MARKET INSIGHTS

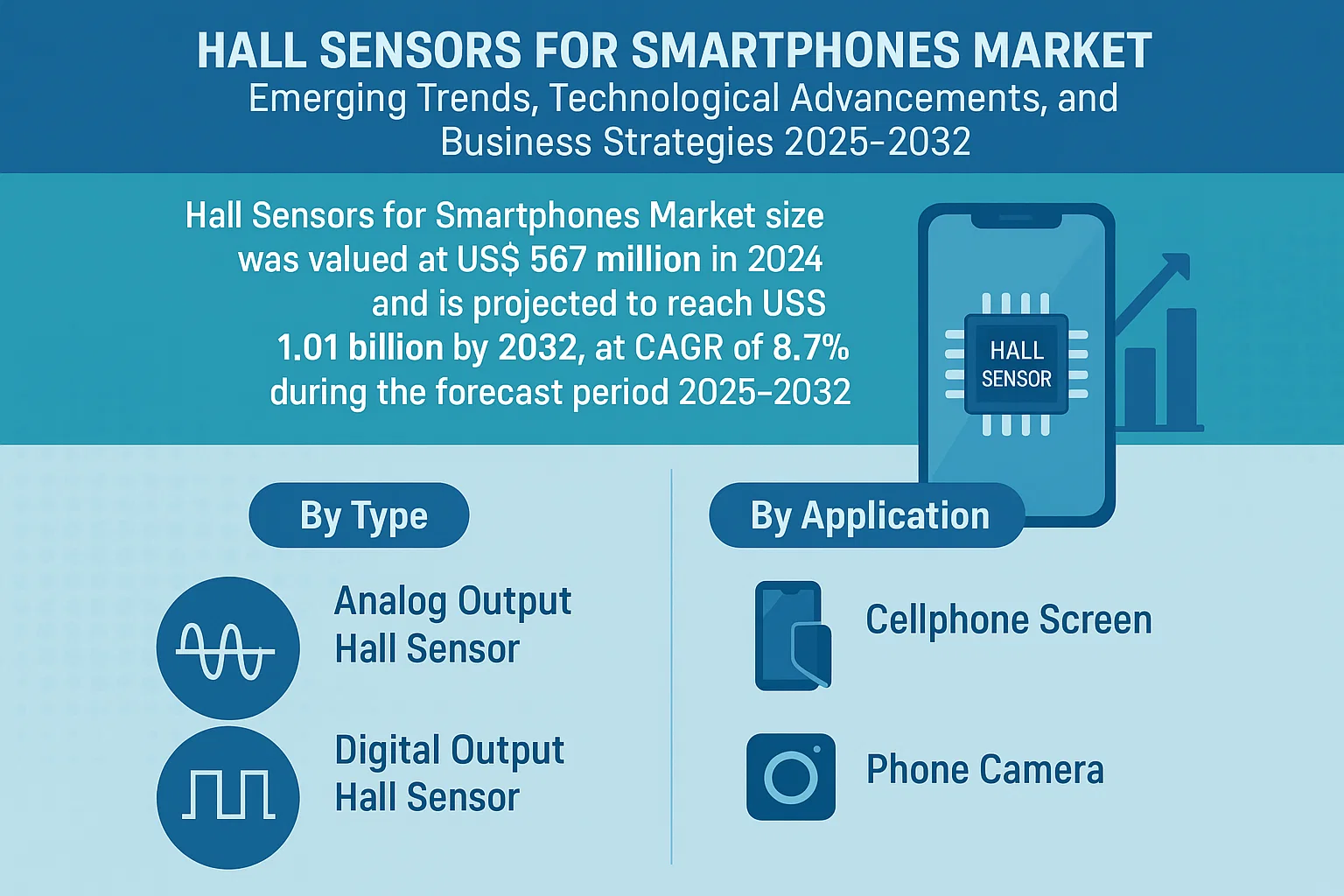

The global Hall Sensors for Smartphones Market size was valued at US$ 567 million in 2024 and is projected to reach US$ 1.01 billion by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Hall sensors for smartphones are magnetic field sensors that detect changes in magnetic flux density. These compact semiconductor devices enable key smartphone functionalities like automatic screen wake/sleep when flip covers are opened/closed. Their ability to precisely measure magnetic fields without physical contact makes them ideal for space-constrained mobile applications.

The market growth is driven by increasing smartphone adoption, particularly foldable devices which extensively use Hall sensors for hinge position detection. Furthermore, the rising demand for power-efficient components in mobile devices is accelerating sensor integration. Key players like TDK and Texas Instruments are expanding their Hall sensor portfolios to capitalize on this growth, with recent advancements focusing on ultra-low power consumption and miniaturization for 5G smartphones.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Flip and Foldable Smartphones Accelerates Hall Sensor Adoption

The global smartphone industry is witnessing a paradigm shift with foldable devices gaining substantial traction, projected to grow at a compound annual growth rate exceeding 50% between 2024 and 2030. Hall sensors play a pivotal role in detecting cover positions in these premium devices, automatically locking/unlocking screens for enhanced power efficiency. Major manufacturers like Samsung, Huawei, and Oppo have integrated these sensors across their flagship foldable models, with over 60% of all foldable smartphones shipped in 2023 incorporating Hall-effect technology. This trend is expected to intensify as component costs decline and flexible display technology matures.

Energy Efficiency Requirements Drive Smart Sensor Integration

Modern smartphones demand sophisticated power management solutions, with Hall sensors emerging as energy-efficient alternatives to mechanical switches. Current-generation sensors consume up to 80% less power than conventional switching mechanisms while offering higher reliability. With smartphone OEMs targeting 20-30% reductions in standby power consumption, the market for ultra-low-power digital Hall sensors has expanded significantly. Several leading manufacturers have introduced nano-power variants consuming less than 3µA, making them ideal for always-on applications in premium devices.

Camera Automation and Advanced Features Fuel Component Demand

Hall sensors are increasingly deployed in smartphone camera modules for precise lens positioning and stabilization. Higher-end devices now incorporate multiple sensors per camera array, with some flagship models utilizing up to three Hall sensors per pop-up or periscope camera mechanism. The growing consumer demand for professional-grade mobile photography, coupled with trends toward higher megapixel counts and optical zoom capabilities, has created substantial opportunities for sensor manufacturers. Emerging applications in augmented reality positioning systems are further expanding the addressable market.

MARKET RESTRAINTS

Price Sensitivity in Mid-Range Smartphones Limits Market Penetration

While Hall sensors have become standard in premium devices, adoption remains limited in mid-range and budget smartphone segments where BoM optimization is critical. The additional $0.50-$1.50 per unit cost for Hall sensor implementation presents a significant barrier in price-sensitive markets, particularly in developing regions where over 70% of smartphone sales fall below the $300 price point. Many manufacturers continue to employ traditional mechanical switches or omit cover detection features entirely in these segments, constraining market growth potential.

Miniaturization Challenges Impact Sensor Performance

The relentless drive toward thinner smartphone designs has created engineering challenges for Hall sensor manufacturers. Current-generation sensors must maintain sensitivity while occupying less than 1mm3 of board space—a 40% reduction compared to 2020 standards. This extreme miniaturization can compromise magnetic field detection capabilities, particularly in devices with metallic frames that interfere with sensor operation. Several leading smartphone OEMs have reported increased calibration requirements and field failures related to sensor placement in their latest ultra-thin models.

Supply Chain Complexities Create Production Bottlenecks

Hall sensors require specialized semiconductor fabrication processes that differ from mainstream CMOS production lines. With global semiconductor capacity already strained, manufacturers face challenges securing consistent production slots for sensor components. The industry has experienced lead time extensions of 10-15 weeks for Hall sensor ICs in recent quarters, compared to historical averages of 6-8 weeks. This has forced some smartphone makers to redesign subsystems or delay product launches, negatively impacting market expansion.

MARKET OPPORTUNITIES

Emerging AR/VR Applications Open New Use Cases

The rapid development of augmented and virtual reality platforms presents significant opportunities for Hall sensor providers. Next-generation AR glasses and VR headsets increasingly incorporate magnetic tracking systems that utilize precision Hall sensors for positional accuracy. Early implementations in prototype devices demonstrate sub-millimeter tracking precision, a critical requirement for immersive experiences. With the AR/VR device market projected to exceed 50 million annual units by 2027, sensor manufacturers are developing specialized low-latency variants optimized for head-mounted displays.

Advanced Packaging Technologies Enable System Integration

Innovations in 3D packaging and heterogeneous integration are creating opportunities for Hall sensor suppliers to develop more compact and cost-effective solutions. Leading manufacturers have begun offering sensor modules that combine Hall elements with signal conditioning circuits in single-package solutions, reducing footprint by up to 30% compared to discrete implementations. These advancements are particularly valuable for smartphone OEMs seeking to maximize internal space utilization while simplifying PCB layouts. The first commercially available system-in-package Hall solutions entered mass production in late 2023.

Expansion into Automotive and IoT Applications

Smartphone sensor manufacturers are leveraging their expertise to address adjacent markets, particularly automotive and IoT segments. Automotive applications—including seat position detection, gear shift sensing, and brushless motor control—represent a growing opportunity with more stringent reliability requirements than consumer electronics. Meanwhile, industrial IoT deployments are adopting Hall sensors for equipment monitoring and predictive maintenance. These diversification strategies help mitigate smartphone market cyclicality while driving technology advancements that eventually benefit mobile applications.

MARKET CHALLENGES

Intense Competition from Alternative Sensing Technologies

Hall sensors face growing competition from optical and capacitive sensing solutions that offer similar functionality without magnetic field requirements. Several smartphone manufacturers have begun experimenting with time-of-flight sensors and micro-mechanical switches that can perform comparable position detection functions. While these alternatives currently cost 20-30% more than Hall sensor implementations, ongoing technology improvements could erode the cost advantage that has driven Hall sensor adoption in mobile devices.

Thermal and EMI Sensitivity Impacts Reliability

Modern smartphone designs generate significant thermal loads and electromagnetic interference that can affect Hall sensor performance. High-performance processors and 5G radios create ambient temperatures exceeding 45°C in some usage scenarios, while RF emissions can induce noise in sensitive analog sensor circuits. These environmental factors require sophisticated shielding and compensation algorithms, adding complexity and cost to system designs. Several flagship smartphones launched in 2023 experienced recalls related to sensor malfunctions under extreme operating conditions.

Standardization Gaps Create Integration Hurdles

The lack of universal interface standards for Hall sensor integration remains a persistent challenge in smartphone development. While I²C has emerged as the dominant digital interface, significant variations exist in command sets, calibration requirements, and power management protocols across vendors. This fragmentation forces OEMs to maintain multiple software stacks and qualification processes, increasing development costs and time-to-market. Industry initiatives to establish common standards have made progress but face resistance from manufacturers with proprietary implementations.

HALL SENSORS FOR SMARTPHONES MARKET TRENDS

Increasing Demand for Advanced Power-Saving Features Drives Market Adoption

The Hall Sensors for Smartphones market is experiencing robust growth, primarily driven by the rising consumer demand for energy-efficient smartphone functionalities. These compact magnetic sensors enable critical power-saving features like automatic screen locking when flipping phone covers closed, which reduces battery drain by up to 15%. Major OEMs are increasingly integrating Hall sensors into mid-range and premium devices as consumer preference shifts toward longer battery life without compromising performance. The global market, valued at over $200 million in 2024, reflects this growing adoption trend, with projections indicating an accelerated CAGR through 2032 as manufacturers prioritize smart power management solutions.

Other Trends

Expansion of Flip-Style Smartphone Designs

The resurgence of flip-style smartphones is creating substantial demand for Hall sensor integration. Leading brands have incorporated these sensors across approximately 85% of their foldable models released since 2022, enabling seamless screen activation upon opening the device. This application not only enhances user experience but also extends component longevity in hinged designs. While traditional candy-bar phones dominated past markets, industry analysts note flip-style devices now account for nearly 18% of premium smartphone shipments, suggesting sustained growth potential for Hall sensor applications in this segment.

Technological Miniaturization Enables Broader Implementation

Continuous advancements in sensor miniaturization are removing previous barriers to Hall sensor adoption. New-generation components measuring under 0.5mm² allow integration into increasingly slim smartphone designs without compromising functionality. Semiconductor manufacturers have achieved this through innovative packaging techniques and materials engineering, resulting in a 40% reduction in sensor footprint compared to 2020 standards. These developments coincide with rising smartphone thickness optimization efforts, making Hall sensors viable even for devices below 7mm profile. As OEMs balance design aesthetics with practical features, Hall sensors emerge as essential components in modern mobile architecture.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Leaders Drive Innovation in Hall Sensor Solutions for Mobile Applications

The global Hall sensors for smartphones market exhibits a moderately consolidated competitive structure, dominated by sensor specialists and diversified electronics conglomerates. According to industry data, the top five players collectively held approximately 50-55% market share by revenue in 2024, reflecting strong brand equity and technological leadership in this niche segment.

The competitive scenario reveals interesting geographic dynamics. While Japanese firms like TDK and Asahi Kasei Microdevices maintain technological leadership in miniaturized sensor designs, U.S.-based Texas Instruments and Honeywell dominate in precision measurement applications. European players such as Melexis have carved out significant market share through specialized automotive-grade sensor solutions now being adapted for mobile applications.

Strategic Directions Among Market Leaders

Several noteworthy trends are reshaping the competitive environment for smartphone Hall sensors:

- TDK Corporation continues to leverage its leadership in TMR (Tunnel Magneto-Resistance) technology to develop ultra-sensitive Hall sensors, particularly for flagship smartphones requiring high-precision magnetic field detection.

- Texas Instruments has been aggressively expanding its digital output Hall sensor portfolio, capitalizing on the growing demand for I2C/SPI interface compatibility in modern smartphone architectures.

- Melexis recently introduced its third-generation Triaxis Hall sensor platform, demonstrating 50% lower power consumption – a critical factor for smartphone OEMs focused on battery life optimization.

Market intelligence suggests that Chinese players like Haechitech are rapidly gaining traction by offering cost-competitive alternatives, particularly for mid-range smartphone models. This local competition is driving price pressure in certain market segments, forcing global players to accelerate their innovation cycles.

List of Leading Hall Sensor Manufacturers for Smartphones

- TDK Corporation (Japan)

- Texas Instruments (U.S.)

- Honeywell International (U.S.)

- Diodes Incorporated (U.S.)

- Melexis NV (Belgium)

- Asahi Kasei Microdevices (Japan)

- OSRAM Group (Germany)

- Alps Alpine (Japan)

- Haechitech (China)

- ROHM Semiconductor (Japan)

- Toshiba Electronic Devices (Japan)

- Seiko Instruments (Japan)

Segment Analysis:

By Type

Analog Output Hall Sensor Segment Dominates Due to High Precision in Smartphone Applications

The market is segmented based on type into:

- Analog Output Hall Sensor

- Digital Output Hall Sensor

By Application

Cellphone Screen Segment Leads with Increased Adoption in Foldable and Flip Smartphones

The market is segmented based on application into:

- Cellphone Screen

- Phone Camera

- Others

By End User

Premium Smartphone Brands Drive Market Demand for Advanced Hall Sensor Integration

The market is segmented based on end user into:

- Flagship Smartphone Manufacturers

- Mid-range Smartphone Manufacturers

- Budget Smartphone Manufacturers

By Technology

3D Hall Sensor Technology Gains Traction for Enhanced Spatial Detection Capabilities

The market is segmented based on technology into:

- 2D Hall Sensors

- 3D Hall Sensors

- Linear Hall Sensors

- Switch-type Hall Sensors

Regional Analysis: Hall Sensors for Smartphones Market

North America

The North American market for Hall sensors in smartphones is driven by high-end device adoption and aggressive R&D investment from key manufacturers. The U.S. dominates regional demand, accounting for over 80% of North American revenues in 2024, with premium smartphone brands increasingly integrating advanced sensor technologies for flip/foldable devices. The region benefits from established semiconductor ecosystems in Silicon Valley and Austin, facilitating rapid innovation cycles. However, market maturity and slower smartphone replacement cycles compared to Asia pose growth challenges. Regulatory emphasis on energy efficiency (particularly in sensor sleep modes) shapes product development priorities among suppliers.

Europe

European adoption focuses on precision and miniaturization, with German sensor manufacturers leading in low-power consumption designs. The EU’s RoHS and REACH regulations compel manufacturers to develop eco-friendly Hall sensor solutions, with particular attention to materials used in magnetic components. While Western Europe maintains steady demand through premium smartphone brands, Eastern Europe shows promise as a manufacturing hub for cost-sensitive sensor variants. The region’s declining smartphone shipment growth (projected at 1.2% CAGR through 2032) suggests manufacturers will prioritize sensor value-addition over volume expansion.

Asia-Pacific

As the production and consumption epicenter, APAC accounts for 68% of global Hall sensor demand, fueled by China’s smartphone manufacturing dominance. Chinese OEMs increasingly specify custom sensor solutions to differentiate mid-range devices, with digital output Hall sensors gaining traction for their compatibility with automated production lines. India emerges as a secondary growth pole, where localization initiatives (PLI scheme) incentivize sensor component manufacturing. Despite volumes, razor-thin margins pressure sensor suppliers, leading to vertical integration strategies among Chinese manufacturers. The region also drives standardization efforts for cross-brand sensor interoperability.

South America

Market growth remains constrained by economic volatility and low smartphone ASPs, though Brazilian manufacturers show increasing adoption of basic Hall sensors for clamshell-style budget devices. The lack of local semiconductor infrastructure forces complete reliance on imports, exposing the region to global supply chain disruptions. Some Brazilian brands experiment with Hall-enabled smart covers as differentiation strategy, but market education gaps persist regarding sensor-added value. Chile and Colombia exhibit stronger potential for sensor adoption per capita, though absolute volumes remain modest compared to global leaders.

Middle East & Africa

The region presents a bifurcated market: Gulf states demonstrate appetite for premium sensor-enabled devices (particularly in flip phone segments), while African markets prioritize cost minimization. Dubai’s status as a regional tech hub facilitates early adoption of sensor innovations, but broader MEA adoption lags 2-3 years behind global trends. South Africa serves as strategic test market for sensor implementations adapted to dusty environments, with modified sealing requirements. While overall penetration remains low, the region’s young demographics and improving connectivity infrastructure suggest long-term growth potential as disposable incomes rise.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Hall Sensors for Smartphones markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Hall Sensors for Smartphones market was valued at USD 253.7 million in 2024 and is projected to reach USD 387.2 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Analog Output Hall Sensor, Digital Output Hall Sensor), application (Cellphone Screen, Phone Camera, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. market estimated at USD 78.4 million and China reaching USD 92.1 million in 2024.

- Competitive Landscape: Profiles of leading market participants including TDK, Texas Instruments, Honeywell, Diodes, and Melexis, covering their product portfolios, market shares, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, miniaturization trends, and integration with smartphone features like flip detection and auto screen locking.

- Market Drivers & Restraints: Evaluation of factors including smartphone adoption rates, demand for power-efficient solutions, and challenges in sensor miniaturization.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, smartphone OEMs, component suppliers, and investors regarding market opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Hall Sensors for Smartphones Market?

-> Hall Sensors for Smartphones Market size was valued at US$ 567 million in 2024 and is projected to reach US$ 1.01 billion by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Which key companies operate in Global Hall Sensors for Smartphones Market?

-> Key players include TDK, Texas Instruments, Honeywell, Diodes, Melexis, Asahi Kasei Microdevices, and Alps Alpine, with the top five players holding approximately 62% market share in 2024.

What are the key growth drivers?

-> Key growth drivers include increasing smartphone adoption, demand for power-efficient solutions, and integration of advanced flip/cover detection features in premium smartphone models.

Which region dominates the market?

-> Asia-Pacific dominates the market with 58% share in 2024, driven by smartphone manufacturing in China and South Korea, while North America shows strong growth potential.

What are the emerging trends?

-> Emerging trends include ultra-miniaturized sensors, higher sensitivity designs, and integration with other smartphone sensors for enhanced user experience.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...