MARKET INSIGHTS

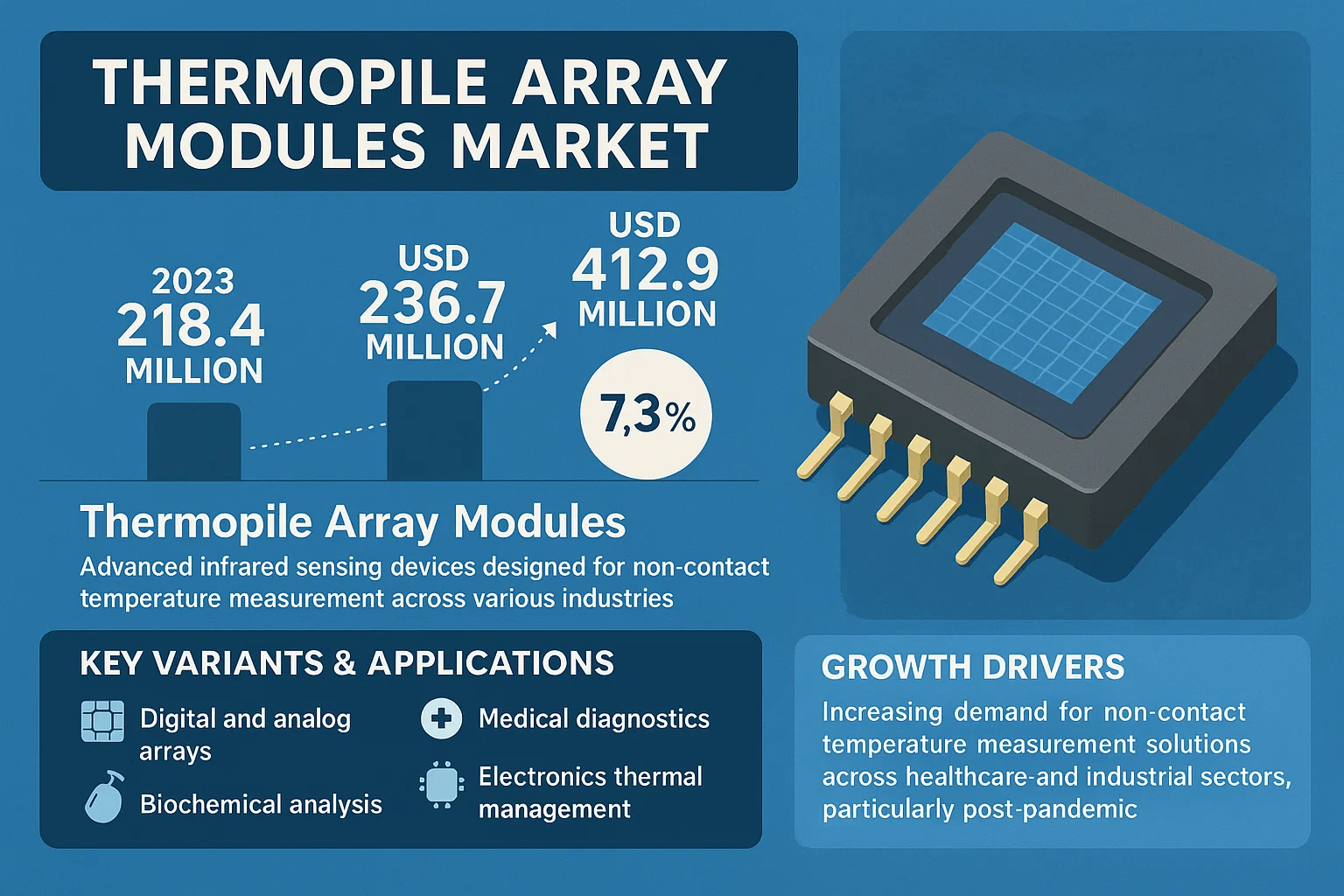

Global Thermopile Array Modules Market size was valued at USD 218.4 million in 2023. The market is projected to grow from USD 236.7 million in 2024 to USD 412.9 million by 2032, exhibiting a CAGR of 7.3% during the forecast period.

Thermopile array modules are advanced infrared sensing devices designed for non-contact temperature measurement across various industries. These modules consist of multiple thermoelectric junctions (thermocouples) arranged in an array pattern, enabling precise thermal imaging and temperature mapping capabilities. Key variants include digital and analog array modules, with applications spanning medical diagnostics, biochemical analysis, food safety monitoring, and electronics thermal management.

Market growth is driven by increasing demand for non-contact temperature measurement solutions across healthcare and industrial sectors, particularly post-pandemic. The medical industry accounted for 32% of market share in 2023 due to rising adoption in fever screening systems. Recent technological advancements in MEMS-based thermopile arrays have enhanced resolution (up to 32×32 pixels) while reducing costs, further accelerating market expansion. FLIR Systems and Hamamatsu Photonics lead the competitive landscape, collectively holding 41% market share as of 2023, with ongoing R&D focused on improving thermal sensitivity below 50mK.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Non-contact Temperature Sensing in Medical Applications to Propel Market Growth

The global thermopile array modules market is experiencing significant growth driven by increasing adoption in medical applications, particularly for fever screening and patient monitoring. The COVID-19 pandemic accelerated the implementation of thermal imaging systems across healthcare facilities, airports, and public spaces, with thermopile arrays being essential components in these systems. The medical sector’s continued emphasis on infection control and non-invasive monitoring is sustaining this demand. Thermopile arrays enable accurate temperature measurement without physical contact, reducing cross-contamination risks while providing reliable data. The global infrared thermography market, which heavily utilizes thermopile arrays, reached approximately $7.2 billion in 2023 and is projected to maintain strong growth through 2030.

Advancements in Industrial Automation and Quality Control to Boost Market Expansion

Industrial automation represents a major growth driver for thermopile array modules, with manufacturers increasingly implementing thermal imaging for quality control, predictive maintenance, and process monitoring. These modules enable real-time temperature profiling of manufacturing processes, helping detect anomalies in electronic components, mechanical systems, and production lines. The growing Industry 4.0 initiative, which emphasizes smart manufacturing and digital transformation, has increased adoption of thermal sensing technologies. Manufacturing facilities worldwide are investing in thermal imaging systems to improve efficiency and reduce downtime, with the industrial segment accounting for over 35% of the total thermopile array market revenue.

Expanding Applications in Consumer Electronics and Automotive Sectors to Drive Adoption

The integration of thermopile array modules in consumer electronics and automotive applications is creating substantial market opportunities. Smart home devices, including smart thermostats, air quality monitors, and home security systems, increasingly incorporate thermal sensing capabilities. The automotive industry is implementing these modules for occupant detection, climate control, and driver monitoring systems. The trend toward autonomous vehicles and enhanced passenger safety features is particularly driving demand, with the automotive thermal imaging market expected to grow at a compound annual growth rate of over 10% through 2028.

MARKET CHALLENGES

High Development and Manufacturing Costs Pose Significant Market Challenges

Despite growing demand, the thermopile array modules market faces substantial challenges related to development and production costs. The manufacturing process requires specialized materials and precise calibration techniques, resulting in higher per-unit costs compared to other sensor technologies. The complex semiconductor fabrication processes and need for temperature stabilization mechanisms add to production expenses. These cost factors become particularly challenging in price-sensitive markets and applications where multiple sensor arrays are required. The average selling price for high-resolution thermopile arrays remains approximately 40-60% higher than alternative temperature sensing technologies, limiting adoption in cost-conscious applications.

Other Challenges

Technical Limitations in Accuracy and Resolution

Thermopile arrays face inherent technical limitations regarding measurement accuracy and spatial resolution. Environmental factors such as humidity, air currents, and ambient temperature variations can affect measurement precision. The typical accuracy range of ±2°C or ±2% of reading presents challenges in applications requiring higher precision. Additionally, the relatively low resolution of most commercial thermopile arrays limits their effectiveness in detailed thermal mapping applications where finer temperature gradients need detection.

Integration Complexities with Existing Systems

Integrating thermopile array modules with existing electronic systems presents implementation challenges. The need for signal conditioning, calibration algorithms, and thermal compensation circuits adds complexity to system design. Many end-users lack the technical expertise to properly integrate these modules, requiring additional engineering resources and increasing total implementation costs. The interface requirements between thermopile arrays and processing units often necessitate custom solutions, further complicating adoption across diverse applications.

MARKET RESTRAINTS

Performance Limitations in Extreme Environmental Conditions to Restrict Market Penetration

Thermopile array modules exhibit performance limitations under extreme environmental conditions, which restricts their application in certain industrial and outdoor settings. Temperature extremes, high humidity environments, and variable atmospheric conditions can significantly impact measurement accuracy and reliability. The modules require stable environmental conditions for optimal performance, with operating temperature ranges typically limited to -40°C to +85°C. Applications in metallurgy, energy production, and outdoor surveillance often encounter conditions beyond these parameters, necessitating additional protective measures that increase system complexity and cost.

Competition from Alternative Sensing Technologies to Limit Market Growth

The market faces restraint from competing infrared sensing technologies and alternative temperature measurement methods. Pyroelectric detectors, microbolometer arrays, and traditional thermocouples offer competitive advantages in specific applications regarding cost, accuracy, or response time. Microbolometers, while generally more expensive, provide better resolution for thermal imaging applications. Traditional contact temperature sensors maintain dominance in applications where physical contact is permissible and highest accuracy is required. This competitive landscape forces thermopile array manufacturers to continually innovate while facing pressure on pricing and performance specifications.

Regulatory and Standardization Challenges to Hinder Market Development

Regulatory requirements and lack of universal standards present significant restraints to market growth. Medical applications particularly face stringent regulatory approvals, with thermopile-based devices requiring certification under various medical device regulations. The absence of unified calibration standards across different manufacturers creates interoperability challenges and increases validation costs for end-users. Compliance with regional electromagnetic compatibility regulations and safety standards adds development time and cost, particularly for international market expansion. These regulatory hurdles disproportionately affect smaller manufacturers and limit innovation pace in the industry.

MARKET OPPORTUNITIES

Emerging Applications in Building Automation and Energy Management to Create Growth Opportunities

The building automation and energy management sector presents substantial growth opportunities for thermopile array modules. Smart building systems increasingly incorporate thermal sensing for occupancy detection, HVAC optimization, and energy efficiency monitoring. The global smart building market is projected to exceed $150 billion by 2026, creating significant demand for advanced sensing technologies. Thermopile arrays enable non-contact people counting, temperature zoning, and equipment monitoring without privacy concerns associated with optical cameras. This application segment is particularly promising due to growing sustainability initiatives and regulatory requirements for energy efficiency in commercial buildings.

Advancements in Miniaturization and Integration to Enable New Application Areas

Technological advancements in miniaturization and integration are creating new market opportunities across various sectors. The development of smaller form-factor thermopile arrays with improved performance characteristics enables integration into portable devices, wearable technology, and IoT applications. Recent innovations in MEMS technology and packaging techniques have reduced module sizes while maintaining thermal performance. The integration of processing capabilities within sensor modules reduces external component requirements and simplifies implementation. These advancements are particularly relevant for consumer electronics and medical wearable applications, where size and power consumption are critical factors.

Growing Research and Development Activities to Unlock Future Potential

Increased research and development activities focused on improving thermopile array performance and reducing costs are creating future growth opportunities. Academic institutions and corporate research centers are investigating new materials, enhanced fabrication techniques, and advanced signal processing algorithms. Developments in graphene-based thermopiles and other novel materials show promise for significantly improved sensitivity and response times. The expanding patent landscape in thermal sensing technologies indicates vigorous innovation activity, with over 200 new patents filed annually related to infrared detection technologies. These R&D efforts are expected to address current limitations and open new application areas in the coming years.

GLOBAL THERMOPILE ARRAY MODULES MARKET TRENDS

Increasing Demand for Non-Contact Temperature Measurement in Industrial Automation

The global thermopile array modules market is experiencing significant growth due to the rising adoption of non-contact temperature measurement solutions in industrial automation. These modules, which convert infrared radiation into electrical signals, are becoming indispensable in applications requiring precise thermal monitoring without physical interaction. Industries such as automotive manufacturing, electronics production, and chemical processing are increasingly implementing thermopile arrays to enhance quality control and process efficiency. Furthermore, the demand for automated inspection systems in smart factories has accelerated the integration of high-resolution thermographic solutions.

Other Trends

Advancements in Medical Thermography

The healthcare sector is rapidly adopting thermopile array modules for applications such as fever screening, dermatological diagnostics, and surgical monitoring. During the COVID-19 pandemic, thermal imaging systems gained prominence for mass fever detection in public spaces, creating sustained demand for accurate and high-speed temperature measurement devices. Recent technological advancements have improved the sensitivity and resolution of medical-grade thermopile arrays, enabling early detection of vascular abnormalities and inflammatory conditions with greater precision.

Emergence of Smart Building and IoT Applications

The expansion of smart building technologies and Internet of Things (IoT) ecosystems is driving new applications for thermopile array modules in occupancy detection, HVAC optimization, and energy management systems. These modules provide cost-effective solutions for monitoring human presence and thermal comfort in commercial and residential spaces without privacy concerns associated with traditional cameras. The growing emphasis on energy efficiency in buildings worldwide has prompted system integrators to incorporate thermal imaging capabilities into environmental control systems for demand-based heating and cooling optimization.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Market Expansion Drive Competition in Thermopile Array Module Sector

The global thermopile array modules market features a dynamic competitive landscape with established players and emerging companies vying for market share. Industry leaders are focusing on technological advancements and geographical expansion to maintain their positions. The market is experiencing steady growth, with increased adoption across medical, industrial, and consumer electronics applications creating new opportunities for both large corporations and specialized manufacturers.

FLIR Systems (now part of Teledyne Technologies) remains a dominant force in the market, leveraging its extensive experience in infrared technology and thermal imaging solutions. The company’s acquisition by Teledyne in 2021 strengthened its position in the defense and industrial sectors, while continued R&D investments have enhanced its thermopile array offerings for commercial applications.

Meanwhile, Hamamatsu Photonics has significantly increased its market presence through innovative product development, particularly in the medical and scientific instrumentation segments. The company’s recent advancements in MEMS-based thermopile arrays have positioned it as a key technology provider for non-contact temperature measurement solutions.

Melexis has emerged as a strong competitor in the automotive and consumer electronics segments, with its compact thermopile array modules gaining traction in applications such as smart home devices and vehicle cabin monitoring systems. The company’s focus on integration and miniaturization has given it a competitive edge in these growth markets.

Geographical expansion remains a key strategy, with companies like TE Connectivity and Amphenol Corporation strengthening their distribution networks in Asia-Pacific markets, where demand for thermal sensors is growing rapidly across multiple industries. These firms are also investing in strategic partnerships to enhance their product portfolios and application expertise.

List of Key Thermopile Array Module Companies Profiled

- FLIR Systems (U.S.) – Now part of Teledyne Technologies

- Heimann Sensor GmbH (Germany)

- Excelitas Technologies Corp. (U.S.)

- Hamamatsu Photonics (Japan)

- Melexis (Belgium)

- TE Connectivity (Switzerland)

- Amphenol Corporation (U.S.)

- PerkinElmer (U.S.)

- Pacer International (U.S.)

- Boston Electronics (U.S.)

While competition intensifies, companies are differentiating through factors such as measurement accuracy, response time, and integration capabilities. The trend toward miniaturization and smart sensor solutions continues to reshape product development strategies across the industry. Smaller, specialized firms are finding success by targeting niche applications where their technical expertise provides competitive advantages, while larger corporations leverage their scale to address broad market needs.

Segment Analysis:

By Type

Digital Array Modules Dominate Due to Enhanced Precision and Integration Capabilities

The market is segmented based on type into:

- Digital Array Modules

- Subtypes: Low resolution, medium resolution, high resolution

- Analog Array Modules

- Hybrid Array Modules

- Subtypes: Custom configurations for specialized applications

By Application

Medical Industry Segment Leads Market Adoption for Non-contact Temperature Measurement

The market is segmented based on application into:

- Medical Industry

- Sub-applications: Fever detection, thermal imaging for diagnostics

- Biochemistry

- Food Industry

- Electronic Products

- Other Industrial Applications

By Resolution

High-Resolution Arrays Gain Traction in Research and Precision Applications

The market is segmented based on resolution into:

- Low Resolution Arrays (≤32×32 pixels)

- Medium Resolution Arrays (64×64 to 128×128 pixels)

- High Resolution Arrays (≥256×256 pixels)

By Detection Range

Medium Range Modules Most Widely Used Across Industries

The market is segmented based on detection range into:

- Short Range (0-5 meters)

- Medium Range (5-20 meters)

- Long Range (>20 meters)

Regional Analysis: Global Thermopile Array Modules Market

Asia-Pacific

Asia-Pacific dominates the global thermopile array modules market, accounting for over 45% of global revenue in 2023. This leadership stems from concentrated manufacturing hubs in China, Japan, and South Korea, where companies like Hamamatsu Photonics and Excelitas Technologies maintain strong production capabilities. The region benefits from high adoption in electronics manufacturing (for thermal imaging in smartphones and IoT devices) and expanding medical diagnostics applications. Governments in China and India are investing in healthcare infrastructure upgrades, pushing demand for non-contact temperature measurement devices. Though cost-sensitive markets still favor analog modules, digital variants are gaining traction in premium medical and industrial applications due to their superior accuracy.

North America

North America follows closely with approximately 30% market share, driven by technological advancements and stringent regulatory standards for medical and food safety applications. The U.S. FDA’s Class II medical device classification for infrared thermometers bolsters demand for high-precision thermopile arrays. Key players like FLIR Systems and TE Connectivity focus on defense and aerospace applications, where these modules are critical for thermal sensing in harsh environments. Recent R&D investments in AI-integrated thermal imaging (notably in autonomous vehicles and smart buildings) position the region as an innovation hub. However, supply chain dependencies on Asian manufacturers create pricing volatility concerns for end-users.

Europe

Europe’s market growth is anchored by Germany’s robust industrial sector and the EU’s emphasis on energy-efficient building management systems. Companies such as Heimann Sensor GmbH and Melexis lead in automotive-grade modules, catering to EV battery monitoring and cabin occupancy detection needs. The region shows increasing preference for digital array modules in food processing plants to comply with EU Regulation (EC) No 852/2004 on hygiene standards. Environmental directives like RoHS also drive adoption of lead-free thermopile components. Market expansion is tempered by slow replacement cycles in established manufacturing industries, though smart city initiatives offer new opportunities.

South America

South America represents an emerging market where growth is concentrated in Brazil’s medical equipment sector and Chile’s mining industry (for equipment overheating detection). Analog modules remain preferred due to budget constraints, with imports constituting 80% of regional supply. Local production is limited to assembly operations by multinationals like Amphenol Corporation. Economic instability and currency fluctuations hinder large-scale deployments, but the post-pandemic focus on public health infrastructure has accelerated hospital-grade thermometer procurement. The lack of standardized testing facilities for module calibration remains a key challenge for quality-conscious buyers.

Middle East & Africa

This region shows niche growth potential in oil & gas pipeline monitoring and luxury automotive markets. The UAE leads in smart building integrations, while South Africa’s mining sector utilizes thermopile arrays for equipment safety. Most modules are imported from Europe and Asia, with distribution channels dominated by Farnell and regional electronics suppliers. Hampered by low local technical expertise, the market relies heavily on foreign vendors for after-sales support. However, increasing FDI in Saudi Arabia’s NEOM smart city project and Egypt’s healthcare modernization indicate future demand spikes for advanced thermal sensing solutions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Thermopile Array Modules markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermopile Array Modules Market?

->Thermopile Array Modules Market size was valued at USD 218.4 million in 2023. The market is projected to grow from USD 236.7 million in 2024 to USD 412.9 million by 2032, exhibiting a CAGR of 7.3% during the forecast period.

Which key companies operate in Global Thermopile Array Modules Market?

-> Key players include Excelitas, Hamamatsu Photonics, FLIR Systems, Melexis, TE Connectivity, Amphenol Corporation, Heimann Sensor GmbH, and PerkinElmer, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for non-contact temperature measurement in medical devices, industrial automation, and consumer electronics, along with advancements in infrared sensing technology.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market due to strong technological adoption and manufacturing presence.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with AI for predictive maintenance, and growing adoption in automotive and smart building applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...