HBM3E Memory Market Insights

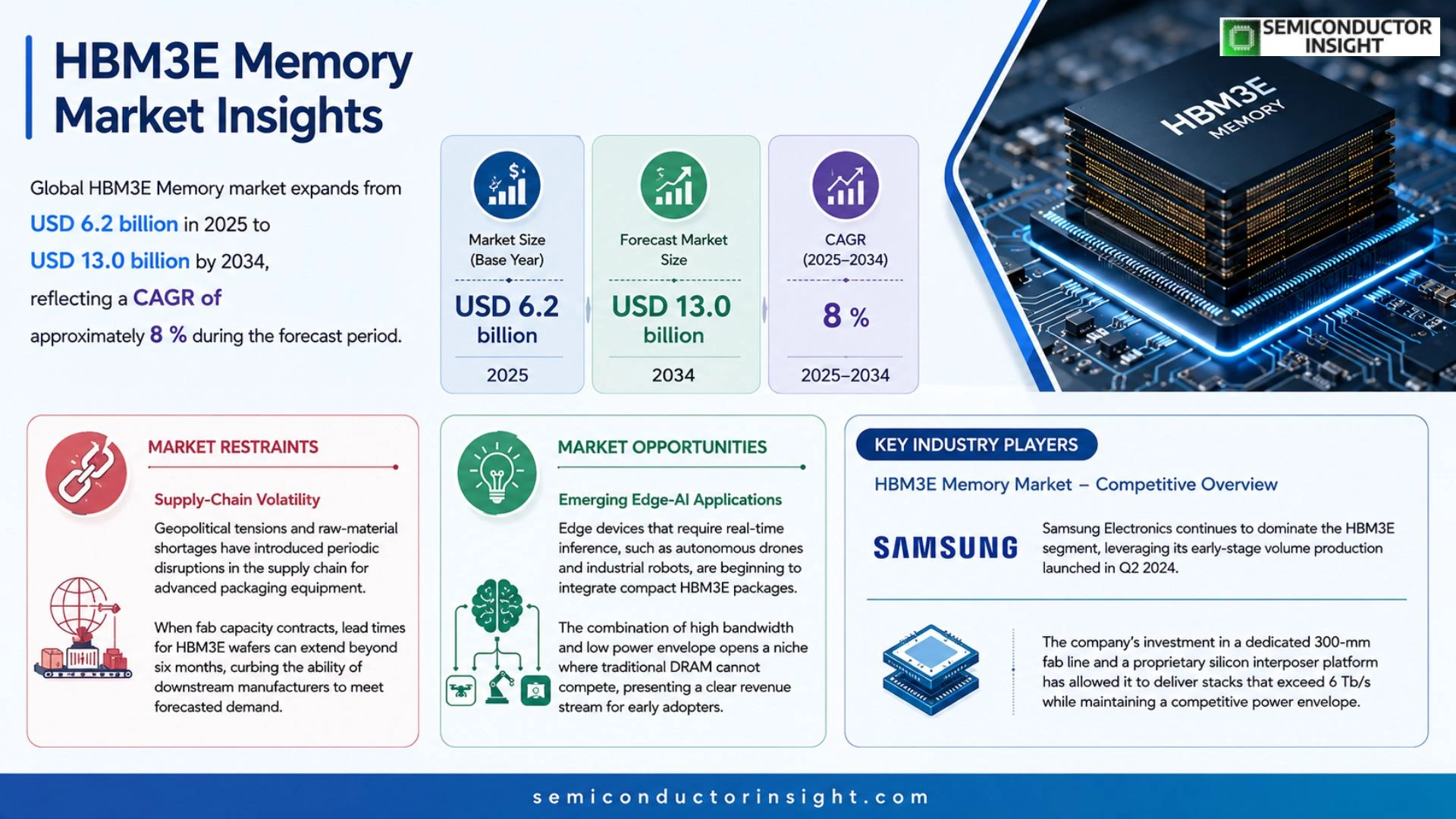

Global HBM3E Memory Market size was valued at USD 6.2 billion in 2025. The market expands from USD 6.2 billion in 2025 to USD 13.0 billion by 2034, reflecting a CAGR of approximately 8 % during the forecast period.

HBM3E represents the latest generation of high‑bandwidth memory engineered for AI inference, graphics rendering and high‑performance computing workloads. It extends the HBM3 architecture with data rates exceeding 6 Tb/s per stack and enhanced thermal efficiency achieved through silicon interposer advances.

The upward trajectory stems from surging demand for AI accelerators in data centers, rollout of next‑generation GPUs and emergence of autonomous‑vehicle platforms that require ultra‑fast memory access. Recent announcements such as Samsung’s commencement of volume production for HBM3E chips in Q2 2024 underscore industry momentum. Leading suppliers,including Samsung Electronics, SK Hynix and Micron Technology,continue expanding their portfolios to satisfy these performance‑driven requirements.

MARKET DRIVERS

Performance Demands from AI Accelerators

Leading chip designers are re‑architecting AI processors to capitalize on the bandwidth that HBM3E Memory Market supplies. The shift from traditional DRAM to stacked‑die solutions means that data‑intensive workloads,such as large‑language‑model inference,can be executed with markedly lower latency. Manufacturers that secure early access to HBM3E stacks will differentiate their offerings and command premium pricing.

Growth of High‑Performance Computing (HPC) Infrastructure

Universities and cloud providers are expanding exascale clusters, a move that forces a rethink of memory hierarchies. The sub‑nanosecond access times of HBM3E enable tighter coupling between compute and storage tiers, directly translating into higher throughput for scientific simulations. This operational advantage encourages procurement cycles that favor the latest stacked memory technology.

➤ “Adoption of HBM3E is less about capacity and more about delivering the bandwidth envelope required for next‑gen AI workloads.”

Venture capital trends also reveal heightened interest in start‑ups building custom ASICs around HBM3E. The convergence of financing, performance pressure, and ecosystem readiness creates a virtuous cycle that accelerates market momentum.

MARKET CHALLENGES

Manufacturing Yield Constraints

Stacked‑die processes remain sensitive to wafer‑level defects, causing yield rates that fluctuate between 70% and 85% depending on fab maturity. Inconsistent yields inflate unit costs, making it difficult for midsize OEMs to justify the investment when budget constraints loom.

Other Challenges

Integration Complexity

System architects must redesign PCB layouts and power delivery networks to accommodate the taller stack height of HBM3E modules. This redesign often extends product development timelines, slowing time‑to‑market for new generations of servers.

MARKET RESTRAINTS

Supply‑Chain Volatility

Geopolitical tensions and raw‑material shortages have introduced periodic disruptions in the supply chain for advanced packaging equipment. When fab capacity contracts, lead times for HBM3E wafers can extend beyond six months, curbing the ability of downstream manufacturers to meet forecasted demand.

MARKET OPPORTUNITIES

Emerging Edge‑AI Applications

Edge devices that require real‑time inference,such as autonomous drones and industrial robots,are beginning to integrate compact HBM3E packages. The combination of high bandwidth and low power envelope opens a niche where traditional DRAM cannot compete, presenting a clear revenue stream for early adopters.

HBM3E Memory Market Trends

AI‑Driven Demand Accelerates HBM3E Adoption

The emergence of AI‑centric workloads in hyperscale data centers has turned HBM3E Memory Market dynamics onto a steep upward path. By 2025 the market recorded a valuation of roughly USD 6.2 billion, and forecasting models indicate a near‑doubling to USD 13.0 billion by 2034. This expansion mirrors the rapid rollout of next‑generation GPUs and dedicated AI inference chips that require bandwidth exceeding 6 Tb/s per stack. The ability of HBM3E to sustain such rates while limiting power draw makes it the preferred substrate for training large language models and real‑time inference engines. Consequently, manufacturers are prioritising volume production, a move underscored by Samsung’s Q2‑2024 commencement of HBM3E chip shipments, signaling confidence in sustained demand.

Other Trends

Supply Chain Diversification and Capacity Scaling

Leading suppliers,Samsung Electronics, SK Hynix, and Micron Technology,have announced multi‑fab line expansions to hedge against geopolitical volatility and raw‑material shortages. By leveraging silicon interposer advancements, they can integrate larger stack counts without compromising thermal margins. This strategic scaling not only reduces lead times for large‑scale AI customers but also creates a competitive buffer that encourages price stabilization as volumes climb. The ripple effect extends to equipment vendors, who are accelerating the development of lithography tools tailored to the finer pitches demanded by HBM3E stacks, thereby tightening the ecosystem around the memory technology.

Thermal Efficiency Innovations Shape Future Deployments

Beyond raw throughput, the HBM3E Memory Market is being reshaped by breakthroughs in thermal management. Enhanced silicon interposers now incorporate micro‑channel cooling pathways, allowing the memory to operate at higher frequencies without triggering throttling mechanisms. These innovations are critical for autonomous‑vehicle platforms where latency budgets are unforgiving and environmental temperatures can swing dramatically. As OEMs integrate AI accelerators directly into edge devices, the need for compact, power‑efficient memory becomes a decisive factor in system architecture decisions. Companies that master this balance are poised to capture a larger share of the emerging edge AI segment, turning thermal efficiency from an engineering nuance into a market differentiator.

COMPETITIVE LANDSCAPE

Key Industry Players

HBM3E Memory Market – Competitive Overview

Samsung Electronics continues to dominate the HBM3E segment, leveraging its early‑stage volume production launched in Q2 2024. The company’s investment in a dedicated 300‑mm fab line and a proprietary silicon interposer platform has allowed it to deliver stacks that exceed 6 Tb/s while maintaining a competitive power envelope. SK Hynix follows closely, differentiating its offering through a staggered‑layer architecture that improves yield on 8‑stack configurations. Micron Technology rounds out the triad, focusing on a modular approach that enables rapid scaling for AI‑centric data‑center accelerators. Collectively, these three manufacturers command the bulk of global shipments, shaping pricing dynamics and setting performance baselines that downstream OEMs must accommodate. Their aggressive roadmap, anchored by successive process‑node shrinkage, forces the supply chain to prioritize advanced packaging services and drives a cascade of investment across substrate suppliers.

Beyond the core trio, a constellation of secondary players exerts measurable influence on the HBM3E value chain. Intel Corporation, while not a direct fab, negotiates long‑term supply agreements with Micron to secure bespoke stacks for its Xeon GPU line, effectively aligning its product roadmap with memory capabilities. AMD and NVIDIA, as system‑level designers, dictate specification tolerances that ripple back to the memory makers, compelling incremental improvements in thermal management. Taiwan Semiconductor Manufacturing Co. (TSMC) and United Microelectronics Corp. (UMC) provide foundry capacity for niche customers, enabling smaller fabless firms to enter the market. Assembly specialists such as ASE Technology Holding and packaging innovators like Powerchip Semiconductor Manufacturing contribute critical interposer and test services. Regional players including Nanya Technology, Winbond Electronics, and Powerchip further diversify the supply base, offering cost‑effective alternatives for mid‑range AI workloads. Their presence tempers concentration risk and encourages competitive pricing across the ecosystem.

List of Key HBM3E Memory Companies Profiled

- Samsung Electronics

- SK Hynix

- Micron Technology

- Intel Corporation

- Advanced Micro Devices (AMD)

- NVIDIA Corporation

- TSMC

- ASE Technology Holding

- Nanya Technology Corp.

- Winbond Electronics Corp.

- Powerchip Semiconductor Manufacturing Corp.

- United Microelectronics Corp. (UMC)

- Vanguard International Semiconductor

- ChipMOS Technologies

- SK Hynix Advanced Memory Solutions

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Stacked HBM3E

|

| By Application |

|

AI Inference

|

| By End User |

|

Data Center Operators

|

| By Integration Form |

|

Silicon Interposer

|

| By Performance Tier |

|

Enhanced Thermal Efficiency

|

Regional Analysis: HBM3E Memory Market

North America

Enterprises deploying large‑scale transformer models are consuming HBM3E at a pace that outstrips legacy memory families. The heightened bandwidth per pin translates directly into reduced training cycles, prompting data‑center operators to allocate budget toward memory upgrades that promise measurable time‑to‑insight gains.

Recent legislative frameworks incentivize domestic wafer fabs and packaging facilities. As a result, several North American consortia are establishing “fab‑to‑fab” pipelines that minimise exposure to overseas logistics disruptions while preserving high‑volume output.

EDA vendors have released specialized modules that model HBM3E thermal and power characteristics. These tools enable chip designers to optimise stack configurations early, reducing costly silicon re‑spins and shortening time‑to‑market.

Alliances between memory manufacturers and GPU producers are deepening, with joint road‑maps that align process node shrinks with memory bandwidth targets, ensuring that future platforms can fully exploit HBM3E capabilities.

Europe

European stakeholders are leveraging the HBM3E Memory Market to reinforce their position in high‑performance computing for scientific research and automotive safety systems. Robust funding mechanisms from the EU’s Horizon programmes are encouraging collaborative projects that integrate HBM3E into heterogeneous compute nodes for climate‑modeling simulations. Meanwhile, regulatory emphasis on energy efficiency is nudging OEMs toward memory solutions that deliver superior performance per watt, a metric where HBM3E excels. German and French chip designers are capitalising on this environment, aligning their product pipelines with the memory’s low‑latency profile to meet stringent automotive functional‑safety standards. The cumulative effect is a growing niche market that balances innovation with compliance, offering manufacturers a differentiated value proposition within the continent.

Asia‑Pacific

The Asia‑Pacific region is witnessing a surge in HBM3E adoption as manufacturers pursue aggressive road‑maps for edge AI and 5G‑enabled infrastructure. Nations such as South Korea and Taiwan, home to some of the world’s most advanced foundries, are scaling capacity to accommodate larger die‑stack counts. Concurrently, Chinese cloud providers are experimenting with HBM3E to accelerate workloads that demand both high bandwidth and low power draw, despite ongoing trade constraints. This dynamic fosters a competitive landscape where design houses must balance performance ambitions against geopolitical considerations, prompting a diversification of supply channels and an emphasis on intellectual‑property protection. The region’s rapid product cycles are likely to pressure global pricing norms and stimulate incremental innovations in packaging technologies.

South America

In South America, the HBM3E Memory Market is still emerging, but early adopters in Brazil’s fintech sector are recognizing its potential to shorten transaction processing times for AI‑driven fraud detection engines. Local system integrators are partnering with multinational memory suppliers to establish pilot production lines that focus on low‑volume, high‑value applications such as scientific instrumentation and satellite communications. Government incentives aimed at expanding digital infrastructure are gradually creating a more favourable investment climate, encouraging firms to upgrade from conventional DRAM to HBM3E in order to achieve competitive differentiation. While the market remains modest, the strategic alignment of technology readiness with policy support hints at a trajectory toward broader uptake in the next few years.

Middle East & Africa

The Middle East & Africa is leveraging HBM3E to underpin ambitious smart‑city initiatives and oil‑field data analytics platforms. United Arab Emirates’ sovereign wealth funds have allocated capital to joint ventures that explore high‑bandwidth memory for real‑time seismic processing, a use‑case where latency reductions can translate into measurable cost savings. Meanwhile, South Africa’s academic institutions are piloting HBM3E‑based clusters to support genomic research, positioning the nation as a regional hub for bio‑informatics. Despite infrastructural challenges, targeted public‑private collaborations are catalysing a niche ecosystem that values performance gains over sheer volume, suggesting a gradual but purposeful market evolution across the region.

Report Scope

This market research report provides a comprehensive analysis of the HBM3E Memory Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of HBM3E Memory Market?

-> HBM3E Memory Market expands from USD 6.2 billion in 2025 to USD 13.0 billion by 2034, reflecting a CAGR of approximately 8 %.

Which key companies operate in HBM3E Memory Market?

-> Key players include Samsung Electronics, SK Hynix, and Micron Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for AI accelerators in data centers, rollout of next‑generation GPUs, and the emergence of autonomous‑vehicle platforms requiring ultra‑fast memory access.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains a dominant market due to its strong semiconductor ecosystem.

What are the emerging trends?

-> Emerging trends include volume production of HBM3E chips (e.g., Samsung’s Q2 2024 launch), integration with high‑performance GPUs, and data‑rate improvements exceeding 6 Tb/s per stack.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...