MARKET INSIGHTS

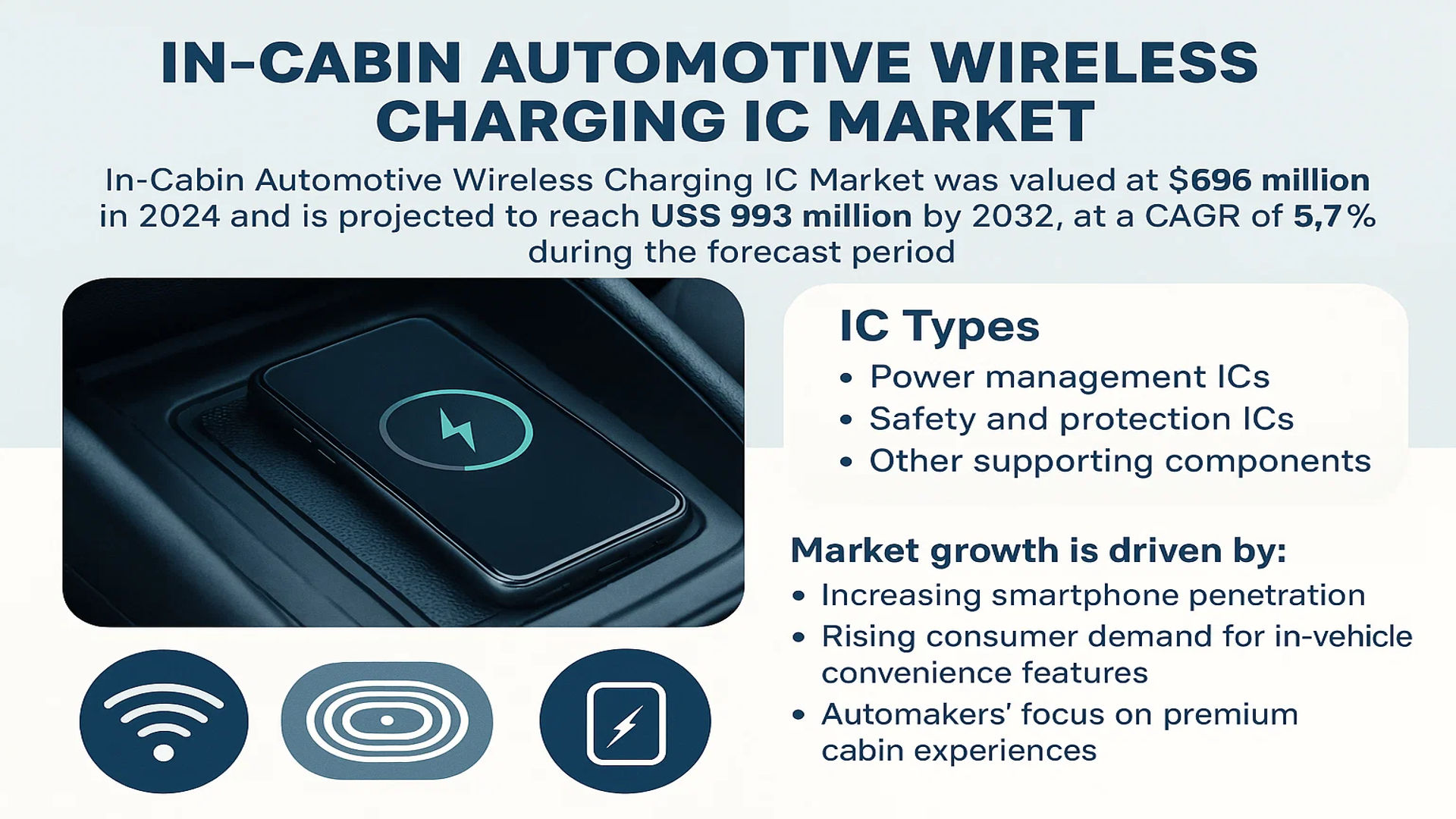

The global In-Cabin Automotive Wireless Charging IC Market was valued at 696 million in 2024 and is projected to reach US$ 993 million by 2032, at a CAGR of 5.7% during the forecast period.

In-cabin automotive wireless charging ICs are specialized integrated circuits designed to facilitate wireless power transfer within vehicle cabins for smartphones, smartwatches, and other portable devices. These components eliminate the need for physical charging cables while maintaining compatibility with Qi and other wireless charging standards. The market includes key IC types such as power management ICs, safety and protection ICs, and other supporting components.

Market growth is driven by increasing smartphone penetration, rising consumer demand for in-vehicle convenience features, and automakers’ focus on premium cabin experiences. While North America and Europe currently lead adoption, Asia-Pacific shows the fastest growth potential due to expanding automotive production in China and India. Major players like Infineon, NXP, and Texas Instruments continue to innovate, with recent developments focusing on higher efficiency (up to 80% power transfer) and multi-device charging solutions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Smartphone Integration and Wireless Charging Standardization to Accelerate Market Growth

The proliferation of smartphones with built-in wireless charging capabilities is driving significant demand for in-cabin automotive wireless charging ICs. Over 60% of premium smartphones now support Qi wireless charging, creating a strong pull-through effect in the automotive sector. Automakers are responding by integrating wireless charging pads as standard or optional features across vehicle segments, particularly in luxury models where adoption currently exceeds 80%. Furthermore, the consolidation around the Qi standard has simplified implementation for both device manufacturers and automakers, reducing compatibility concerns that previously hindered adoption.

Growing Demand for Premium In-Car Experiences to Boost Market Expansion

Consumer expectations for seamless connectivity and convenience features are reshaping automotive interiors. The global automotive infotainment market, valued at over $20 billion, continues to grow rapidly, with wireless charging becoming a key differentiator in vehicle purchase decisions. Nearly 75% of new vehicle buyers consider wireless charging capability an important feature, according to recent consumer surveys. This demand is prompting automakers to integrate more sophisticated charging solutions that maintain signal integrity even when multiple devices are charging simultaneously – a technical challenge that advanced IC designs are overcoming through improved electromagnetic interference management.

Electric Vehicle Adoption and Smart Cabin Trends to Drive Future Growth

The rapid electrification of vehicle fleets presents substantial growth opportunities for in-cabin wireless charging solutions. Electric vehicle manufacturers are particularly focused on creating technologically advanced cabins that maximize user convenience, often incorporating multiple wireless charging zones. With global EV sales projected to reach 45 million units annually by 2030, this represents a significant addressable market. Moreover, the integration of wireless charging with emerging smart cabin ecosystems – including digital keys, voice assistants, and IoT connectivity – is creating additional demand for more sophisticated ICs that can handle higher power levels while maintaining thermal efficiency.

MARKET RESTRAINTS

High Development and Integration Costs to Limit Market Penetration

While the technology offers significant convenience benefits, the high cost of developing and integrating wireless charging ICs remains a substantial barrier to broader adoption. The sophisticated semiconductor designs required for automotive-grade solutions can be up to 50% more expensive than consumer-grade alternatives, factoring in the need for extended temperature range operation, vibration resistance, and long-term reliability. These cost factors limit adoption primarily to premium vehicle segments, with fewer than 30% of mid-range vehicles currently offering the feature even as an option.

Other Restraints

Thermal Management Challenges

Efficient thermal dissipation remains a significant technical hurdle, particularly as power requirements increase to accommodate faster charging speeds. ICs must balance charging efficiency with temperature control to prevent overheating, requiring complex thermal management solutions that add to both cost and design complexity.

Standardization Limitations

While Qi has emerged as the dominant standard, ongoing refinements to the specification and the emergence of alternative standards create integration challenges that can slow adoption cycles. Automotive development timelines, which typically span 3-5 years, must carefully account for potential standard evolutions during the vehicle design phase.

MARKET CHALLENGES

Technical Complexities in Multi-Device Charging Scenarios to Create Performance Hurdles

As consumers expect to charge multiple devices simultaneously – often including smartphones, wearables, and tablets – the technical challenges multiply significantly. Current IC designs struggle with cross-device interference, with efficiency often dropping by 30-40% when charging more than one device concurrently. This performance degradation creates user experience issues that automakers are working to address through more advanced coil designs and intelligent power management algorithms at the IC level.

Other Challenges

Electromagnetic Compatibility Requirements

Stringent automotive EMC standards require careful engineering to prevent interference with other vehicle systems. The increasing density of electronic components in modern vehicles makes this particularly challenging, often requiring multiple design iterations to meet all regulatory requirements while maintaining charging performance.

Power Delivery Limitations

Vehicle electrical systems typically provide 12V power, while newer fast charging standards require higher voltage conversion. This creates efficiency losses at the IC level that must be carefully managed to deliver acceptable charging speeds without overtaxing vehicle electrical systems.

MARKET OPPORTUNITIES

Emerging High-Power Wireless Charging Standards to Unlock New Applications

The development of high-power wireless charging standards capable of delivering 30W or more presents significant growth opportunities for IC manufacturers. These next-generation solutions will enable faster device charging and potentially power larger devices like laptops in vehicle cabins. Early implementations in premium vehicles have demonstrated the technical feasibility, though widespread adoption awaits cost reductions through economies of scale and manufacturing process improvements.

Integration with Vehicle-to-Device Ecosystems to Create Additional Value

Forward-looking automakers are exploring deeper integration between wireless charging systems and vehicle infotainment/connectivity platforms. Future IC designs may incorporate features like device recognition for personalized settings activation, or secure communication channels for digital key functionality. These value-added capabilities could command premium pricing while differentiating vehicle brands in competitive markets.

Expansion into Fleet and Commercial Vehicle Segments to Diversify Market Base

While currently concentrated in passenger vehicles, wireless charging technology is finding new applications in commercial and fleet vehicles where driver connectivity and device power needs are equally important. Ride-hailing services and delivery fleets particularly value solutions that keep drivers’ devices charged without cable clutter, representing a growing market segment that could account for 15-20% of total adoption by 2030.

IN-CABIN AUTOMOTIVE WIRELESS CHARGING IC MARKET TRENDS

Shift Toward High-Efficiency Wireless Charging Solutions Driving Market Growth

The global in-cabin automotive wireless charging IC market is experiencing robust growth, propelled by rising consumer demand for seamless device charging in vehicles. The market was valued at $696 million in 2024 and is projected to reach $993 million by 2032, registering a steady CAGR of 5.7% during the forecast period. Automotive manufacturers are increasingly integrating wireless charging solutions to enhance user convenience, particularly in premium and mid-range vehicles. Recent advancements in power management ICs and Qi wireless charging standards (up to 15W) have significantly improved charging efficiency, reducing heat dissipation issues and optimizing energy transfer, which has accelerated adoption rates.

Other Trends

Expansion of Smartphone Compatibility

The growing compatibility of wireless charging ICs with flagship smartphones from Apple, Samsung, and Xiaomi is bolstering market demand. Over 80% of premium smartphones now support Qi-based wireless charging, driving automakers to integrate in-cabin solutions as a standard feature. Furthermore, the rise of electric vehicles (EVs)—projected to account for 35% of new car sales by 2030—has amplified the need for advanced in-cabin technologies, including wireless charging, as part of a broader push toward connected and automated vehicle ecosystems.

Integration of Safety and Protection ICs Mitigating Risks

The market is witnessing increasing adoption of safety and protection ICs to address concerns such as overvoltage, overheating, and electromagnetic interference (EMI). Automotive-grade ICs now incorporate multi-layered protection mechanisms, including foreign object detection (FOD) and temperature control, ensuring compliance with stringent automotive safety standards like AEC-Q100. Key players such as Infineon, NXP, and Texas Instruments are investing in R&D to enhance the reliability of these ICs, particularly for high-power applications. This trend aligns with the broader industry focus on reducing in-cabin electronic failures, which account for nearly 12% of automotive warranty claims related to infotainment systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Drive Innovation and Expand Market Presence in In-Cabin Wireless Charging ICs

The global in-cabin automotive wireless charging IC market is characterized by a mix of established semiconductor leaders and emerging specialized players. Infineon Technologies and STMicroelectronics currently dominate the market, jointly holding nearly 30% revenue share as of 2024. Their lead stems from longstanding relationships with automotive OEMs and comprehensive solutions that integrate power management with vehicle connectivity systems.

Meanwhile, Texas Instruments and NXP Semiconductors have been gaining traction through their focus on high-efficiency designs compatible with multiple charging standards. These companies benefit from their ability to deliver complete reference designs that reduce development time for tier-1 suppliers and automakers.

Asian manufacturers like Renesas Electronics and ROHM Semiconductor are expanding aggressively, particularly in the cost-sensitive mid-range vehicle segment. Their growth strategy emphasizes localization and customization for regional automotive markets while maintaining compliance with global safety regulations.

Innovation and Partnerships Shape Market Dynamics

The competitive landscape is evolving rapidly as companies invest in next-generation technologies. Several key developments emerged in 2024:

- Infineon launched its new 15W multi-coil reference design, improving charging efficiency by 12% compared to previous generations

- NXP expanded its automotive wireless charging portfolio with integrated NFC pairing capabilities

- Startups like NuVolta Technologies secured major design wins with Chinese EV manufacturers through innovative thermal management solutions

Strategic alliances are also reshaping the market. Recent partnerships between semiconductor companies and automakers focus on developing vehicle-specific charging solutions that integrate seamlessly with infotainment systems and battery management technologies.

List of Key In-Cabin Automotive Wireless Charging IC Manufacturers

- Infineon Technologies (Germany)

- STMicroelectronics (Switzerland)

- Texas Instruments (U.S.)

- Renesas Electronics (Japan)

- indie Semiconductor (U.S.)

- NXP Semiconductors (Netherlands)

- Broadcom (U.S.)

- ROHM Semiconductor (Japan)

- NuVolta Technologies (China)

- ConvenientPower Semiconductor (China)

- Maxic Technology (Taiwan)

- Shenzhen Injoinic Technology (China)

Segment Analysis:

By Type

Power Management IC Segment Leads Due to Critical Role in Efficient Energy Conversion

The market is segmented based on type into:

- Power Management IC

- Subtypes: Voltage regulators, battery management ICs, and others

- Safety and Protection IC

- Subtypes: Overvoltage protection, overcurrent protection, and others

- Radio Frequency (RF) ICs

- Others

By Application

Smartphones Segment Dominates with High Demand for Connectivity Solutions

The market is segmented based on application into:

- Smartphones

- Smart Watches

- Tablets

- In-Vehicle Infotainment Systems

- Others

By Technology

Qi Standard Segment Prevails as Industry Norm for Wireless Charging

The market is segmented based on technology into:

- Qi Standard

- PMA Standard

- AirFuel Alliance Standard

- Others

By Vehicle Type

Passenger Vehicles Segment Leads With Higher Adoption Rates

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Luxury Vehicles

Regional Analysis: In-Cabin Automotive Wireless Charging IC Market

Asia-Pacific

The Asia-Pacific region dominates the global in-cabin wireless charging IC market, driven primarily by China’s booming automotive industry and rapid adoption of electric vehicles (EVs). With major semiconductor manufacturers like Renesas, STMicroelectronics, and local players such as Southchip Semiconductor operating in the region, the supply chain is well-established. China’s push for smart mobility solutions has accelerated the integration of wireless charging in vehicles, with domestic OEMs leading the adoption curve. Japan follows closely with advanced R&D in power management ICs, while India’s growing middle class and smartphone penetration create substantial demand. However, cost sensitivity in price-conscious markets remains a challenge for premium wireless charging solutions.

North America

North America represents the second-largest market for in-cabin wireless charging ICs, where automotive technology adoption is driven by consumer demand for convenience features and stringent safety standards. The U.S. accounts for nearly 85% of regional revenue, with Texas Instruments, NXP, and Broadcom being key suppliers. The region’s leadership in electric vehicles (Tesla, Ford, GM) and tech-savvy consumer base fuels demand for advanced charging solutions. While adoption is slower in Canada due to longer vehicle replacement cycles, the overall market benefits from automakers prioritizing wireless charging as a standard feature in mid-to-high-end vehicles. Regulatory support for EV infrastructure further propels market growth.

Europe

Europe’s market is characterized by premium automakers (BMW, Mercedes-Benz, Volkswagen) integrating wireless charging as a value-added feature. With EU regulations pushing for standardized charging solutions and Infineon leading IC development, the region maintains strong technological capabilities. Germany remains the largest market, accounting for over 30% of regional demand, followed by the UK and France. The focus on luxury vehicles and growing EV production accelerates wireless charging adoption, though economic uncertainties and high component costs temporarily hinder mass-market penetration. Recent partnerships between automakers and semiconductor companies aim to develop more cost-effective solutions for broader vehicle segments.

Middle East & Africa

The MEA region shows emerging potential, particularly in GCC countries where luxury vehicle penetration is high. While the overall market remains small, premium car brands drive initial adoption in countries like UAE and Saudi Arabia. Local manufacturing is nearly nonexistent, relying entirely on imports from European and Asian suppliers. South Africa presents moderate growth opportunities through its established automotive sector, though economic constraints limit widespread adoption. Infrastructure limitations and low consumer awareness currently restrict market expansion, but long-term growth is anticipated as regional EV initiatives gain traction.

South America

South America represents the smallest regional market, hindered by economic volatility and low vehicle electrification rates. Brazil accounts for most demand through its sizeable automotive industry, though wireless charging remains limited to premium imported vehicles. Argentina shows marginal growth, primarily in Buenos Aires’ luxury vehicle segment. The lack of local IC production and dependence on costly imports create price barriers, while currency fluctuations further complicate market stability. However, gradual improvements in consumer electronics adoption and potential EV investments could stimulate future market development.

Report Scope

This market research report provides a comprehensive analysis of the global In-Cabin Automotive Wireless Charging IC market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 696 million in 2024 and is projected to reach USD 993 million by 2032, growing at a CAGR of 5.7%.

- Segmentation Analysis: Detailed breakdown by product type (Power Management IC, Safety and Protection IC, Others), application (Smart Phones, Smart Watches, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading market participants including Infineon, STMicroelectronics, Texas Instruments, Renesas, and NXP, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging wireless charging standards, integration with vehicle infotainment systems, and efficiency improvements in power management ICs.

- Market Drivers & Restraints: Evaluation of factors such as increasing smartphone penetration, demand for connected vehicles, and challenges related to charging efficiency and standardization.

- Stakeholder Analysis: Strategic insights for automotive OEMs, semiconductor manufacturers, and technology providers regarding market opportunities and competitive positioning.

The research employs primary and secondary methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global In-Cabin Automotive Wireless Charging IC Market?

-> In-Cabin Automotive Wireless Charging IC Market was valued at 696 million in 2024 and is projected to reach US$ 993 million by 2032, at a CAGR of 5.7% during the forecast period.

Which key companies operate in this market?

-> Key players include Infineon, STMicroelectronics, Texas Instruments, Renesas, NXP, Broadcom, and emerging players like NuVolta and ConvenientPower Semiconductor.

What are the key growth drivers?

-> Growth is driven by rising smartphone adoption, increasing demand for connected vehicles, and OEM focus on enhanced in-cabin experiences.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America and Europe lead in technology adoption.

What are the emerging trends?

-> Emerging trends include higher power charging solutions, integration with vehicle systems, and multi-device charging capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...