MARKET INSIGHTS

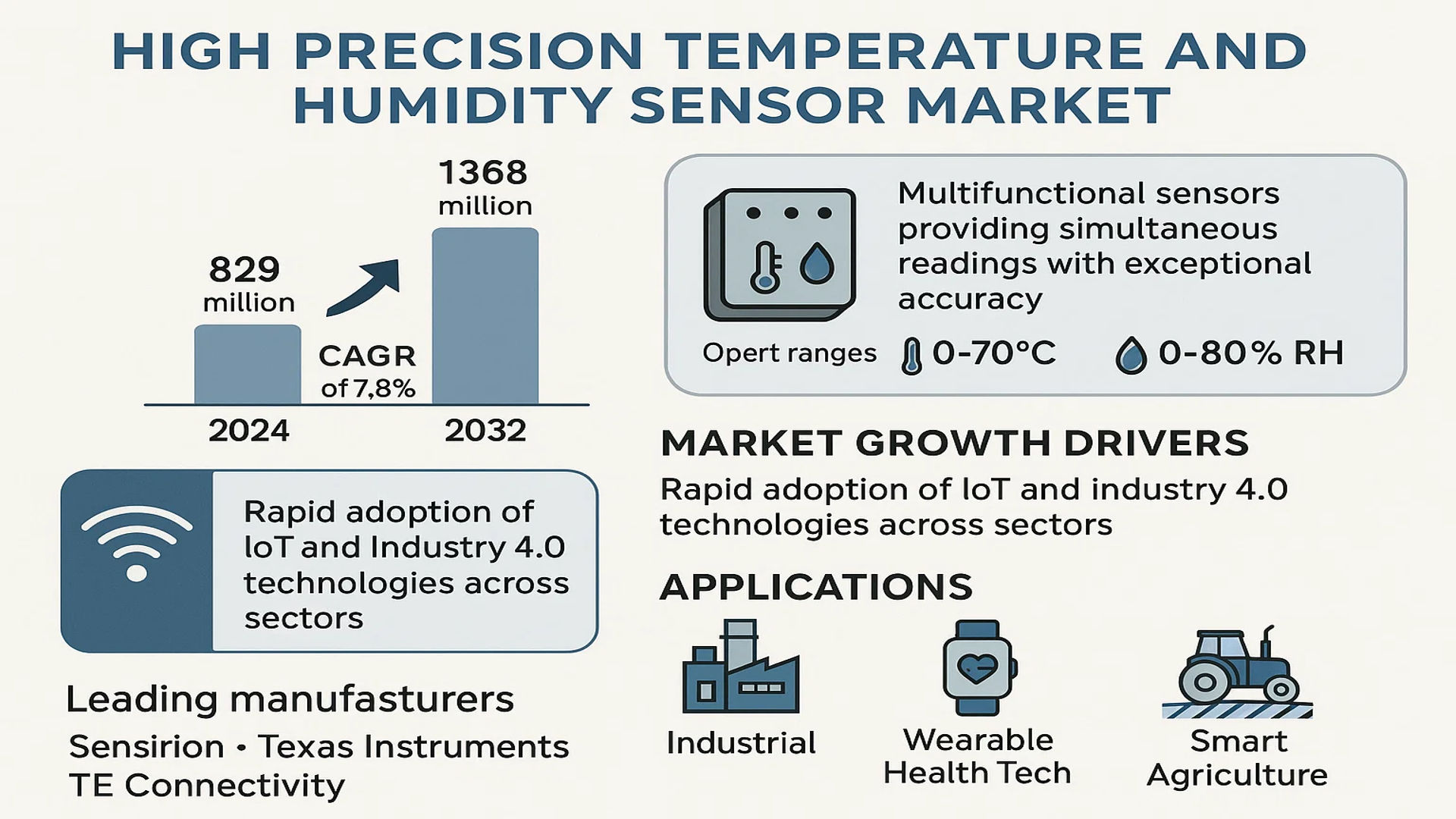

The global High Precision Temperature and Humidity Sensor Market was valued at 819 million in 2024 and is projected to reach US$ 1368 million by 2032, at a CAGR of 7.8% during the forecast period.

High precision temperature and humidity sensors are multifunctional devices that provide simultaneous readings of both temperature and relative humidity with exceptional accuracy. These sensors deliver reliable measurements within operational ranges of 0-80% relative humidity and 0-70°C temperature, making them indispensable for applications requiring stringent environmental monitoring.

Market expansion is being driven by the rapid adoption of IoT and Industry 4.0 technologies across sectors. These sensors play a critical role in automation, predictive maintenance, and real-time data collection. While industrial applications dominate current demand, emerging sectors like wearable health tech and smart agriculture are creating new growth opportunities. Leading manufacturers including Sensirion, Texas Instruments, and TE Connectivity are investing heavily in miniaturization and energy efficiency to capture these expanding applications.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Adoption of IoT and Industry 4.0 Technologies Fuels Sensor Demand

The global proliferation of Industry 4.0 initiatives has become a pivotal driver for high-precision temperature and humidity sensors, with manufacturing facilities increasingly integrating these components into smart factory systems. IoT-connected sensors enable real-time monitoring of production environments, where maintaining precise climatic conditions directly impacts product quality in sectors like pharmaceuticals, semiconductors, and food processing. The pharmaceutical industry alone requires ±0.5°C accuracy for vaccine storage compliance, creating sustained demand for precision sensors. With global smart manufacturing investments projected to grow at 12% annually, sensor manufacturers are experiencing unprecedented demand from industrial automation applications.

Expansion of Smart Building Ecosystems Creates New Application Verticals

Building automation systems now account for approximately 28% of global sensor deployments, driven by stringent energy efficiency regulations and the push for healthier indoor environments. Modern HVAC systems integrate multiple high-precision sensors to maintain optimal conditions while reducing energy consumption, with recent advancements enabling ±2% RH humidity accuracy. The proliferation of green building certifications like LEED and WELL has further accelerated adoption, particularly in commercial real estate markets where sensor data contributes to both operational efficiency and tenant wellness metrics. This trend shows no signs of slowing, as smart city initiatives worldwide mandate more sophisticated environmental monitoring infrastructure.

➤ High-rise commercial buildings now deploy an average of 350-500 environmental sensors per structure, with precision devices commanding premium pricing in retrofit markets.

Medical and Life Sciences Demand Drives Precision Requirements Higher

Healthcare applications now represent one of the fastest-growing segments for precision environmental sensors, with hospital isolation rooms, laboratories, and vaccine storage facilities requiring unprecedented measurement accuracy. The post-pandemic emphasis on infection control has led to adoption of sensors capable of maintaining ±0.3°C stability in critical care environments, while pharmaceutical manufacturing clean rooms demand 0.1°C resolution for process validation. This sector’s growth is further propelled by increasing regulatory scrutiny, where documentation of environmental conditions has become mandatory for compliance with good manufacturing practices worldwide.

MARKET RESTRAINTS

High Development Costs and Extended Calibration Requirements Limit Adoption

While demand grows, the market faces significant barriers in the substantial R&D investments required to develop industrial-grade precision sensors. Achieving sub-1% humidity accuracy necessitates advanced MEMS fabrication techniques and proprietary compensation algorithms, with development cycles often exceeding 18 months. Additionally, high-accuracy sensors require periodic recalibration—typically every 6-12 months in industrial environments—creating substantial lifetime ownership costs. These factors particularly impact price-sensitive markets, where customers may opt for lower-precision alternatives despite compromised performance.

Other Restraints

Material Science Limitations

Current sensor technologies face fundamental accuracy ceilings due to material properties, with even advanced polymer-based humidity sensors experiencing 0.5-1% RH drift over time. Research into novel nanomaterials shows promise but remains years away from commercial viability, temporarily capping performance improvements in mainstream products.

Supply Chain Vulnerabilities

Specialized semiconductor components critical for precision signal conditioning remain subject to allocation, with lead times for certain ASICs extending beyond 40 weeks. This fragility in the supply network creates production bottlenecks during periods of surging demand.

MARKET CHALLENGES

Integration Complexities in Legacy Systems Create Deployment Hurdles

The transition to smart monitoring systems presents significant technical challenges, particularly when retrofitting existing industrial infrastructure. Many facilities operate with outdated control systems lacking modern communication protocols, forcing sensor manufacturers to maintain extensive product portfolios with various output options. Interoperability issues between different manufacturers’ equipment further complicate system integration, often requiring costly custom interface development. These factors lengthen deployment timelines and increase total project costs, particularly in sectors like oil & gas where equipment certifications add additional complexity.

Environmental Durability Requirements Constrain Design Options

Industrial applications demand sensors capable of withstanding extreme conditions—from -40°C freezer warehouses to 85°C factory floors—while maintaining specified accuracy. Developing housings and sensing elements that endure years of exposure to chemicals, cleaning agents, and mechanical stress requires extensive testing and validation. The automotive industry exemplifies these challenges, where under-hood applications require sensors to survive temperature cycling between -40°C and 125°C while resisting oil and fuel vapors—specifications that dramatically increase production costs.

MARKET OPPORTUNITIES

Emerging Precision Agriculture Applications Open New Growth Frontiers

The agriculture sector presents substantial untapped potential, where controlled environment farming operations increasingly demand industrial-grade environmental monitoring. Modern greenhouse facilities now deploy sensor grids providing 0.5°C temperature resolution across cultivation zones, enabling precise climate control that optimizes crop yields while minimizing resource consumption. Vertical farming operations are particularly intensive users, with some facilities installing over 200 sensors per 1,000 square meters to maintain ideal growing conditions. As global investments in agtech continue their double-digit growth trajectory, sensor manufacturers are developing specialized product lines to serve this expanding market.

Advancements in Edge Computing Enable Smarter Sensor Networks

The integration of local processing capabilities represents a paradigm shift in environmental monitoring, allowing sensors to perform complex compensation algorithms and anomaly detection directly on-device. This reduces reliance on centralized systems while improving responsiveness—critical for applications like data center cooling management where milliseconds matter. Recent product launches incorporate machine learning cores that continuously adapt calibration parameters based on historical performance data, potentially extending maintenance intervals while improving long-term accuracy. These innovations are creating premium market segments where performance justifies higher price points.

HIGH PRECISION TEMPERATURE AND HUMIDITY SENSOR MARKET TRENDS

IoT and Industry 4.0 Expansion Driving Sensor Demand

The rapid adoption of Internet of Things (IoT) and Industry 4.0 technologies has significantly increased the demand for high precision temperature and humidity sensors. These sensors play a critical role in data collection, real-time monitoring, and automation across industrial applications, enabling predictive maintenance and process optimization. Statistics indicate that over 50% of manufacturing firms have integrated IoT-based sensor solutions into their operations to enhance efficiency. Furthermore, the proliferation of smart factories and automated production lines has accelerated this trend, pushing sensor demand to record levels.

Other Trends

Wearable Devices and Smart Textiles

The emergence of wearable health monitoring devices and smart textiles has introduced new application segments for high precision sensors. These devices require ultra-accurate environmental tracking to monitor user health and comfort conditions. The wearable technology market is expanding rapidly, with sensors in this sector projected to grow at a CAGR of 14% through 2032. Innovations such as embedded textile sensors for athletic performance tracking and temperature-regulated clothing are leveraging the latest advancements in humidity and thermal sensing.

Advancements in Sensor Technology

Technological innovations in sensor design and materials have significantly improved accuracy and durability. Modern sensors now utilize MEMS (Micro-Electro-Mechanical Systems) and solid-state sensing elements to achieve ±0.1°C temperature accuracy and ±1.5% RH humidity precision, even in harsh environments. Integration with wireless communication protocols like LoRaWAN and NB-IoT has further enhanced remote monitoring capabilities. Additionally, the shift toward energy-efficient sensor designs has reduced power consumption by approximately 30%, making them ideal for battery-operated IoT applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Market Leadership in Sensor Technology

The global high precision temperature and humidity sensor market is characterized by intense competition, with leading players investing heavily in R&D to enhance accuracy, reliability, and adaptability across applications. The market structure ranges from established electronics giants to specialized sensor manufacturers, all vying for dominance in this high-growth sector.

Sensirion AG currently holds the largest market share at approximately 18%, a position reinforced by their groundbreaking SHTC3 digital humidity and temperature sensor series. Their patented CMOSens® Technology has become an industry benchmark, particularly for IoT and industrial automation applications where ±1.5% RH accuracy is mission-critical. The company’s 2024 partnership with Bosch to develop next-gen automotive climate sensors illustrates their commitment to innovation.

Meanwhile, Texas Instruments and STMicroelectronics are gaining traction through their semiconductor-based solutions, leveraging existing manufacturing infrastructure to offer cost-competitive alternatives. Their HDC3020 (TI) and HTS221 (STMicro) sensors have seen particularly strong adoption in smart home devices, capturing nearly 12% combined market share in consumer applications.

Strategic acquisitions are reshaping the landscape – as seen when TE Connectivity acquired First Sensor AG in 2023, significantly expanding their industrial sensor capabilities. Similarly, TDK Corporation’s 2024 launch of the Humidity Humirel HS300x series demonstrates how component manufacturers are expanding into higher-margin precision sensing solutions.

List of Key High Precision Temperature & Humidity Sensor Manufacturers

- Sensirion AG (Switzerland)

- Robert Bosch GmbH (Germany)

- Testo SE & Co. KGaA (Germany)

- BorgWarner Inc. (U.S.)

- TE Connectivity (Switzerland)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Analog Devices, Inc. (U.S.)

- Omron Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- ScioSense B.V. (Netherlands)

- Apogee Instruments, Inc. (U.S.)

- Hoperf (Hong Kong) Limited (China)

Mid-sized innovators like ScioSense and Apogee Instruments are carving out profitable niches – the former in ultra-low-power designs for wearables, the latter in scientific-grade environmental monitoring systems. This diversity ensures healthy competition across all market segments from mass-produced consumer electronics to high-end industrial applications.

The competitive intensity is further amplified by regional players in Asia, particularly Chinese manufacturers like Hoperf, who are gaining share in price-sensitive markets. However, Western and Japanese firms maintain technological leadership in medical and aerospace applications where precision requirements exceed ±0.5°C accuracy thresholds.

Segment Analysis:

By Type

Digital Output Sensors Lead the Market Due to IoT Integration and Enhanced Data Processing Capabilities

The market is segmented based on type into:

- Analog Output

- Digital Output

- Subtypes: I2C, SPI, and others

By Application

Industrial Production Dominates with Growing Automation and Quality Control Requirements

The market is segmented based on application into:

- Household Appliances

- Industrial Production

- Environmental Monitoring

- Other

By Technology

Capacitive Sensors Gain Traction Due to High Accuracy and Long-Term Stability

The market is segmented based on technology into:

- Capacitive

- Resistive

- Thermal

By End-Use Industry

Healthcare Sector Shows Strong Growth Potential with Medical Equipment and Wearable Applications

The market is segmented based on end-use industry into:

- Automotive

- Healthcare

- Manufacturing

- Agriculture

- Consumer Electronics

Regional Analysis: High Precision Temperature and Humidity Sensor Market

Asia-Pacific

As the fastest-growing market for high-precision temperature and humidity sensors, Asia-Pacific dominates global demand, driven by rapid industrialization and digital transformation across China, Japan, and South Korea. China alone accounts for over 40% of regional market share due to its robust electronics manufacturing sector and government initiatives like “Made in China 2025” promoting IoT adoption. The region benefits from concentrated semiconductor production facilities requiring stringent environmental monitoring, with sensor demand further amplified by smart city projects across India and Southeast Asia. However, price sensitivity in emerging economies creates a competitive landscape favoring mid-range precision solutions.

North America

North America maintains technological leadership in sensor innovation, with the U.S. spearheading R&D in MEMS-based humidity sensors for mission-critical applications. The region’s stringent FDA and OSHA compliance requirements for pharmaceutical manufacturing and data centers fuel demand for calibration-grade sensors with ±0.1°C accuracy. Recent investments in electric vehicle battery production and climate-controlled vertical farming are creating new growth avenues. Major tech hubs like Silicon Valley continue driving advancements in miniaturized sensors for wearable devices, though supply chain dependencies on Asian component manufacturers pose strategic challenges.

Europe

Europe’s market is characterized by strong regulatory frameworks (EN 60751, EN 60594) ensuring sensor reliability for automotive and industrial applications. Germany’s Industry 4.0 initiatives and Scandinavia’s focus on sustainable building technologies are accelerating digital sensor adoption. The region shows particular strength in high-end industrial applications, where sensors must withstand extreme conditions in food processing and chemical plants. However, slower IoT infrastructure rollout compared to Asia and complex CE certification processes have moderately constrained growth rates, despite the presence of leading manufacturers like Sensirion and STMicroelectronics.

South America

The South American market remains nascent but demonstrates growing potential, particularly in Brazil’s agritech sector where precision agriculture drives demand for environmental monitoring solutions. While economic instability has limited large-scale industrial adoption, increasing foreign investment in renewable energy projects is creating pockets of opportunity for weather-resistant sensors. The lack of localized manufacturing and reliance on imports continue to hinder market expansion, though regional trade agreements are gradually improving sensor accessibility at competitive price points.

Middle East & Africa

This emerging market shows dichotomy – Gulf nations are implementing smart building technologies using advanced sensors for climate control in extreme desert conditions, while Sub-Saharan Africa’s growth is constrained by infrastructure limitations. The UAE’s focus on AI-driven city management and Saudi Arabia’s NEOM project represent high-value opportunities for precision sensors. Across African markets, mobile-based weather monitoring for agriculture shows promise, but counterfeit products and lack of calibration standards remain significant barriers to quality sensor adoption.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High Precision Temperature and Humidity Sensor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 819 million in 2024 and is projected to reach USD 1,368 million by 2032, growing at a CAGR of 7.8%.

- Segmentation Analysis: Detailed breakdown by product type (analog/digital output), application (household appliances, industrial production, environmental monitoring), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Asia-Pacific accounting for 42% market share in 2024.

- Competitive Landscape: Profiles of 15 key players including Sensirion, Bosch, TE Connectivity and STMicroelectronics, covering their market share (top 5 players held 58% share in 2024), product portfolios, and recent M&A activity.

- Technology Trends: Analysis of IoT integration, Industry 4.0 applications, miniaturization trends, and emerging MEMS-based sensor technologies with accuracy levels reaching ±0.1°C for temperature and ±1.5% RH for humidity.

- Market Drivers: Evaluation of growth factors including smart city deployments (projected 135 billion IoT connections by 2030), industrial automation adoption, and climate monitoring requirements.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, IoT platform providers, industrial automation firms, and investors regarding the USD 2.1 billion market opportunity by 2032.

The research employs primary interviews with 35+ industry experts and analysis of 120+ data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Precision Temperature and Humidity Sensor Market?

-> High Precision Temperature and Humidity Sensor Market was valued at 819 million in 2024 and is projected to reach US$ 1368 million by 2032, at a CAGR of 7.8% during the forecast period.

Which key companies dominate this market?

-> Market leaders include Sensirion (18% share), Bosch (15%), TE Connectivity (12%), STMicroelectronics (8%), and Texas Instruments (5%) as of 2024.

What are the primary growth drivers?

-> Key drivers are IoT adoption (growing at 18% CAGR), industrial automation investments (USD 395 billion in 2024), and smart building deployments requiring precise environmental monitoring.

Which region shows highest growth potential?

-> Asia-Pacific dominates with 42% share (2024) and projects 9.2% CAGR through 2032, led by China’s manufacturing and smart city initiatives.

What are the emerging technology trends?

-> Emerging innovations include MEMS-based sensors, wireless sensor networks, AI-enabled predictive monitoring, and ultra-low power designs for IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...