Market Insights

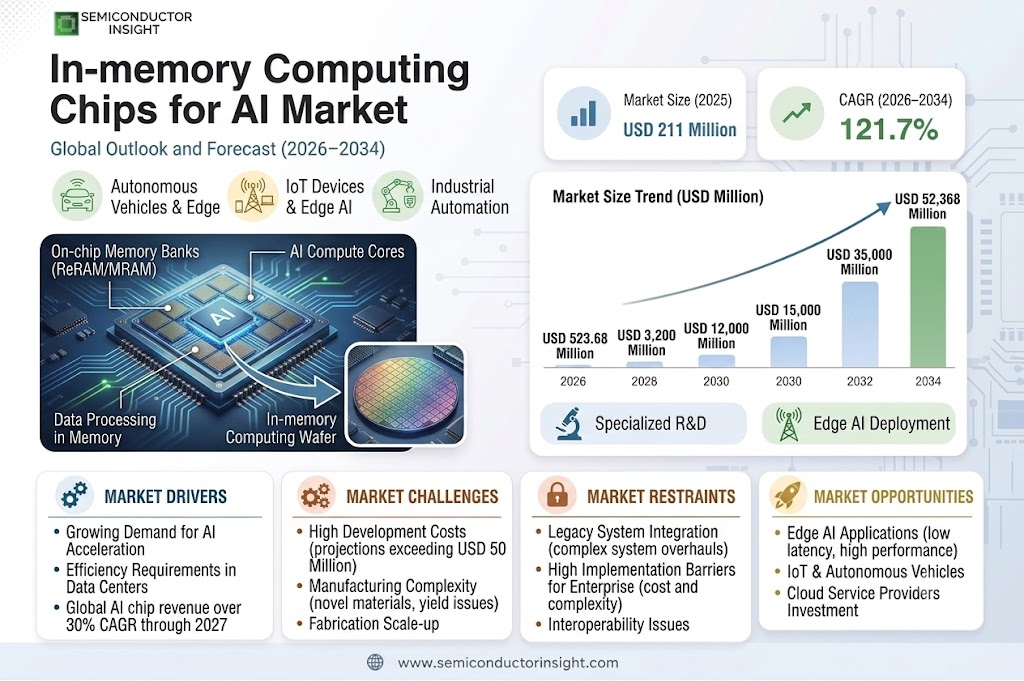

Global In-memory Computing Chips for AI Market size was valued at USD 211 million in 2025. The market is projected to grow from USD 523.68 million in 2026 to USD 52,368 million by 2034, exhibiting a CAGR of 121.7% during the forecast period.

In-memory Computing Chips for AI Market are specialized semiconductor devices designed to perform artificial intelligence computations directly within memory arrays, eliminating the need for data movement between separate processing units. These chips leverage SRAM, DRAM, or emerging non-volatile memory technologies like ReRAM and MRAM to execute neural network operations with significantly reduced energy consumption and latency compared to traditional von Neumann architectures.

The market growth is primarily driven by escalating demand for energy-efficient AI inference solutions across edge computing applications, where power constraints and real-time processing requirements make conventional GPU architectures impractical. Recent technological breakthroughs in analog computing-in-memory designs and increasing investments from major semiconductor manufacturers are accelerating commercialization efforts, though challenges remain in achieving manufacturing consistency and software ecosystem maturity for widespread adoption.

MARKET DRIVERS

Growing Demand for AI Acceleration

The increasing adoption of artificial intelligence across industries is driving demand for In-memory Computing Chips for AI Market. These specialized processors reduce latency by processing data directly in memory, enabling real-time decision-making in AI applications. Global AI chip revenue is projected to grow at over 30% CAGR through 2027.

Efficiency Requirements in Data Centers

Data centers are adopting in-memory computing chips to address the power consumption challenges of traditional AI computation. These chips can deliver 10x-100x improvements in energy efficiency compared to conventional architectures, making them critical for sustainable AI infrastructure.

The combination of improved performance and energy savings is creating strong market pull from cloud providers and hyperscalers investing heavily in AI infrastructure.

MARKET CHALLENGES

High Development Costs

The specialized nature of In-memory Computing Chips for AI Market creates significant R&D barriers. Developing new architectures requires substantial investment in both design and manufacturing processes, with prototyping costs often exceeding USD 50 million.

Other Challenges

Manufacturing Complexity

Fabricating in-memory computing chips at scale presents yield challenges due to the integration of novel materials and 3D architectures required for optimal performance.

MARKET RESTRAINTS

Legacy System Integration

Adoption of in-memory computing chips for AI faces constraints from existing infrastructure. Enterprises may hesitate to invest in new architectures that require complete system overhauls, especially when their current AI workloads run adequately on conventional processors.

MARKET OPPORTUNITIES

Edge AI Applications

The growth of edge computing presents significant potential for In-memory Computing Chips for AI Market. These processors’ ability to deliver high performance with low power consumption makes them ideal for AI applications in IoT devices, autonomous vehicles, and industrial automation systems at the network edge.

In-memory Computing Chips for AI Market Trends

Accelerated Adoption in Edge AI Applications

In-memory Computing Chips for AI Market is witnessing significant traction in edge AI deployments, where power efficiency and low latency are critical. These specialized chips reduce energy consumption by 60-80% compared to traditional architectures, making them ideal for smart sensors, robotics, and IoT devices. Major semiconductor foundries are collaborating with startups to optimize fabrication processes for mass production.

Other Trends

Transition from Prototyping to Commercial Scaling

While initial implementations were limited to research labs and pilot projects, commercial deployments are now expanding in automotive ADAS and industrial automation. Foundry partners report a 300% increase in tape-outs for analog CIM designs since 2023, signaling maturing manufacturing readiness.

Memory Technology Diversification

The market is seeing parallel development across multiple memory technologies – with SRAM-based designs dominating early shipments but emerging ReRAM solutions gaining traction for higher density applications. Memory vendors are allocating 15-20% of R&D budgets to non-volatile CIM architectures targeting data center inference workloads.

Software Ecosystem Development

Toolchain maturity remains a bottleneck, but cross-industry consortia have standardized three major compiler frameworks in 2024. Leading AI framework providers now offer native support for CIM execution modes, reducing deployment barriers.

Geographic Market Expansion

North America currently leads in design activity, but Asia-Pacific adoption is accelerating with government-backed semiconductor initiatives. China’s national IC fund has prioritized CIM development, with 12 domestic startups reaching volume production since Q3 2023.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Partnerships Drive Early-Stage Market Growth

In-memory Computing Chips for AI Market is currently led by specialized semiconductor startups and memory manufacturers developing novel architectures. Samsung and SK Hynix leverage their memory technology expertise to pioneer commercial solutions, while fabless startups like Mythic and Syntiant focus on ultra-low-power AI inference chips. The competitive environment remains highly collaborative, with strategic alliances between memory vendors, foundries, and AI accelerator firms to address manufacturing challenges.

Emerging players are targeting niche applications with differentiated approaches: Graphcore and D-Matrix focus on high-performance computing, while Axelera AI and EnCharge AI optimize for edge deployment. Chinese firms like Witmem and Yizhu Intelligent Technology are gaining traction in domestic markets through government-backed initiatives. The ecosystem also includes research-driven companies such as Beijing Houmo Technology developing analog in-memory computing solutions.

List of Key In-memory Computing Chips for AI Market Companies Profiled

- Samsung

- SK Hynix

- Syntiant

- D-Matrix

- Mythic

- Graphcore

- EnCharge AI

- Axelera AI

- Hangzhou Zhicun (Witmem) Technology

- Suzhou Yizhu Intelligent Technology

- Shenzhen Reexen Technology

- Beijing Houmo Technology

- AistarTek

- Beijing Pingxin Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CIM chips are emerging as the dominant architecture for AI acceleration due to:

|

| By Application |

|

Edge AI Devices represent the most promising application segment because:

|

| By End User |

|

Semiconductor Vendors are driving innovation through:

|

| By Memory Technology |

|

Emerging NVM technologies show strong potential because:

|

| By Deployment Mode |

|

Embedded Solutions are gaining traction due to:

|

Regional Analysis: In-memory Computing Chips for AI Market

North America

The Boston-Seattle-San Francisco triangle forms North America’s primary innovation hub for in-memory AI chips, combining academic research (MIT, Stanford) with corporate R&D centers. This concentration facilitates rapid commercialization of new architectures and frequent technological breakthroughs in processing efficiency.

Financial services and tech companies particularly favor in-memory computing for real-time fraud detection and recommendation systems. The region’s mature digital infrastructure enables seamless integration of novel chip architectures into existing AI workflows across multiple industry verticals.

Government programs like the CHIPS Act provide funding for domestic in-memory computing chip development, addressing supply chain concerns. Patent laws and trade policies protect intellectual property while encouraging cross-border technology transfers under controlled conditions.

Top-tier engineering schools produce specialized graduates in neuromorphic computing and chip design. Tech companies maintain aggressive recruitment from these programs, ensuring a steady flow of expertise to advance in-memory computing solutions for complex AI workloads.

Europe

Europe demonstrates strong growth in in-memory computing chips for AI, driven by automotive and industrial automation sectors. German and French semiconductor initiatives foster local chip ecosystems, while the EU’s digital sovereignty agenda prioritizes alternative computing architectures. Research institutions focus on energy-efficient designs suitable for edge AI applications, with particular emphasis on automotive AI processors. Strict data regulations encourage adoption of chips with built-in privacy features, giving European manufacturers a unique market position.

Asia-Pacific

The Asia-Pacific region emerges as the fastest-growing market, with China, South Korea, and Japan investing heavily in memory-centric AI processors. Chinese tech giants develop proprietary in-memory computing solutions to bypass Western chip restrictions, while Japanese firms excel in precision manufacturing. South Korea leverages its memory production leadership to develop next-generation hybrid chips. India’s expanding AI startups create new demand for cost-effective in-memory computing solutions.

Middle East & Africa

Gulf nations invest strategically in AI infrastructure, adopting in-memory computing for smart city projects and oil/gas predictive analytics. Special economic zones attract chip designers with favorable policies. Africa shows nascent adoption, with South Africa and Kenya piloting AI applications using imported in-memory processors for healthcare and agricultural analytics.

South America

Brazil leads regional adoption of in-memory computing chips for agricultural AI and fintech applications. Government-backed technology parks encourage local startups to develop specialized AI accelerators. Chile and Argentina focus on mining sector applications, though market growth remains constrained by infrastructure limitations and access to advanced manufacturing capabilities.

Report Scope

This market research report provides a comprehensive analysis of the Global In-memory Computing Chips for AI Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of In-memory Computing Chips for AI Market?

-> In-memory Computing Chips for AI Market size was valued at USD 211 million in 2025. The market is projected to grow from USD 523.68 million in 2026 to USD 52,368 million by 2034, exhibiting a CAGR of 121.7% during the forecast period.

What is the growth rate (CAGR) of the In-memory Computing Chips for AI Market?

-> The market is expected to grow at a CAGR of 121.7% during the forecast period (2025-2032).

Which key companies operate in In-memory Computing Chips for AI Market?

-> Key players include Samsung, SK Hynix, Syntiant, D-Matrix, Mythic, Graphcore, EnCharge AI, Axelera AI, Hangzhou Zhicun (Witmem) Technology, and Suzhou Yizhu Intelligent Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient AI inference, edge-AI applications, and the need to overcome memory bandwidth limitations of traditional architectures.

Which region dominates the market?

-> Asia is the dominant market, with key contributions from China, Japan, and South Korea.

What are the key applications of In-memory Computing Chips for AI Market?

-> Key applications include edge AI devices, robotics, smart cameras, industrial automation, and IoT solutions where power efficiency and low latency are critical.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...