MARKET INSIGHTS

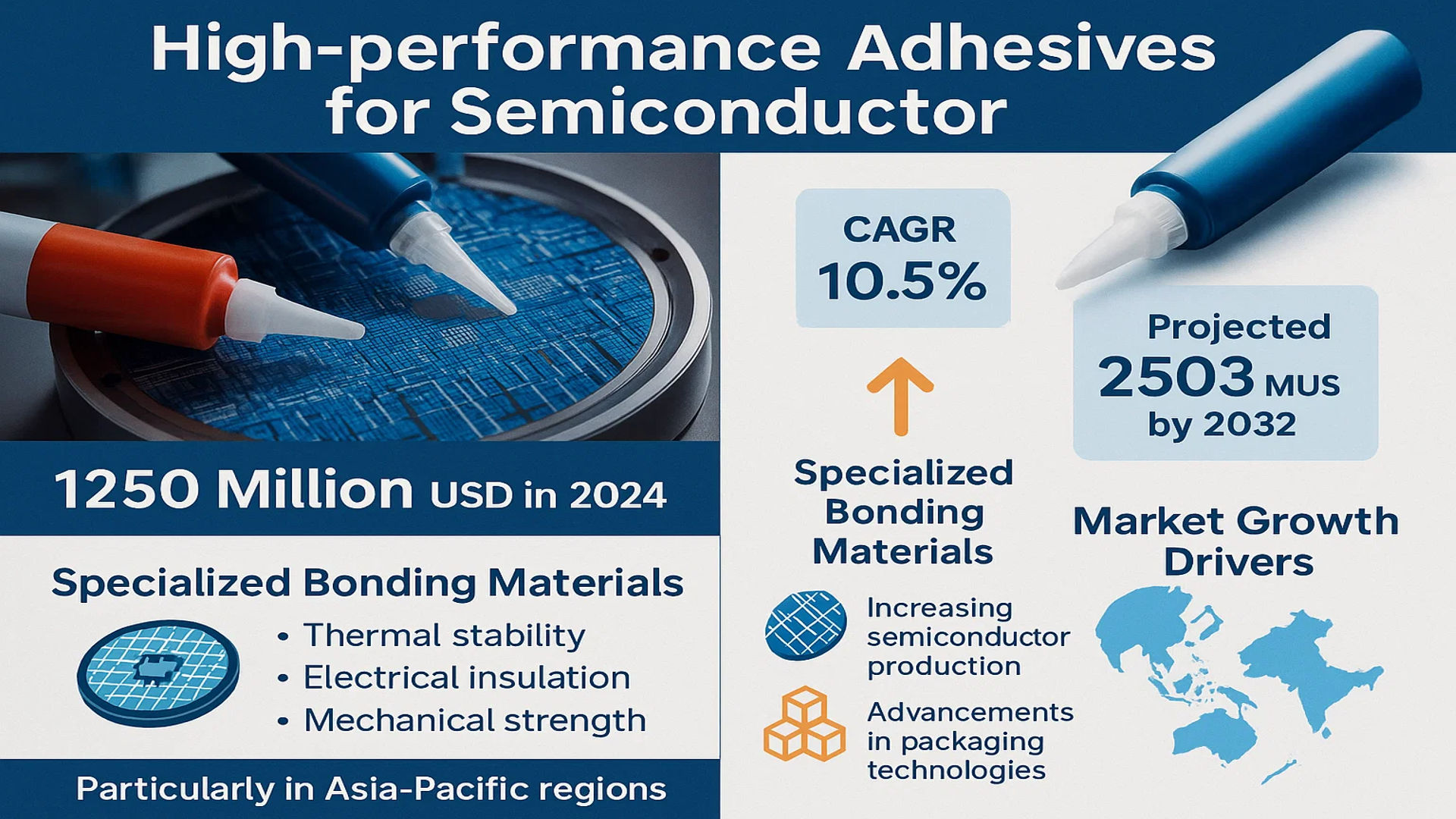

The global High performance Adhesives for Semiconductor Market was valued at 1250 million in 2024 and is projected to reach US$ 2503 million by 2032, at a CAGR of 10.5% during the forecast period.

High-performance adhesives for semiconductors are specialized bonding materials designed to meet the rigorous demands of semiconductor manufacturing. These adhesives provide exceptional thermal stability, electrical insulation, and mechanical strength for critical applications including die attachment, chip bonding, and encapsulation. The materials must withstand extreme processing conditions while maintaining reliability throughout the product lifecycle.

The market growth is driven by increasing semiconductor production, particularly in Asia-Pacific regions, and advancements in packaging technologies like 3D IC and fan-out wafer-level packaging. Epoxy-based adhesives currently dominate the market due to their excellent bonding strength and thermal resistance, while silicone alternatives are gaining traction for flexible applications. Key industry players such as Henkel, DuPont, and 3M continue to innovate adhesive formulations to address emerging challenges in miniaturization and high-density packaging requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Semiconductor Industry to Fuel High-Performance Adhesives Demand

The semiconductor industry is experiencing unprecedented growth, with global semiconductor revenues projected to exceed $600 billion in 2024. This expansion is driving significant demand for high-performance adhesives as they play a critical role in semiconductor packaging and assembly processes. Modern semiconductor devices require adhesives that can withstand extreme temperatures, mechanical stress, and corrosive environments while maintaining electrical stability. The shift toward advanced packaging technologies like 3D IC packaging and wafer-level packaging has particularly increased the need for specialized adhesives with ultra-precise application capabilities.

Growing Adoption of Advanced Electronics to Accelerate Market Growth

The proliferation of 5G technology, IoT devices, and automotive electronics is creating robust demand for semiconductor components, consequently driving the high-performance adhesives market. In the automotive sector alone, semiconductor content per vehicle is expected to double by 2028, necessitating reliable bonding solutions for advanced driver-assistance systems (ADAS) and in-vehicle infotainment. Furthermore, the consumer electronics market continues to push boundaries with thinner, more compact devices requiring adhesives that can maintain structural integrity while enabling miniaturization. The demand for flexible and foldable displays in smartphones represents another key growth area where specialized adhesives are indispensable.

Increasing Investment in Semiconductor Manufacturing Facilities to Drive Market

Governments and private entities worldwide are making substantial investments in semiconductor manufacturing capacity to address global chip shortages and enhance supply chain resilience. The United States recently announced over $50 billion in semiconductor manufacturing incentives, while the European Union has committed similar funds through its Chips Act. These investments are leading to the construction of new fabrication plants and packaging facilities, all of which require high-performance adhesives for equipment assembly and semiconductor packaging processes. This trend is particularly pronounced in Asia, where countries like Taiwan, South Korea, and China continue to expand their semiconductor manufacturing footprint.

MARKET RESTRAINTS

Stringent Performance Requirements to Challenge Market Penetration

The semiconductor industry’s exacting standards present significant challenges for adhesive manufacturers. Adhesives must maintain performance across temperatures ranging from -40°C to 300°C, resist thermal cycling stresses, and demonstrate exceptional reliability over extended periods. Developing formulations that meet these rigorous specifications without compromising bonding strength, electrical properties, or curing characteristics requires substantial R&D investment. Additionally, the need for ultra-low outgassing adhesives for space and high-reliability applications further complicates product development, potentially limiting market accessibility for some manufacturers.

Volatile Raw Material Prices to Constrain Market Growth

The high-performance adhesives market faces pressure from fluctuating prices of key raw materials such as epoxy resins, silicones, and specialty chemicals. Recent supply chain disruptions have caused price variations of up to 30-40% for certain adhesive components, making cost management challenging for manufacturers. This volatility affects profit margins and can lead to price increases for end users, potentially slowing market adoption. Moreover, the industry’s reliance on petroleum-based materials makes it vulnerable to geopolitical factors and energy price fluctuations, creating additional uncertainty in the supply chain.

MARKET CHALLENGES

Complex Application Processes to Hinder Widespread Adoption

Applying high-performance adhesives in semiconductor manufacturing presents numerous technical challenges that can deter adoption. The deposition of adhesives requires precision equipment capable of handling viscosities ranging from 1,000 to 1,000,000 centipoise, with placement accuracy down to micron levels. Achieving consistent bond line thicknesses while accommodating different substrate materials adds further complexity. These application challenges require specialized equipment and trained personnel, increasing implementation costs for semiconductor manufacturers. Additionally, the curing process often requires precise temperature control and may involve UV or thermal activation, necessitating capital investment in specialized curing systems.

MARKET OPPORTUNITIES

Emergence of Eco-friendly Adhesive Solutions to Create New Market Potential

The growing emphasis on sustainability in semiconductor manufacturing presents significant opportunities for innovative adhesive solutions. There is increasing demand for formulations that reduce volatile organic compound (VOC) emissions, eliminate hazardous substances, and enable easier recycling of electronic components. Bio-based adhesives derived from renewable resources are gaining attention, with some formulations demonstrating comparable performance to traditional epoxy systems. The development of adhesives compatible with low-temperature processing can also contribute to energy savings during semiconductor manufacturing, aligning with industry-wide sustainability goals.

Advancements in Nanotechnology to Open New Application Areas

Nanotechnology innovations are creating exciting possibilities for next-generation semiconductor adhesives. The incorporation of nanomaterials like carbon nanotubes and graphene can enhance thermal conductivity while maintaining electrical insulation properties. These advanced materials enable the development of adhesives that simultaneously address thermal management and bonding requirements in high-power semiconductor applications. Furthermore, self-healing adhesive formulations based on nanotechnology principles show promise for improving long-term reliability in harsh operating environments. As semiconductor devices continue to push performance boundaries, these cutting-edge adhesive technologies will play an increasingly vital role in device packaging and assembly.

HIGH-PERFORMANCE ADHESIVES FOR SEMICONDUCTOR MARKET TRENDS

Miniaturization and Advanced Semiconductor Packaging Drive Market Growth

The global high-performance adhesives for semiconductor market is witnessing robust growth, projected to reach $2.5 billion by 2032, driven by the increasing demand for miniaturized electronic components and advanced packaging solutions. As semiconductor devices shrink in size while requiring higher performance, specialized adhesives capable of maintaining strong bonds at micro-scale dimensions have become indispensable. These materials must deliver exceptional thermal conductivity (often exceeding 10 W/m·K for advanced formulations) while providing electrical insulation – properties that conventional adhesives cannot match. The shift toward 3D IC packaging and heterogeneous integration has particularly intensified demand for adhesives with ultra-low bleed characteristics and precise flow control during dispensing processes.

Other Trends

Thermal Management Challenges in High-Power Devices

With semiconductor devices operating at increasingly higher power densities, thermal management has emerged as a critical factor influencing adhesive selection. Modern high-power LEDs and automotive power modules require adhesives that can withstand operating temperatures exceeding 200°C while maintaining structural integrity. This has led to the development of novel filler materials, including boron nitride and aluminum oxide composites, which enhance thermal conductivity without compromising electrical insulation properties. The market for thermally conductive adhesives is growing at approximately 12% annually, outpacing the overall semiconductor adhesive segment.

Material Innovation and Eco-Friendly Solutions

The industry is experiencing significant material innovation, with manufacturers developing halogen-free and low-VOC formulations to meet stringent environmental regulations. Epoxy-based adhesives continue to dominate with over 60% market share, but silicone alternatives are gaining traction in applications requiring greater flexibility and temperature cycling resistance. Recent advancements in nanoparticle-reinforced adhesives have demonstrated remarkable improvements in mechanical strength and moisture resistance, critical for automotive and aerospace applications where reliability under harsh conditions is paramount. The development of room-temperature-cure adhesives with industrial-grade performance characteristics is also reducing energy consumption in semiconductor manufacturing processes.

The Asia-Pacific region, accounting for nearly 45% of global consumption, remains the focal point for high-performance adhesive development, driven by the concentration of semiconductor fabrication facilities and packaging houses in countries like Taiwan, South Korea, and China. Meanwhile, North American and European markets are focusing on specialty formulations for defense and medical applications where reliability standards are particularly stringent. Across all regions, the push toward wafer-level packaging and fan-out technologies continues to create new opportunities for adhesive innovations that can meet the evolving demands of next-generation semiconductor devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation to Maintain Competitive Edge

The global high-performance adhesives for semiconductor market features a dynamic competitive landscape, characterized by established multinational corporations competing alongside specialized adhesive manufacturers. Henkel emerges as a dominant player, leveraging its comprehensive portfolio of epoxy and silicone-based adhesives specifically engineered for semiconductor applications. With manufacturing facilities spanning across North America, Europe, and Asia, Henkel maintains a strong supply chain advantage.

DuPont and 3M closely follow with their technologically advanced adhesive solutions that offer superior thermal conductivity and mechanical stability under extreme conditions. Both companies have significantly invested in R&D to develop formulations that meet the evolving needs of advanced semiconductor packaging and die attach applications.

The market also sees strong participation from regional specialists like TOK in Japan and Heraeus Electronics in Germany, who are expanding their global footprint through strategic acquisitions and partnerships. These companies differentiate themselves through ultra-precise application-specific formulations that address niche requirements in semiconductor manufacturing.

Recent years have witnessed intensified competition as mid-sized players like AI Technology and Laird Performance Materials introduce innovative conductive adhesives with lower curing temperatures – a critical requirement for temperature-sensitive semiconductor components. This technological arms race is driving continuous product enhancements across the sector.

List of Key High-Performance Adhesives for Semiconductor Companies

- Henkel AG & Co. KGaA (Germany)

- DuPont de Nemours, Inc. (U.S.)

- DELO Industrial Adhesives (Germany)

- Meridian Adhesives Group (U.S.)

- Tokyo Ohka Kogyo Co., Ltd. (TOK) (Japan)

- 3M Company (U.S.)

- Heraeus Electronics (Germany)

- Sekisui Chemical Co., Ltd. (Japan)

- AI Technology, Inc. (U.S.)

- United Adhesives Corporation (U.S.)

Segment Analysis:

By Type

Epoxy Segment Leads the Market Due to Superior Binding Strength and Thermal Stability

The market is segmented based on type into:

- Epoxy

- Subtypes: Electrically conductive, Thermally conductive, and others

- Silicone

- Other

- Subtypes: Polyurethane, Acrylic, and specialty formulations

By Application

Semiconductor Packaging Segment Dominates with Highest Adoption in Advanced Chip Manufacturing

The market is segmented based on application into:

- Semiconductor packaging

- Die Attach

- Other

- Subtypes: Encapsulation, Wire bonding, and substrate mounting

By Technology

UV Curable Adhesives Gaining Traction for Faster Processing Times

The market is segmented based on technology into:

- Thermal cure

- UV cure

- Moisture cure

- Others

By End User

IDMs and OSATs Account for Majority Market Share

The market is segmented based on end user into:

- Integrated Device Manufacturers (IDMs)

- Outsourced Semiconductor Assembly and Test (OSAT)

- Foundries

Regional Analysis: High-Performance Adhesives for Semiconductor Market

Asia-Pacific

The Asia-Pacific region dominates the global high-performance adhesives market for semiconductors, accounting for over 45% of total market share in 2024. This leadership position stems from China’s massive semiconductor manufacturing ecosystem and Taiwan’s status as the global hub for chip fabrication. Countries like South Korea and Japan complement this dominance through their advanced electronics industries requiring precision bonding solutions. The region benefits from concentrated demand across the semiconductor value chain – from wafer production to advanced packaging. However, geopolitical tensions and export controls present supply chain risks that could impact adhesive suppliers. Local manufacturers are increasingly investing in R&D to develop next-generation formulations that meet the thermal and mechanical demands of 3D chip stacking and other emerging technologies.

North America

North America represents the second largest market, driven by strong semiconductor R&D activities and reshoring initiatives under the U.S. CHIPS Act. The region shows particular strength in specialty epoxy formulations for military/aerospace applications where reliability under extreme conditions is paramount. California’s Silicon Valley and Arizona’s expanding fab capacity create concentrated demand clusters. Canadian innovators are making strides in low-outgassing adhesives critical for space-grade electronics. Supply chain localization efforts are prompting adhesive manufacturers to establish North American production facilities, though material costs remain higher than Asian alternatives. Regulatory requirements for hazardous substance compliance add another layer of complexity for market participants.

Europe

Europe maintains a strong position in the high-performance adhesives market through technological leadership in automotive semiconductors and industrial electronics. German chemical giants like Henkel and DELO develop specialized formulations meeting stringent EU REACH regulations. The region excels in thermally conductive adhesives for power electronics used in electric vehicles. However, higher production costs compared to Asian manufacturers and limited local semiconductor fabrication capacity create headwinds. Recent EU initiatives like the Chips Act aim to boost domestic semiconductor production, which could drive adhesive demand if successful. Sustainability concerns are pushing development of bio-based adhesive alternatives without compromising performance characteristics.

South America

South America represents an emerging market with growth potential but currently plays a minor role in the global semiconductor adhesive landscape. Brazil shows pockets of demand for consumer electronics assembly, while Argentina has niche applications in automotive sensors. The region suffers from limited local semiconductor manufacturing and reliance on imported electronic components. Economic volatility and currency fluctuations create challenges for adhesive suppliers looking to establish local presence. Some multinational corporations maintain small-scale operations in free trade zones, creating opportunities for regional distributors. As electronics manufacturing gradually expands, demand for basic die-attach adhesives is expected to rise modestly.

Middle East & Africa

This region shows nascent development in semiconductor-related industries, with Israel standing out for its advanced electronics sector and growing fabless chip design ecosystem. Countries like UAE and Saudi Arabia are investing in technology parks that could spur future demand. Currently, adhesive requirements focus primarily on consumer electronics repair and maintenance rather than high-volume manufacturing. Infrastructure limitations and lack of technical expertise constrain market growth, though some global suppliers maintain distribution networks to serve multinational OEMs. Long-term potential exists as part of broader technology investment strategies in Gulf nations, particularly for adhesives used in renewable energy and smart city applications.

Report Scope

This market research report provides a comprehensive analysis of the global High-performance Adhesives for Semiconductor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1,250 million in 2024 and is projected to reach USD 2,503 million by 2032, growing at a CAGR of 10.5%.

- Segmentation Analysis: Detailed breakdown by product type (epoxy, silicone, others), application (semiconductor packaging, die attach, others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates with China expected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including Henkel, DuPont, DELO, Meridian Adhesives Group, TOK, and 3M, their product portfolios, market share (top five held approximately % in 2024), and recent strategic developments.

- Technology Trends & Innovation: Assessment of emerging adhesive technologies, thermal management solutions, and evolving semiconductor packaging requirements.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing semiconductor demand, miniaturization trends) along with challenges (material costs, technical complexities).

- Stakeholder Analysis: Insights for semiconductor manufacturers, adhesive suppliers, investors, and policymakers regarding market opportunities and strategic positioning.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High-performance Adhesives for Semiconductor Market?

->High performance Adhesives for Semiconductor Market was valued at 1250 million in 2024 and is projected to reach US$ 2503 million by 2032, at a CAGR of 10.5% during the forecast period.

Which key companies operate in this market?

-> Key players include Henkel, DuPont, DELO, Meridian Adhesives Group, TOK, 3M, Heraeus Electronics, and Sekisui Chemical, among others.

What are the key growth drivers?

-> Key growth drivers include rising semiconductor demand, advanced packaging technologies, and increasing electronics miniaturization.

Which region dominates the market?

-> Asia-Pacific leads the market, driven by semiconductor manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include high-temperature resistant adhesives, conductive adhesives for advanced packaging, and eco-friendly formulations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...