MARKET INSIGHTS

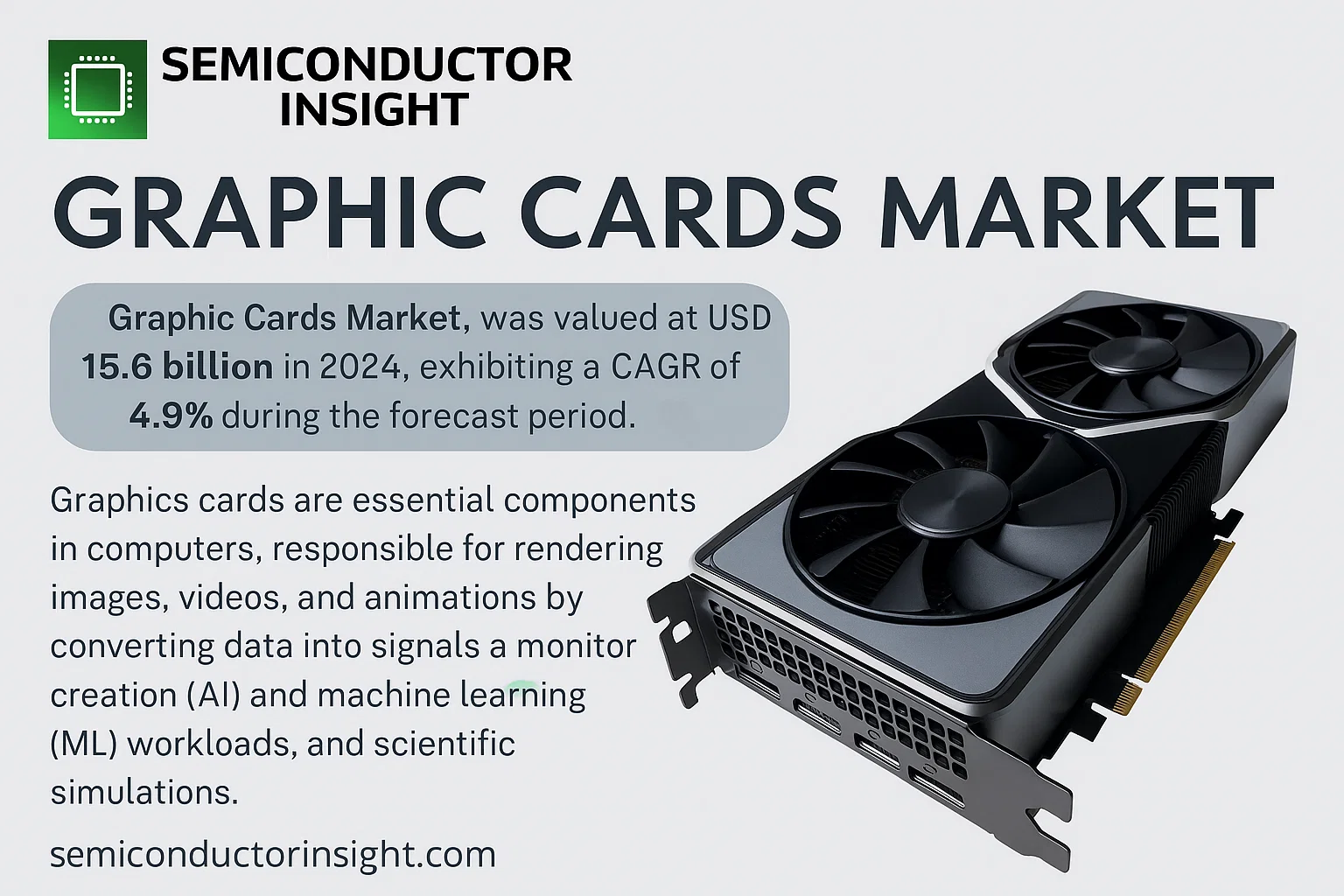

Global Graphic Cards Market, commonly referred to as the graphics card market, was valued at USD 15.6 billion in 2024 to USD 21.6 billion by 2032, exhibiting a CAGR of 4.9% during the forecast period.

Graphics cards are essential components in computers, responsible for rendering images, videos, and animations by converting data into signals a monitor can display. They are crucial for gaming, content creation, artificial intelligence (AI) and machine learning (ML) workloads, and scientific simulations. The market is segmented into integrated graphics, which are built into the computer’s processor, and discrete graphics cards, which are separate units dedicated to handling graphical computations.

The market is experiencing steady growth due to several factors, including the rising popularity of PC gaming, the increasing demand for high-definition (HD) and ultra-high-definition (UHD) content creation and consumption, and the expanding adoption of AI and ML technologies that require significant parallel processing power. The growth of virtual reality (VR) and augmented reality (AR) applications also contributes to the demand. Additionally, the ongoing digital transformation across industries and the increasing use of multi-monitor setups for productivity are driving demand. However, the market faces challenges such as the global semiconductor shortage, which affects production, and the high cost of advanced graphics cards, which can limit adoption in cost-sensitive markets.

Key players in the market include NVIDIA Corporation, Advanced Micro Devices, Inc. (AMD), Intel Corporation, ASUSTeK Computer Inc., and Micro-Star International Co., Ltd. (MSI), among others. These companies are continuously innovating, focusing on improving performance-per-watt, enhancing real-time ray tracing capabilities, and developing AI-driven upscaling technologies like NVIDIA’s DLSS and AMD’s FSR to improve image quality without significantly increasing the hardware cost. The market is also seeing a shift towards more energy-efficient designs to address environmental concerns.

MARKET DRIVERS

Demand Surge from Gaming and Content Creation

The global graphic cards market is experiencing robust growth, primarily fueled by the expanding gaming industry and the rising demand for high-performance computing in content creation. The rapid adoption of 4K and 8K resolution gaming, virtual reality (VR), and augmented reality (AR) applications necessitates powerful GPUs. Furthermore, the burgeoning creator economy, including video editing, 3D rendering, and live streaming, continues to drive upgrades to more advanced graphic cards capable of handling intensive workloads.

Accelerated Adoption in AI and Data Centers

The proliferation of artificial intelligence (AI), machine learning (ML), and high-performance computing (HPC) represents a significant driver. Graphic cards, particularly GPUs, are essential for parallel processing tasks in data centers, powering everything from complex algorithms to scientific simulations. The increasing investment in AI infrastructure by enterprises and cloud service providers is creating sustained demand for data center-grade GPUs.

➤ The global GPU market is projected to grow at a compound annual growth rate of over 33% through 2028, largely driven by these technological advancements.

Finally, the continuous evolution of graphics APIs and software that leverage GPU capabilities for general-purpose computing (GPGPU) ensures that the demand for more powerful and efficient graphic cards remains strong across multiple sectors.

MARKET CHALLENGES

Supply Chain Constraints and Component Shortages

The market faces significant challenges related to global supply chain disruptions and shortages of critical components, such as semiconductors and substrates. These constraints have led to extended lead times, production bottlenecks, and inflated prices, impacting the ability of manufacturers to meet robust consumer and enterprise demand.

Other Challenges

High Product Costs and Market Accessibility

The advanced technology and research & development costs associated with next-generation GPUs result in high retail prices. This creates a barrier to entry for budget-conscious consumers and can slow adoption rates in price-sensitive markets.

Rapid Technological Obsolescence

The fast-paced innovation cycle in the graphic cards industry means products can become obsolete quickly. This pressures consumers to upgrade frequently and creates challenges for manufacturers in managing inventory and product lifecycles effectively.

MARKET RESTRAINTS

Volatility in Cryptocurrency Mining Demand

The graphic cards market has historically been susceptible to boom-and-bust cycles tied to cryptocurrency mining. Sharp declines in cryptocurrency values can lead to a sudden influx of used mining GPUs into the secondary market, destabilizing prices and demand for new products. This volatility makes long-term planning and inventory management difficult for manufacturers and retailers.

Increasing Integration of Integrated Graphics

A key market restraint is the improving performance of integrated graphics solutions in modern CPUs. For mainstream users whose computing needs are satisfied by web browsing, office applications, and light media consumption, the value proposition of a discrete graphic card is diminishing, potentially shrinking the addressable market for entry-level and mid-range GPUs.

MARKET OPPORTUNITIES

Expansion into the Automotive and Industrial Sectors

The advancement of autonomous driving technologies, advanced driver-assistance systems (ADAS), and in-vehicle infotainment systems presents a substantial growth avenue. These applications require powerful GPUs for real-time data processing and high-resolution displays, opening a new and lucrative market for graphic card manufacturers beyond traditional computing.

Growth of Cloud Gaming Services

The rise of cloud gaming (or gaming-as-a-service) platforms is a significant opportunity. These services rely on powerful server-side GPUs to render games remotely, shifting the hardware demand from consumers to data centers. This model promises to make high-end gaming accessible to a broader audience, driving demand for data center GPUs.

Graphic Cards Market Trends

Steady Market Expansion Driven by Gaming and Desktop Demands

The global Graphic Cards market is on a consistent upward trajectory, valued at $15,600 million in 2024 and projected to reach approximately $21,600 million by 2032, representing a compound annual growth rate (CAGR) of 4.9%. The market’s expansion continues to be primarily driven by the sustained demand in the desktop computer segment, which remains the dominant application area. This foundational demand is supplemented by growth in other sectors, including high-performance laptops, which are increasingly incorporating powerful discrete graphics solutions to cater to both gaming and professional creative workloads. The market’s growth is also influenced by technological advancements in GPU architecture and rising consumer expectations for high-resolution and high-refresh-rate visual experiences.

Other Trends

Geographic Production Concentration and Competitive Landscape

The production of graphic cards is heavily concentrated geographically, with the Chinese mainland leading as the dominant production region, accounting for approximately 68% of the global market share. It is followed by Taiwan, China. This concentration underscores the region’s pivotal role in the global supply chain for electronics manufacturing. In terms of competition, the market is characterized by the dominance of a few key players. The top two manufacturers, ASUSTeK Computer and Micro-Star, collectively hold a significant market share of about 30%. Other notable competitors include GIGABYTE Technology, Colorful, GALAX, and SAPPHIRE, among others, creating a competitive environment focused on innovation, price, and brand loyalty.

Market Segmentation and Future Development Potential

Market segmentation highlights distinct opportunities. By product type, the market is divided between built-in independent graphics cards and external graphics solutions. Built-in cards represent the mainstream segment due to their integration into desktop and laptop systems, while the external graphics segment, though smaller, offers a growing niche for enhancing the graphical capabilities of existing hardware. The application-based segmentation reinforces the desktop computer’s position as the largest end-user market, although the laptop segment is anticipated to see accelerated growth due to the increasing popularity of gaming laptops and mobile workstations. Regional analysis indicates that the Asia-Pacific market, led by China, holds the largest share, but North America and Europe remain crucial markets with significant development potential driven by high consumer spending on advanced computing hardware.

COMPETITIVE LANDSCAPE

Key Industry Players

An Industry Dominated by Manufacturing Powerhouses and Branded Partners

The global Graphics Cards market is characterized by a concentration of manufacturing power, with the top two manufacturers, ASUSTeK Computer and Micro-Star, collectively holding approximately 30% of the market share. These companies leverage significant production scale and strong brand recognition to maintain their leading positions. Chinese mainland is the dominant production region globally, accounting for about 68% of market share, followed by Taiwan, China. This geographic concentration underscores the importance of established supply chains and manufacturing capabilities in the industry’s competitive structure. The market primarily serves the desktop computer segment, which drives a substantial portion of demand and shapes product development cycles focused on performance and power for stationary computing. The competitive dynamics are heavily influenced by relationships with key component suppliers, particularly GPU designers like NVIDIA and AMD, whose architecture cycles dictate the pace of innovation and product launches for all downstream card manufacturers.

Beyond the dominant players, a diverse array of other companies hold significant niches. These include major partners like GIGABYTE Technology, Colorful, and SAPPHIRE, which have cultivated strong reputations among enthusiasts and builders. Specialized brands such as EVGA (noted for its customer service and cooling solutions), ZOTAC (focusing on compact form factors), and PNY Technologies (with a strong presence in professional and workstation markets) demonstrate the variety of strategic positions within the industry. Regional players like Maxsun, YESTON, and ONDA also contribute to the competitive mix, particularly within the Asia-Pacific market. Furthermore, companies like GALAX and Gainward add to the competitive intensity with their own unique product lines and marketing approaches. This ecosystem of brands competes on factors including cooling technology, factory overclocking, warranty terms, and aesthetic design to differentiate their offerings in a crowded marketplace.

List of Key Graphic Cards Companies Profiled

- ASUSTeK Computer

- Micro-Star

- GIGABYTE Technology

- Colorful

- GALAX

- SAPPHIRE

- EVGA

- ZOTAC

- Maxsun

- PNY Technologies

- Gainward

- YESTON

- ONDA

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Built-in Independent Graphics Card is the dominant segment, forming the core of the modern computing experience. These dedicated GPUs are essential for delivering the high-performance graphics required for demanding applications like AAA gaming, professional content creation, and complex data visualization. The segment’s leadership is reinforced by its integration into a vast majority of desktop computers and high-performance laptops, making it a standard for users seeking a seamless and powerful visual performance upgrade without the need for additional external hardware. The ongoing innovation in this segment focuses on increasing processing power and energy efficiency, driving continuous market growth as consumer expectations for visual fidelity rise across all digital experiences. |

| By Application |

|

Desktop applications represent the cornerstone of the graphic cards market, demonstrating the highest demand and utilization. The inherent advantages of desktop PCs, such as superior thermal management, greater physical space for larger and more powerful cards, and easier upgrade paths, make them the preferred platform for the most powerful graphics solutions. This segment primarily caters to hardcore gamers, professional designers, engineers, and researchers who require maximum graphical computational power, driving continuous innovation in high-end GPU technology and fostering a vibrant ecosystem of compatible components and peripherals that sustains its market leadership. |

| By End User |

|

Gaming Enthusiasts are the most influential end-user segment, acting as the primary driver for technological advancement and premium product demand. This demographic consistently pushes the boundaries of performance, seeking the latest graphics cards to achieve high frame rates, support virtual reality, and enable cutting-edge visual effects in games. Their demand creates a robust market for high-margin products and fuels a competitive environment among manufacturers to release more powerful generations of GPUs. The segment’s influence extends beyond pure sales, as gaming trends often dictate feature sets and performance targets that eventually trickle down to other user categories, cementing their role as the market’s innovation vanguard. |

| By Performance Tier |

|

Mid-Range / Performance tier graphics cards represent the sweet spot in the market, striking an optimal balance between cost and capability that appeals to the broadest customer base. These cards deliver substantial performance improvements over entry-level options, capable of handling modern games at respectable settings and accelerating creative workflows, without commanding the premium price of high-end enthusiast models. This segment’s popularity is driven by its value proposition, making advanced graphics technology accessible to a wide audience and serving as the default choice for consumers upgrading from integrated graphics or older hardware, thereby representing the volume driver for most manufacturers. |

| By Architecture |

|

Latest Generation architectures are the leading segment, capturing significant market attention and driving the industry’s forward momentum. These newest GPU designs incorporate advanced manufacturing processes, novel features like AI-accelerated upscaling and real-time ray tracing, and substantial improvements in performance-per-watt. The demand for these architectures is fueled by early adopters, competitive gamers, and professionals who require the absolute best performance and feature sets. This segment’s dynamics are characterized by rapid innovation cycles and strong initial sales, setting new industry standards that define competition and influence the entire product stack for years to come. |

Regional Analysis: Graphic Cards Market

Asia-Pacific

The region’s dominance is rooted in its control over semiconductor fabrication and assembly. Major foundries and OEM partners for leading GPU companies are concentrated here, creating an unparalleled supply chain. This proximity to production allows for faster time-to-market for new generations of graphic cards and greater resilience in managing component shortages. The established infrastructure supports massive scale, catering to both local consumption and global exports, making it the core of the worldwide supply network.

A massive and digitally-savvy population drives unprecedented consumer demand. The popularity of esports, PC gaming, and live streaming, particularly in countries like South Korea and China, creates a constant need for high-performance graphics hardware. Furthermore, growing disposable income enables upgrades to premium gaming rigs and workstations for content creation. This vast consumer base is a primary engine for both mid-range and high-end graphic card sales, ensuring sustained market vitality.

Beyond gaming, demand from the enterprise sector is a critical growth pillar. The rapid expansion of data centers across the region, supporting cloud services, artificial intelligence, and machine learning applications, requires immense computational power provided by server-grade graphic cards. Countries like Japan, Singapore, and China are investing heavily in AI infrastructure, creating a robust and high-value market segment that complements consumer demand and drives technological advancement.

The market is characterized by fierce competition among global giants and aggressive local players. This environment fosters rapid innovation cycles and aggressive pricing strategies, benefiting consumers. Local brands often tailor products and marketing to specific regional preferences, challenging the dominance of international companies. This competitive intensity ensures a continuous flow of new features and performance improvements, keeping the Asia-Pacific market at the forefront of graphic card technology trends.

North America

North America remains a critical high-value market for graphic cards, characterized by strong demand for premium and high-performance components. The region has a mature and affluent consumer base with a deep-rooted culture of PC gaming and content creation, leading to early adoption of the latest GPU technologies. High disposable income allows consumers to frequently upgrade to flagship models from leading brands. The enterprise sector is another major driver, with substantial investments in AI research, data analytics, and professional visualization workloads across industries like entertainment (for animation and VFX), engineering, and finance. While manufacturing is limited, the region’s strength lies in its R&D capabilities, being home to the headquarters of major GPU designers, which influences global product roadmaps and innovation directions.

Europe

The European graphic cards market exhibits steady growth, powered by a tech-literate population and a strong gaming community. Demand is robust across Western European nations, with countries like Germany, the UK, and France showing particular strength in both consumer and professional segments. The market is known for its price sensitivity and high expectations for quality and warranty support, influencing vendor strategies. There is significant demand from the professional sector for workstations used in automotive design, architectural visualization, and scientific research. Environmental regulations and energy efficiency standards also play a more prominent role in purchasing decisions compared to other regions, pushing manufacturers to emphasize power-efficient designs in their marketing and product development for the European market.

South America

The graphic cards market in South America is an emerging region with growth potential constrained by economic volatility and import dependencies. Demand is primarily concentrated in major economies like Brazil and Argentina, driven by a growing but price-conscious gaming community. High import taxes and currency fluctuations often lead to significantly higher final prices for consumers, making mid-range and older generation cards more popular than cutting-edge models. The market is highly dependent on distribution channels and parallel imports. Despite these challenges, there is a passionate base of enthusiasts, and increased internet penetration is fueling demand for hardware capable of supporting online gaming and digital content consumption, presenting long-term growth opportunities as economic conditions stabilize.

Middle East & Africa

The Middle East and Africa represent diverse and developing markets for graphic cards. The Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, form the high-value segment with strong demand for luxury gaming setups and hardware for thriving esports scenes, supported by high disposable income. In contrast, the broader African market is largely characterized by demand for entry-level and mid-range cards, with growth driven by increasing PC adoption and mobile gaming. Economic disparities and logistical challenges affect consistent availability and pricing. The professional market is nascent but growing, with potential in sectors like oil and gas simulation and architectural design. Overall, the region presents a patchwork of opportunities, with the Middle East leading in premium adoption and Africa focusing on accessibility.

Report Scope

This market research report provides a comprehensive analysis of the Graphic Cards Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Graphic Cards Market?

->Graphic Cards Market, commonly referred to as the graphics card market, was valued at USD 15.6 billion in 2024 to USD 21.6 billion by 2032, exhibiting a CAGR of 4.9% during the forecast period.

Which key companies operate in Graphic Cards Market?

-> Key players include ASUSTeK Computer, Micro-Star, GIGABYTE Technology, Colorful, GALAX, SAPPHIRE, EVGA, ZOTAC, Maxsun, PNY Technologies, Gainward, YESTON, and ONDA, among others. The top two manufacturers, ASUSTeK Computer and Micro-Star, hold a combined market share of about 30%.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-performance computing, expansion of the gaming industry, increasing adoption in data centers for AI workloads, and the proliferation of advanced graphics applications.

Which region dominates the market?

-> Chinese mainland is the leading production region, accounting for about 68% of the global market share, followed by Taiwan, China.

What are the emerging trends?

-> Emerging trends include integration of AI capabilities, advancements in real-time ray tracing technology, increased focus on energy efficiency, and the expansion of graphic card applications beyond traditional gaming into professional visualization and cloud gaming.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...