MARKET INSIGHTS

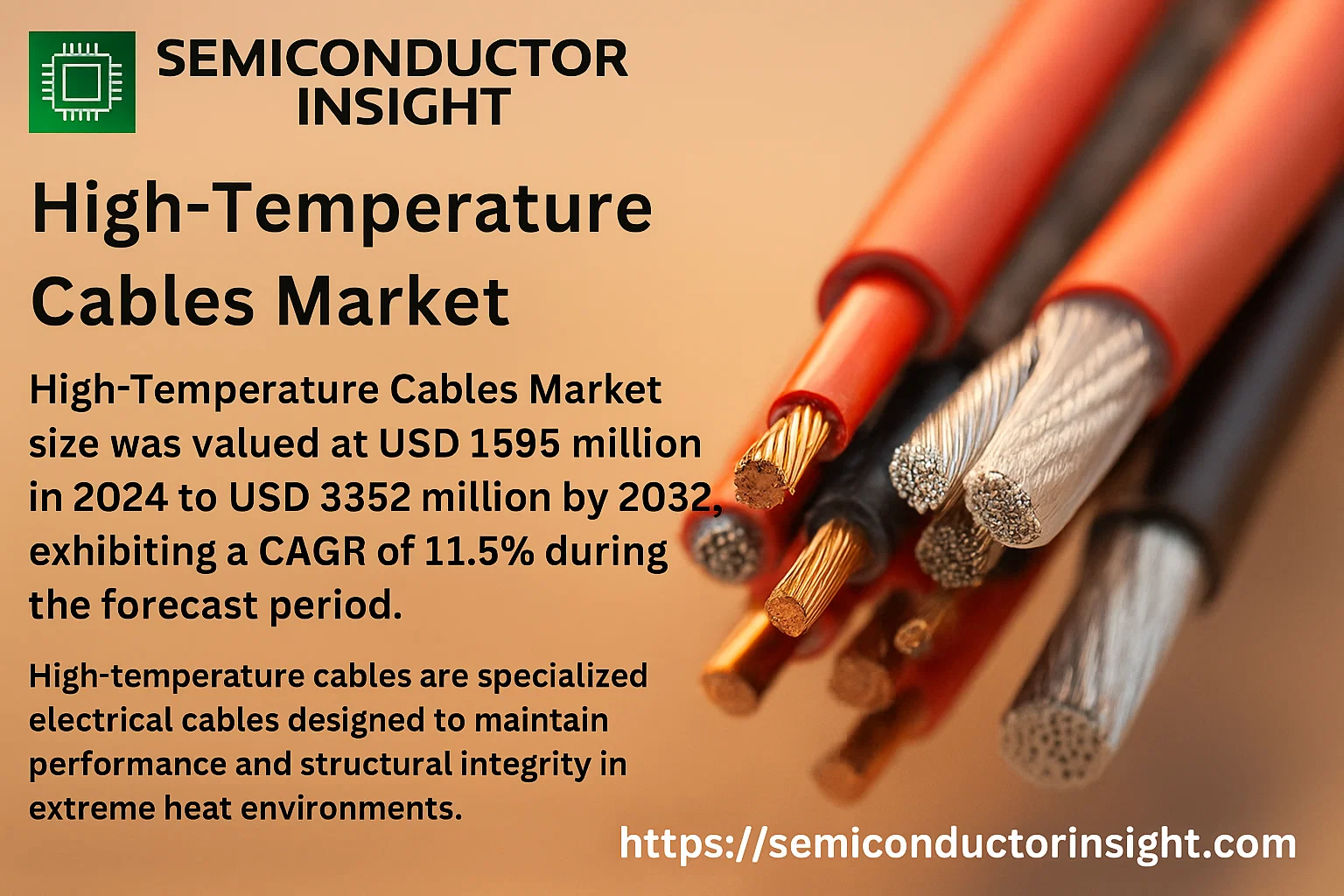

Global High-Temperature Cables Market size was valued at USD 1595 million in 2024 to USD 3352 million by 2032, exhibiting a CAGR of 11.5% during the forecast period.

High-temperature cables are specialized electrical cables designed to maintain performance and structural integrity in extreme heat environments. These cables are engineered with insulation and jacketing materials such as silicone rubber, PTFE (Teflon), or fiberglass that can withstand continuous operating temperatures typically ranging from 150°C to over 500°C. They encompass various types including Maximum 125°C, Maximum 150°C, Maximum 200°C, Maximum 250°C, Maximum 450°C, and Maximum 550°C.

The Market is experiencing robust growth due to several factors, including increasing demand from the energy sector for applications in power plants and refineries, alongside growth in industrial automation and transportation. Furthermore, stringent safety regulations requiring reliable performance in harsh conditions are contributing to Market expansion. Initiatives by key players in the Market are also expected to fuel the Market growth. For instance, leading manufacturers like Nexans and Prysmian Group continuously invest in developing advanced materials to enhance cable durability and efficiency under thermal stress. Nexans S.A., Prysmian Group, Leoni AG, and Belden Inc. are some of the key players that operate in the Market with a wide range of portfolios.

MARKET DRIVERS

Expansion in Industrial and Energy Sectors

The demand for high-temperature cables is primarily driven by robust growth in heavy industries such as oil and gas, manufacturing, and metal processing. These sectors require reliable cabling solutions that can withstand extreme thermal conditions exceeding 125°C, with some applications demanding performance above 1000°C. Global push for industrialization, particularly in emerging economies, is accelerating the installation of new facilities and upgrading existing infrastructure, directly fueling Market growth.

Advancements in Renewable Energy Infrastructure

The rapid expansion of renewable energy, especially concentrated solar power (CSP) plants and geothermal energy systems, represents a significant driver. These applications involve high ambient temperatures and require cables with exceptional thermal endurance. Global installed capacity for CSP is projected to grow significantly, creating a substantial and sustained demand for high-temperature cables capable of reliable operation in harsh environments.

➤ Stringent Safety and Performance Regulations

Increasingly stringent international safety standards and regulations mandate the use of certified high-temperature cables in critical applications to prevent failures, fires, and ensure operational continuity. Regulatory bodies like IEC, UL, and others have established rigorous testing requirements, compelling industries to adopt high-performance cabling solutions. This regulatory pressure is a key factor driving the replacement of standard cables with specialized high-temperature alternatives.

MARKET CHALLENGES

High Material and Manufacturing Costs

The production of high-temperature cables involves specialized materials such as fluoropolymers (PTFE, FEP, PFA), silicone rubber, and ceramic fibers, which are significantly more expensive than standard PVC or polyethylene. The complex manufacturing processes required to ensure consistency and performance further elevate costs. This high price point can be a barrier to adoption, particularly for cost-sensitive projects or in price-competitive Markets.

Other Challenges

Technical Complexity and Customization Requirements

High-temperature cable applications are highly specific, often requiring custom-designed solutions for unique voltage, flexibility, chemical resistance, and temperature profiles. This necessitates close collaboration between manufacturers and end-users, leading to longer development cycles and potential challenges in scaling production to meet diverse global demands efficiently.

MARKET RESTRAINTS

Volatility in Raw Material Prices

The Market is susceptible to fluctuations in the prices of key raw materials, including specialty polymers and metals like silver or nickel used in conductors. Supply chain disruptions and geopolitical factors can lead to price volatility, impacting profit margins for manufacturers and creating pricing uncertainty for buyers. This instability can delay investment decisions and project timelines, acting as a restraint on Market growth.

MARKET OPPORTUNITIES

Growth in Electric Vehicle and Aerospace Industries

The booming electric vehicle (EV) Market and the aerospace sector present significant growth opportunities. EVs require high-temperature cables for battery packs, charging systems, and powertrains that operate under the hood. Similarly, aerospace applications demand lightweight, fire-resistant cables for engines and avionics. Global EV Market is expected to grow exponentially, directly translating into increased demand for advanced high-temperature cable solutions.

Emerging Applications in Digitalization and Industry 4.0

The integration of IoT sensors and automation in high-temperature industrial environments, such as steel mills or chemical plants, creates a new frontier for these cables. They are essential for connecting sensors and control systems that must operate reliably in extreme heat, enabling predictive maintenance and smarter operations. The ongoing adoption of Industry 4.0 principles is expected to open substantial new Markets for high-temperature data and control cables.

High-Temperature Cables Market Trends

Robust Market Expansion Driven by Industrial Demand

Global High-Temperature Cables Market is demonstrating significant and sustained growth, with a valuation of USD 1,595 million in 2024. The Market is projected to more than double, reaching an estimated USD 3,352 million by the year 2032. This expansion is driven by a Compound Annual Growth Rate (CAGR) of 11.5% throughout the forecast period. The demand for cables that maintain performance in extreme thermal environments is increasing across diverse industrial sectors, fueling this substantial Market growth.

Other Trends

Regional Market Dynamics

Europe currently stands as the largest Market for high-temperature cables, holding a dominant share of over 30% of the global Market. This leadership is attributed to a strong industrial base and stringent safety and performance regulations. Following Europe, the combined Markets of China and North America account for approximately 50% of the global Market share, indicating significant demand and manufacturing capabilities in these regions. This geographic distribution highlights the global nature of the industry’s demand drivers.

Product and Application Segmentation Trends

In terms of product types, cables rated for a maximum temperature of 150°C represent the largest product segment, commanding about 25% of the Market. This segment’s popularity is linked to its suitability for a wide range of industrial applications where moderate to high heat resistance is required. Regarding application, the Energy sector is the largest consumer of high-temperature cables, followed closely by the Transportation and Electric Appliances industries. The critical need for reliable power transmission and control systems in harsh environments within these sectors is a primary growth driver.

Consolidated Competitive Landscape

Global high-temperature cables Market features a competitive landscape with a notable degree of concentration. The top two manufacturers, Nexans and Prysmian Group, collectively hold over 20% of the global Market share. This indicates an industry where scale, technological expertise, and global supply chains are significant competitive advantages. The presence of other key players such as Leoni, Belden, and General Cable ensures a dynamic Market with continued innovation in cable materials and designs to meet evolving application requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

A Concentrated Market with Significant European Influence

Global High-Temperature Cables Market is characterized by the dominance of a few major international players, with the top two manufacturers, Nexans and Prysmian Group, collectively holding a share of over 20%. This indicates a moderately concentrated Market structure where large, established companies leverage their extensive global distribution networks, significant R&D capabilities, and diverse product portfolios to serve a wide range of demanding applications from energy to transportation. These leading players are headquartered in Europe, which is the single largest Market globally, accounting for over 30% of the Market share. The competitive dynamics are heavily influenced by the need for product innovation to meet stringent safety and performance standards across various industries, as well as strategic mergers and acquisitions to expand geographical and application-specific reach.

Beyond the Market leaders, the landscape includes numerous other significant players that compete by focusing on niche applications, specific temperature ratings, or regional Markets. Companies such as Leoni, Belden, and Lapp Group have established strong positions by specializing in cables for industrial automation, manufacturing, and specialty applications. Furthermore, regional manufacturers, particularly in Asia, are increasingly important. Chinese companies like Jiangsu Yinxi and Tongguang Electronic are growing their presence, capitalizing on the large domestic Market and cost advantages. This tier of companies often competes on price, customization, and rapid response to local Market needs, creating a diverse and dynamic competitive environment alongside the global giants.

List of Key High-Temperature Cables Companies Profiled

- Nexans

- Prysmian Group

- Leoni

- Anixter

- Belden

- Lapp Group

- Hansen

- General Cable

- Jiangsu Yinxi

- Tongguang Electronic

- Yueqing City Wood

- Axon Cable

- Thermal Wire&Cable

- Flexible & Specialist Cables

- Tpc Wire & Cable

- Bambach

- Eland Cables

- BING

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Maximum 150°C cables are the leading segment due to their broad applicability across multiple industries, offering an optimal balance between performance and cost-efficiency. This temperature rating is well-suited for a vast range of industrial processes, automotive applications, and general manufacturing environments where thermal resistance is critical but extreme heat is not a constant factor. The extensive adoption is driven by the material science that allows for durable insulation without excessive cost, making it the standard choice for many original equipment manufacturers. Furthermore, ongoing material innovations continue to enhance the longevity and safety profile of these cables, solidifying their dominant Market position. |

| By Application |

|

Energy is the leading application segment, fueled by the critical need for reliable power transmission and distribution infrastructure in power generation plants, including nuclear, solar, and fossil fuel facilities. High-temperature cables are indispensable in these settings for connecting generators, transformers, and switchgear where elevated temperatures are inherent to operation. Global push for energy security and the modernization of aging grid infrastructure further propels demand. Additionally, the expansion of renewable energy projects, which often involve harsh environmental conditions, relies heavily on these specialized cables to ensure operational safety and efficiency over long periods. |

| By End User |

|

Industrial Manufacturing constitutes the leading end-user segment, as these cables are fundamental components in machinery, furnaces, ovens, and industrial automation systems that operate under continuous thermal stress. The demand is driven by the need for minimal downtime and high safety standards in processes like metal processing, glass manufacturing, and chemical production. The trend towards industrial automation and smart factories, which require robust and reliable wiring for sensors and control systems in hot environments, further strengthens this segment’s dominance. This broad-based industrial reliance ensures consistent and growing demand from this key user group. |

| By Insulation Material |

|

Silicone Rubber insulation is the leading material segment due to its exceptional combination of flexibility, high thermal stability, and excellent electrical properties. Its widespread adoption is attributed to its ability to maintain integrity across a wide temperature range while providing resistance to moisture, chemicals, and weathering. This makes it ideal for demanding applications in the energy, manufacturing, and transportation sectors. The material’s versatility allows for easier installation in complex routing scenarios compared to more rigid alternatives, contributing significantly to its preference among engineers and specifiers for a multitude of high-temperature cable applications. |

| By Cable Construction |

|

Multi-core Cables represent the leading construction type, driven by the need for consolidated wiring solutions in complex control and instrumentation systems within industrial plants and energy facilities. Their design simplifies installation by reducing the number of individual cables required for signal and power transmission, leading to improved space efficiency and lower overall installation costs. The demand is particularly strong in automation and process control applications where multiple signals need to be transmitted from a single point. The ability of multi-core constructions to be manufactured with various shielding options also makes them versatile for environments with electromagnetic interference, solidifying their leading position. |

Regional Analysis: High-Temperature Cables Market

The region’s vast manufacturing base is the primary consumer. Industries such as metal processing, cement, and automotive assembly rely heavily on high-temperature cables for furnace operations, engine compartments, and process control systems, creating consistent and high-volume demand that outpaces other global Markets.

Massive investments in new power generation facilities, including conventional thermal plants and renewable energy projects, drive demand. High-temperature cables are essential for power distribution, control circuits, and connections within high-heat environments of these plants, a Market segment experiencing robust growth.

National initiatives focusing on industrial modernization, urbanization, and transportation infrastructure (like high-speed rail) create significant opportunities. These large-scale projects necessitate durable cabling for signaling, traction systems, and industrial controls that can operate reliably under thermal stress.

A concentration of cable manufacturers and raw material suppliers within the region enables rapid response to Market needs and cost competitiveness. This ecosystem fosters the development of specialized cables for emerging applications, such as those required in electric vehicle production and data centers.

North America

The North American Market for high-temperature cables is characterized by mature yet technologically advanced industries with a strong emphasis on safety, reliability, and upgrades to existing infrastructure. Demand is steady, driven by the region’s robust oil and gas sector, particularly in shale exploration and refining, where cables must endure extreme downhole and processing temperatures. The aerospace and defense industries are also significant contributors, requiring cables that meet stringent specifications for aircraft engines and military applications. A key Market dynamic is the ongoing modernization of aging power grids and industrial facilities, which involves replacing older cabling with newer, more efficient high-temperature alternatives. Strict regulatory standards governing fire safety and material performance further shape the Market, favoring suppliers with proven compliance and high-quality products.

Europe

Europe represents a sophisticated Market for high-temperature cables, driven by a strong industrial base, stringent environmental and safety regulations, and a leading position in automotive and machinery manufacturing. The region’s demand is significantly influenced by the automotive industry’s shift towards electric vehicles, which require specialized high-temperature cables for battery packs and power electronics. Furthermore, Europe’s well-established chemical processing, metal production, and renewable energy sectors, especially offshore wind, provide consistent demand. The Market is characterized by a high value on innovation and quality, with manufacturers focusing on developing cables with improved thermal endurance, halogen-free materials, and sustainability credentials to meet the European Union’s strict directives.

South America

The high-temperature cables Market in South America is developing, with growth primarily linked to the mining, oil and gas, and power generation sectors. Countries with significant mineral and hydrocarbon resources drive demand for cables used in extraction, processing, and transportation equipment exposed to high temperatures. Investment in energy infrastructure, including hydroelectric and thermal power plants, also contributes to Market activity. However, the Market’s growth pace is often tied to regional economic stability and levels of foreign investment in industrial projects. The adoption of newer technologies is gradual, with a focus on cost-effective solutions that meet the essential performance requirements of key industries.

Middle East & Africa

The Market dynamics in the Middle East & Africa are heavily shaped by the massive oil, gas, and petrochemical industries, which are the predominant consumers of high-temperature cables. The extreme environmental conditions and demanding applications in refineries, drilling rigs, and desalination plants create a steady need for highly durable and reliable cabling solutions. In the Middle East, large-scale construction projects and investments in power and water infrastructure further bolster demand. In Africa, growth is more sporadic, concentrated in regions with active mining and energy development. The Market is price-sensitive, but there is a growing recognition of the importance of quality and longevity in cables to ensure operational safety and reduce downtime in critical industries.

Report Scope

This Market research report provides a comprehensive analysis of the High-Temperature Cables Market , covering the forecast period 2025–2032. It offers detailed insights into Market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current Market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and Market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into Market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading Market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving Market growth along with challenges, supply chain constraints, regulatory issues, and Market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time Market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current Market size of High-Temperature Cables Market?

-> High-Temperature Cables Market size was valued at USD 1595 million in 2024 to USD 3352 million by 2032, exhibiting a CAGR of 11.5% during the forecast period.

Which key companies operate in High-Temperature Cables Market?

-> Key players include Nexans, Prysmian Group, Leoni, Anixter, Belden, Lapp Group, Hansen, General Cable, and Jiangsu Yinxi, among others. Global top two manufacturers hold a share of over 20%.

What are the key growth drivers?

-> Key growth drivers include increasing demand from the energy and transportation sectors, infrastructure development, and the widespread use of high-temperature cables in electric appliances.

Which region dominates the Market?

-> Europe is the largest Market, with a share of over 30%, followed by China and North America, which together hold a share of about 50%.

What are the emerging trends?

-> Emerging trends include the development of cables with higher temperature ratings, increased adoption in renewable energy applications, and advancements in insulation materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...