Wire and Cables for Semiconductor Equipment Market Overview

Semiconductor manufacturing requires cables and wires that can withstand fast-paced, precise movements without contaminating the chips from component particle emission.

This report provides a deep insight into the global Wire and Cables for Semiconductor Equipment market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Wire and Cables for Semiconductor Equipment Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Wire and Cables for Semiconductor Equipment market in any manner.

Wire and Cables for Semiconductor Equipment Market Analysis:

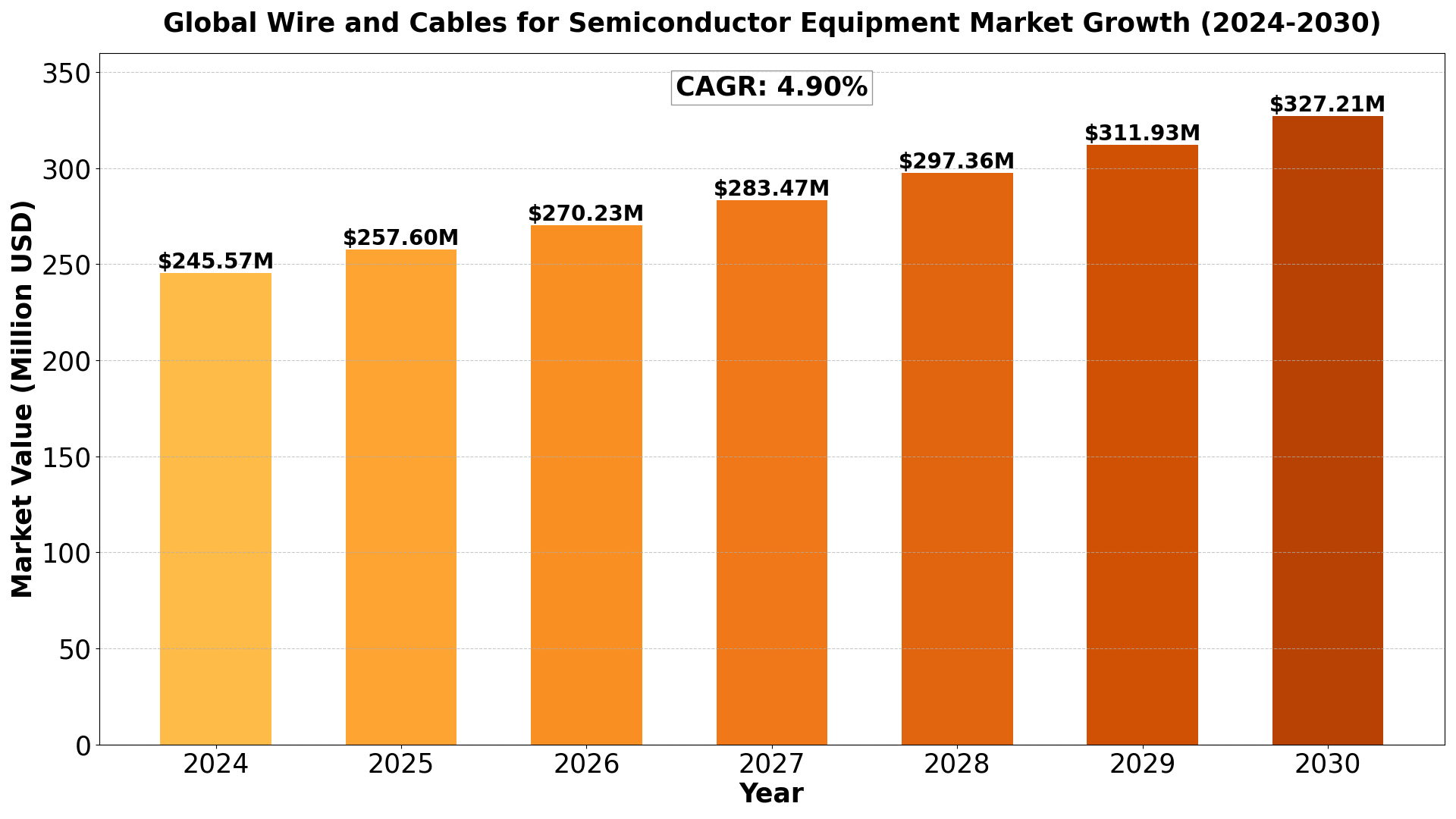

The Global Wire and Cables for Semiconductor Equipment Market size was estimated at USD 234.10 million in 2023 and is projected to reach USD 327.21 million by 2030, exhibiting a CAGR of 4.90% during the forecast period.

North America Wire and Cables for Semiconductor Equipment market size was USD 61.00 million in 2023, at a CAGR of 4.20% during the forecast period of 2024 through 2030.

1. Growing Demand for Semiconductor Manufacturing Equipment

As semiconductor manufacturing processes become more complex and advanced, there is a rising demand for specialized wire and cable solutions to support these systems. The demand for semiconductor equipment, particularly in industries such as electronics, automotive, telecommunications, and consumer goods, is pushing the need for high-performance wires and cables that can withstand high frequencies, high temperatures, and ensure data integrity. The expansion of semiconductor fabs and the adoption of more advanced equipment (e.g., photolithography systems, etching tools) is driving the growth of this market.

2. Miniaturization and Increased Power Efficiency

The trend of miniaturization in semiconductor devices, such as smaller process nodes and integrated circuits, requires wires and cables that are not only compact but also capable of handling higher power densities and smaller geometries. With the trend toward ultra-compact devices, cables and wires must provide better insulation, heat resistance, and noise reduction while maintaining high data transmission speeds. The evolution of semiconductor equipment to handle these smaller and more complex components is creating a need for innovative wire and cable solutions.

3. Rise of Electric Vehicles (EVs) and Automotive Electronics

The automotive sector, particularly with the rise of electric vehicles (EVs), is a significant driver for the wire and cables market for semiconductor equipment. Automotive manufacturers are increasingly adopting advanced semiconductor solutions to power and control electric drivetrains, battery management systems, and autonomous driving features. Semiconductor components used in automotive applications require specialized wiring and cable systems to ensure reliable performance under harsh conditions, contributing to the growth of the market.

4. Increasing Demand for High-Speed Data Transmission

With the ongoing development of high-speed networks (such as 5G), there is a growing need for semiconductor devices capable of handling high-frequency data transmissions. This is driving the demand for wires and cables that can efficiently transmit data without signal loss or interference. As industries adopt high-speed internet, cloud computing, and data center technologies, the need for semiconductor equipment capable of supporting these services is growing, further increasing the demand for advanced wire and cable solutions.

5. Focus on Durability, Safety, and Compliance

Semiconductor manufacturing involves highly sensitive equipment that must operate with extreme precision and reliability. As such, wire and cable solutions must meet strict safety, durability, and compliance standards. The market is seeing increased demand for cables that are resistant to chemical exposure, heat, and wear, while also ensuring low electromagnetic interference (EMI). Manufacturers are investing in wires and cables that adhere to international safety standards and offer longer lifespans to minimize maintenance costs and downtime in semiconductor production facilities.

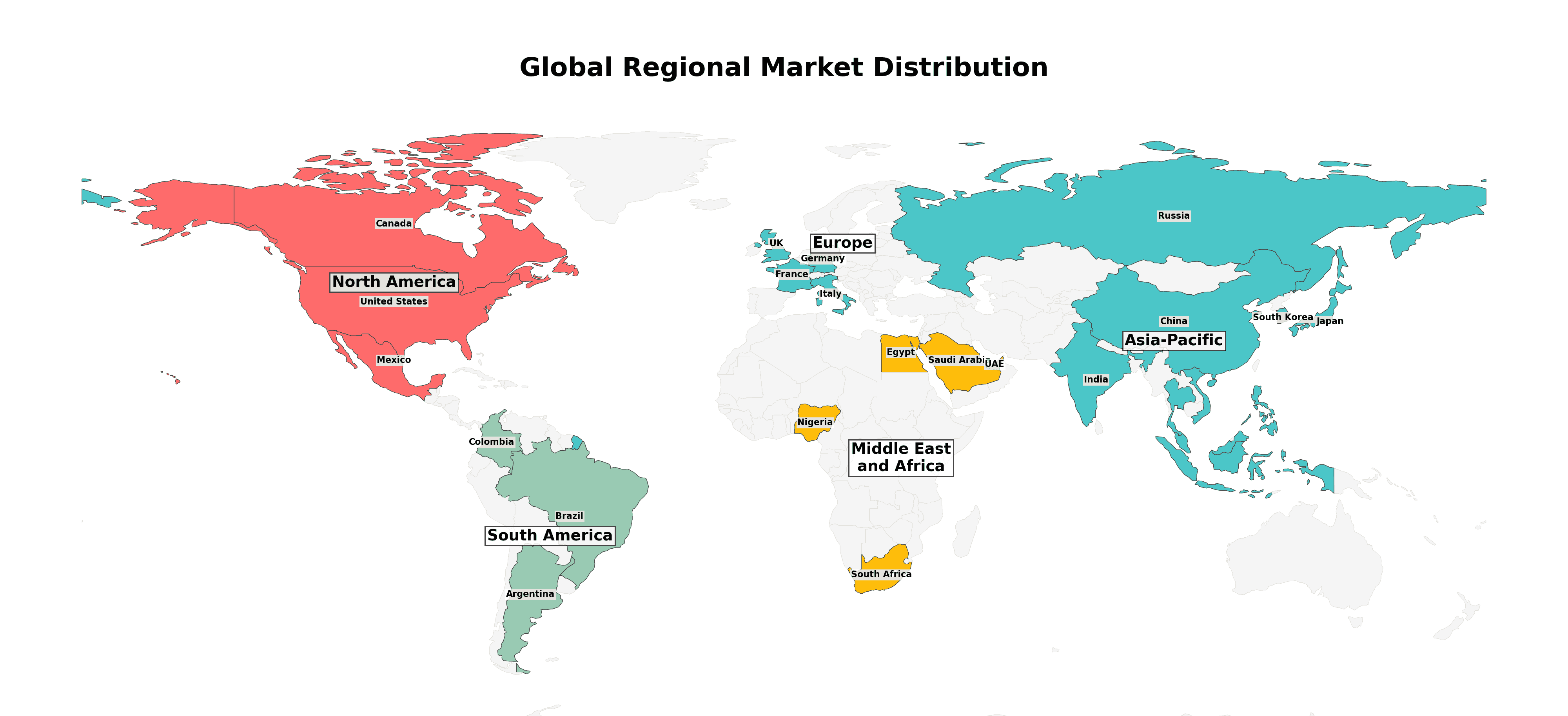

Wire and Cables for Semiconductor Equipment Market Regional Analysis :

1. North America (USA, Canada, Mexico)

- USA: The largest market in the region due to advanced infrastructure, high disposable income, and technological advancements. Key industries include technology, healthcare, and manufacturing.

- Canada: Strong market potential driven by resource exports, a stable economy, and government initiatives supporting innovation.

- Mexico: A growing economy with strengths in automotive manufacturing, agriculture, and tourism, benefitting from trade agreements like the USMCA.

2. Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Germany: The region’s industrial powerhouse with a focus on engineering, automotive, and machinery.

- UK: A hub for financial services, fintech, and pharmaceuticals, though Brexit has altered trade patterns.

- France: Strong in luxury goods, agriculture, and aerospace with significant innovation in renewable energy.

- Russia: Resource-driven economy with strengths in oil, gas, and minerals but geopolitical tensions affect growth.

- Italy: Known for fashion, design, and manufacturing, especially in luxury segments.

- Rest of Europe: Includes smaller yet significant economies like Spain, Netherlands, and Switzerland with strengths in finance, agriculture, and manufacturing.

3. Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- China: The largest market in the region with a focus on technology, manufacturing, and e-commerce. Rapid urbanization and middle-class growth fuel consumption.

- Japan: Technological innovation, particularly in robotics and electronics, drives the economy.

- South Korea: Known for technology, especially in semiconductors and consumer electronics.

- India: Rapidly growing economy with strengths in IT services, agriculture, and pharmaceuticals.

- Southeast Asia: Key markets like Indonesia, Thailand, and Vietnam show growth in manufacturing and tourism.

- Rest of Asia-Pacific: Emerging markets with growing investment in infrastructure and services.

4. South America (Brazil, Argentina, Colombia, Rest of South America)

- Brazil: Largest economy in the region, driven by agriculture, mining, and energy.

- Argentina: Known for agriculture exports and natural resources but faces economic instability.

- Colombia: Growing economy with strengths in oil, coffee, and flowers.

- Rest of South America: Includes Chile and Peru, which have strong mining sectors.

5. The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Saudi Arabia: Oil-driven economy undergoing diversification with Vision 2030 initiatives.

- UAE: Financial hub with strengths in tourism, real estate, and trade.

- Egypt: Growing infrastructure development and tourism.

- Nigeria: Largest economy in Africa with strengths in oil and agriculture.

- South Africa: Industrialized economy with strengths in mining and finance.

- Rest of MEA: Includes smaller yet resource-rich markets like Qatar and Kenya with growing infrastructure investments.

Wire and Cables for Semiconductor Equipment Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- TE Connectivity (TE)

- Alpha Wire

- HELUKABEL

- BizLink

- Winchester Interconnect

- LEONI

- Oki Electric Industry

- MC Electronics

- Cicoil

- Teledyne

- Kowa Denzai Sha LTD

- CHUGOKU ELECTRIC WIRE & CABLE CO.,LTD.

- Prysmian

- Nexans

- LS Cable & System

- TF Kable

- W. L. Gore & Associates

- TOTOKU INC.

- SAB

- Daiichi Denzai (DID)

- NICHIGOH COMMUNICATION ELECTRIC WIRE CO.,LTD.

Market Segmentation (by Type)

- Unshielded

- Foil Shielded

- Braid Shielded

- Foil+ Braid Shielded

Market Segmentation (by Application)

- Front-End Processes

- Back-End Processes

- Fab Support Equipment

Drivers:

- Expansion of Semiconductor Manufacturing Facilities: With the global demand for semiconductor devices rising due to the proliferation of consumer electronics, automotive applications, and industrial systems, there is a growing need for the expansion of semiconductor manufacturing facilities. The construction and upgrading of fabs (semiconductor fabrication plants) and foundries, especially in emerging markets, is a significant driver for the wire and cables market. These facilities require high-quality wiring and cabling solutions for power supply, communication, and control systems in manufacturing equipment.

- Advancements in Semiconductor Manufacturing Technologies: The semiconductor industry is evolving toward smaller, more complex process nodes (e.g., 7nm, 5nm, and 3nm), which require more precise, reliable, and efficient equipment. As semiconductor fabrication becomes increasingly complex, the demand for specialized wire and cable products to handle high frequencies, temperatures, and voltages continues to rise. Additionally, new technologies such as 5G, AI, and quantum computing are driving the need for state-of-the-art semiconductor equipment, further driving the demand for advanced wire and cable solutions.

- Increased Demand for Electric and Autonomous Vehicles: The automotive industry is increasingly adopting semiconductor technology for advanced driver-assistance systems (ADAS), electric vehicle (EV) powertrains, and autonomous driving systems. These applications require highly reliable and durable wire and cable solutions to ensure the seamless operation of semiconductor equipment used in the production of automotive ICs. The growing adoption of electric and autonomous vehicles is a key driver for the wire and cables for semiconductor equipment market.

- Growth in Consumer Electronics and IoT Devices: As consumer electronics, including smartphones, tablets, wearables, and IoT devices, become more widespread, the demand for semiconductor devices also increases. These electronic devices rely on semiconductors to function, driving the need for cutting-edge semiconductor manufacturing equipment. The ongoing expansion of consumer electronics and IoT networks boosts the requirement for reliable wire and cable solutions for semiconductor equipment.

- Rising Demand for High-Speed and High-Performance Electronics: The rapid growth of high-performance computing (HPC), cloud computing, and big data applications requires the continuous miniaturization of semiconductor devices. As semiconductor manufacturers develop increasingly advanced equipment to meet the demands of these applications, specialized wire and cable systems designed to handle the higher power, frequency, and cooling requirements will continue to see increased demand.

Restraints:

- High Manufacturing Costs: The production of high-performance, specialized wires and cables for semiconductor equipment can be costly. Factors such as the use of high-quality materials (e.g., copper, gold, high-temperature insulation), advanced manufacturing techniques, and compliance with stringent industry standards contribute to the high cost of these components. These expenses can lead to higher overall production costs for semiconductor manufacturers, which may restrict the affordability of these products for smaller players in the industry.

- Supply Chain Vulnerabilities: The semiconductor industry is highly dependent on global supply chains for raw materials and components, and disruptions in these supply chains can significantly impact the availability of wires and cables. Factors such as geopolitical tensions, trade restrictions, or natural disasters can disrupt the sourcing of essential materials, leading to delays in production and potential cost increases for wire and cable manufacturers.

- Complexity of Technical Specifications: Semiconductor equipment requires highly specialized wire and cable solutions tailored to the specific needs of the equipment being used. Different types of equipment, such as photolithography tools, etching machines, and testing systems, have distinct electrical, thermal, and mechanical requirements. Developing and producing cables that meet these exacting standards can be complex and time-consuming, limiting the ability of manufacturers to scale production quickly and efficiently.

- Limited Availability of Skilled Labor: The design and manufacturing of specialized wires and cables for semiconductor equipment require a highly skilled workforce with expertise in materials science, electrical engineering, and semiconductor manufacturing processes. A shortage of skilled labor in certain regions can limit the capacity of manufacturers to meet growing demand for advanced wire and cable solutions, slowing market growth.

Opportunities:

- Customization for Specific Semiconductor Equipment: As semiconductor manufacturing equipment becomes more specialized, there is an opportunity to provide customized wire and cable solutions that meet the unique needs of specific applications. For instance, wires and cables used in photolithography machines or cleanroom environments must meet distinct specifications related to electrical conductivity, temperature resistance, and chemical resistance. Manufacturers that can offer tailored solutions for these specific use cases stand to benefit from a growing market.

- Sustainability and Eco-Friendly Materials: With increasing focus on sustainability and environmental regulations, there is an opportunity for manufacturers to develop eco-friendly wire and cable solutions for the semiconductor industry. Using sustainable materials, minimizing waste, and reducing the environmental impact of production processes could provide a competitive advantage in a market where corporate social responsibility is becoming more important to customers.

- Integration of Advanced Insulation and Shielding Technologies: The need for higher performance and more reliable semiconductor equipment creates opportunities for innovation in wire and cable insulation and shielding technologies. The development of advanced insulation materials, such as fluoropolymers and thermoplastic elastomers, can enable cables to operate effectively in higher temperatures and harsh environments. Additionally, improved shielding materials can help reduce electromagnetic interference (EMI) and enhance signal integrity in high-frequency applications.

- Adoption of Advanced Wiring Solutions for 5G and High-Speed Data Transmission: The growing adoption of 5G technology and the increasing demand for high-speed data transmission networks create opportunities for specialized wire and cable solutions. These applications require high-performance cables that can handle the increased data throughput, high frequencies, and power demands. Manufacturers that can provide cutting-edge wiring solutions to support these advancements in communication networks have significant growth potential.

- Expansion in Emerging Markets: The semiconductor industry is expanding in emerging markets such as China, India, and Southeast Asia. These regions are increasingly investing in semiconductor manufacturing infrastructure to meet the growing demand for semiconductors in consumer electronics, automotive, and industrial applications. As these markets develop, there will be increased demand for wire and cable solutions that can support the operation of semiconductor equipment. Companies that can expand their footprint in these regions are well-positioned to benefit from the market growth.

Challenges:

- Technological Advancements Outpacing Production Capabilities: As semiconductor equipment becomes more advanced and demands greater performance, the technology used in wire and cables must also evolve. The constant need for miniaturization, higher power handling, and faster data transmission requires ongoing innovation in wire and cable design. Manufacturers must stay ahead of these technological advancements to meet the evolving needs of semiconductor equipment.

- Intense Competition from Global Players: The wire and cables market for semiconductor equipment is highly competitive, with major players dominating the market. Established companies that have strong supply chains, advanced manufacturing capabilities, and global reach pose significant challenges for new entrants. Competing with these well-established players in terms of quality, pricing, and innovation can be difficult for smaller companies.

- Stringent Industry Standards and Compliance: Wire and cables used in semiconductor equipment must comply with stringent industry standards and regulations, including those related to electrical performance, safety, and environmental impact. Ensuring compliance with these standards requires constant testing, quality control, and certification processes, which can add to the complexity and cost of manufacturing.

- Global Economic Uncertainty: Economic fluctuations, trade tensions, and uncertainties in key markets can impact the semiconductor industry’s growth prospects, which in turn affects the demand for wire and cable solutions. Any downturn in the global economy could reduce investments in semiconductor manufacturing and equipment, which may negatively impact the wire and cables market.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Wire and Cables for Semiconductor Equipment Market

- Overview of the regional outlook of the Wire and Cables for Semiconductor Equipment Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q1. What is the Wire and Cables for Semiconductor Equipment market?

A1. The Wire and Cables for Semiconductor Equipment market involves the production and supply of specialized wires and cables used in semiconductor manufacturing equipment, ensuring efficient electrical connectivity and performance in the semiconductor production process.

Q2. What is the current market size and forecast for the Wire and Cables for Semiconductor Equipment market until 2030?

A2. The market size was estimated at USD 234.10 million in 2023 and is projected to reach USD 327.21 million by 2030, exhibiting a CAGR of 4.90% during the forecast period.

Q3. What are the key growth drivers in the Wire and Cables for Semiconductor Equipment market?

A3. Key growth drivers include the expanding semiconductor industry, the growing demand for advanced semiconductor manufacturing equipment, and the need for high-performance, durable wires and cables that can withstand the complex manufacturing environments.

Q4. Which regions dominate the Wire and Cables for Semiconductor Equipment market?

A4. Asia-Pacific dominates the market, with major contributions from countries like China, South Korea, and Taiwan, which have significant semiconductor manufacturing hubs. North America and Europe also contribute to the market due to the presence of leading semiconductor companies.

Q5. What are the emerging trends in the Wire and Cables for Semiconductor Equipment market?

A5. Emerging trends include the development of cables with higher data transmission rates, the increasing adoption of materials that enhance performance and durability, and the shift toward automation and smart manufacturing techniques in semiconductor production.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...