MARKET INSIGHTS

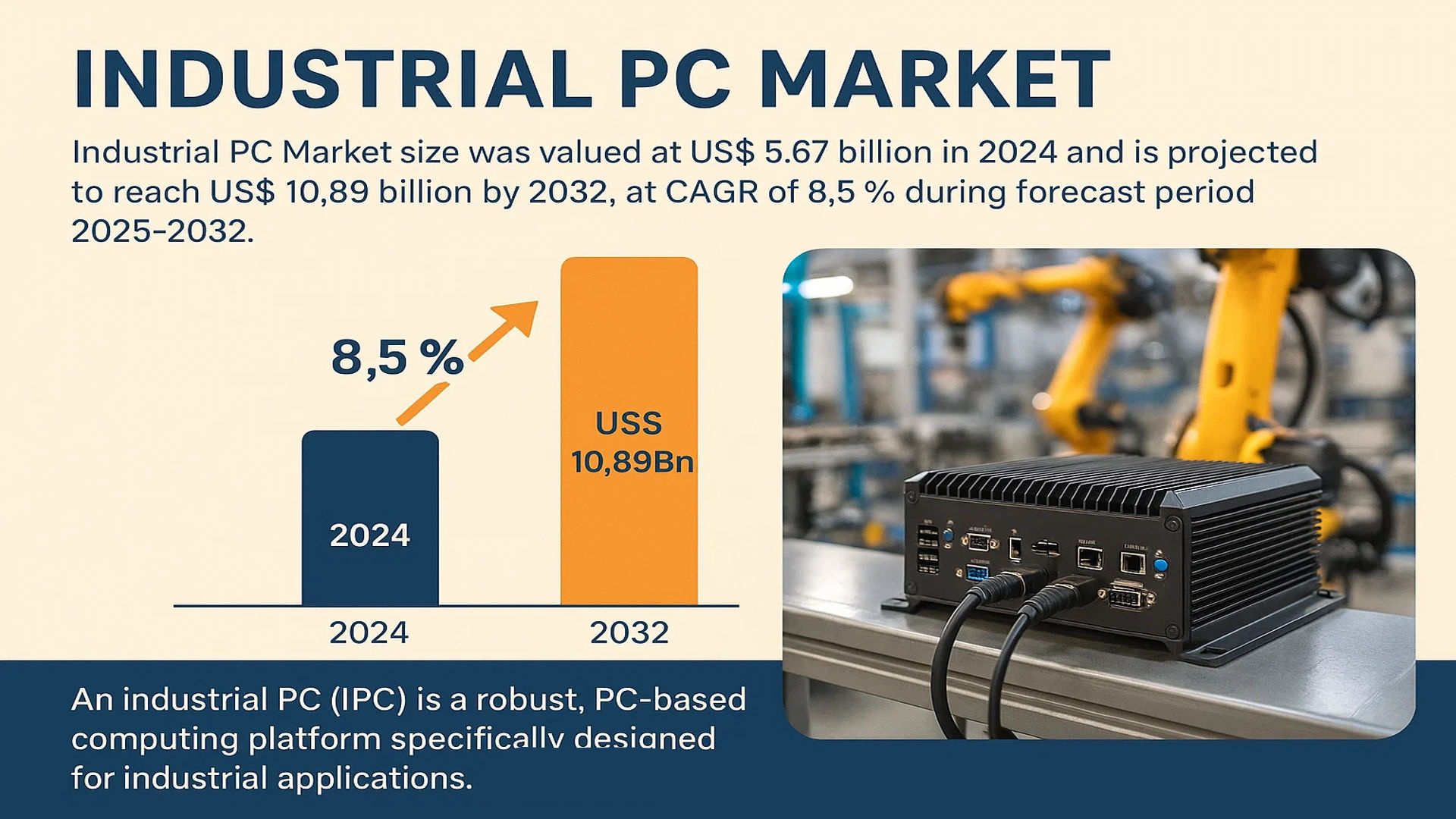

The global Industrial PC Market size was valued at US$ 5.67 billion in 2024 and is projected to reach US$ 10.89 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032.

An Industrial PC (IPC) is a robust, PC-based computing platform specifically engineered for industrial applications. These systems are designed to operate reliably in harsh environments characterized by extreme temperatures, dust, moisture, and electromagnetic interference. They are integral to automation processes, providing the computational power for tasks such as machine control, data acquisition, and human-machine interface (HMI) operations across various sectors.

The market is experiencing significant growth driven by the accelerating adoption of Industry 4.0 and smart manufacturing initiatives, which demand robust computing at the edge. Furthermore, the expansion of automation in sectors like automotive and pharmaceuticals, coupled with the increasing need for real-time data processing and IoT integration, is fueling demand. The competitive landscape is concentrated, with the top three players in China—Advantech, Adlinktech, and Siemens—collectively holding approximately 31% of the market share, underscoring the presence of established, dominant players driving innovation and market consolidation.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Industry 4.0 Adoption to Drive Industrial PC Demand

The global push towards Industry 4.0 and smart manufacturing is significantly driving the industrial PC market. Industrial PCs serve as the computational backbone for automated systems, enabling real-time data processing, machine-to-machine communication, and advanced analytics in manufacturing environments. The manufacturing sector’s digital transformation investments are projected to grow substantially, with smart factory initiatives accounting for over 35% of all manufacturing technology spending by 2025. These systems require robust computing platforms that can withstand harsh industrial environments while processing massive data streams from IoT sensors, vision systems, and robotic controllers. The integration of artificial intelligence and machine learning capabilities into production lines further amplifies the need for high-performance industrial computing solutions that can operate reliably in temperature extremes, vibration-intensive settings, and contaminated atmospheres where commercial computers would fail.

Expanding Automation Across Verticals to Boost Market Growth

Industrial automation is expanding beyond traditional manufacturing into sectors such as energy, pharmaceuticals, and transportation, creating substantial growth opportunities for industrial PCs. The energy sector’s digital transformation is particularly noteworthy, with smart grid implementations requiring industrial-grade computing solutions for substation automation, distribution management, and renewable energy integration. In pharmaceutical manufacturing, stringent regulatory requirements are driving adoption of computerized systems for process validation and quality control, where industrial PCs provide the necessary reliability and compliance documentation capabilities. The automotive industry’s transition to electric vehicle production has also created new demand for industrial computing solutions that can monitor and control specialized manufacturing processes with extreme precision and reliability.

Furthermore, the increasing need for remote monitoring and predictive maintenance capabilities is accelerating industrial PC adoption. Modern industrial PCs equipped with IoT connectivity enable manufacturers to monitor equipment health, predict maintenance needs, and optimize production schedules from centralized control rooms or even mobile devices. This capability reduces downtime, improves operational efficiency, and enhances overall equipment effectiveness metrics.

➤ For instance, major automotive manufacturers have reported up to 40% reduction in unplanned downtime through implementation of industrial PC-based predictive maintenance systems.

The convergence of operational technology and information technology networks is creating additional demand for industrial PCs that can bridge these traditionally separate domains securely and efficiently.

MARKET CHALLENGES

High Initial Investment and Total Cost of Ownership Present Significant Challenges

While industrial PCs offer substantial operational benefits, their high initial cost and total ownership expenses present significant market challenges. Industrial-grade computing solutions typically cost 2-3 times more than commercial equivalents due to their ruggedized designs, extended temperature range components, and enhanced reliability features. This cost differential becomes particularly challenging for small and medium-sized enterprises with limited capital budgets. The specialized components required for industrial environments, such as wide-temperature-range memory, industrial-grade storage, and protective enclosures, contribute to these higher costs. Additionally, the certification processes for hazardous environments and compliance with industry-specific standards further increase development and manufacturing expenses.

Other Challenges

Cybersecurity Vulnerabilities

Industrial PCs face increasing cybersecurity threats as they become more connected to enterprise networks and the internet. The convergence of IT and OT networks has exposed industrial control systems to cyber attacks that could disrupt critical operations. Protecting these systems requires specialized security measures that don’t interfere with real-time operations, creating complex implementation challenges. The average cost of industrial cybersecurity incidents has been increasing annually, with manufacturing facilities experiencing significant financial impacts from production disruptions.

Rapid Technological Obsolescence

The fast pace of technological change creates obsolescence challenges for industrial PC deployments. Industrial systems typically have longer lifecycles than commercial IT equipment, often remaining in operation for 7-10 years. This creates compatibility issues when integrating new industrial PCs with legacy machinery and control systems. The need to maintain long-term support for older operating systems and applications while adopting new technologies presents significant technical and financial challenges for end-users.

MARKET RESTRAINTS

Supply Chain Constraints and Component Shortages to Limit Market Growth

The industrial PC market faces significant restraints from ongoing supply chain disruptions and component shortages. The global semiconductor shortage has particularly impacted industrial computing manufacturers, who require specialized components with extended temperature ranges and extended life availability. Industrial PC manufacturers typically need guaranteed component availability for 5-7 years to support their product lifecycles, which conflicts with the rapid innovation cycles of commercial semiconductor manufacturers. This mismatch creates production challenges and extended lead times that can delay industrial automation projects. The average lead time for industrial PCs increased by approximately 40% during recent supply chain disruptions, affecting project timelines across multiple industries.

Additionally, the concentration of semiconductor manufacturing in specific geographic regions creates vulnerability to geopolitical tensions and trade restrictions. Industrial PC manufacturers are facing increased pressure to diversify their supply chains and develop alternative sourcing strategies, which involves significant additional costs and qualification processes. These challenges are particularly acute for military and aerospace applications where component traceability and domestic sourcing requirements further constrain available supply options.

MARKET OPPORTUNITIES

Emerging Edge Computing Applications to Create New Growth Opportunities

The rapid growth of edge computing in industrial environments presents substantial opportunities for industrial PC manufacturers. As manufacturers deploy more IoT sensors and connected devices, they require local computing power at the network edge to process data in real-time before sending it to cloud or central systems. Industrial PCs are ideally positioned to serve as edge computing nodes due to their ruggedness, reliability, and ability to operate in harsh environments. The edge computing market in industrial settings is projected to grow at a compound annual growth rate exceeding 25% over the next five years, driven by requirements for low-latency processing, bandwidth optimization, and data sovereignty concerns.

Advanced applications such as real-time quality inspection using machine vision, predictive maintenance through vibration analysis, and autonomous material handling systems all require substantial local computing power that industrial PCs can provide. The integration of GPU acceleration for AI inference at the edge is creating additional opportunities for high-performance industrial computing solutions. Manufacturers are increasingly looking for industrial PCs that can run complex machine learning models directly on the factory floor without relying on cloud connectivity, enabling faster response times and improved operational reliability.

Furthermore, the transition to 5G connectivity in industrial environments is enabling new applications that require the computing power and reliability of industrial PCs. Private 5G networks in manufacturing facilities allow for unprecedented mobility and connectivity, but they also require robust computing infrastructure at the edge to manage network functions and process the increased data flow effectively.

INDUSTRIAL PC MARKET TRENDS

Integration of IoT and Industry 4.0 to Emerge as a Dominant Trend in the Market

The proliferation of Industry 4.0 and the Industrial Internet of Things (IIoT) is fundamentally reshaping manufacturing and industrial processes, creating unprecedented demand for robust computing solutions. Industrial PCs serve as the central nervous system of smart factories, facilitating real-time data acquisition, processing, and communication between machinery, sensors, and control systems. This connectivity enables predictive maintenance, which can reduce machine downtime by up to 50% and lower maintenance costs by nearly 30%, driving significant operational efficiency. Furthermore, the need for edge computing capabilities is accelerating, as data processing at the source reduces latency and bandwidth usage. Modern IPCs are increasingly equipped with advanced features like AI co-processors and enhanced cybersecurity protocols to manage the vast data streams generated by connected devices, making them indispensable in the automated, data-driven industrial landscape.

Other Trends

Rising Demand for Ruggedized and Fanless Systems

There is a growing emphasis on durability and reliability in harsh industrial environments, leading to increased adoption of ruggedized and fanless Industrial PCs. These systems are designed to operate flawlessly in extreme conditions involving dust, moisture, vibration, and wide temperature ranges, which are common in sectors like oil & gas, mining, and heavy machinery. The elimination of moving parts, such as fans, significantly enhances mean time between failures (MTBF), a critical metric for continuous operations. This trend is particularly strong in the Asia-Pacific region, which accounts for over 45% of global manufacturing output, where the need for uninterrupted production lines is paramount. Manufacturers are responding by innovating with solid-state cooling solutions and robust enclosures that meet international protection standards, ensuring long-term operational integrity.

Expansion in Automation Across Diverse Sectors

Beyond traditional manufacturing, automation is penetrating a wider array of industries, each with unique demands for industrial computing. The automotive sector utilizes IPCs for robotic assembly lines and automated quality control, while the pharmaceutical industry employs them in precision filling and packaging machines that require sterile, compliant operations. This sectoral expansion is a primary growth driver. Additionally, the energy and power sector is integrating IPCs into smart grid management systems to enhance distribution efficiency and monitor renewable energy sources. This broadening application scope necessitates specialized IPC form factors, from compact panel PCs for human-machine interfaces (HMIs) in tight spaces to powerful rackmount systems for data-intensive control rooms, fueling innovation and market diversification.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Ruggedization and IoT Integration to Maintain Market Leadership

The global Industrial PC market exhibits a semi-consolidated competitive structure, featuring a mix of multinational technology conglomerates, specialized industrial automation providers, and emerging regional players. Advantech Co., Ltd. stands as a dominant force, commanding a significant portion of the market share. This leadership is largely due to its extensive and diverse product portfolio, which spans panel, rackmount, and box IPCs tailored for harsh environments, and its formidable global distribution network across key industrial regions in Asia, North America, and Europe.

Siemens AG and Beckhoff Automation (represented by B&R Automation, a part of the ABB Group) also hold substantial market positions. Siemens leverages its deep integration capabilities within its own Totally Integrated Automation (TIA) ecosystem, making its IPCs a preferred choice for large-scale manufacturing and process automation projects. Beckhoff, renowned for its PC-based control technology, continues to grow its share through innovation in high-performance, software-centric control solutions.

These established players are aggressively pursuing growth through strategic initiatives. This includes geographical expansion into high-growth emerging markets, continuous investment in research and development for next-generation IPCs with enhanced computing power and connectivity for Industry 4.0, and a stream of new product launches featuring improved ruggedization, wider operating temperature ranges, and support for IoT protocols.

Meanwhile, other key participants like AAEON Technology Inc. and Adlink Technology Inc. are strengthening their competitive stance. They are focusing on niche applications, forming strategic partnerships with software and sensor companies, and expanding their offerings in edge computing and AI-enabled industrial computers to capture new growth avenues and ensure their relevance in an evolving technological landscape.

List of Key Industrial PC Companies Profiled

- Advantech Co., Ltd. (Taiwan)

- Siemens AG (Germany)

- Adlink Technology Inc. (Taiwan)

- Shenzhen EVOC Intelligent Technology Co., Ltd. (China)

- Norco, Inc. (U.S.)

- Contec, Inc. (Japan)

- Anovo International Co., Limited (China)

- AAEON Technology Inc. (Taiwan)

- Axiomtek Co., Ltd. (Taiwan)

- B&R Automation (ABB Group) (Austria)

Segment Analysis:

By Type

Panel IPC Segment Dominates the Market Due to its Intuitive HMI and Space-Efficient Design

The market is segmented based on type into:

- Panel IPC

- Rackmount IPC

- Box IPC

- Embedded IPC

- DIN Rail IPC

- Others

By Application

Automotive Segment Leads Due to High Adoption in Automated Manufacturing and Quality Control

The market is segmented based on application into:

- Energy & Power

- Oil & Gas

- Chemical

- Pharmaceutical

- Automotive

- Aerospace & Defense

- Others

By Form Factor

Ruggedized Segment Leads Due to Critical Need for Reliability in Harsh Industrial Environments

The market is segmented based on form factor into:

- Ruggedized

- Fanless

- Waterproof & Dustproof

- Extreme Temperature

By Sales Channel

Direct Sales Segment Leads Due to Customization Requirements and Long-Term OEM Relationships

The market is segmented based on sales channel into:

- Direct Sales

- Distributors & Value-Added Resellers

- System Integrators

- Online Retail

Regional Analysis: Industrial PC Market

Asia-Pacific

The Asia-Pacific region dominates the global Industrial PC market, accounting for approximately 45% of total revenue in 2024. This leadership position is driven by massive manufacturing infrastructure, rapid industrialization, and significant government initiatives like China’s “Made in China 2025” and India’s “Make in India” programs. China alone represents over 60% of the regional market, with key manufacturers including Advantech, Adlinktech, and EVOC. The region’s growth is further accelerated by extensive adoption in automotive manufacturing, electronics production, and energy sectors. While cost-competitive solutions remain popular, there is increasing demand for high-reliability IPCs capable of operating in harsh environments, supported by growing investments in factory automation and smart manufacturing technologies.

North America

North America represents a mature yet steadily growing market for Industrial PCs, characterized by high adoption of advanced automation technologies and stringent quality standards. The region benefits from strong manufacturing revitalization efforts, particularly in the United States where reshoring initiatives and investments in advanced manufacturing are driving demand. Key applications include aerospace & defense, pharmaceutical manufacturing, and energy sectors where ruggedized, high-performance IPCs are essential. The market is distinguished by preference for premium products with advanced features such as enhanced cybersecurity, longer product lifecycles, and compliance with strict industry standards. Major players like Siemens and Rockwell Automation maintain significant presence, while the growing emphasis on Industry 4.0 and IoT integration continues to fuel market expansion.

Europe

Europe maintains a sophisticated Industrial PC market driven by strong manufacturing heritage, particularly in Germany’s automotive sector and the region’s leadership in industrial automation. The market is characterized by high demand for precision-engineered IPCs that meet rigorous EU standards for safety, energy efficiency, and environmental compliance. Germany accounts for the largest share within the region, supported by its robust manufacturing base and leadership in Industrie 4.0 initiatives. The European market shows particular strength in pharmaceutical applications where validation and compliance requirements drive demand for specialized IPCs. While growth is steady, the market faces pressure from cost competition and the need for continuous innovation to maintain technological leadership in increasingly automated manufacturing environments.

South America

The South American Industrial PC market is emerging, with growth primarily driven by Brazil’s manufacturing sector and increasing investments in industrial automation across the region. The market remains price-sensitive, with cost-effective solutions preferred over high-end configurations. Growth opportunities exist in mining, oil & gas, and food processing industries where basic automation needs are expanding. However, market development is constrained by economic volatility, limited local manufacturing capabilities, and infrastructure challenges. Most IPCs are imported from international suppliers, though local system integrators play a crucial role in adapting solutions to regional requirements. The market shows potential for growth as industrial modernization efforts gain momentum, particularly in countries with stable economic conditions.

Middle East & Africa

The Middle East & Africa region presents a developing market for Industrial PCs, characterized by uneven adoption across different countries and industries. The GCC countries, particularly Saudi Arabia and the UAE, show the strongest demand driven by oil & gas applications and infrastructure development projects. South Africa represents the most mature market in sub-Saharan Africa, with established manufacturing and mining sectors requiring industrial computing solutions. The region’s growth is hampered by limited industrial diversification, reliance on imports, and infrastructure challenges. However, increasing investments in smart city projects, industrial diversification initiatives, and energy sector modernization are creating new opportunities for IPC adoption, particularly in ruggedized and environmentally hardened configurations suitable for the region’s challenging operating conditions.

Report Scope

This market research report provides a comprehensive analysis of the global Industrial PC (IPC) market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial PC Market?

-> Industrial PC Market size was valued at US$ 5.67 billion in 2024 and is projected to reach US$ 10.89 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032.

Which key companies operate in Global Industrial PC Market?

-> Key players include Advantech, Siemens, Adlinktech, EVOC, AAEON, Axiomtek, B&R Automation, Norco, Contec, and Anovo, among others.

What are the key growth drivers?

-> Key growth drivers include Industry 4.0 adoption, increasing automation in manufacturing, demand for robust computing in harsh environments, and the integration of AI and IoT technologies.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by manufacturing hubs in China, Japan, and South Korea, while North America and Europe remain significant markets due to advanced industrial automation.

What are the emerging trends?

-> Emerging trends include edge computing integration, fanless and ruggedized designs, increased adoption of ARM-based processors, and the development of energy-efficient industrial computing solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...