MARKET INSIGHTS

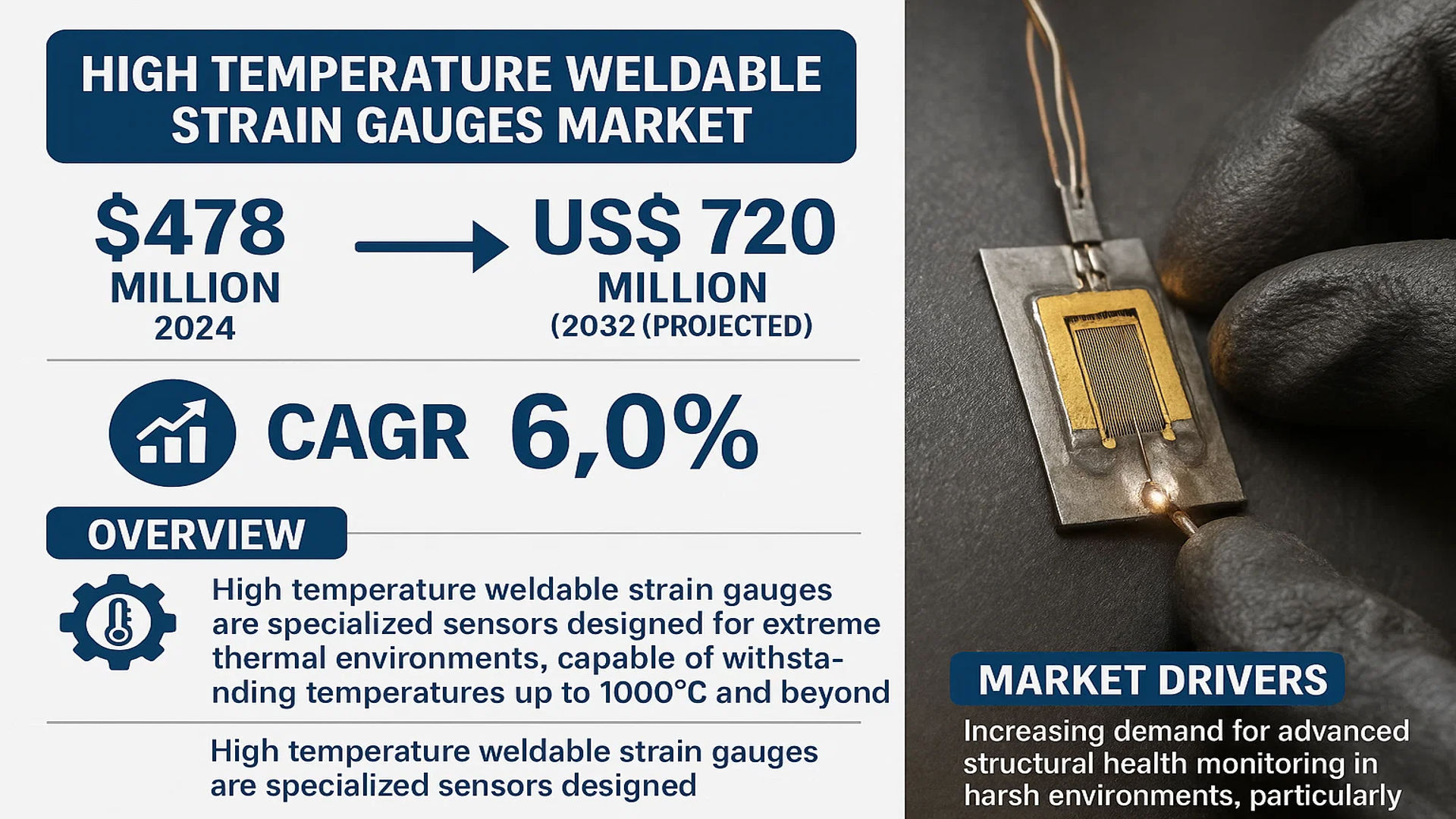

The global High Temperature Weldable Strain Gauges Market was valued at 478 million in 2024 and is projected to reach US$ 720 million by 2032, at a CAGR of 6.0% during the forecast period.

High temperature weldable strain gauges are specialized sensors designed for extreme thermal environments, capable of withstanding temperatures up to 1000°C and beyond. These precision devices measure material deformation (strain) under high heat conditions using advanced alloys and ceramic composites, ensuring reliable performance in critical applications. They are directly welded onto test surfaces for superior accuracy in aerospace engine monitoring, power plant equipment, automotive testing, and industrial process control.

The market growth is driven by increasing demand for advanced structural health monitoring in harsh environments, particularly in aerospace and energy sectors. While stainless steel variants dominate current applications, ceramics are gaining traction due to superior thermal resistance. Key players like TML.JP, HBK, and Kyowa Electronic Instruments collectively held significant market share in 2024, with ongoing R&D focused on enhancing temperature tolerance and measurement precision.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Aerospace and Energy Sectors Fueling Market Demand

The global aerospace industry, valued at over $800 billion, continues to drive demand for high temperature weldable strain gauges due to their critical role in structural health monitoring of aircraft components. With increasing air travel and next-generation aircraft development, these sensors are essential for testing turbine blades, engine mounts, and landing gear that operate at extreme temperatures. The energy sector similarly relies on these gauges for monitoring gas turbines, nuclear reactors, and geothermal systems where temperatures routinely exceed 800°C. Major power generation projects worldwide are incorporating advanced monitoring systems, creating sustained demand growth.

Technological Advancements Enhancing Product Capabilities

Recent innovations in materials science have significantly improved the performance characteristics of high temperature strain gauges. New ceramic-based strain-sensitive alloys now maintain stability at temperatures up to 1200°C with less than 1% drift—a crucial improvement for precision applications. Leading manufacturers are developing wireless variants with integrated temperature compensation, eliminating signal interference issues common in high EMI environments. These technological breakthroughs are expanding applications into previously inaccessible sectors like hypersonic vehicle development and advanced nuclear reactor designs.

Stringent Safety Regulations Driving Adoption

Global regulatory frameworks increasingly mandate continuous structural monitoring for critical infrastructure. Recent updates to aviation safety standards require real-time strain monitoring of aircraft components exposed to thermal cycling. Similarly, nuclear power plant operators must implement advanced monitoring systems under revised international safety protocols. These regulatory changes create compulsory markets for high temperature strain gauges, with non-compliance penalties ensuring steady adoption. The petrochemical industry is following suit, implementing similar monitoring requirements for refinery pressure vessels and pipelines.

MARKET RESTRAINTS

High Costs and Complex Installation Limiting Market Penetration

Premium materials and specialized manufacturing processes make high temperature weldable strain gauges significantly more expensive than conventional strain sensors—often costing 3-5 times more per unit. Installation requires certified welding technicians and sophisticated calibration equipment, adding substantial implementation costs. Many small and medium enterprises find these barriers prohibitive, particularly in developing markets where budget constraints are tighter. While large industrial operations can absorb these costs, the price sensitivity of broader markets remains a persistent challenge.

Material Science Challenges at Extreme Temperatures

Despite advances, maintaining consistent gauge factor and minimal creep at sustained ultra-high temperatures remains technically challenging. Thermal expansion mismatches between sensor materials and test specimens can introduce measurement errors exceeding 10% in some applications. Oxidation of metallic components above 900°C continues to degrade performance over time, requiring more frequent replacement cycles. These material limitations restrict deployment in the most extreme environments like rocket propulsion systems or metallurgical furnaces, leaving significant unmet needs in these sectors.

Skilled Labor Shortage Impacting Market Growth

The specialized nature of high temperature strain gauge installation and calibration creates dependency on highly trained personnel. Industry estimates indicate a global shortfall of approximately 15,000 certified installation technicians—a gap projected to widen as experienced professionals retire. This shortage leads to project delays and quality control issues, particularly in emerging markets where training infrastructure is underdeveloped. Without accelerated workforce development initiatives, implementation bottlenecks may constrain market expansion despite strong underlying demand.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Sector

The rapid growth of concentrated solar power (CSP) plants presents significant opportunities, with receiver tubes and thermal storage systems requiring strain monitoring at operational temperatures exceeding 750°C. Similarly, next-generation geothermal energy projects drilling deeper into high-temperature reservoirs will require robust monitoring solutions. These renewable energy applications represent a potential $120 million annual market by 2030, with governments worldwide funding demonstration projects that incorporate advanced monitoring technologies.

Advancements in Additive Manufacturing Opening New Possibilities

Metal 3D printing is revolutionizing component design but introduces new measurement challenges for residual stresses in high-temperature alloys. Manufacturers are developing specialized strain gauges that integrate directly into additive manufacturing processes, enabling in-situ monitoring during both fabrication and service. This convergence of measurement technologies with advanced manufacturing could create entirely new product categories, with early adopters in aerospace and medical implant sectors already testing prototypes.

Smart Factory Initiatives Driving Demand for IoT-Enabled Solutions

Industry 4.0 implementations increasingly require wireless, networked sensors capable of operating in harsh industrial environments. New self-powered, LoRa-enabled strain gauges are emerging that transmit data directly to predictive maintenance systems without wiring infrastructure. With global smart factory investments exceeding $400 billion annually, this represents a major growth vector for manufacturers who can successfully integrate traditional strain measurement with digital transformation initiatives.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Specialty Materials

Geopolitical tensions and trade restrictions have created bottlenecks for rare earth elements and specialty alloys used in high-performance strain gauges. Certain nickel-chromium formulations essential for high-temperature stability now face 6-9 month lead times, disrupting production schedules. Manufacturers are struggling to diversify supply chains while maintaining strict material specifications—a challenge compounded by trade secret protections that limit alternative sourcing options.

Standardization and Certification Complexities

Divergent international standards for high-temperature strain measurement create compliance hurdles for global manufacturers. Certification processes for aerospace and nuclear applications can take 18-24 months, delaying product launches. Recent changes to aviation safety regulations in key markets have forced costly redesigns of established products, highlighting the risks of operating in such a tightly regulated space.

Competition from Alternative Measurement Technologies

Non-contact measurement methods like digital image correlation and fiber optic sensors are making inroads in some high-temperature applications. While these alternatives currently lack the precision of weldable strain gauges for certain use cases, their non-invasive nature and decreasing costs pose a long-term competitive threat. Manufacturers must continue advancing core technologies while educating the market on the unique advantages of traditional strain measurement approaches.

HIGH TEMPERATURE WELDABLE STRAIN GAUGES MARKET TRENDS

Growing Demand in Aerospace and Energy Sectors Drives Market Expansion

The high temperature weldable strain gauges market is experiencing significant growth, driven primarily by increasing applications in aerospace and energy sectors. These strain gauges, capable of withstanding extreme temperatures up to 1000°C or higher, are essential for monitoring structural integrity in jet engines, gas turbines, and nuclear reactors. With the aerospace industry projected to grow at a CAGR of 5.2% over the next decade, the demand for reliable high-temperature measurement tools is accelerating. Additionally, expanding investments in renewable energy infrastructure, particularly in geothermal and nuclear power plants, are further propelling adoption due to stringent safety and performance monitoring requirements.

Other Trends

Advancements in Material Science

Continuous material innovations, including the development of ceramic-based and specialty alloy strain gauges, are enhancing the durability and accuracy of high-temperature measurements. Manufacturers are leveraging advanced alloys like Karma and Nichrome V, which exhibit minimal drift under thermal stress, ensuring precise strain readings in extreme conditions. This trend is particularly impactful in the petrochemical industry, where equipment exposed to corrosive environments requires robust sensing solutions.

Automotive and Transportation Sector Emerges as a Key Growth Area

The automotive industry, particularly in engine and exhaust system testing, is adopting high-temperature weldable strain gauges to optimize performance and comply with emission regulations. With global automobile production rebounding to over 85 million units annually, the need for real-time strain monitoring in combustion engines and electric vehicle battery systems is escalating. Furthermore, rail and heavy machinery applications are increasingly integrating these gauges for predictive maintenance, reducing downtime and operational risks in high-temperature environments.

Challenges and Regional Dynamics

While North America and Europe currently dominate the market due to their established aerospace and energy sectors, the Asia-Pacific region is witnessing the fastest growth, fueled by rapid industrialization and infrastructure development in China and India. However, the high cost of advanced materials and the technical complexity of installation remain barriers for smaller enterprises. Manufacturers are addressing these challenges through modular designs and collaborative R&D initiatives aimed at cost reduction without compromising performance.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Technical Expertise Drive Market Leadership

The global high temperature weldable strain gauges market is characterized by moderate competition, with established players and specialized manufacturers vying for market share. TML.JP and Kyowa Electronic Instruments currently dominate the market, collectively holding about 30% of the global revenue share in 2024. Their leadership stems from decades of expertise in strain measurement technologies and strong relationships with aerospace and energy sector clients.

While TML.JP maintains dominance in Asia-Pacific through its advanced ceramic-based gauges, Kyowa has secured robust market positions in North America and Europe by focusing on specialized alloy solutions. Meanwhile, HBK (Hottinger Brüel & Kjær) is gaining traction through strategic acquisitions, having expanded its high-temperature product lines by integrating niche technologies from smaller competitors.

The market sees active participation from regional specialists like Bestech Australia in oceanic markets and ZHONGHANG ELECTRONIC in China, who are capitalizing on local manufacturing advantages. These players are increasingly challenging global leaders through competitive pricing and customized solutions for regional industrial requirements.

Strategic Developments Shape Market Dynamics

Recent years have witnessed significant R&D investments as companies race to develop gauges capable of withstanding extreme temperatures above 1,200°C. In 2023, Hitec Products, Inc. launched a breakthrough stainless steel variant with enhanced fatigue resistance, specifically developed for next-generation jet engine testing.

Merger activity has also intensified, particularly in Europe where Müller Instruments acquired Slentech’s strain gauge division to strengthen its position in the petrochemical sector. Similarly, GEOKON and Geosense have formed a strategic alliance to combine their expertise in energy infrastructure monitoring solutions.

List of Key High Temperature Weldable Strain Gauge Companies

- TML.JP (Japan)

- Kyowa Electronic Instruments Co., Ltd. (Japan)

- Hitec Products, Inc. (U.S.)

- HBK Global (Germany)

- GEOKON, Incorporated (U.S.)

- Geosense Ltd. (U.K.)

- Bestech Australia (Australia)

- Durham Instruments (Canada)

- Müller Instruments (Germany)

- ZHONGHANG ELECTRONIC MEASURING INSTRUMENTS CO.,LTD. (China)

Segment Analysis:

By Type

Stainless Steel Segment Leads Due to High Durability and Cost-Effectiveness in Extreme Conditions

The market is segmented based on type into:

- Stainless Steel

- Subtypes: Austenitic, Martensitic, and Ferritic grades

- Special Alloys

- Subtypes: Nickel-based, Cobalt-based, and Iron-based alloys

- Ceramics

- Subtypes: Alumina-based, Silicon nitride-based, and others

By Application

Aerospace Sector Dominates Market Demand for Structural and Engine Component Testing

The market is segmented based on application into:

- Aerospace

- Sub-applications: Turbine blade monitoring, Fuselage stress analysis

- Energy and Power

- Sub-applications: Nuclear reactor vessels, Gas turbine monitoring

- Transportation

- Sub-applications: Automotive engine testing, Brake system analysis

- Petrochemical

- Sub-applications: Refinery piping, Pressure vessel monitoring

By Temperature Range

High-Temperature Segment (Above 600°C) Shows Strong Growth Due to Expanding Industrial Applications

The market is segmented based on temperature range into:

- Medium Temperature (200-600°C)

- High Temperature (600-1000°C)

- Ultra High Temperature (Above 1000°C)

By Installation Method

Spot Weld Installation Maintains Market Preference Due to Superior Stability in High Vibration Environments

The market is segmented based on installation method into:

- Spot Weld

- Bead Weld

- Capacitor Discharge Weld

Regional Analysis: High Temperature Weldable Strain Gauges Market

Asia-Pacific

The Asia-Pacific region dominates the global high temperature weldable strain gauges market, primarily driven by China, Japan, and South Korea. China’s rapid industrialization, coupled with heavy investments in aerospace, energy, and automotive sectors, has positioned it as the largest consumer of these sensors. The region benefits from robust manufacturing capabilities and increasing R&D activities in material science. Japan leads in technological advancements, with key players like Kyowa Electronic Instruments and TML.JP developing high-performance gauges capable of operating above 1000°C. India is emerging as a growth hotspot due to expanding infrastructure projects and rising demand for power plant monitoring systems. While cost sensitivity remains a challenge, the adoption of ceramic-based gauges is accelerating in critical applications.

North America

North America represents a technologically mature market, with the U.S. accounting for over 60% of regional demand. Strict aerospace certification requirements (FAA, NASA) and extensive gas turbine deployments in the energy sector drive the need for precision strain measurement. Major manufacturers like Hitec Products and HBK focus on developing specialized alloys to withstand extreme conditions in jet engines and nuclear reactors. Canada’s oil sands industry also contributes to demand for high-temperature monitoring solutions. However, market growth faces headwinds from supply chain complexities and the high cost of advanced materials. Strategic partnerships between research institutions and manufacturers are fostering innovation in this space.

Europe

Europe maintains a strong position in the high temperature strain gauges market, with Germany and France leading technological development. The region’s emphasis on renewable energy infrastructure, particularly in wind turbine and concentrated solar power applications, creates steady demand for durable strain measurement solutions. EU-funded projects like Horizon Europe are accelerating material innovations, with companies such as ZSE Electronic pioneering ceramic-matrix composites. The aerospace sector remains a key driver, with Airbus operations requiring sophisticated strain monitoring across manufacturing and testing processes. However, competitive pressure from Asian manufacturers and stringent REACH compliance costs present ongoing challenges for European suppliers.

Middle East & Africa

This region shows promising growth potential, particularly in Gulf Cooperation Council (GCC) countries where massive investments in petrochemical and power generation infrastructure are underway. Saudi Arabia’s Vision 2030 project and UAE’s diversification from oil are driving demand for high-temperature monitoring in refinery and desalination plants. South Africa’s mining and energy sectors also contribute to market growth. While the current market size remains modest compared to other regions, increasing foreign direct investment in industrial projects and gradual technology transfer are expected to boost adoption rates. The lack of local manufacturing capabilities and reliance on imports currently constrain more rapid expansion.

South America

South America’s market is developing, with Brazil and Argentina representing the primary demand centers. The region’s growing aerospace sector, including Embraer’s operations, and expansion of thermal power generation are key drivers. Brazil’s pre-salt oil fields require specialized strain gauges for deep-sea drilling equipment, creating niche opportunities. However, economic instability, limited R&D investment, and underdeveloped industrial standards hinder faster market penetration. Local manufacturers focus mainly on lower-temperature applications, while high-performance gauges are typically imported from North American and European suppliers. The region’s long-term potential remains tied to infrastructure development and stability in key industries.

Report Scope

This market research report provides a comprehensive analysis of the Global High Temperature Weldable Strain Gauges Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 478 million in 2024 and is projected to reach USD 720 million by 2032, growing at a CAGR of 6.0%.

- Segmentation Analysis: Detailed breakdown by product type (Stainless Steel, Special Alloys, Ceramics), application (Aerospace, Energy and Power, Transportation, Petrochemical), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets, with Asia-Pacific showing significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including TML.JP, Hitec Products, Inc., Kyowa Electronic Instruments, ZSE Electronic, and HBK, analyzing their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging materials, fabrication techniques, and high-temperature measurement advancements.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand from aerospace and energy sectors, alongside challenges like material costs and supply chain constraints.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Temperature Weldable Strain Gauges Market?

-> High Temperature Weldable Strain Gauges Market was valued at 478 million in 2024 and is projected to reach US$ 720 million by 2032, at a CAGR of 6.0% during the forecast period.

Which key companies operate in Global High Temperature Weldable Strain Gauges Market?

-> Key players include TML.JP, Hitec Products, Inc., Kyowa Electronic Instruments, ZSE Electronic, HBK, GEOKON, and Bestech Australia, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand from aerospace and energy sectors, advancements in high-temperature materials, and increasing industrial automation.

Which region dominates the market?

-> North America holds a significant market share, while Asia-Pacific is the fastest-growing region due to expanding industrial and infrastructure development.

What are the emerging trends?

-> Emerging trends include development of ceramic-based strain gauges, integration with IoT for real-time monitoring, and increasing adoption in renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...