MARKET INSIGHTS

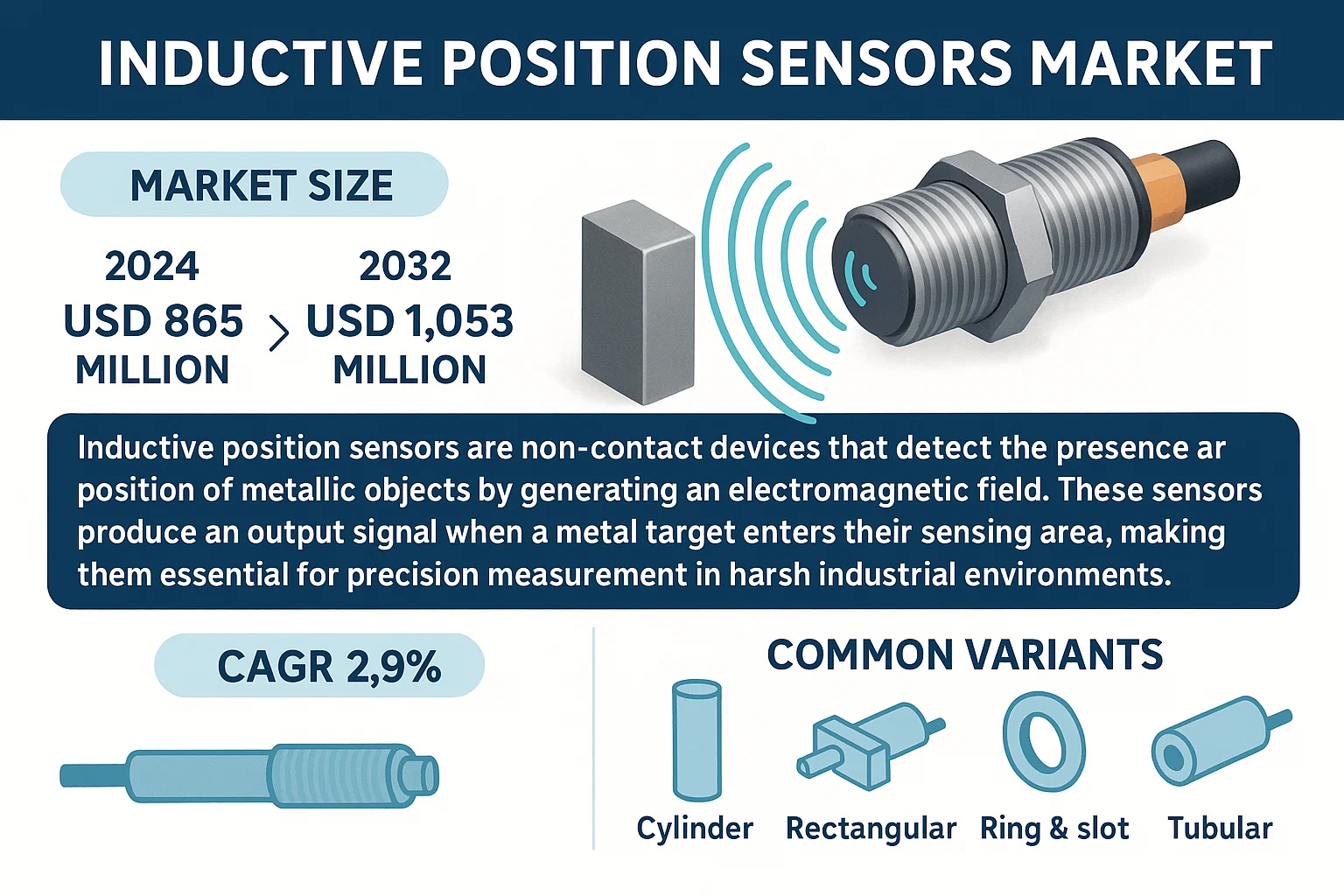

Global Inductive Position Sensors Market size was valued at USD 865 million in 2024 to USD 1,053 million by 2032, exhibiting a CAGR of 2.9% during the forecast period.

Inductive position sensors are non-contact devices that detect the presence or position of metallic objects by generating an electromagnetic field. These sensors produce an output signal when a metal target enters their sensing area, making them essential for precision measurement in harsh industrial environments. Common variants include cylinder, rectangular, ring & slot, and tubular sensors, catering to diverse applications like automotive, aerospace, and industrial automation.

The market growth is driven by increasing automation across industries and the need for reliable position sensing in critical applications. Europe and North America dominate production, while Asia-Pacific shows promising growth due to expanding manufacturing sectors. Leading players like ifm Electronic, Pepperl+Fuchs, and Turck collectively hold 60% market share, with continuous innovation in ruggedized designs for extreme conditions.

MARKET DRIVERS

Rising Demand for High-Accuracy Position Sensing

The increasing automation across industries requires precise motion control, driving demand for inductive position sensors with resolution capabilities under 10 micrometers. This is particularly critical in semiconductor manufacturing and precision engineering applications.

Growth in Industrial Automation and Robotics

Industrial robots now require absolute position feedback throughout their operating range, creating strong demand for durable non-contact position sensors. The global robotics market expanding at 12.5% CAGR directly drives sensor adoption.

➤ Industry 4.0 initiatives are accelerating the adoption of smart sensors across manufacturing sectors, with inductive variants seeing 18.3% year-over-year growth in factory automation applications.

Additionally, the integration of IIoT capabilities into position sensors enables predictive maintenance, reducing downtime by up to 45% in continuous production environments.

MARKET CHALLENGES

High Cost of Advanced Inductive Position Sensors

The integration of signal conditioning electronics and precision manufacturing processes results in average unit costs 40-60% higher than conventional sensors. This creates significant adoption barriers in price-sensitive emerging markets where cost remains the primary purchase driver.

Other Challenges

Technical Complexity in Integration

Integrating inductive position sensors with existing systems can be complex, requiring specialized knowledge and sometimes leading to increased implementation costs.

Limited Awareness in Emerging Markets

In some emerging markets, there is limited awareness of the benefits of advanced inductive position sensors, which can slow down adoption.

MARKET RESTRAINTS

Impact of Economic Downturns on Industrial Investments

During economic downturns, companies often cut back on capital expenditures, including investments in new machinery and automation. This can temporarily reduce the demand for inductive position sensors as manufacturers delay automation projects and equipment upgrades.

MARKET OPPORTUNITIES

Expansion of Electric and Hybrid Vehicles

The rapid growth of the electric vehicle (EV) market is driving demand for various sensors, including inductive position sensors used in motor encoders and battery management systems. With global EV sales projected to reach 45 million units by 2030, the demand for precision position sensing in motor control and battery management presents substantial growth opportunities.

Inductive Position Sensors Market Trends

Regional Market Expansion and Concentration

The global Inductive Position Sensors market demonstrates significant regional concentration in both production and consumption. Europe and North America remain the dominant production hubs, collectively accounting for over 60% of global manufacturing capacity. Meanwhile, Asia-Pacific markets show the fastest growth rates in consumption, particularly in China, Japan, and Southeast Asian countries, driven by rapid industrialization and automation adoption across manufacturing sectors.

Other Trends

Technology Integration and Miniaturization

Leading manufacturers are increasingly integrating advanced signal processing and communication capabilities into inductive sensors. The trend toward miniaturization continues with new product releases featuring 30% smaller form factors compared to previous generations while maintaining or improving sensing distances. This evolution supports installation in space-constrained industrial applications without compromising performance.

Industry 4.0 and Smart Manufacturing Integration

Adoption of Industry 4.0 principles drives demand for smart sensors with IIoT connectivity. Major manufacturers now offer inductive position sensors with integrated IO-Link communication, enabling real-time monitoring, predictive maintenance, and data analytics integration. This connectivity allows for real-time monitoring of equipment performance, predictive maintenance scheduling, and integration with manufacturing execution systems for improved operational efficiency.

Application Sector Growth

The automotive industry remains the largest application sector, accounting for approximately 32% of global demand, driven by increasing automation in production lines and quality control processes. The industrial manufacturing segment follows closely, particularly in metalworking, packaging, and assembly automation. Emerging applications in renewable energy installation and robotics continue to show above-average growth rates.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders in Inductive Position Sensors Manufacturing

The global inductive position sensors market is dominated by established European and American manufacturers, with ifm Electronic, Pepperl+Fuchs, and TURCK holding significant market shares. These companies lead in technological innovation and global distribution networks, offering comprehensive product portfolios for diverse industrial applications.

Japanese manufacturers like Omron Corporation contribute significantly to the Asian market with advanced sensing technologies, while North American players like Eaton maintain strong presence in industrial automation sectors. The market structure remains moderately concentrated with top 6 players controlling approximately 60% of global production capacity.

List of Key Inductive Position Sensors Companies

- ifm Electronic

- PEPPERL+FUCHS

- TURCK

- Omron Corporation

- Eaton Corporation

- Baumer Group

- Honeywell International Inc

- Schneider Electric

- Rockwell Automation

- Balluff GmbH

- Sick AG

- Panasonic Corporation

- GARLO GAVAZZI

- Fargo Controls

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Linear Position Sensors dominate due to their precision in measuring straight-line movements, which is critical for industrial automation and robotics applications where accuracy is paramount. |

| By Application |

|

Industrial Automation leads as these sensors provide critical feedback for automated machinery, robotic arms, and CNC machines where positional accuracy directly impacts manufacturing quality and operational safety. |

| By End User |

|

OEM Manufacturers lead as they integrate these sensors directly into their products during manufacturing, particularly in automotive, industrial equipment, and robotic systems where integrated position sensing is a fundamental component. |

| By Sensing Range |

|

Medium-Range sensors lead as they provide the optimal balance between detection distance and precision for most industrial applications, from robotic arms to assembly line positioning where both range and accuracy are equally critical. |

| By Technology |

|

LVDT-based Sensors lead due to their exceptional linearity and resolution for applications requiring micron-level precision, particularly in aerospace components and scientific instrumentation where measurement integrity is non-negotiable. |

Regional Analysis: Inductive Position Sensors Market

North American manufacturers lead in developing advanced inductive position sensors with enhanced accuracy and durability. Continuous innovation in miniaturization and wireless capabilities keeps the region at the forefront of global competition, with companies investing heavily in R&D for next-generation industrial automation.

The region’s mature industrial sector utilizes inductive position sensors across robotic systems, CNC machinery, and automated assembly lines. High adoption in automotive manufacturing and aerospace sectors drives continuous demand, with sensors becoming integral to predictive maintenance and real-time monitoring systems in smart factories.

North American markets benefit from standardized regulations that ensure quality and interoperability while encouraging innovation. Certification processes and industry standards facilitate export opportunities and enable seamless integration with international markets, particularly in cross-border manufacturing ecosystems.

Well-developed logistics and distribution networks enable efficient supply of inductive position sensors across the region. Strong relationships between manufacturers and distributors ensure availability even during peak demand periods, while e-commerce platforms enhance accessibility for smaller enterprises seeking automation solutions.

Europe

Europe maintains a strong position in inductive position sensor adoption, particularly in Germany’s precision engineering sector and Western European industrial automation. The region benefits from extensive manufacturing heritage combined with digital transformation initiatives, creating sustained demand across automotive, industrial machinery, and renewable energy sectors. Strict quality standards and environmental regulations drive innovation in energy-efficient sensor technologies.

Asia-Pacific

The Asia-Pacific region demonstrates the fastest growth in inductive position sensor adoption, led by China’s manufacturing expansion and Japan’s technological expertise. Rapid industrialization and increasing automation across manufacturing sectors drives demand, particularly in China, South Korea, and Southeast Asian markets. Government initiatives supporting Industry 4.0 adoption further accelerate market growth.

Latin America

Latin American markets show gradual but steady growth in inductive position sensor adoption, particularly in Brazil and Mexico where automotive and industrial manufacturing sectors are expanding. Economic fluctuations occasionally impact investment cycles, but long-term industrial development plans continue to drive demand. Infrastructure development projects create additional opportunities across the region.

Middle East & Africa

While currently a smaller market, the Middle East and Africa show promising growth potential as industrialization initiatives gain momentum. Infrastructure development and gradual industrial automation in key economies create emerging opportunities. Regional partnerships and technology transfer agreements are gradually improving accessibility to advanced sensor technologies across developing markets.

Report Scope

This market research report provides a comprehensive analysis of the Inductive Position Sensors Market, covering the forecast period 2025-2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand-supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Inductive Position Sensors Market?

-> The Global Inductive Position Sensors Market was valued at USD 865 million in 2024 and is projected to reach USD 1053 million by 2032.

Which key companies operate in the Inductive Position Sensors Market?

-> Key players include Ifm Electronic, PEPPERL+FUCHS, TURCK, Omron Corporation, Eaton, and Baumer, among others.

What is the growth rate of the Inductive Position Sensors Market?

-> The market is expected to grow at a CAGR of 2.9% from 2024 to 2032.

What are the key application areas?

-> Key applications include Aerospace & Defense, Automotive, Industrial Manufacturing, and Food & Beverage industries.

Which regions dominate the market?

-> Europe and North America are the dominant markets, while Asia-Pacific shows the fastest growth rate.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...