MARKET INSIGHTS

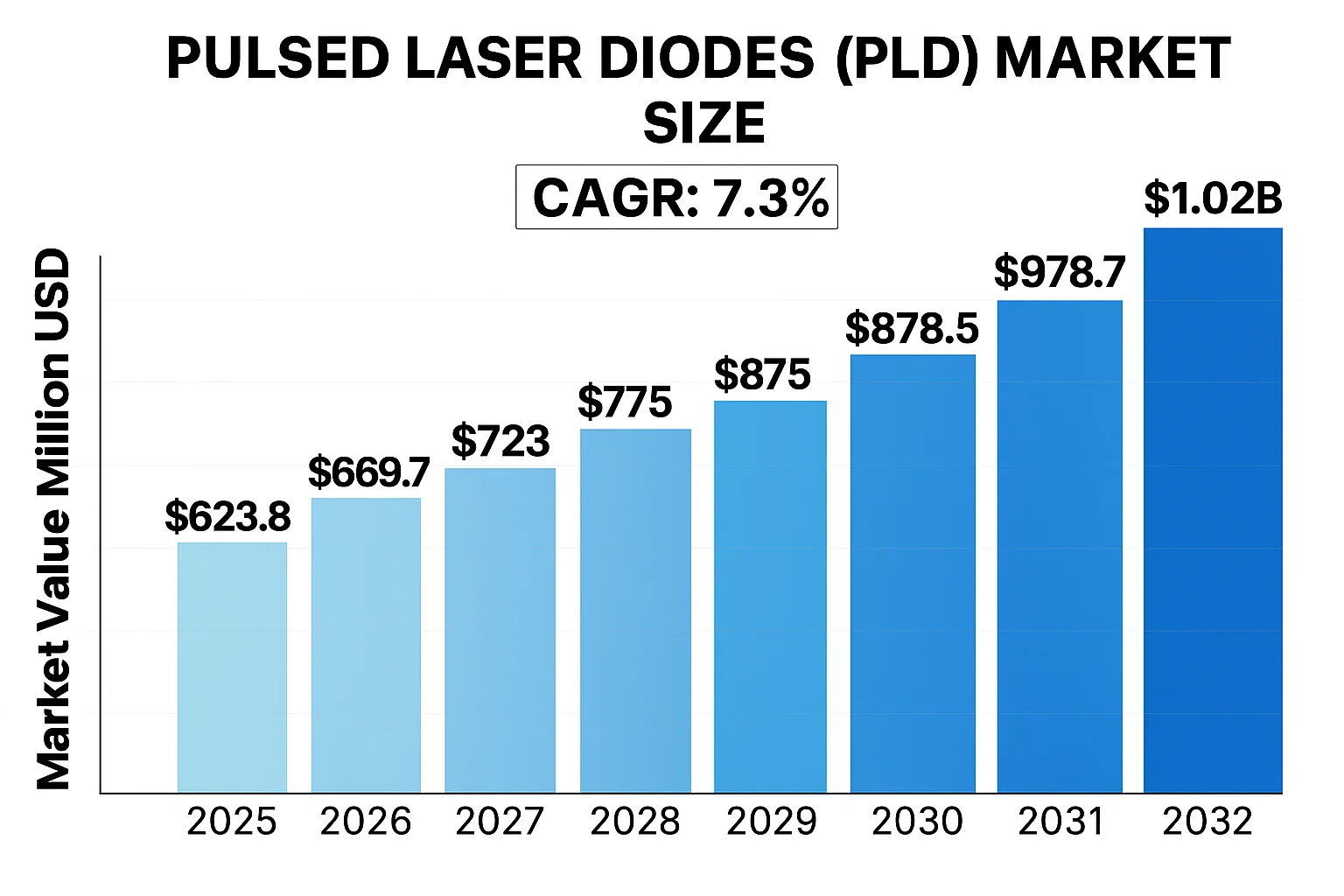

The Global Pulsed Laser Diodes (PLD) Market size was valued at US$ 623.8 million in 2024 and is projected to reach US$ 1.02 billion by 2032, at a CAGR of 7.3% during the forecast period 2025-2032.

Pulsed Laser Diodes are semiconductor devices that emit high-intensity light pulses in short bursts, typically in nanoseconds or picoseconds. These devices operate by injecting electrical current to generate optical pulses, making them crucial for applications requiring precise timing and high peak power. Key variants include 905 nm, 850 nm, and 1550 nm wavelength types, each optimized for specific use cases like LiDAR, range finding, and medical diagnostics.

The market growth is driven by increasing adoption in autonomous vehicles, industrial automation, and defense applications. The rising demand for LiDAR systems in automotive safety and smart city infrastructure is particularly noteworthy, with automotive LiDAR applications expected to account for over 35% of PLD demand by 2027. Technological advancements in pulse duration control and thermal management are further expanding application possibilities. Major players like Hamamatsu Photonics and Coherent are investing heavily in R&D to develop energy-efficient PLDs with higher repetition rates.

MARKET DRIVERS

Rising Adoption in Automotive LiDAR Applications to Accelerate Market Growth

The global pulsed laser diode market is experiencing substantial growth driven by increasing demand from automotive LiDAR systems. With autonomous vehicle development programs accelerating globally, manufacturers are integrating high-performance PLDs for precise object detection and ranging. The automotive LiDAR market is projected to expand significantly, reflecting the critical role of PLDs in this emerging technology. These components enable accurate distance measurements crucial for collision avoidance systems, with wavelengths of 905nm and 1550nm becoming industry standards. Recent advancements in semiconductor fabrication have improved PLD efficiency, making them more viable for mass-market automotive applications.

Growing Defense and Aerospace Investments Fuel PLD Demand

Defense modernization programs worldwide are creating robust demand for pulse laser diodes in applications including target designation, rangefinding, and secure communications. Military expenditure growth has been particularly strong in emerging economies, with many nations prioritizing electro-optical systems that incorporate PLD technology. These components offer advantages such as compact size, high reliability, and precise pulse control – critical attributes for defense applications. The development of next-generation counter-drone systems and directed energy weapons is further propelling market expansion, as PLDs serve as essential components in these advanced platforms.

➤ Specialized PLDs with pulse widths in nanosecond range and high peak power capabilities are becoming particularly valuable for defense applications where accuracy and control are paramount.

Furthermore, commercial space sector growth is opening new opportunities for PLD applications in satellite communications and space-based sensing systems. The proliferation of small satellite constellations is creating additional demand for reliable, space-qualified laser diode solutions.

MARKET CHALLENGES

Thermal Management Issues Pose Technical Hurdles

While PLD technology continues to advance, thermal management remains a significant challenge affecting performance and reliability. Pulsed operation generates concentrated heat at the semiconductor junction, which can degrade device performance and lifespan. This is particularly problematic in high-power applications where maintaining optimal operating temperature becomes crucial. Industry data shows that thermal issues account for a significant portion of PLD failures in field applications, raising concerns about long-term reliability.

Other Challenges

Supply Chain Vulnerabilities

The global semiconductor shortage has impacted PLD manufacturing, with lead times for specialized components extending significantly. This supply chain pressure is particularly acute for products requiring custom wavelengths or packaging, creating bottlenecks for system integrators.

Performance Standardization

Absence of unified performance metrics across different PLD manufacturers makes system integration more complex. Variations in pulse characteristics, divergence angles, and spectral properties require additional engineering effort to compensate for these differences.

MARKET RESTRAINTS

Regulatory Constraints Limit Market Expansion in Some Regions

Stringent laser safety regulations in certain markets are creating barriers to PLD adoption. Eye safety concerns have led to power limitations and additional compliance requirements that increase product development costs. These regulatory hurdles are most pronounced in consumer-facing applications and vary significantly between regions, complicating global product strategies. Some jurisdictions have implemented classification systems that restrict certain PLD products without specialized certifications, limiting market accessibility.

Additionally, export controls on high-performance laser technologies affect international trade in PLDs, particularly those with potential dual-use applications. These constraints disproportionately impact manufacturers seeking to serve global defense and aerospace markets.

MARKET OPPORTUNITIES

Emerging Medical Applications Present Growth Potential

The healthcare sector represents a promising growth avenue for PLD technology, particularly in minimally invasive surgical procedures and diagnostic imaging. Laser-based medical systems increasingly utilize pulsed diodes for precision tissue interaction with minimal thermal damage. Ophthalmology applications including retinal photocoagulation are adopting advanced PLD solutions that offer improved patient outcomes. The medical laser market growth is creating demand for compact, reliable PLD sources that meet strict regulatory requirements.

Furthermore, developments in biomedical sensing technologies are incorporating PLDs for applications such as flow cytometry and optical coherence tomography. These emerging uses are expected to expand significantly as healthcare providers seek more precise diagnostic tools.

PULSED LASER DIODES (PLD) MARKET TRENDS

Growing Demand for LiDAR Applications Fuels PLD Market Expansion

The global Pulsed Laser Diodes (PLD) market is experiencing significant growth, primarily driven by increasing adoption in LiDAR (Light Detection and Ranging) applications. With the autonomous vehicle industry projected to reach a valuation of over $500 billion by 2030, the demand for high-performance PLDs capable of precise distance measurement is rising sharply. These components enable critical functions such as object detection, navigation, and collision avoidance systems. Furthermore, advancements in semiconductor manufacturing have enhanced the power efficiency and reliability of PLDs, making them indispensable for next-generation automotive safety solutions. The integration of 905 nm and 1550 nm wavelength PLDs in commercial and industrial LiDAR systems is particularly noteworthy, offering superior performance in varying environmental conditions.

Other Trends

Expansion in Telecommunications and Optical Sensing

Beyond LiDAR, PLDs are gaining traction in telecommunications and optical sensing applications due to their ability to deliver high-speed pulsed signals. The increasing deployment of 5G networks worldwide has created demand for efficient optical components capable of supporting faster data transmission rates. PLDs operating at 850 nm and 1550 nm wavelengths are widely used in fiber-optic communication systems, contributing to improved signal integrity and long-distance transmission capabilities. Additionally, in medical diagnostics and industrial sensing, PLDs enable precise measurements in spectroscopy and imaging systems. The global optical communication market’s projected compound annual growth rate (CAGR) of 7-9% over the next five years further underscores these opportunities.

Advancements in Semiconductor Technology Drive Innovation

Continuous improvements in semiconductor fabrication techniques are revolutionizing the PLD market. The shift toward quantum well structures and edge-emitting laser diodes has significantly enhanced power output and thermal stability, extending the operational lifespan of PLDs in demanding environments. Companies like Hamamatsu Photonics and Coherent are investing heavily in research and development to optimize pulse repetition rates and beam quality. Emerging applications in defense and aerospace, such as target designation and free-space optical communication, are also benefiting from these innovations. While the Asia-Pacific region leads in manufacturing capabilities due to established semiconductor supply chains, North American and European markets remain key hubs for high-end R&D activities.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Expansion

The global Pulsed Laser Diodes (PLD) market features a moderately consolidated competitive landscape, dominated by established optical technology providers alongside emerging specialists. Hamamatsu Photonics leads the market with a 19.2% revenue share in 2024, attributable to its vertically integrated manufacturing capabilities and broad wavelength portfolio ranging from 650nm to 1550nm.

Coherent and OSI Laser Diode collectively account for approximately 26% of the market, with their strong foothold in defense and LiDAR applications. Both companies have demonstrated consistent year-over-year growth above 7.8% CAGR, outperforming industry averages through strategic acquisitions and custom solution development.

The market has witnessed significant R&D investment in gallium arsenide (GaAs) and indium gallium arsenide (InGaAs) technologies, with Excelitas recently launching their new high-power 905nm pulse laser diode series for automotive LiDAR applications. Meanwhile, NKT Photonics has strengthened its position through licensing agreements with multiple European research institutions.

Regional manufacturers like Roithner Lasertechnik are gaining traction in niche medical and scientific applications, leveraging specialized engineering capabilities that complement rather than compete with global players. This creates a dynamic competitive environment where collaboration and specialization coexist.

List of Leading Pulsed Laser Diode Manufacturers

- Hamamatsu Photonics K.K. (Japan)

- Coherent, Inc. (U.S.)

- OSI Laser Diode, Inc. (U.S.)

- Laser Components GmbH (Germany)

- Excelitas Technologies Corp. (U.S.)

- NKT Photonics A/S (Denmark)

- Analog Modules, Inc. (U.S.)

- Edinburgh Instruments Ltd (UK)

- Roithner Lasertechnik GmbH (Austria)

- Genuine Optronics Limited (China)

Segment Analysis:

By Type

905 nm Pulsed Laser Diodes Lead the Market Owing to High Demand in LiDAR and Range-Finding Applications

The market is segmented based on type into:

- 905 nm Type

- 850 nm Type

- 1550 nm Type

- Other Wavelengths

By Application

LiDAR Segment Dominates with Increasing Adoption in Autonomous Vehicles and Industrial Automation

The market is segmented based on application into:

- Range Finding

- LiDAR

- Medical Applications

- Industrial Processing

- Others

By Power Output

Medium Power (10-50W) Segment Leads Due to Balanced Performance in Industrial and Consumer Applications

The market is segmented based on power output into:

- Low Power (Below 10W)

- Medium Power (10-50W)

- High Power (Above 50W)

By End-Use Industry

Automotive Sector Shows Strong Growth Potential Driven by ADAS and Autonomous Vehicle Development

The market is segmented based on end-use industry into:

- Automotive

- Industrial Manufacturing

- Healthcare

- Aerospace & Defense

- Consumer Electronics

Regional Analysis: Global Pulsed Laser Diodes (PLD) Market

North America

The North American pulsed laser diode market is driven by strong demand from defense, automotive LiDAR, and medical applications. The U.S. holds the largest share, with significant investments in autonomous vehicle development and military-grade sensing technologies. Companies like Coherent and Excelitas have a strong regional presence, benefiting from R&D initiatives in quantum computing and aerospace applications. However, strict export controls on laser technologies and high manufacturing costs present challenges for market expansion. The region benefits from robust IP protection laws that encourage innovation in semiconductor lasers.

Europe

Europe maintains a technologically advanced PLD market focused on precision manufacturing and scientific research applications. Germany leads in industrial laser adoption, while the UK shows growing demand for environmental sensing lasers. The market is constrained by complex CE marking requirements for laser products and competition from Asian manufacturers. However, EU-funded photonics projects like Horizon Europe stimulate innovation. A notable trend is increasing adoption of 1550 nm PLDs for eye-safe LiDAR in automotive safety systems. Environmental regulations favor manufacturers developing energy-efficient pulsed laser solutions.

Asia-Pacific

As the fastest-growing PLD market, Asia-Pacific benefits from massive electronics manufacturing ecosystems in China, Japan, and South Korea. China dominates production capacity with government-supported photonics industrial parks. The region sees surging demand for 905 nm diodes in consumer electronics and industrial automation. While price competition is intense, Japanese manufacturers like Hamamatsu Photonics maintain technology leadership in high-power PLDs. Emerging applications in facial recognition and gesture control systems drive growth, although trade tensions occasionally disrupt supply chains for critical semiconductor materials.

South America

The South American PLD market remains niche but shows potential in mining automation and agricultural sensing applications. Brazil accounts for over 60% of regional demand, primarily for industrial marking systems. Market growth is hindered by economic instability and reliance on imports for advanced laser components. However, increasing emphasis on precision farming creates opportunities for ruggedized PLD solutions. Trade agreements with Asian manufacturers help improve technology access, though local technical support infrastructure remains underdeveloped compared to other regions.

Middle East & Africa

This emerging market shows particular strength in oil/gas pipeline monitoring and security applications. The UAE and Saudi Arabia lead in adopting PLD-based perimeter security systems. While the market size is relatively small, government initiatives to build technology hubs are attracting global PLD manufacturers. Challenges include harsh environmental conditions requiring specialized laser packaging and lack of local maintenance expertise. The region presents long-term potential as smart city projects incorporate LiDAR for urban planning and autonomous transportation infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Pulsed Laser Diodes (PLD) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global PLD market was valued at USD 1.2 billion in 2024 and is projected to reach USD 2.3 billion by 2032 at a CAGR of 8.5%.

- Segmentation Analysis: Detailed breakdown by product type (905 nm, 850 nm, 1550 nm), application (LiDAR, range finding), and end-user industries to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis of key markets like the U.S., China, Germany, and Japan.

- Competitive Landscape: Profiles of leading market participants including Hamamatsu Photonics, Coherent, and NKT Photonics, covering their product portfolios, R&D investments, manufacturing capabilities, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging PLD technologies, integration with autonomous systems, advancements in semiconductor materials, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of growth drivers including rising demand for LiDAR in autonomous vehicles and challenges such as supply chain disruptions in semiconductor components.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory filings, trade associations, and proprietary databases to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Pulsed Laser Diodes (PLD) Market?

-> The global Pulsed Laser Diodes (PLD) market size was valued at US$ 623.8 million in 2024 and is projected to reach US$ 1.02 billion by 2032, at a CAGR of 7.3% during the forecast period 2025-2032.

Which key companies operate in Global Pulsed Laser Diodes Market?

-> Key players include Hamamatsu Photonics, Coherent, NKT Photonics, Excelitas, and Laser Components, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption in autonomous vehicles, defense applications, and increasing demand for 3D sensing technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to automotive electronics expansion, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include miniaturization of PLDs, development of high-power diodes, and integration with AI-based systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...