MARKET INSIGHTS

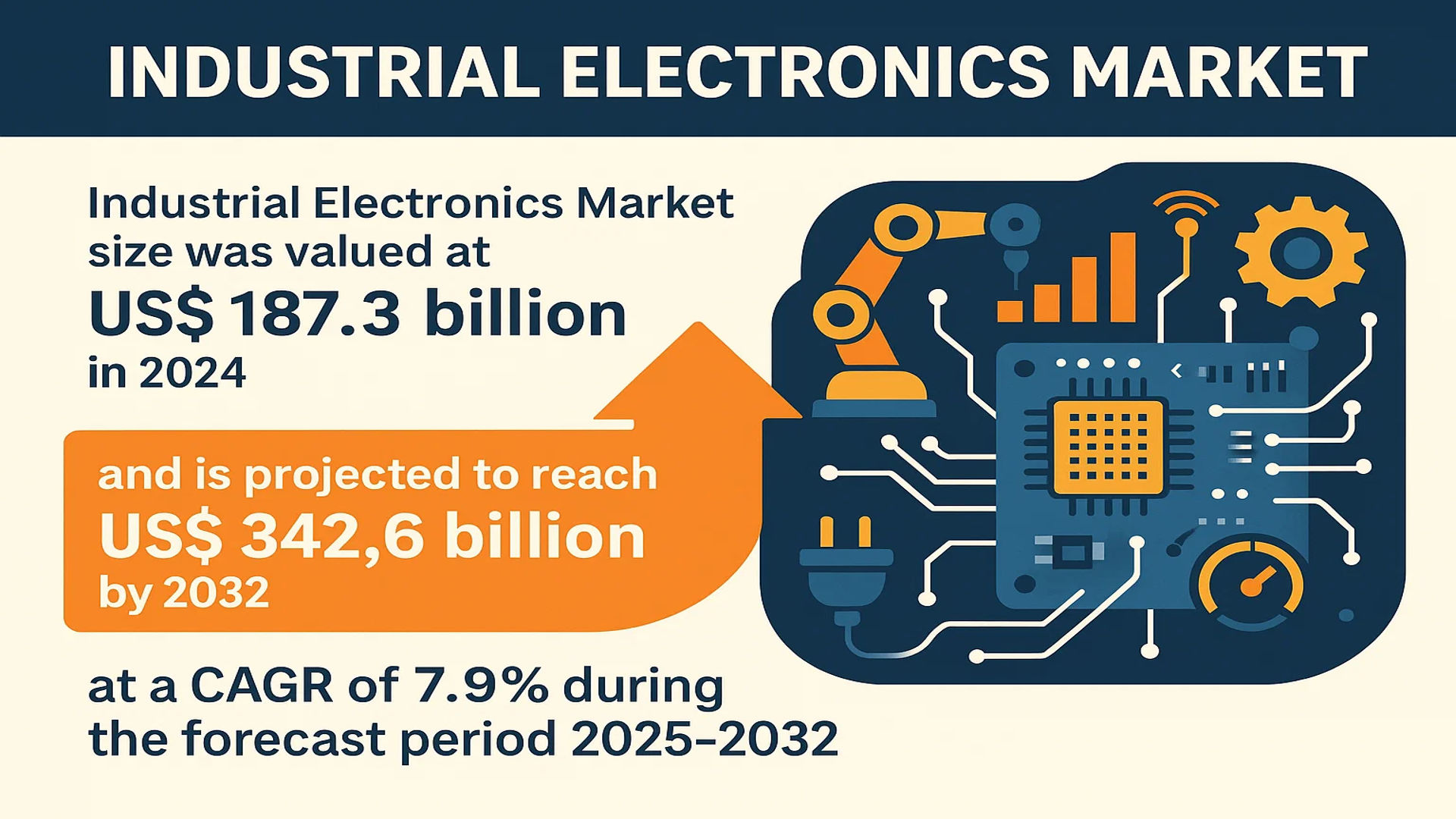

The global Industrial Electronics Market size was valued at US$ 187.3 billion in 2024 and is projected to reach US$ 342.6 billion by 2032, at a CAGR of 7.9% during the forecast period 2025-2032.

Industrial electronics is a specialized branch of electronic engineering focused on the design, development, and application of electronic devices and systems for industrial use. This field encompasses a wide array of components and systems, including power semiconductor devices, sensors and actuators, motor drives, and sophisticated instrumentation. These technologies are fundamental to modern industrial operations because they enable control systems, automation, signal processing, and diagnostic mechanisms across various applications.

The market is experiencing robust growth driven by the accelerating global adoption of Industry 4.0 and smart manufacturing principles, which demand higher levels of automation and connectivity. Furthermore, significant investments in infrastructure modernization, particularly in the energy and semiconductor sectors, are fueling demand. The push for greater operational efficiency and predictive maintenance is also a key growth driver. The market is highly competitive, with the top three players—ABB, Mitsubishi Electric, and Rockwell Automation—collectively holding approximately 20% of the global market share, underscoring a fragmented but innovation-driven competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Industry 4.0 Adoption to Propel Industrial Electronics Demand

The global push toward Industry 4.0 is fundamentally transforming manufacturing ecosystems, driving unprecedented demand for industrial electronics components. Smart factories require sophisticated power semiconductor devices, sensors, and intelligent electronic systems to enable real-time data processing, predictive maintenance, and autonomous operations. The manufacturing sector’s digital transformation investment is projected to exceed $1.2 trillion annually by 2025, with industrial electronics serving as the foundational infrastructure. These components facilitate seamless communication between operational technology (OT) and information technology (IT) systems, enabling manufacturers to achieve productivity gains of 20-30% through optimized processes. The convergence of industrial IoT, artificial intelligence, and advanced robotics creates a robust demand environment for precision instrumentation, motor drives, and control systems that form the backbone of modern industrial automation.

Expansion of Renewable Energy Infrastructure to Fuel Market Growth

The global transition toward renewable energy sources is creating substantial opportunities for industrial electronics manufacturers. Solar and wind power installations require advanced power conversion systems, grid stabilization equipment, and sophisticated monitoring devices—all relying on high-performance industrial electronic components. The renewable energy sector is expected to account for nearly 95% of the increase in global power capacity through 2026, necessitating massive investments in power electronics and control systems. Industrial electronics enable efficient energy conversion, distribution, and storage solutions that are critical for integrating intermittent renewable sources into existing power grids. Power semiconductor devices, particularly insulated-gate bipolar transistors (IGBTs) and silicon carbide (SiC) components, are experiencing surging demand due to their superior efficiency in high-power applications. This sector’s growth directly correlates with increased adoption of industrial electronics in energy infrastructure projects worldwide.

Automotive Electrification to Drive Semiconductor and Sensor Demand

The rapid electrification of automotive transportation represents a significant growth driver for industrial electronics. Electric vehicles (EVs) incorporate approximately twice the semiconductor content compared to traditional internal combustion engine vehicles, creating substantial market expansion opportunities. The global EV market is projected to grow at a compound annual growth rate exceeding 25% through 2030, directly increasing demand for power electronics, sensors, and control systems. Industrial electronics components are essential for battery management systems, charging infrastructure, power conversion, and vehicle automation functions. The automotive industry’s transformation toward electrification and autonomous driving requires sophisticated electronic systems that must meet rigorous industrial standards for reliability, temperature tolerance, and operational safety. This vertical market’s expansion consequently fuels innovation and production scaling across multiple industrial electronics segments.

MARKET RESTRAINTS

Global Semiconductor Supply Chain Disruptions to Constrain Market Expansion

The industrial electronics market faces significant constraints due to ongoing semiconductor supply chain vulnerabilities. The concentration of semiconductor manufacturing capacity in specific geographic regions creates systemic risks that became particularly evident during recent global disruptions. Industrial electronics manufacturers experience extended lead times ranging from 26 to 52 weeks for critical components, particularly advanced microcontrollers, power management integrated circuits, and specialized sensors. These supply constraints directly impact production schedules and increase costs throughout the value chain. The automotive industry’s recovery from semiconductor shortages has intensified competition for available manufacturing capacity, further straining industrial electronics supply. Additionally, geopolitical tensions and trade restrictions complicate sourcing strategies for manufacturers who require consistent access to advanced semiconductor technologies.

Rising Raw Material and Energy Costs to Impact Profitability

Escalating production costs present substantial challenges for industrial electronics manufacturers. The industry faces increasing prices for raw materials including silicon wafers, rare earth elements, copper, and specialty chemicals essential for component production. Energy-intensive manufacturing processes become significantly more expensive as global energy prices fluctuate, particularly affecting fabrication facilities and testing operations. These cost pressures are compounded by transportation expenses and tariffs that have increased by approximately 15-20% across major trade routes. Manufacturers must navigate these economic headwinds while maintaining competitive pricing for industrial customers who themselves face budget constraints. The capital-intensive nature of industrial electronics production means that margin compression directly impacts research and development investments necessary for technological advancement.

Technical Complexity and Certification Requirements to Slow Market Penetration

The industrial electronics market encounters significant barriers due to the technical sophistication required for product development and certification. Industrial applications demand extreme reliability, often requiring components to operate in harsh environments with wide temperature ranges, vibration, and electromagnetic interference. Meeting these specifications necessitates extensive testing and validation processes that can extend development cycles by 40-60% compared to consumer electronics. Certification requirements vary across regions and industries, with industrial equipment typically requiring compliance with multiple safety and performance standards. The aerospace, defense, and energy sectors impose particularly rigorous qualification processes that can take several years to complete. These technical and regulatory hurdles create substantial entry barriers for new market participants and slow the adoption of innovative technologies in critical industrial applications.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Industrial Control Systems to Pose Operational Risks

The increasing connectivity of industrial electronics introduces significant cybersecurity challenges that threaten operational integrity. Industrial control systems (ICS) and operational technology networks historically operated in isolation but now integrate with enterprise IT systems, creating expanded attack surfaces. Cybersecurity incidents targeting industrial infrastructure have increased by over 200% in recent years, with attacks becoming more sophisticated and potentially catastrophic. Industrial electronics manufacturers must implement robust security architectures at the component level, including hardware-based encryption, secure boot processes, and intrusion detection capabilities. The legacy nature of many industrial systems complicates security upgrades, as equipment often remains operational for decades. Addressing these vulnerabilities requires coordinated efforts across manufacturers, system integrators, and end-users to develop comprehensive security frameworks that protect critical infrastructure without compromising operational efficiency.

Skills Gap in Industrial Electronics Engineering to Hinder Innovation

The industrial electronics sector faces a critical shortage of qualified engineering talent capable of developing next-generation technologies. The interdisciplinary nature of industrial electronics requires expertise across power systems, control theory, semiconductor physics, and software development—a combination increasingly rare in the labor market. Educational institutions produce insufficient numbers of graduates with practical experience in industrial applications, creating a talent pipeline that cannot keep pace with industry demands. This skills gap is exacerbated by an aging workforce with deep institutional knowledge approaching retirement. Companies report requiring 30-50% longer recruitment cycles for specialized positions, delaying product development and technological advancement. The complexity of modern industrial systems necessitates continuous training and knowledge transfer that becomes increasingly challenging without adequate technical resources.

Technological Obsolescence and Legacy System Integration to Complicate Upgrades

Industrial electronics manufacturers confront the challenge of balancing innovation with backward compatibility in rapidly evolving technological landscapes. Industrial equipment typically has operational lifespans exceeding 15 years, creating integration challenges when introducing new electronic components and systems. The persistence of legacy communication protocols, voltage standards, and mechanical interfaces requires manufacturers to maintain support for outdated technologies while developing advanced solutions. This dual requirement increases development complexity and costs, as engineers must design systems that interface with both modern digital networks and analog control systems from previous generations. The industrial sector’s risk aversion further complicates technology adoption, as equipment failures can result in substantial production losses and safety incidents. Manufacturers must demonstrate unequivocal reliability advantages before customers will undertake costly system upgrades.

MARKET OPPORTUNITIES

Edge Computing and AI Integration to Create New Application Frontiers

The convergence of industrial electronics with edge computing and artificial intelligence presents transformative opportunities across multiple sectors. Industrial equipment generates massive data volumes that require real-time processing at the network edge rather than centralized cloud infrastructure. This paradigm shift drives demand for industrial-grade computing hardware capable of operating in harsh environments while delivering substantial processing power. AI algorithms deployed at the edge enable predictive maintenance, quality control, and optimization processes that significantly enhance operational efficiency. The industrial edge computing market is projected to grow at a compound annual growth rate exceeding 30% through 2030, creating substantial opportunities for manufacturers of industrial servers, gateways, and specialized processing units. These systems require robust industrial electronics designed for reliability, low latency, and power efficiency in demanding operational environments.

Advanced Semiconductor Materials to Enable Next-Generation Performance

Breakthroughs in semiconductor materials science create significant opportunities for performance advancement in industrial electronics. Wide-bandgap semiconductors including silicon carbide (SiC) and gallium nitride (GaN) offer substantial advantages over traditional silicon in power conversion applications, enabling higher efficiency, power density, and operating temperatures. These materials are particularly valuable for industrial applications where energy efficiency and thermal management are critical concerns. The wide-bandgap semiconductor market is experiencing accelerated adoption across industrial motor drives, renewable energy systems, and electric vehicle charging infrastructure. Material innovations allow industrial electronics manufacturers to develop products with improved performance characteristics that address evolving customer requirements for smaller form factors, reduced cooling requirements, and enhanced reliability. The continuous advancement of semiconductor technologies creates opportunities for product differentiation and market expansion.

Sustainable Manufacturing Initiatives to Drive Electronics Innovation

Global sustainability imperatives create substantial opportunities for industrial electronics that enable energy efficiency and emissions reduction. Industrial operations account for approximately one-third of global energy consumption, creating significant demand for electronics that optimize energy usage. Variable frequency drives, smart sensors, and energy management systems represent growing market segments as manufacturers seek to reduce operational costs and environmental impact. Regulatory pressures and corporate sustainability commitments drive investments in industrial electronics that monitor and control energy consumption across manufacturing processes. Additionally, the circular economy movement creates opportunities for electronics designed for repairability, upgradability, and end-of-life recovery. Manufacturers that develop products aligned with sustainability objectives can access growing market segments and potentially command premium pricing for environmentally conscious industrial solutions.

INDUSTRIAL ELECTRONICS MARKET TRENDS

Industrial Automation and Industry 4.0 Integration as a Primary Market Driver

The global push towards Industry 4.0 and smart manufacturing is fundamentally reshaping the industrial electronics landscape. This trend is characterized by the deep integration of cyber-physical systems, the Internet of Things (IoT), and cloud computing into industrial environments. A key driver is the escalating demand for industrial automation to enhance operational efficiency, reduce human error, and optimize production lines. This has led to a surge in the adoption of sophisticated components like Programmable Logic Controllers (PLCs), sensors, and motor drives. The market for industrial sensors alone is projected to grow at a significant rate, underpinned by the need for real-time data acquisition and process control. Furthermore, the increasing deployment of collaborative robots (cobots) and automated guided vehicles (AGVs) in warehouses and factories is creating substantial demand for the power electronics and control systems that form their core. This shift is not merely about replacing manual labor but about creating interconnected, data-driven ecosystems that can predict maintenance needs and adapt to changing production demands autonomously.

Other Trends

Electrification of Transportation and Energy Infrastructure

The global transition towards electrification, particularly in the transportation and energy sectors, is generating massive opportunities for industrial electronics. The rapid expansion of electric vehicle (EV) manufacturing necessitates advanced power semiconductor devices, battery management systems, and charging infrastructure, all of which fall under the industrial electronics umbrella. Similarly, the modernization of the power grid to incorporate renewable energy sources like solar and wind requires robust industrial electronics for power conversion, grid stability, and smart energy management. Investments in upgrading aging energy infrastructure in developed economies, coupled with building new smart grids in developing regions, are fueling demand for products like high-voltage direct current (HVDC) transmission systems and smart meters. This trend is further accelerated by government policies and corporate sustainability goals aiming for carbon neutrality, making energy efficiency a paramount concern for industrial operations worldwide.

Advancements in Semiconductor and Component Technology

Continuous innovation in semiconductor technology is a critical enabler for the entire industrial electronics sector. The development of wide-bandgap semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), is revolutionizing power electronics. These materials offer superior performance compared to traditional silicon, including higher efficiency, faster switching speeds, and the ability to operate at higher temperatures and voltages. This makes them ideal for high-demand applications in motor drives, renewable energy systems, and industrial power supplies, leading to overall system size reduction and energy savings. Moreover, the miniaturization of components and the integration of more functionalities into single chips (SoC – System on Chip) are allowing for the design of more compact, reliable, and powerful industrial control systems. These technological leaps are crucial for meeting the increasingly complex requirements of modern industrial applications, from precision manufacturing to harsh environment operation.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Innovation and Strategic Expansions to Maintain Market Position

The global industrial electronics market exhibits a semi-consolidated competitive structure, featuring a dynamic mix of multinational corporations, specialized medium-sized enterprises, and agile smaller players. ABB Ltd. stands as a dominant force, largely due to its comprehensive portfolio spanning power semiconductors, automation systems, and robotics. Its extensive global manufacturing footprint and sustained investment in R&D, particularly in areas like industrial IoT and energy efficiency, have cemented its leadership. In 2024, ABB, alongside Mitsubishi Electric Corporation and Rockwell Automation, collectively accounted for a significant portion of the global market share, estimated at approximately 20%.

Infineon Technologies and Texas Instruments also command considerable influence, driven by their critical role as suppliers of core components like power management ICs, sensors, and microcontrollers. Their growth is intrinsically linked to the broader expansion of key end-markets, especially semiconductor manufacturing, renewable energy infrastructure, and industrial automation. These companies maintain their edge through continuous innovation; for instance, Infineon’s focus on silicon carbide (SiC) and gallium nitride (GaN) semiconductors addresses the growing demand for high-efficiency power electronics in electric vehicles and industrial motor drives.

Furthermore, strategic initiatives are a primary growth driver across the competitive landscape. Companies are actively pursuing mergers, acquisitions, and partnerships to broaden their technological capabilities and geographic reach. Recent developments include significant investments in expanding production capacity for advanced components to alleviate supply chain constraints and meet rising demand. This focus on strategic expansion and product diversification is expected to be a key factor in shaping market shares throughout the forecast period.

Meanwhile, other established players like STMicroelectronics and NXP Semiconductors are strengthening their positions by deepening their engagement in high-growth application segments such as automotive electronics and aerospace & defense. Their strategy involves significant R&D expenditure aimed at developing more integrated, secure, and connected solutions, ensuring their continued relevance in an increasingly digital industrial ecosystem.

List of Key Industrial Electronics Companies Profiled

- ABB Ltd. (Switzerland)

- Mitsubishi Electric Corporation (Japan)

- Rockwell Automation, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Vishay Intertechnology, Inc. (U.S.)

- Microchip Technology Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics N.V. (Switzerland)

- NXP Semiconductors N.V. (Netherlands)

- Toshiba Corporation (Japan)

- ON Semiconductor (U.S.)

- Renesas Electronics Corporation (Japan)

- Maxim Integrated (Part of Analog Devices, Inc.) (U.S.)

- Fuji Electric Co., Ltd. (Japan)

Segment Analysis:

By Type

Power Semiconductor Devices Segment Dominates the Market Due to Critical Role in Energy Efficiency and Power Management

The market is segmented based on type into:

- Power Semiconductor Devices

- Subtypes: Thyristors, SCRs, IGBTs, MOSFETs, and others

- Sensors and Actuators

- Instrumentation

- Intelligent Electronic Devices

- Motor Drives

- Power Systems

- Measurement and Testing Equipment

By Application

Semiconductor Manufacturing Segment Leads Due to High Precision and Automation Requirements

The market is segmented based on application into:

- Semiconductor

- Telecommunication

- Energy

- Transportation

- Healthcare

- Aerospace and Defense

- Chemical

- Mining

By End User

Industrial Manufacturing Sector Represents the Largest End-User Segment

The market is segmented based on end user into:

- Industrial Manufacturing

- Oil & Gas

- Utilities

- Automotive

- Electronics

Regional Analysis: Industrial Electronics Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global industrial electronics market, driven by its massive manufacturing base and rapid technological adoption. China is the primary engine of growth, accounting for a significant portion of both production and consumption, fueled by government initiatives like “Made in China 2025” which prioritizes advanced manufacturing and industrial automation. Japan and South Korea remain powerhouses in high-precision components, such as power semiconductor devices and sensors, with leading firms like Mitsubishi Electric and Toshiba Corporation maintaining strong global positions. While cost-competitive manufacturing of conventional electronics is prevalent, there is a pronounced and accelerating shift towards sophisticated automation systems, IoT-enabled devices, and energy-efficient power electronics, spurred by rising labor costs and the need for enhanced operational efficiency. The semiconductor and telecommunications application segments are particularly dominant here, supported by extensive local supply chains and relentless infrastructure development.

North America

North America is a highly advanced and innovation-centric market characterized by stringent regulatory standards and early adoption of Industry 4.0 technologies. The region boasts a strong presence of key market leaders including Rockwell Automation, Texas Instruments, and Microchip Technology. Growth is primarily propelled by substantial investments in industrial automation, smart manufacturing, and the modernization of aging infrastructure across sectors like energy, aerospace, and defense. The recent Infrastructure Investment and Jobs Act further catalyzes demand for industrial electronics used in grid modernization and transportation systems. A significant trend is the integration of AI and machine learning with industrial control systems to optimize production processes and predictive maintenance. The market is also seeing robust demand in the healthcare and telecommunications application segments, driven by a need for high-reliability and precision components.

Europe

Europe’s market is defined by its strong regulatory framework, emphasizing energy efficiency, safety, and environmental sustainability, which drives innovation in green electronics and automation solutions. Germany, with its flagship “Industrie 4.0” initiative, is at the forefront, fostering the development of smart factories and cyber-physical systems. Major players like Infineon Technologies, STMicroelectronics, and ABB have a formidable presence, focusing on high-value products such as motor drives, power systems, and sophisticated sensors. The region shows strong demand from the automotive, chemical, and renewable energy sectors, where precision instrumentation and robust power management are critical. However, the market faces challenges from economic uncertainties and high manufacturing costs, which can slow investment. Despite this, the push towards digitalization and circular economy principles ensures steady, innovation-driven growth.

South America

The industrial electronics market in South America is emerging, with growth opportunities tied to the gradual modernization of industrial sectors in countries like Brazil and Argentina. The mining and energy industries are primary consumers, creating demand for ruggedized sensors, motor drives, and power systems designed for harsh environments. However, the market’s expansion is frequently hindered by economic volatility, political instability, and fluctuating currency values, which impact capital expenditure and the adoption of advanced technologies. There is a reliance on imported high-end components, as local manufacturing capabilities for sophisticated electronics are still developing. While investments in infrastructure and industrial projects present a positive long-term outlook, the market currently progresses at a more measured pace compared to other regions, with cost sensitivity being a major factor in purchasing decisions.

Middle East & Africa

This region represents an emerging market with potential concentrated in specific nations undertaking significant infrastructure and industrial diversification projects, such as those in the UAE, Saudi Arabia, and Turkey. The energy sector, including both traditional oil & gas and burgeoning renewable projects, is a major driver of demand for industrial electronics, particularly measurement & testing equipment, control systems, and power electronics. Visionary programs like Saudi Arabia’s Vision 2030 are creating opportunities in manufacturing and smart city development. However, the broader market growth is constrained by factors including limited local manufacturing, reliance on imports, and underdeveloped regulatory frameworks for advanced industrial technologies. While the demand for durable and reliable electronics is rising, the market’s evolution is gradual, with long-term growth hinging on economic stability and continued investment in industrial modernization.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Industrial Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Industrial Electronics Market?

-> Industrial Electronics Market size was valued at US$ 187.3 billion in 2024 and is projected to reach US$ 342.6 billion by 2032, at a CAGR of 7.9% during the forecast period 2025-2032.

Which key companies operate in Global Industrial Electronics Market?

-> Key players include ABB, Mitsubishi Electric, Rockwell Automation, Infineon Technologies, Texas Instruments, STMicroelectronics, and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include Industry 4.0 adoption, automation across manufacturing sectors, increasing demand for energy-efficient systems, and infrastructure modernization initiatives.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, accounting for over 45% of global revenue, followed by North America and Europe.

What are the emerging trends?

-> Emerging trends include integration of AI and IoT in industrial systems, adoption of wide-bandgap semiconductors, predictive maintenance technologies, and sustainable manufacturing solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...