MARKET INSIGHTS

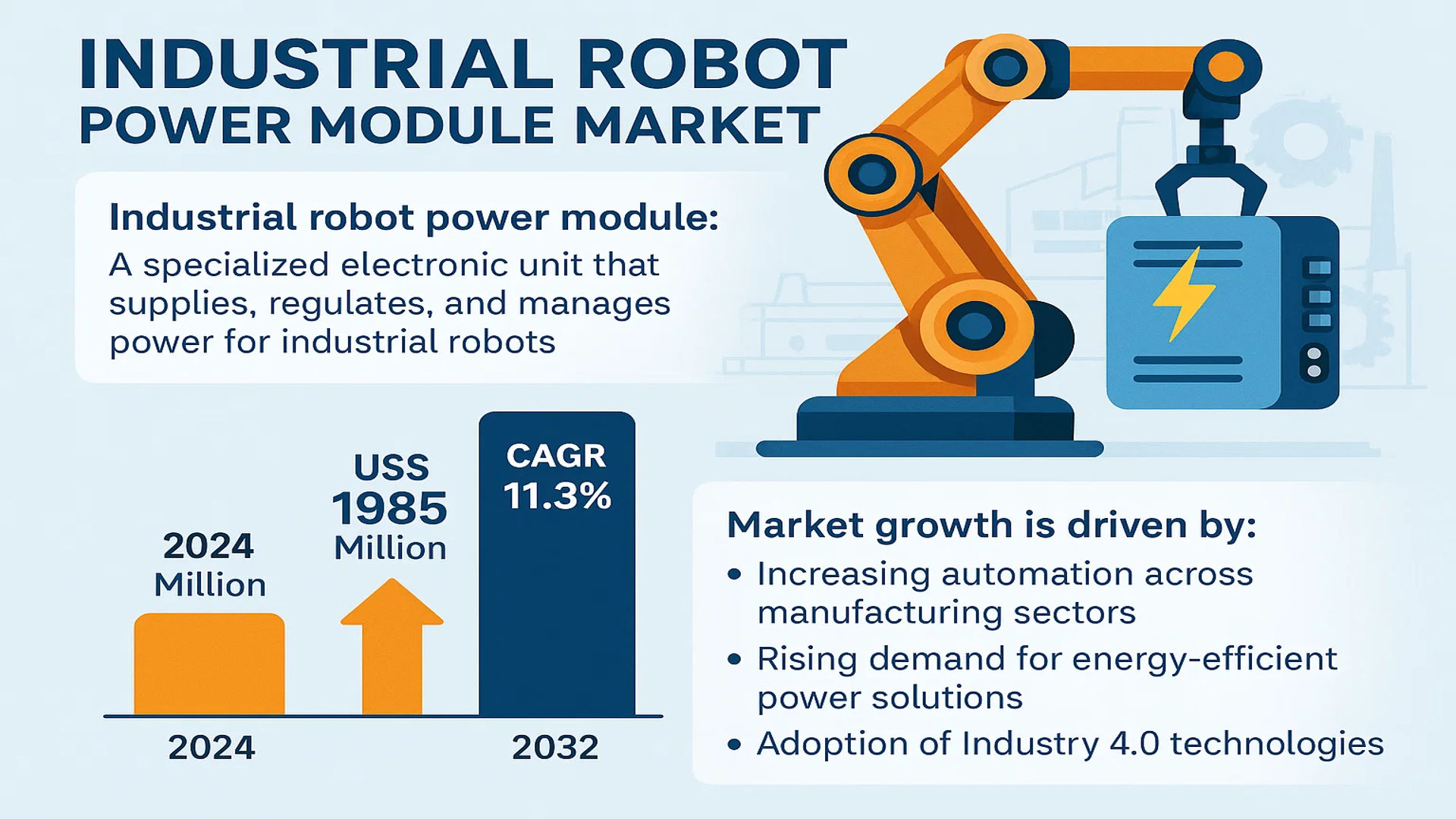

The global Industrial Robot Power Module Market was valued at 1004 million in 2024 and is projected to reach US$ 1985 million by 2032, at a CAGR of 11.3% during the forecast period.

An industrial robot power module is a specialized electronic unit designed to supply, regulate, and manage power for industrial robots operating in automated manufacturing and industrial environments. These modules ensure stable and efficient power distribution to support robotic movements, control systems, sensors, and communication modules, which are critical for high-precision applications in industries such as automotive, electronics, and logistics.

The market growth is driven by increasing automation across manufacturing sectors, rising demand for energy-efficient power solutions, and the adoption of Industry 4.0 technologies. Key players such as Yaskawa, Vicor, and TDK-Lambda are actively investing in R&D to enhance power module efficiency and reliability. For instance, in 2023, Yaskawa introduced a new generation of high-performance power modules with advanced thermal management, catering to heavy-duty robotic applications. While the AC input segment currently dominates the market, the DC input segment is expected to witness accelerated growth due to its compatibility with renewable energy systems.

MARKET DYNAMICS

MARKET DRIVERS

Rising Automation in Manufacturing to Accelerate Market Expansion

The global industrial landscape is witnessing unprecedented growth in automation adoption, with manufacturing facilities increasingly integrating robotic systems to enhance productivity. Industrial robot power modules serve as the backbone of these systems, ensuring reliable power distribution for precision movements and control functions. The automotive sector alone accounted for over 30% of industrial robot installations last year, driving significant demand for high-performance power modules. As factories modernize production lines to meet Industry 4.0 standards, the need for robust power management solutions becomes critical, propelling market growth.

Technological Advancements in Power Electronics to Fuel Innovation

Continuous improvements in power semiconductor technologies are revolutionizing industrial robot power modules. Wide-bandgap materials like silicon carbide (SiC) and gallium nitride (GaN) enable higher efficiency, reduced thermal losses, and compact designs. Manufacturers are developing modules that operate at frequencies above 20kHz while maintaining 98% efficiency ratings. For instance, recent product launches feature intelligent thermal management systems that automatically regulate power flow based on real-time robot performance data. These innovations allow industrial robots to operate with greater precision and energy efficiency, directly supporting market expansion.

Furthermore, the integration of IoT capabilities in power modules creates new value propositions:

➤ Modern power modules now incorporate predictive maintenance features that can anticipate component failures up to 500 operating hours in advance, reducing unplanned downtime by approximately 45% across industrial applications.

MARKET RESTRAINTS

Complex Integration Requirements to Hinder Market Penetration

While industrial robot power modules offer significant benefits, their integration into existing automation systems presents substantial challenges. Many manufacturing facilities still operate legacy equipment that lacks standardized interfaces for modern power solutions. Retrofitting outdated systems requires extensive modifications that can increase total implementation costs by 25-40%. Additionally, synchronization issues between new power modules and older control architectures frequently lead to compatibility problems, forcing operators to make costly compromises in system performance.

Other Critical Constraints

Supply Chain Vulnerabilities

The global semiconductor shortage continues to impact power module production, with lead times for key components extending beyond 52 weeks in some cases. This supply-demand imbalance forces manufacturers to either delay deliveries or accept higher input costs that ultimately get passed to end-users.

Regulatory Compliance Burdens

Evolving safety standards for industrial equipment impose rigorous testing requirements on power modules. Meeting IEC 61800-5-1 and UL 1740 certifications adds approximately 18-24 months to product development cycles while increasing compliance costs by an average of 15% per unit.

MARKET OPPORTUNITIES

Emerging Applications in Collaborative Robotics to Create New Growth Avenues

The rapid adoption of cobots (collaborative robots) across small and medium enterprises presents significant opportunities for power module manufacturers. Unlike traditional industrial robots, cobots require ultra-compact power solutions with enhanced safety features. The cobot market is projected to maintain a 35% annual growth rate, driving demand for specialized power modules that combine low-voltage operation with advanced touch-protection mechanisms. Leading manufacturers are already developing 48V DC input modules specifically optimized for cobot applications, reducing energy consumption while meeting stringent human-machine interaction standards.

Additionally, the renewable energy sector offers promising expansion potential:

Solar panel and wind turbine manufacturers increasingly utilize robotic systems for installation and maintenance operations in harsh environmental conditions. This trend creates demand for ruggedized power modules capable of operating reliably across temperature extremes from -40°C to 85°C while withstanding vibration levels exceeding 5Grms. Market players that can deliver these specialized solutions stand to capture substantial growth in emerging industrial segments.

MARKET CHALLENGES

Thermal Management Complexities to Strain Development Resources

Industrial robot power modules face persistent challenges in heat dissipation, particularly as power densities continue increasing. Contemporary modules must handle current loads exceeding 500A while maintaining junction temperatures below 150°C – a technical feat that requires advanced cooling solutions. Liquid cooling systems add approximately 30% to module costs while introducing potential leak points, whereas air-cooled designs struggle with space constraints in compact robotic joints. These thermal limitations currently restrict maximum continuous operating periods for high-payload robots to under 12 hours before requiring cooldown intervals.

Other Pressing Challenges

Cybersecurity Vulnerabilities

The growing connectivity of power modules exposes industrial robots to potential cyber threats. Recent vulnerability assessments revealed that nearly 65% of networked power components lacked basic encryption protocols, creating entry points for malicious actors seeking to disrupt manufacturing operations.

Technical Skills Gap

The specialized nature of robotic power systems has created a shortage of qualified technicians. Industry surveys indicate that 43% of manufacturing facilities delay robotic deployments due to insufficient in-house expertise for power module maintenance and troubleshooting.

INDUSTRIAL ROBOT POWER MODULE MARKET TRENDS

Rise of Smart Manufacturing and Industry 4.0 to Drive Market Expansion

The global industrial robot power module market is experiencing substantial growth, driven by the rapid adoption of smart manufacturing and Industry 4.0 technologies. Industrial robots are now integral to automation, with power modules playing a critical role in ensuring efficient energy distribution and operational stability. The rise of collaborative robots (cobots) and AI-driven automation systems has further amplified demand, with manufacturers increasingly investing in high-performance power modules to enhance robot efficiency. The market is projected to grow at a compound annual growth rate (CAGR) of 11.3%, reaching US$ 1,985 million by 2032. This growth is supported by increasing demand in automotive, electronics, and logistics sectors, where precision and energy efficiency are paramount.

Other Trends

Growing Demand for Energy-Efficient Solutions

Energy efficiency has become a priority in industrial automation, with companies seeking power modules that minimize energy consumption and heat dissipation. Innovations in wide-bandgap semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), are transforming power module designs, enabling higher efficiency and reduced power losses. Leading manufacturers like Yaskawa and Vicor are investing heavily in these technologies, contributing to market expansion. Additionally, regulatory pressures to reduce carbon footprints are pushing industries toward adopting sustainable power management solutions.

Expansion in Robotics Across Emerging Economies

Emerging economies, particularly in Asia-Pacific, are witnessing accelerated adoption of industrial robots due to rising labor costs and government incentives for automation. China, for instance, aims to become a global robotics leader, with investments exceeding US$ 2 billion annually in robotic infrastructure. The AC input segment is projected to grow significantly, catering to industrial applications requiring stable power supply for high-performance robotic arms and SCARA robots. Meanwhile, North America and Europe remain key markets, with the U.S. contributing heavily due to its advanced manufacturing and automotive industries. Competitive pricing and technological innovation among key players like NACT and TDK-Lambda will further influence market dynamics.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in Industrial Robot Power Module Market

The global industrial robot power module market exhibits a semi-consolidated structure, with a mix of established multinationals and emerging regional players competing for market share. Yaskawa Electric Corporation (Japan) leads the segment with its comprehensive power solutions portfolio, capturing over 18% revenue share in 2024. Their dominance stems from proprietary servo drive technologies and strategic partnerships with automotive manufacturers across Europe and North America.

Meanwhile, Vicor Corporation (U.S.) and TDK-Lambda (Japan) have significantly strengthened their positions through high-efficiency DC-DC converter modules specifically designed for collaborative robots. Both companies reported 22% year-on-year growth in power module revenues during 2023, outpacing market averages.

The competitive intensity is further amplified by Chinese manufacturers like Shenzhen Jichuang Robot Technology, which commanded 12% of the APAC market in 2024. Their cost-competitive solutions for SCARA robots have enabled rapid penetration in electronics manufacturing applications.

Recent developments show leading players prioritizing three key strategies:

- Vertical integration with robot OEMs to develop application-specific power solutions

- R&D investments in wide-bandgap semiconductors (GaN/SiC) for higher energy efficiency

- Modular designs that simplify maintenance in harsh industrial environments

Europe’s competitive dynamics are particularly noteworthy, where companies like RRC Power Solutions (Germany) have gained traction by complying with stringent CE directives while maintaining power density advantages over Asian imports.

List of Key Industrial Robot Power Module Manufacturers

- Yaskawa Electric Corporation (Japan)

- Vicor Corporation (U.S.)

- TDK-Lambda Corporation (Japan)

- NACT Corporation (U.S.)

- RoboMaster Technologies (China)

- RRC POWER SOLUTIONS GmbH (Germany)

- Lead-Win Technology Co., Ltd. (Taiwan)

- Shenzhen Jichuang Robot Technology Co., Ltd (China)

- Delta Electronics (Taiwan)

Segment Analysis:

By Type

AC Input Segment Dominates Due to Higher Compatibility with Industrial Power Grids

The market is segmented based on type into:

- AC Input

- DC Input

By Application

Multi-axis Robots Segment Leads Owing to Complex Power Requirements in Advanced Automation

The market is segmented based on application into:

- Multi-axis Robots

- SCARA Robots

- Others

By Voltage Range

High Voltage Modules Dominate for Heavy Industrial Applications

The market is segmented based on voltage range into:

- Low Voltage (Below 24V)

- Medium Voltage (24V-48V)

- High Voltage (Above 48V)

By End-Use Industry

Automotive Sector Remains Primary Consumer of Industrial Robot Power Modules

The market is segmented based on end-use industry into:

- Automotive

- Electronics & Electrical

- Metal & Machinery

- Food & Beverage

- Pharmaceutical

- Others

Regional Analysis: Industrial Robot Power Module Market

Asia-Pacific

The Asia-Pacific region dominates the global industrial robot power module market, accounting for the largest revenue share in 2024. This is primarily driven by China’s aggressive automation push, where government initiatives like “Made in China 2025” are accelerating smart manufacturing investments. Japan continues to lead in technological innovation, with companies like Yaskawa and Fanuc developing high-efficiency power modules for precision robotics. South Korea’s thriving electronics manufacturing sector produces strong demand for SCARA robot power solutions. While cost sensitivity remains a factor, there is a clear trend toward energy-efficient AC input modules as regional manufacturers prioritize sustainability. The market benefits from robust supply chains and increasing adoption of collaborative robots (cobots) across industries.

North America

North America represents a high-value market for industrial robot power modules, particularly in the U.S., where automotive and aerospace industries demand reliable power solutions for multi-axis robots. Strict safety standards and the need for precision drive adoption of advanced DC input modules with overload protection features. The region shows increasing preference for modular power systems that simplify maintenance, reflecting the shift toward Industry 4.0. Key players like Vicor and TDK-Lambda have strengthened their foothold through partnerships with automation solution providers. Though labor costs influence adoption rates, reshoring initiatives and federal incentives for advanced manufacturing are creating new growth opportunities.

Europe

Europe’s market growth stems from stringent industrial safety regulations and the rapid digital transformation of manufacturing. Germany, as the region’s industrial hub, leads in deploying power modules for heavy-duty robotic applications in automotive production lines. The EU’s focus on energy efficiency has accelerated R&D in low-loss power conversion technologies. While the market faces pricing pressures from Asian competitors, European manufacturers differentiate through customized solutions for niche applications like pharmaceutical robotics. The UK and France are seeing increased investments in automated logistics, driving demand for compact power modules with integrated cooling systems.

South America

South America presents emerging opportunities, particularly in Brazil’s automotive sector and Chile’s mining industry, where robotic automation is gradually being adopted. The market suffers from infrastructure limitations and economic instability, leading to preference for cost-effective refurbished power modules in some cases. However, multinational manufacturers are establishing local service centers to support the growing installed base of industrial robots. The lack of standardized power infrastructure across countries remains a challenge, requiring adaptable module designs that can handle varying voltage conditions.

Middle East & Africa

This region shows promising growth potential, particularly in UAE and Saudi Arabia, where smart factory initiatives are gaining momentum. The oil & gas industry’s automation drives specialized demand for ruggedized power modules capable of operating in extreme environments. While market penetration remains low compared to other regions, increasing government support for industrial diversification is creating new opportunities. South Africa serves as a gateway for technology transfers, though adoption is constrained by skills shortages and reliance on imported components. The market is expected to see gradual expansion as regional manufacturers prioritize productivity enhancement.

Report Scope

This market research report provides a comprehensive analysis of the Global Industrial Robot Power Module market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 1,004 million in 2024 and is projected to reach USD 1,985 million by 2032 at a CAGR of 11.3%.

- Segmentation Analysis: Detailed breakdown by product type (AC Input, DC Input), application (Multi-axis Robots, SCARA Robots, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies in power management, energy efficiency improvements, and integration with smart manufacturing systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as industrial automation adoption along with challenges like supply chain constraints and regulatory compliance.

- Stakeholder Analysis: Insights for robot manufacturers, component suppliers, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial Robot Power Module Market?

-> Industrial Robot Power Module Market was valued at 1004 million in 2024 and is projected to reach US$ 1985 million by 2032, at a CAGR of 11.3% during the forecast period.

Which key companies operate in Global Industrial Robot Power Module Market?

-> Key players include Yaskawa, NACT, RoboMaster, Vicor, RRC POWER SOLUTIONS COMPANY LIMITED, TDK-Lambda, Lead-Win, and Shenzhen Jichuang Robot Technology Co., Ltd.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for energy-efficient power solutions, and expansion of smart manufacturing facilities.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by China, Japan, and South Korea’s robust manufacturing sectors, while North America shows strong growth potential.

What are the emerging trends?

-> Emerging trends include modular power solutions, integration of AI for predictive maintenance, and development of high-efficiency power modules for next-generation industrial robots.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...