Market Insights

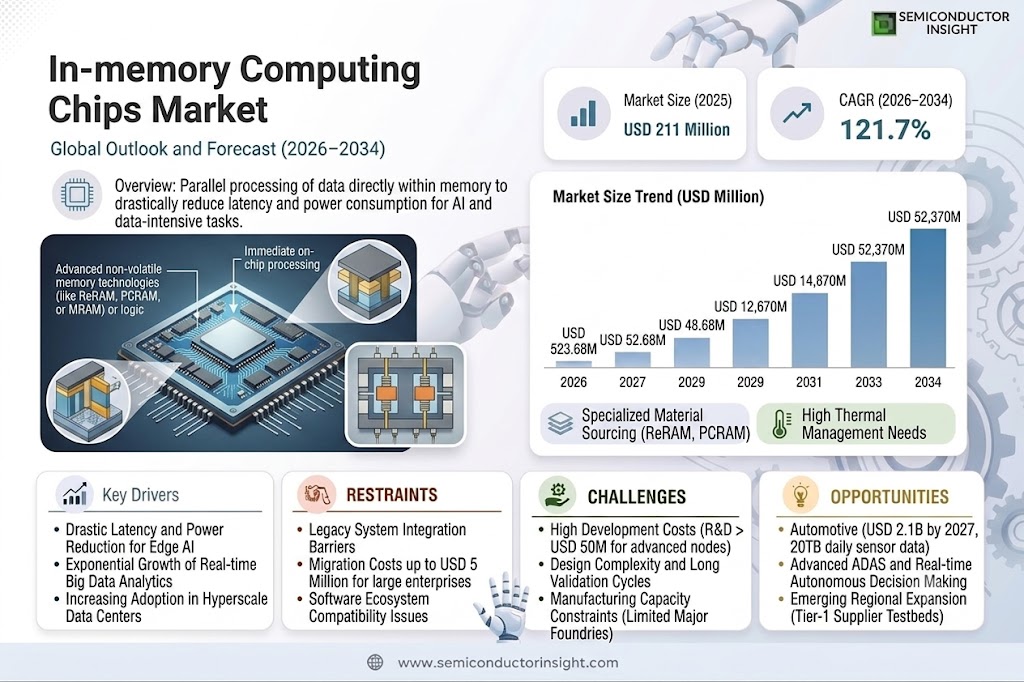

Global In-memory Computing Chips Market size was valued at USD 211 million in 2025. The market is projected to grow from USD 523.68 million in 2026 to USD 52.37 billion by 2034, exhibiting a CAGR of 121.7% during the forecast period.

In-memory computing chips are semiconductor devices that process data directly within memory arrays, eliminating the need for separate processing and storage units. These chips leverage architectures such as SRAM, DRAM, or emerging non-volatile memory technologies to accelerate AI workloads, reduce power consumption, and minimize latency. Their applications span edge AI devices, robotics, smart sensors, and industrial automation systems where real-time processing and energy efficiency are critical.

The market growth is driven by escalating demand for low-power AI solutions and advancements in memory-centric computing architectures. While adoption remains concentrated in specialized applications, broader commercialization is anticipated as manufacturing scalability and software ecosystems mature.

MARKET DRIVERS

Growing Demand for High-Speed Data Processing

In-memory Computing Chips Market is witnessing significant growth due to increasing demand for real-time data processing across industries. With enterprises requiring faster analytics and AI-driven insights, in-memory computing chips eliminate storage bottlenecks, delivering performance improvements of up to 100x compared to traditional architectures.

AI and Machine Learning Adoption

Advancements in artificial intelligence are accelerating adoption of in-memory computing chips, as they enable low-latency processing for neural networks. The global AI chip market is projected to grow at 35% CAGR, directly benefiting in-memory computing solutions that reduce data movement energy by 70%.

5G network expansion further drives demand, as telecom providers require in-memory processing chips to handle massive data streams with sub-millisecond latency.

MARKET CHALLENGES

High Development Costs and Complexity

While in-memory computing chips offer superior performance, their design complexity results in R&D costs exceeding USD 50 million for advanced nodes. Fabrication requires specialized materials like resistive RAM (ReRAM) and phase-change memory, creating supply chain dependencies.

Other Challenges

Thermal Management Issues

Power densities in in-memory computing architectures can exceed 100W/cm², requiring advanced cooling solutions that increase system costs by 20-30%.

Limited Ecosystem Support

Only 3 major foundries currently offer volume production for in-memory computing chips, creating capacity constraints during market upturns.

MARKET RESTRAINTS

Legacy System Integration Barriers

Enterprise adoption of in-memory computing chips faces resistance due to compatibility issues with existing data center infrastructure. Migration costs can reach USD 5 million for Fortune 500 companies, delaying ROI realization. Software ecosystems also require significant modification to leverage in-memory architectures effectively.

MARKET OPPORTUNITIES

Automotive and Autonomous Driving Applications

The automotive sector presents a USD 2.1 billion opportunity for in-memory computing chips by 2027, as next-gen vehicles require processing 20TB of sensor data daily. Tier-1 suppliers are actively testing in-memory processors for real-time decision making in ADAS systems.

Healthcare Analytics Expansion

Medical imaging and genomic sequencing are adopting in-memory computing solutions to reduce analysis time from days to hours. The healthcare segment is projected to grow at 42% CAGR through 2030.

In-memory Computing Chips Market Trends

Edge AI Adoption Driving Demand for In-memory Computing Chips

In-memory Computing Chips Market is witnessing rapid growth due to increasing adoption in edge AI applications. These chips excel in energy-efficient processing for devices requiring real-time analytics, such as smart cameras, robotics, and IoT systems. By eliminating data movement between memory and processors, they reduce power consumption by up to 70% compared to traditional architectures while improving latency.

Other Trends

Customized Design Partnerships Between Chip Vendors and OEMs

Major manufacturers are collaborating closely with system integrators to develop application-specific In-memory Computing Chips solutions. This trend reflects the market’s current specialization phase, where over 80% of deployments involve customized designs rather than off-the-shelf products, particularly for industrial automation and sensor processing applications.

Emerging Memory Technologies Gaining Traction

Non-volatile memory technologies are being increasingly integrated into In-memory Computing Chips to enhance energy efficiency. Hybrid architectures combining SRAM and novel memory types are showing promise for AI workloads, with several startups demonstrating prototypes that achieve superior power-performance ratios for neural network processing at the edge.

Regional Growth in Asia-Pacific Markets

China, South Korea, and Japan are emerging as key hubs for In-memory Computing Chips development, accounting for approximately 45% of recent patent filings in this domain. Government initiatives supporting AI hardware innovation and strong semiconductor ecosystems are accelerating commercial deployment in these regions.

Software Ecosystem Development Becomes Critical

As hardware matures, industry focus is shifting toward creating robust software toolchains for In-memory Computing Chips. Major challenges being addressed include compiler optimization for analog computing models and frameworks for precision control in AI inference tasks, which are essential for broader market adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation Leaders Driving the In-Memory Computing Revolution

In-memory Computing Chips Market is characterized by a mix of established semiconductor giants and specialized startups. Samsung and SK Hynix lead the space with their advanced memory technologies, leveraging their DRAM manufacturing expertise for compute-in-memory applications. These industry behemoths are complemented by AI-focused innovators like Syntiant and Mythic, whose ultra-low-power neural processors are gaining traction in edge devices. The market structure remains fragmented, with most players focusing on niche AI workloads rather than general-purpose computation.

Several emerging companies are making notable strides in specialized segments. China-based Witmem and Yizhu Intelligent Technology are pioneering analog in-memory computing solutions for domestic AI applications, while U.S. startups D-Matrix and EnCharge AI are developing digital CIM architectures for data center acceleration. European player Axelera AI focuses on vision processing, and UK’s Graphcore offers IPU architectures with memory-centric designs. These specialists often collaborate with system integrators to co-develop optimized solutions for target applications.

List of Key In-Memory Computing Chips Companies Profiled

- Samsung Electronics

- SK Hynix

- Syntiant

- D-Matrix

- Mythic AI

- Graphcore

- EnCharge AI

- Axelera AI

- Hangzhou Zhicun (Witmem) Technology

- Suzhou Yizhu Intelligent Technology

- Shenzhen Reexen Technology

- Beijing Houmo Technology

- AistarTek

- Beijing Pingxin Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

In-memory Computation (CIM) dominates due to superior energy efficiency for AI workloads:

|

| By Application |

|

Edge AI Devices represent the most mature application segment:

|

| By End User |

|

AI Chip Startups currently lead innovation in this space:

|

| By Technology |

|

Analog CIM shows strong potential for edge applications:

|

| By Memory Type |

|

SRAM-based solutions currently dominate the market:

|

Regional Analysis: In-memory Computing Chips Market

North America

Financial services and healthcare sectors lead adoption, leveraging in-memory computing chips for real-time fraud detection and genomic sequencing. The technology enables sub-millisecond processing crucial for algorithmic trading platforms.

A dense network of semiconductor fabs, design houses, and cloud providers accelerates product iteration cycles. Universities like MIT and Stanford contribute cutting-edge research in resistive RAM and phase-change memory architectures.

Mature 5G networks and distributed edge computing setups provide ideal deployment environments for in-memory solutions. Colocation facilities optimized for high-performance computing are widely available across major metros.

Favorable policies like the CHIPS Act stimulate domestic production while defense contracts drive specialized in-memory computing applications for aerospace and intelligence systems.

Europe

Europe maintains strong in-memory computing adoption through collaborative research initiatives like the European Processor Initiative. Germany’s automotive sector implements these chips for autonomous vehicle decision systems, while French research institutions pioneer neuromorphic computing architectures. The EU’s focus on digital sovereignty boosts investments in alternative chip designs, though the region trails North America in commercial deployment scales.

Asia-Pacific

Asia-Pacific emerges as the fastest-growing market, with China aggressively expanding domestic in-memory computing capabilities. South Korean memory chip manufacturers are pivoting to compute-in-memory designs, while Singapore’s smart city initiatives create demand for real-time urban analytics solutions. India’s thriving startup ecosystem explores cost-optimized variants for emerging market needs.

South America

South America shows nascent adoption, primarily in Brazil’s financial technology sector and Chile’s mining operations for real-time equipment monitoring. Limited semiconductor infrastructure and reliance on imports constrain market growth, though cloud providers are introducing in-memory solutions through their regional data centers.

Middle East & Africa

The region demonstrates strategic adoption in UAE’s smart city projects and Saudi Arabia’s Vision 2030 initiatives. South Africa leads in research applications for astronomy and climate modeling. Market growth faces challenges from limited local expertise and high infrastructure costs, offset by partnerships with global technology providers.

Report Scope

This market research report provides a comprehensive analysis of the In-memory Computing Chips Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of In-memory Computing Chips Market?

-> In-memory Computing Chips Market size was valued at USD 211 million in 2025. The market is projected to grow from USD 523.68 million in 2026 to USD 52.37 billion by 2034, exhibiting a CAGR of 121.7% during the forecast period.

What is the CAGR of In-memory Computing Chips Market?

-> Global In-memory Computing Chips market will grow at a CAGR of 121.7% during 2025-2032.

Which key companies operate in In-memory Computing Chips Market?

-> Key players include Samsung, SK Hynix, Syntiant, D-Matrix, Mythic, Graphcore, EnCharge AI, Axelera AI, Hangzhou Zhicun (Witmem) Technology, and Suzhou Yizhu Intelligent Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption in edge AI applications, demand for energy-efficient computing, and increasing AI/ML workloads requiring high memory bandwidth.

Which region dominates the market?

-> Asia currently leads the market (2025) while North America shows significant growth potential.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...