MARKET INSIGHTS

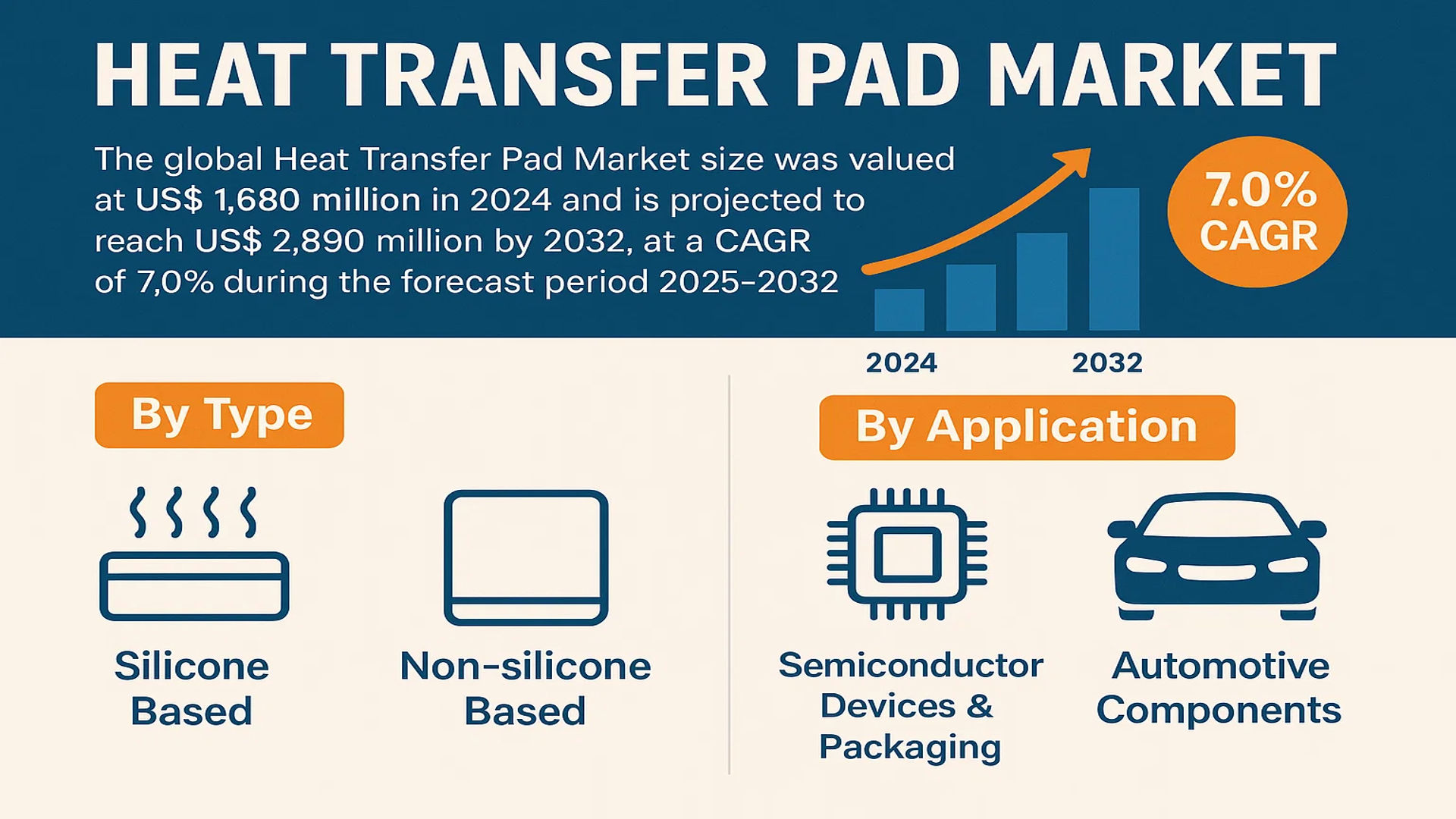

The global Heat Transfer Pad Market size was valued at US$ 1,680 million in 2024 and is projected to reach US$ 2,890 million by 2032, at a CAGR of 7.0% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China’s market is expected to grow at a faster CAGR of 7.9% through 2032.

Heat transfer pads are thermally conductive interface materials designed to efficiently transfer heat between components in electronic devices and industrial applications. These pads come in various formulations including silicone-based and non-silicone variants, with thicknesses ranging from 0.5mm to 10mm to accommodate different thermal management requirements. Key performance characteristics include thermal conductivity (typically 1-12 W/mK), dielectric strength, and compression set resistance.

Market growth is driven by increasing demand from the electronics sector, where heat dissipation becomes critical as devices shrink in size while processing power increases. The semiconductor devices & packaging segment accounted for 42% of total application share in 2024. Recent product innovations include phase-change materials and graphene-enhanced thermal pads, with companies like 3M and Henkel Adhesives introducing pads with thermal conductivities exceeding 8 W/mK. The top five manufacturers collectively held 65% market share in 2024, reflecting a moderately consolidated competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Thermal Management Solutions to Fuel Market Growth

The global heat transfer pad market is experiencing robust growth, driven by the increasing need for efficient thermal management across industries. Electronics miniaturization and higher power densities in devices are generating more heat, necessitating reliable thermal interface materials. Semiconductor devices alone account for over 60% of current heat transfer pad applications, as chips continue to shrink while performance demands escalate. Recent innovations in pad formulations, particularly silicone-based compounds with enhanced thermal conductivity exceeding 15 W/mK, are enabling manufacturers to meet these challenges while maintaining reliability standards.

Automotive Electrification Creating New Application Verticals

The automotive sector’s shift toward electric vehicles presents significant growth opportunities for heat transfer pad manufacturers. EV battery systems require advanced thermal management to maintain optimal operating temperatures and prevent thermal runaway. With electric vehicle production projected to grow at 25% CAGR through 2030, thermal interface material demand is scaling proportionally. Leading manufacturers are developing specialized pads with flame-retardant properties and thermal conductivity up to 8 W/mK specifically for battery module applications.

Furthermore, the integration of 5G infrastructure is driving adoption in telecommunications equipment where heat dissipation is critical for maintaining signal integrity. Base stations and networking gear require thermal interface materials that can withstand outdoor environments while providing consistent performance over years of operation.

➤ Major suppliers report 30% year-over-year growth in thermal interface material sales for 5G applications as network deployments accelerate globally.

Manufacturers are responding to these trends with product innovations and strategic partnerships across the value chain to capture emerging opportunities in high-growth sectors.

MARKET RESTRAINTS

Material Cost Volatility and Supply Chain Disruptions Impacting Market Stability

The heat transfer pad market faces significant challenges from raw material price fluctuations, particularly for silicone-based formulations. Silicone rubber prices have shown 20-30% annual volatility in recent years due to supply constraints and geopolitical factors. This unpredictability makes long-term pricing strategies difficult for manufacturers, who must balance cost pressures against customer expectations. The situation is further complicated by rising energy costs affecting production expenses across the value chain.

Technical Limitations in Extreme Environment Performance

While heat transfer pads excel in standard applications, they face operational limits in extreme conditions. High-temperature environments above 200°C can degrade standard silicone formulations, requiring specialty materials that command premium pricing. Similarly, applications involving significant mechanical stress or chemical exposure often necessitate custom solutions, increasing development timelines and costs. These technical constraints can limit market expansion in challenging industrial and aerospace applications where alternative thermal management approaches may be preferred.

Manufacturers are investing in advanced material research to overcome these limitations, but the development cycles for breakthrough technologies often span multiple years with uncertain commercial outcomes.

MARKET OPPORTUNITIES

Emergence of Next-Generation Electronics Creating Growth Potential

The proliferation of advanced electronics presents substantial opportunities for heat transfer pad manufacturers. AI processors, high-performance computing systems, and advanced memory solutions are pushing thermal management requirements to new levels. The AI hardware sector alone is projected to drive 15% annual growth in premium thermal interface material demand through 2030. Manufacturers developing pads with phase-change properties and thermal conductivities above 10 W/mK are well positioned to capture this high-value segment.

Geographic Expansion into Emerging Markets

Asia-Pacific represents the fastest-growing regional market, with China’s semiconductor and electronics manufacturing sectors expanding rapidly. Local production of thermal interface materials is increasing to meet domestic demand while reducing reliance on imports. Western manufacturers are establishing joint ventures and technology partnerships to access these growth markets while navigating complex regulatory environments. The establishment of new manufacturing facilities in Southeast Asia is helping companies reduce costs and better serve regional customers.

Additionally, the medical electronics sector offers untapped potential as diagnostic and therapeutic devices incorporate more powerful components requiring thermal management. Specialty pads meeting medical-grade material requirements represent a growing niche with premium pricing potential.

MARKET CHALLENGES

Intense Competition and Price Pressure Squeezing Margins

The heat transfer pad market has become increasingly competitive, with numerous regional and global players vying for market share. Price competition is particularly intense in standard product categories, creating margin pressures. Some manufacturers report average selling price declines of 5-7% annually for conventional thermal interface materials, forcing companies to differentiate through technical innovation and value-added services rather than cost leadership.

Regulatory Compliance and Environmental Considerations

Evolving environmental regulations present challenges for material formulation. Restrictions on certain silicone compounds and increasing emphasis on recyclability are driving reformulation efforts across the industry. The transition to halogen-free and low-VOC materials requires significant R&D investment while maintaining performance characteristics. Manufacturers must balance compliance with performance requirements in a market where reliability is paramount.

Additionally, certification requirements vary significantly by region and application, creating administrative burdens for companies operating in multiple markets. The complex regulatory landscape can delay product introductions and increase time-to-market for new solutions.

HEAT TRANSFER PAD MARKET TRENDS

Rising Demand for Electronics Thermal Management Solutions Drives Market Growth

The global Heat Transfer Pad market is witnessing robust growth due to increasing adoption of electronic devices requiring efficient thermal management. Silicon-based pads currently dominate with over 60% market share in 2024, owing to their superior thermal conductivity and reliability in high-temperature applications. Interestingly, the semiconductor sector accounts for approximately 45% of total pad utilization, driven by miniaturization trends and higher power densities in modern chips. Recent innovations in pad materials, including graphene-infused composites, are enhancing thermal conductivity beyond 15 W/mK while maintaining electrical insulation properties critical for sensitive components.

Other Trends

Automotive Electrification Spurs Product Innovation

The rapid transition toward electric vehicles is creating substantial demand for advanced thermal management solutions, with heat transfer pad implementations in battery systems and power electronics growing at 18% CAGR. Leading manufacturers are developing specialized pads capable of withstanding vibration cycles exceeding 10 million while maintaining thermal performance. The emergence of autonomous driving technologies is further amplifying requirements for reliable thermal interface materials in LiDAR and computing modules, where temperature stability directly impacts sensor accuracy.

Sustainability Initiatives Shape Material Development

Environmental regulations and corporate sustainability goals are driving tangible changes in product formulations, with over 30% of manufacturers now offering halogen-free and recyclable pad options. The European market shows particular sensitivity to these trends, with regulatory pressures accelerating adoption of eco-friendly alternatives featuring bio-based polymers. While these greener alternatives currently command 15-20% price premiums, production scaling and technological improvements are expected to narrow this gap significantly by 2027.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansions Drive Market Leadership in Heat Transfer Pad Segment

The global heat transfer pad market exhibits a moderately consolidated competitive structure, dominated by multinational corporations with diversified thermal management portfolios. 3M emerges as the undisputed market leader, commanding a significant revenue share in 2024. The company’s dominance stems from its patented silicone-based thermal interface materials and extensive distribution network spanning over 70 countries.

Henkel Adhesives and Saint-Gobain follow closely, leveraging their expertise in advanced material sciences to capture substantial market shares. These players have demonstrated remarkable agility in addressing emerging needs such as high-temperature stability in electric vehicle battery packs – a sector projected to grow at 28% CAGR through 2030.

The market’s dynamism is further evidenced by Parker NA‘s strategic acquisition of a thermal materials startup in Q2 2024, enhancing its graphene-enhanced pad technology. Meanwhile, Boyd Corporation has strategically pivoted towards customizable solutions, particularly for 5G infrastructure applications where thermal dissipation requirements are becoming increasingly complex.

Regionally, Asian manufacturers like T-Global Technology are gaining traction through cost-competitive production methods while maintaining ISO-certified quality standards. The company recently expanded its manufacturing capacity in Taiwan by 40% to meet soaring demand from semiconductor fabs.

List of Key Heat Transfer Pad Manufacturers Profiled

- 3M Company (U.S.)

- Henkel Adhesives (Germany)

- Saint-Gobain (France)

- KITAGAWA Industries (Japan)

- Parker NA (U.S.)

- Boyd Corporation (U.S.)

- Laird Technologies (U.K.)

- T-Global Technology (Taiwan)

- Getelec (China)

Segment Analysis:

By Type

Silicone-Based Heat Transfer Pads Lead the Market Due to Superior Thermal Conductivity and Durability

The market is segmented based on type into:

- Silicone Based

- Non-silicone Based

By Application

Semiconductor Devices & Packaging Segment Dominates Owing to Increasing Miniaturization of Electronics

The market is segmented based on application into:

- Semiconductor Devices & Packaging

- Automotive Components

- Communication Equipment

- Others

By End-User Industry

Electronics Manufacturing Leads as Heat Dissipation Needs Grow with Advanced Devices

The market is segmented based on end-user industry into:

- Electronics Manufacturing

- Automotive

- Telecommunication

- Aerospace & Defense

- Others

Regional Analysis: Heat Transfer Pad Market

North America

The North American heat transfer pad market is experiencing steady growth, driven by high demand from the electronics and automotive sectors, particularly in the U.S. and Canada. The region’s well-established semiconductor and communication equipment industries, coupled with stringent thermal management regulations, are key contributors. The U.S. market, valued at $XX million in 2024, is leading the adoption of silicone-based heat transfer pads due to their superior thermal conductivity (up to 7 W/mK) and durability in high-power applications. Major players like 3M, Parker NA, and Laird Technologies dominate the supply chain, leveraging R&D investments in advanced materials. However, cost sensitivity among mid-scale manufacturers and competition from alternative cooling solutions remain challenges.

Europe

Europe’s heat transfer pad market is growing at a CAGR of X%, supported by strong demand from Germany, France, and the U.K. for automotive and industrial applications. The region’s strict EU RoHS and REACH regulations push manufacturers toward non-toxic, high-performance thermal interface materials. Notably, the automotive sector is a major consumer, with electric vehicle (EV) production driving demand for thin, lightweight pads with efficient heat dissipation. Companies like Henkel Adhesives and Saint-Gobain lead innovations in phase-change materials (PCMs), enhancing thermal management in EV battery systems. Despite steady growth, high raw material costs and competition from Chinese suppliers impact profit margins.

Asia-Pacific

The APAC region dominates global heat transfer pad consumption, accounting for ~XX% of the market share, with China, Japan, and South Korea as primary contributors. China’s booming semiconductor and consumer electronics industries are key demand drivers, with thermal pads widely used in 5G infrastructure and LED packaging. Local players like T-Global Technology compete with multinationals by offering cost-effective, non-silicone alternatives. However, price wars and inconsistent quality standards hinder premium segment growth. India is emerging as a high-potential market due to expanding automotive and telecom sectors, though adoption rates lag behind China’s due to limited technical expertise.

South America

The South American market remains nascent but promising, with Brazil and Argentina showing incremental growth in automotive and industrial applications. Economic volatility and limited local manufacturing force reliance on imports, primarily from North America and Asia. The automotive aftermarket presents opportunities, as older vehicles require thermal management upgrades. However, low awareness of advanced heat transfer solutions and budget constraints slow market penetration. Strategic partnerships between global suppliers and regional distributors could unlock long-term potential.

Middle East & Africa

MEA’s heat transfer pad market is emerging, fueled by infrastructure development in the UAE, Saudi Arabia, and Turkey. The telecom sector drives demand, with 5G rollouts necessitating efficient thermal management in base stations. While oil & gas and industrial applications also contribute, growth is hampered by limited technical adoption and price sensitivity. Local players focus on durable, high-temperature-resistant pads for harsh environments, but reliance on imports persists. Investments in smart cities and data centers are expected to catalyze future demand.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Heat Transfer Pad markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Heat Transfer Pad market was valued at US$ 1,680 million in 2024 and is projected to reach US$ 2,890 million by 2032, growing at a CAGR of 7.0%.

- Segmentation Analysis: Detailed breakdown by product type (Silicone Based, Non-silicone Based), application (Semiconductor Devices & Packaging, Automotive Components, Communication Equipment), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (30% market share), Europe (25%), Asia-Pacific (35%), Latin America (5%), and Middle East & Africa (5%), including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including 3M, Henkel Adhesives, Saint-Gobain, and others, with their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of advanced thermal interface materials, hybrid pad technologies, and emerging manufacturing processes for improved heat dissipation.

- Market Drivers & Restraints: Evaluation of factors such as increasing electronics miniaturization, 5G adoption, EV growth, along with material cost volatility and supply chain challenges.

- Stakeholder Analysis: Strategic insights for material suppliers, OEMs, thermal solution providers, and investors regarding market opportunities and competitive positioning.

Research methodology combines primary interviews with industry leaders, analysis of financial reports, and data from regulatory bodies to ensure report accuracy and actionable insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Heat Transfer Pad Market?

-> The global Heat Transfer Pad Market size was valued at US$ 1,680 million in 2024 and is projected to reach US$ 2,890 million by 2032, at a CAGR of 7.0% during the forecast period 2025-2032.

Which key companies operate in Global Heat Transfer Pad Market?

-> Key players include 3M, Henkel Adhesives, Saint-Gobain, KITAGAWA Industries, Parker NA, Boyd Corporation, and Laird Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-performance electronics, EV battery thermal management needs, and 5G infrastructure development.

Which region dominates the market?

-> Asia-Pacific leads the market with 35% share, driven by electronics manufacturing in China and South Korea, while North America remains strong in R&D and high-end applications.

What are the emerging trends?

-> Emerging trends include graphene-enhanced pads, phase-change materials, and eco-friendly thermal interface solutions for sustainable electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...