MARKET INSIGHTS

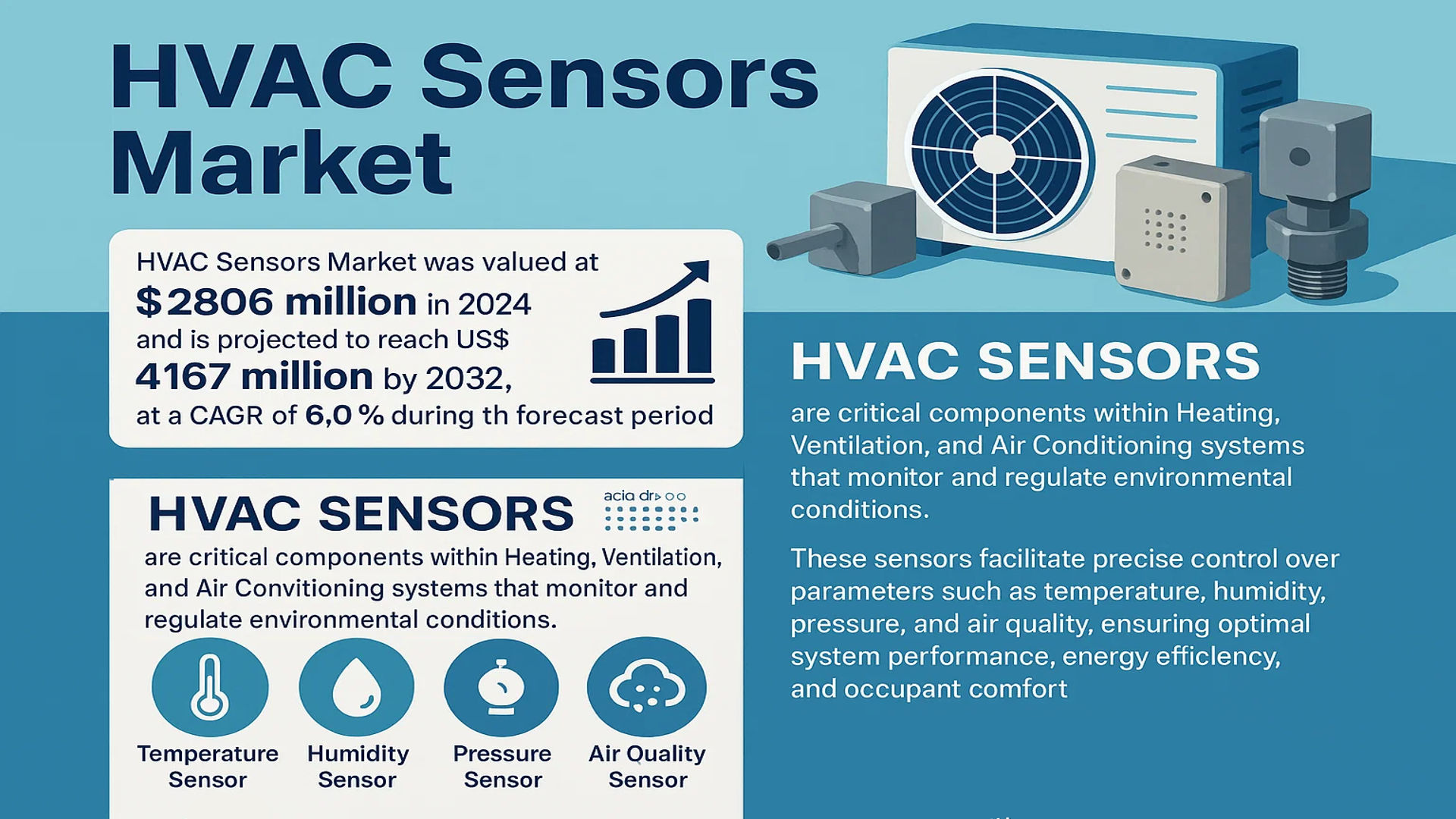

The global HVAC Sensors Market was valued at 2806 million in 2024 and is projected to reach US$ 4167 million by 2032, at a CAGR of 6.0% during the forecast period.

HVAC Sensors are critical components within Heating, Ventilation, and Air Conditioning systems that monitor and regulate environmental conditions. These sensors facilitate precise control over parameters such as temperature, humidity, pressure, and air quality, ensuring optimal system performance, energy efficiency, and occupant comfort. The primary types include Temperature Sensors, Humidity Sensors, Pressure Sensors, Air Quality Sensors, and others.

The market is experiencing steady growth driven by factors such as increasing global demand for energy-efficient building management systems, stringent government regulations on building emissions, and the rising adoption of smart and connected HVAC systems. Furthermore, the push towards improved indoor air quality, particularly in commercial and residential spaces, is significantly contributing to market expansion. Key players like Siemens AG, which held a 15% market share in 2016, along with Schneider Electric and Johnson Controls, continue to innovate and expand their product portfolios to capture greater market share.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Energy Efficiency Regulations and Green Building Standards to Drive Market Expansion

Global emphasis on energy conservation and sustainability is significantly accelerating HVAC sensor adoption. Regulatory frameworks mandating improved energy performance in buildings are compelling stakeholders to integrate advanced sensing technologies. The commercial building sector, which accounts for over 40% of global energy consumption, is particularly affected by these regulations. Building energy management systems increasingly rely on precise environmental monitoring through temperature, humidity, and air quality sensors to optimize HVAC operation. Recent updates to international building codes require real-time monitoring and automated control systems, creating substantial demand for sensor technologies that can deliver accurate data for energy optimization algorithms.

Rising Demand for Smart Building Automation and IoT Integration to Fuel Growth

The proliferation of smart building technologies and IoT-enabled HVAC systems is creating robust demand for advanced sensor solutions. Modern building automation systems require continuous environmental data streams to maintain optimal conditions while minimizing energy consumption. The integration of wireless sensor networks allows for comprehensive spatial monitoring without extensive wiring infrastructure, reducing installation costs by approximately 30-40%. These systems enable predictive maintenance capabilities, with sensors detecting performance degradation before system failures occur. The commercial sector’s rapid adoption of Building Management Systems (BMS), which grew by over 15% annually in recent years, directly correlates with increased sensor deployment across HVAC applications.

Furthermore, the convergence of HVAC systems with broader smart building ecosystems creates additional value propositions. Sensors originally deployed for climate control are increasingly being utilized for occupancy monitoring, space utilization analytics, and air quality management, providing building operators with multifaceted data streams from single installation points.

➤ For instance, major technology companies have launched integrated building platforms that utilize HVAC sensor data for multiple building management functions, creating additional justification for sensor deployment beyond traditional climate control applications.

The ongoing digital transformation in building management, coupled with rising tenant expectations for environmental quality, ensures sustained market momentum for advanced HVAC sensing solutions across all building categories.

MARKET CHALLENGES

High Initial Investment and Installation Complexity to Impede Market Penetration

While the long-term benefits of advanced HVAC sensors are well-documented, the substantial upfront costs present significant adoption barriers, particularly in price-sensitive market segments. High-precision sensors with advanced communication capabilities can cost 2-3 times more than basic alternatives, creating resistance among budget-conscious building owners. The installation process often requires specialized technicians and potential system modifications, adding both time and expense to deployment. In retrofit applications, which represent approximately 65% of the market opportunity, integration with existing HVAC infrastructure presents particular technical and financial challenges that can deter investment decisions.

Other Challenges

Interoperability Issues

The lack of standardized communication protocols across different manufacturers creates integration difficulties that hinder market growth. Building operators frequently encounter compatibility problems when attempting to mix sensors from various vendors, leading to increased system complexity and maintenance requirements. This fragmentation forces customers to choose between limited ecosystem options or accept suboptimal integration, potentially delaying technology adoption decisions.

Technical Reliability Concerns

Performance degradation and calibration drift in harsh HVAC environments raise concerns about long-term sensor accuracy. Environmental factors including temperature extremes, humidity variations, and airborne contaminants can affect sensor performance over time, necessitating frequent maintenance and recalibration. These reliability issues create operational uncertainties that may lead specifiers to choose more conservative, albeit less efficient, system designs.

MARKET RESTRAINTS

Economic Volatility and Construction Sector Fluctuations to Moderate Growth Pace

Macroeconomic uncertainties and cyclical patterns in construction activity directly impact HVAC sensor market performance. During economic downturns or construction slowdowns, building projects face delays or scope reductions, affecting sensor procurement decisions. The commercial construction sector, which represents the largest application segment, experienced project deferrals and cancellations during recent economic uncertainties, creating demand volatility for associated HVAC components. This sensitivity to economic conditions creates unpredictable demand patterns that complicate manufacturing planning and inventory management across the supply chain.

Additionally, budget constraints during economic contractions often lead building owners to prioritize essential expenditures over advanced system upgrades. While HVAC sensors provide operational benefits, they are frequently categorized as discretionary improvements rather than essential infrastructure, making them vulnerable to budget cuts during financial uncertainty. This perception challenge, combined with the capital-intensive nature of building projects, moderates market growth during periods of economic instability.

MARKET OPPORTUNITIES

Emerging Applications in Health and Wellness Monitoring to Create New Growth Frontiers

The growing emphasis on indoor environmental quality and occupant health presents substantial expansion opportunities for HVAC sensor technologies. Beyond traditional climate control, sensors are increasingly deployed for monitoring airborne pathogens, particulate matter, and volatile organic compounds. The global focus on health-conscious building design has accelerated demand for comprehensive air quality monitoring systems that integrate multiple sensor types. This trend has gained particular momentum following increased awareness of ventilation importance in disease transmission prevention, creating new application scenarios for advanced sensor deployments.

Furthermore, the integration of HVAC sensors with broader digital twin and building analytics platforms opens additional revenue streams. Sensor data becomes increasingly valuable when aggregated and analyzed for pattern recognition, predictive maintenance, and operational optimization. Major building technology providers are developing analytics services that leverage sensor data for value-added insights, creating opportunities for sensor manufacturers to participate in service-based revenue models beyond hardware sales.

Additionally, regulatory developments emphasizing building health performance and sustainability reporting requirements are expected to drive sensor adoption. Compliance with emerging building health standards and certification programs increasingly requires verifiable environmental data, creating mandated demand for monitoring technologies that can provide auditable performance records.

HVAC SENSORS MARKET TRENDS

Integration of IoT and Smart Building Technologies to Emerge as a Dominant Trend

The proliferation of the Internet of Things (IoT) and the accelerated adoption of smart building solutions are fundamentally reshaping the HVAC sensors landscape. Modern building management systems now demand a network of interconnected sensors that provide real-time, granular data on environmental conditions. This connectivity enables predictive maintenance, where anomalies detected by pressure or temperature sensors can trigger automated service requests before system failures occur, significantly reducing downtime and operational costs. Furthermore, the push towards energy efficiency, driven by stringent global regulations and corporate sustainability goals, is mandating the use of high-precision sensors. For instance, advanced air quality sensors that monitor CO2 and volatile organic compound (VOC) levels are becoming standard in commercial spaces to ensure optimal indoor air quality and occupant health, a concern magnified by recent global health awareness. This trend is not merely about data collection but about creating intelligent, self-regulating environments that optimize energy consumption while maximizing comfort.

Other Trends

Miniaturization and Enhanced Sensor Capabilities

The relentless drive towards miniaturization is producing sensors that are smaller, more power-efficient, and capable of measuring multiple parameters simultaneously. These multi-functional sensors, which can combine temperature, humidity, and pressure sensing into a single compact unit, are critical for space-constrained applications in modern HVAC systems, particularly in variable refrigerant flow (VRF) systems and compact air handling units. This technological evolution allows for more flexible system design and installation while reducing the overall component count and potential points of failure. The enhanced accuracy of these devices, often boasting deviations of less than ±0.5°C for temperature and ±2% RH for humidity, provides the precise data necessary for the sophisticated algorithms that control modern, high-efficiency HVAC equipment. This trend is directly supporting the growth of complex HVAC applications in data centers and pharmaceutical manufacturing, where environmental stability is non-negotiable.

Rising Demand in the Industrial and Logistics Sectors

Beyond commercial and residential applications, the industrial and transportation & logistics sectors are exhibiting robust growth in HVAC sensor adoption. In industrial settings, maintaining specific environmental conditions is crucial for manufacturing processes, product integrity, and worker safety. For example, in pharmaceutical and food production, stringent regulations require continuous monitoring and logging of temperature and humidity, creating a sustained demand for highly reliable and often certified sensors. Similarly, the transportation and logistics sector, which accounts for approximately 17% of the market, relies heavily on sensor technology to protect perishable goods and sensitive electronics during transit. The expansion of cold chain logistics, vital for the global distribution of vaccines and fresh produce, is a key driver here. This sector’s growth is further amplified by the global expansion of e-commerce, which necessitates a larger and more sophisticated network of warehouses and distribution centers, all requiring precise climate control systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Drive Market Leadership

The global HVAC sensors market exhibits a semi-consolidated structure, characterized by the presence of multinational industrial conglomerates alongside specialized sensor manufacturers and numerous smaller regional players. This dynamic creates a competitive environment where technological prowess, extensive distribution networks, and deep industry expertise are paramount. Siemens AG has consistently maintained a dominant position, leveraging its comprehensive building automation portfolio and global service infrastructure. Historical data indicates Siemens held approximately 15% of the global market share in sales, a testament to its entrenched position across commercial and industrial applications worldwide.

Schneider Electric and Johnson Controls are other pivotal contenders, holding significant market shares estimated at around 13% and 11% respectively. Their growth is heavily driven by integrated offerings that combine sensors with broader building management systems (BMS) and energy efficiency solutions, which are increasingly in demand. These companies compete not just on product features but on their ability to provide holistic, data-driven building optimization, making their sensor portfolios a critical component of a larger ecosystem.

Furthermore, these established players are actively engaged in strategic initiatives to fortify their standing. This includes significant investments in research and development for next-generation IoT-enabled and wireless sensors, along with strategic mergers and acquisitions to acquire novel technologies and expand their geographical footprint. Such moves are crucial for capturing growth in emerging markets and new application segments.

Meanwhile, other key participants like Honeywell International Inc. and Emerson Electric are strengthening their market presence through a focus on high-reliability products for critical environments and strategic partnerships with HVAC OEMs. Companies such as Sensirion AG compete by providing highly specialized, advanced sensing components, particularly in the air quality and humidity segments, to both end-users and other larger players in the market. This ensures a continuous cycle of innovation and competition across all tiers of the market.

List of Key HVAC Sensors Companies Profiled

- Siemens AG (Germany)

- Schneider Electric (France)

- Johnson Controls (Ireland)

- Honeywell International Inc. (U.S.)

- Sensata Technologies Inc. (U.S.)

- United Technologies Corporation (U.S.)

- Ingersoll Rand (U.S.)

- Emerson Electric (U.S.)

- Sensirion AG (Switzerland)

Segment Analysis:

By Type

Temperature Sensors Segment Commands Significant Market Share Owing to Fundamental Role in Climate Control

The market is segmented based on type into:

- Temperature Sensors

- Subtypes: Thermistors, Resistance Temperature Detectors (RTDs), Thermocouples, and others

- Humidity Sensors

- Pressure Sensors

- Subtypes: Absolute Pressure Sensors, Differential Pressure Sensors, Gauge Pressure Sensors, and others

- Air Quality Sensors

- Subtypes: CO2 Sensors, VOC Sensors, Particulate Matter Sensors, and others

- Others

By Application

Commercial Sector Leads the Market Fueled by Demand for Smart Building Management Systems

The market is segmented based on application into:

- Commercial

- Subtypes: Office Buildings, Retail Spaces, Healthcare Facilities, Hotels, and others

- Residential

- Industrial

- Subtypes: Manufacturing Plants, Warehouses, Cleanrooms, and others

- Transportation & Logistics

- Subtypes: Automotive HVAC, Railway Systems, Aircraft Environmental Control, and others

Regional Analysis: HVAC Sensors Market

North America

North America holds the largest market share for HVAC sensors, accounting for approximately 32% of global sales. This dominance is driven by stringent building codes and energy efficiency standards, such as those enforced by ASHRAE and the U.S. Department of Energy. The region’s mature commercial real estate sector, which constitutes 43% of global HVAC sensor applications, demands advanced building automation systems for optimal energy management and occupant comfort. Furthermore, the push towards smart buildings and the integration of IoT within HVAC systems in the United States and Canada fuels the adoption of sophisticated sensors, including air quality monitors and networked temperature sensors. Leading manufacturers like Johnson Controls and Honeywell International Inc. have a strong presence here, continuously innovating to meet the high standards for reliability and connectivity required by North American clients.

Europe

Europe represents a highly developed and regulation-driven market, accounting for 28.47% of global HVAC sensor sales. The region’s growth is heavily influenced by the EU’s stringent energy efficiency directives and environmental policies, such as the Energy Performance of Buildings Directive (EPBD). There is a significant focus on retrofitting existing building stock with modern, energy-saving HVAC controls, creating sustained demand for sensors. Temperature and humidity sensors are particularly prevalent, but there is growing emphasis on air quality sensors to ensure healthy indoor environments, especially in densely populated urban areas. Germany, France, and the U.K. are key markets, with major players like Siemens AG and Schneider Electric leading innovation in smart and sustainable building technologies.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for HVAC sensors, propelled by massive urbanization, rapid construction of commercial and residential spaces, and increasing industrialization, particularly in China and India. China alone accounts for 15% of the global market. While cost sensitivity can lead to a preference for basic sensor types, there is a clear and accelerating trend towards adopting more advanced, connected sensors to improve energy efficiency and meet green building standards. The sheer scale of new construction projects across the region presents immense opportunities for sensor manufacturers. However, the market is also highly competitive, with both global giants and local suppliers vying for market share.

South America

The South American HVAC sensors market, while smaller in global share at approximately 6%, shows potential for gradual growth. Economic volatility in key countries like Brazil and Argentina often constrains large-scale investments in advanced building technologies. Consequently, market growth is primarily driven by essential replacement demand and specific projects in the industrial and commercial sectors, rather than widespread new adoption. The focus tends to be on core, reliable temperature and pressure sensors, with slower uptake of premium air quality or smart networked sensors due to budget limitations and less stringent regulatory frameworks compared to North America or Europe.

Middle East & Africa

This region is an emerging market with distinct growth drivers, primarily centered around major urban development projects and extreme climatic conditions that necessitate robust HVAC systems. Nations like the UAE, Saudi Arabia, and Israel are investing significantly in smart city infrastructure and high-end commercial real estate, which drives demand for advanced HVAC controls and sensors. The market’s development is uneven, however, with progress often linked to oil-based economies and national development plans. While there is a recognized need for durable sensors capable of performing in harsh environments, market expansion can be hindered by economic diversification efforts and varying levels of infrastructural development across different countries.

Report Scope

This market research report provides a comprehensive analysis of the global and regional HVAC Sensors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global HVAC Sensors Market?

-> HVAC Sensors Market was valued at 2806 million in 2024 and is projected to reach US$ 4167 million by 2032, at a CAGR of 6.0% during the forecast period.

Which key companies operate in Global HVAC Sensors Market?

-> Key players include Siemens AG, Schneider Electric, Johnson Controls, Honeywell International Inc., and Sensata Technologies Inc., among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for energy-efficient buildings, stringent government regulations for indoor air quality, and the rapid growth of smart building infrastructure.

Which region dominates the market?

-> North America holds the largest market share at 32%, while Asia-Pacific is experiencing the fastest growth due to rapid urbanization and infrastructure development.

What are the emerging trends?

-> Emerging trends include integration of IoT and AI for predictive maintenance, development of wireless sensor networks, and increasing adoption of smart HVAC controls.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...