initiatives are expected to reshape market shares as industrial security becomes integral to modern automation architectures.

List of Key Industrial Security Controller Companies Profiled

- Infineon Technologies (Germany)

- Banner Engineering (U.S.)

- SICK AG (Germany)

- Schneider Electric (France)

- Siemens (Germany)

- Phoenix Contact (Germany)

- IDEC Corporation (Japan)

- Schmersal (Germany)

- Mitsubishi Electric (Japan)

Segment Analysis:

By Type

32-bit Security Controller Segment Dominates the Market Due to High Processing Power and Robust Security Features

The market is segmented based on type into:

- 32-bit Security Controller

- 16-bit Security Controller

- 8-bit Security Controller

- Others

By Application

IoT Applications Segment Leads Due to Growing Smart Device Integration and Connectivity Requirements

The market is segmented based on application into:

- IoT Applications

- AGV (Automated Guided Vehicles)

- Factory Automation

- Industrial Robotics

- Others

By End User

Manufacturing Sector Accounts for Largest Share Owing to Industry 4.0 Adoption

The market is segmented based on end user into:

- Manufacturing

- Energy and Utilities

- Transportation

- Healthcare

- Others

Regional Analysis: Industrial Security Controller Market

North America

The North American industrial security controller market is driven by robust industrial automation adoption, particularly in the manufacturing and critical infrastructure sectors. With the U.S. accounting for over 65% of regional revenue in 2024, the market benefits from stringent cybersecurity regulations like NIST SP 800-82 for industrial control systems. Major players like Infineon Technologies and Siemens dominate through innovative IoT-enabled controller solutions, while growing investments in smart manufacturing initiatives propel demand for 32-bit security controllers, expected to grow at a CAGR of 7.2% through 2032. However, high implementation costs and skilled labor shortages remain key challenges.

Europe

Europe’s market is characterized by strict IEC 62443 compliance standards and rapid Industry 4.0 adoption, with Germany and France leading deployments. The region emphasizes cyber-physical system security, driving demand for controllers with advanced encryption and real-time monitoring. Schneider Electric and Phoenix Contact hold significant market shares, particularly in factory automation applications, which account for 42% of regional sales. While western Europe shows maturity, eastern European nations exhibit growth potential due to increasing foreign direct investments in manufacturing. The EU’s Cybersecurity Act further accelerates market expansion.

Asia-Pacific

APAC is the fastest-growing region, projected to expand at a 9.1% CAGR through 2032, led by China’s “Made in China 2025” initiative and India’s smart cities mission. Japan and South Korea contribute through high-tech manufacturing demands, while Southeast Asia benefits from low-cost production shifts. Though 16-bit controllers dominate price-sensitive markets, rising awareness about industrial cybersecurity is boosting premium product adoption. Challenges include fragmented regulatory frameworks and intellectual property concerns, particularly in emerging economies.

South America

The region shows moderate growth, with Brazil’s oil & gas sector driving 53% of industrial security controller demand. Economic instability and currency fluctuations hinder large-scale deployments, but Mitsubishi Electric and local players are capitalizing on mining and energy applications. Chile and Colombia exhibit potential with infrastructure modernization projects, though market penetration remains low due to limited cybersecurity expertise and budget constraints in small-to-medium enterprises.

Middle East & Africa

MEA’s market is bifurcated—Gulf nations prioritize critical infrastructure protection (especially in oil refineries and power plants) with high-end security controllers, while Africa lags due to limited industrialization. The UAE and Saudi Arabia account for 68% of regional revenue, investing heavily in smart city projects. However, the lack of localized technical support and reliance on imports restrict growth in secondary markets.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Industrial Security Controller markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Industrial Security Controller market was valued at US$ 892 million in 2024 and is projected to reach US$ 1,520 million by 2032, growing at a CAGR of 7.9% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (32-bit and 16-bit Security Controllers), application (IoT, AGV, Factory Automation), and end-user industry to identify high-growth segments. The 32-bit segment is expected to dominate with over 65% market share by 2032.

- Regional Outlook: Insights into market performance across North America (estimated at USD 420 million in 2024), Europe, Asia-Pacific (China projected at USD 580 million by 2032), Latin America, and Middle East & Africa.

- Competitive Landscape: Profiles of leading market participants including Infineon Technologies, Siemens, Schneider Electric, and Mitsubishi Electric, which collectively held 48% market share in 2024.

- Technology Trends & Innovation: Assessment of AI integration, industrial IoT security solutions, and temperature-resistant designs (-40 to 105°C operational range).

- Market Drivers & Restraints: Evaluation of factors including Industry 4.0 adoption and cybersecurity concerns versus supply chain challenges and high implementation costs.

- Stakeholder Analysis: Strategic insights for component suppliers, system integrators, and industrial automation providers regarding emerging opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial Security Controller Market?

-> Industrial Security Controller Market size was valued at US$ 892 million in 2024 and is projected to reach US$ 1,520 million by 2032, at a CAGR of 7.9% during the forecast period 2025-2032.

Which key companies operate in Global Industrial Security Controller Market?

-> Key players include Infineon Technologies, Siemens, Schneider Electric, Mitsubishi Electric, SICK AG, and Phoenix Contact, among others.

What are the key growth drivers?

-> Key growth drivers include Industry 4.0 adoption, increasing cybersecurity threats, and demand for ruggedized industrial controllers.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing market, while North America maintains technological leadership with 34% market share in 2024.

What are the emerging trends?

-> Emerging trends include AI-powered security controllers, edge computing integration, and modular security solutions for industrial IoT.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...