MARKET INSIGHTS

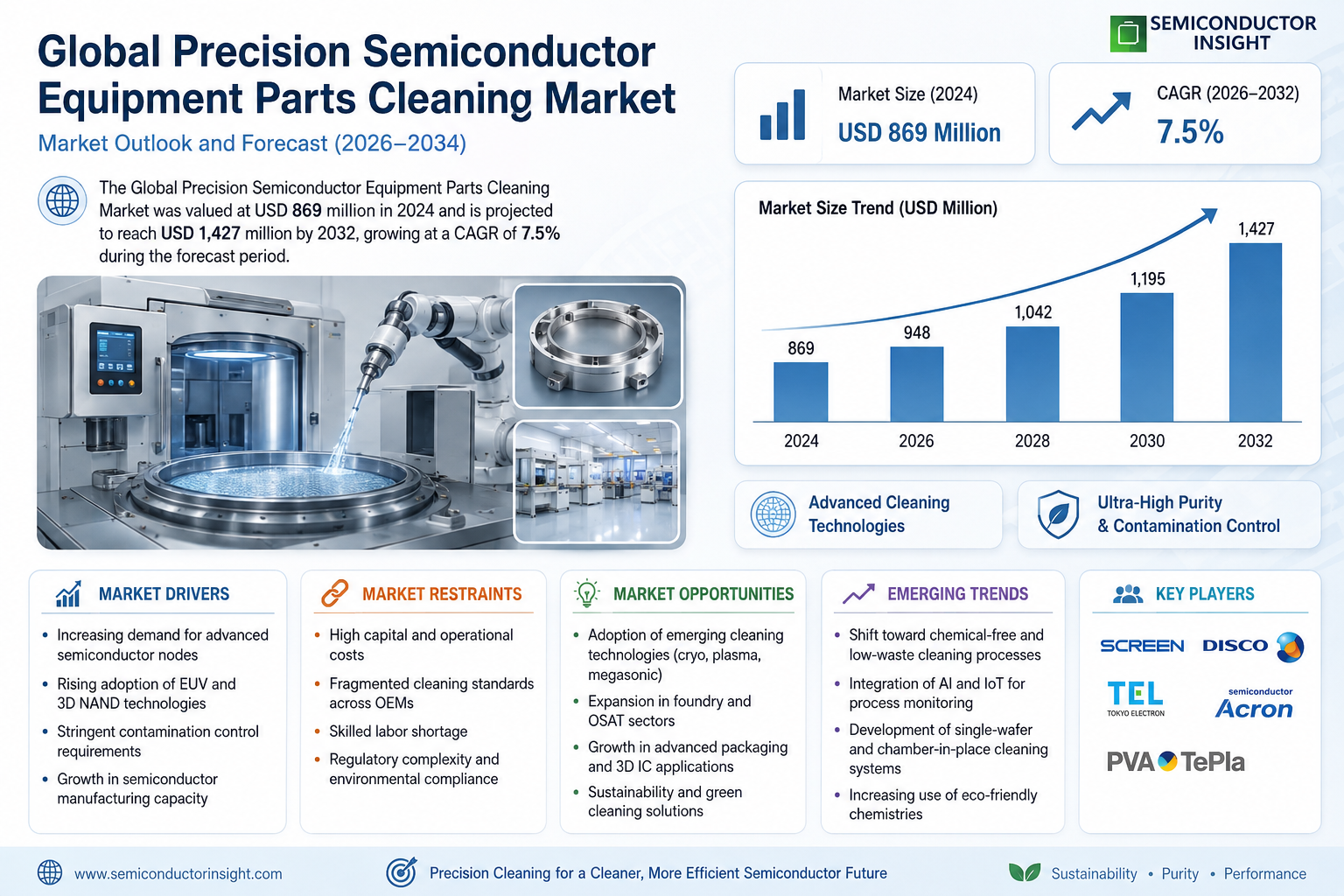

The global Precision Semiconductor Equipment Parts Cleaning Market was valued at 869 million in 2024 and is projected to reach US$ 1427 million by 2032, at a CAGR of 7.5% during the forecast period.

Precision Semiconductor Equipment Parts Cleaning involves specialized processes to remove contaminants from semiconductor manufacturing components, ensuring optimal performance and yield. These processes target particle levels, atomic-level contamination, and chemical residues on critical parts such as chamber components, wafer handling systems, and deposition equipment. The demand for ultra-clean parts has intensified as semiconductor nodes shrink below 5nm, where even nanometer-scale impurities can impact device performance.

Growth is driven by increasing semiconductor fabrication complexity, rising adoption of advanced packaging technologies, and stringent cleanliness requirements in EUV lithography. Taiwan dominates demand, with TSMC alone accounting for over 60% of the regional market. The top six players in Taiwan held an 82% revenue share in 2023, reflecting high market consolidation. While wet chemical cleaning remains prevalent, emerging technologies like supercritical CO2 cleaning are gaining traction for their environmental benefits and superior particle removal capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Semiconductor Nodes to Fuel Market Growth

The global semiconductor industry is transitioning toward advanced process nodes, with leading foundries like TSMC already mass-producing 3nm chips and targeting 2nm production by 2025. This technological evolution demands exponentially cleaner chamber surfaces, as even nanoscale contaminants can significantly impact chip yields. The precision cleaning market directly benefits from this trend, with advanced node fabrication requiring up to 30% more frequent chamber cleaning compared to legacy nodes. As semiconductor manufacturers invest over $500 billion in new fabrication facilities globally through 2030, the need for precision cleaning services is growing in lockstep.

Stringent Yield Requirements in Semiconductor Manufacturing Accelerate Adoption

With semiconductor device geometries shrinking below 7nm, particulate contamination has become one of the top three yield-limiting factors in chip production. Modern fabs cannot tolerate more than 0.01 particles/cm² larger than 20nm, creating unprecedented demand for precision cleaning solutions. The economic impact is substantial – a single wafer scrap at advanced nodes can represent a $10,000 loss. This has led semiconductor manufacturers to double their cleaning budgets over the past five years, with particular emphasis on atomic-level contamination removal.

➤ Leading foundries now require parts cleaning to achieve surface metal contamination levels below 1×10¹⁰ atoms/cm², pushing cleaning technology providers to develop advanced chemistries and processes.

Furthermore, the shift toward EUV lithography introduces new cleaning challenges. The mirrors used in EUV systems degrade with hydrocarbon contamination, creating specialized cleaning requirements that didn’t exist with previous lithography technologies.

MARKET CHALLENGES

High Capital and Operational Costs Present Significant Barriers

Establishing a precision cleaning facility requires substantial upfront investment, with a single advanced cleaning line costing over $5 million to equip. The operational costs are equally demanding, as maintaining ISO Class 1 cleanroom environments consumes significant energy and requires expensive filtration systems. Additionally, the specialized chemistries used for removing atomic-scale contamination can cost over $1,000 per liter, significantly impacting operating margins.

Other Challenges

Skilled Labor Shortage

The precision cleaning process requires technicians with specialized training in semiconductor processes and contamination control. The limited pool of qualified personnel leads to intense competition for talent, with salary costs increasing approximately 8-10% annually in key semiconductor regions.

Regulatory Complexity

Strict environmental regulations governing the use and disposal of cleaning chemicals add compliance costs and operational complexity. Different regions have varying standards for chemical handling, requiring cleaning providers to maintain multiple process flows for global operations.

MARKET RESTRAINTS

Fragmented Cleaning Standards Hinder Market Expansion

The semiconductor industry lacks unified standards for parts cleanliness, with each major manufacturer maintaining proprietary specifications. This fragmentation forces cleaning service providers to develop custom solutions for each client, increasing development costs and limiting economies of scale. The absence of standardized measurement techniques for surface contamination below 10nm further complicates quality assurance processes.

Additionally, the trend toward more complex chamber materials and designs creates technical challenges. New materials like silicon carbide and specialized ceramics require different cleaning approaches than traditional aluminum chambers, necessitating ongoing R&D investments. The semiconductor industry’s continuous process innovations mean cleaning technologies must constantly evolve to keep pace.

MARKET OPPORTUNITIES

Emerging Cleaning Technologies Create New Growth Avenues

The development of novel cleaning methods presents significant opportunities. Cryogenic cleaning, which uses solid CO₂ pellets, is gaining traction for its ability to remove particles without chemical residues. Similarly, plasma-based cleaning systems are being adopted for their superior performance in removing organic contaminants at the atomic scale. These advanced technologies command premium pricing and are expected to grow at nearly double the rate of conventional cleaning methods.

The geographic expansion of semiconductor manufacturing also opens new markets. With major fabs being built in regions previously without significant semiconductor presence, local precision cleaning capacity must be developed. This creates opportunities for both new market entrants and established players expanding their global footprints.

Furthermore, the increasing focus on sustainable manufacturing is driving demand for environmentally friendly cleaning solutions. Processes that reduce chemical usage, water consumption, and energy requirements are gaining preference, allowing providers with green technologies to capture market share.

PRECISION SEMICONDUCTOR EQUIPMENT PARTS CLEANING MARKET TRENDS

Rising Demand for Advanced Node Semiconductor Manufacturing Driving Cleaning Technology Innovations

The global precision semiconductor equipment parts cleaning market is experiencing significant growth due to the increasing demand for high-performance computing (HPC) chips and the transition to sub-7nm process nodes. As semiconductor manufacturers push the boundaries of Moore’s Law, contamination control has become critical with particle tolerances now measured in single-digit nanometers. This has led to the development of atomic-level cleaning technologies capable of removing contamination at the angstrom level. The market is responding with advanced cleaning solutions that combine wet chemical processes with plasma treatment and ultra-pure water rinsing systems, achieving particle removal efficiency exceeding 99.99% for sub-5nm applications.

Other Trends

Transition to Sustainable Cleaning Solutions

Environmental regulations are pushing semiconductor manufacturers to adopt eco-friendly cleaning chemistries that reduce hazardous chemical usage while maintaining cleaning efficacy. This includes the development of water-based cleaning solutions and the implementation of closed-loop recycling systems that recover and reuse cleaning chemicals. The shift is particularly evident in regions with stringent environmental policies, where companies are investing in advanced filtration and waste treatment technologies to meet both cleanliness and sustainability targets simultaneously.

Expansion of Chip Manufacturing Capacity in Asia-Pacific

The Asia-Pacific region, particularly Taiwan, China and South Korea, is seeing massive investments in semiconductor fabrication facilities, creating significant demand for precision cleaning services. Chipmakers are expanding production capacity for advanced logic, memory, and compound semiconductor devices, requiring more sophisticated cleaning solutions to maintain yield rates. This regional expansion is driving the development of localized cleaning service providers and the establishment of on-site cleaning facilities at major foundries to reduce part transportation and turnaround times.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements Drive Market Competition in Semiconductor Parts Cleaning

The global precision semiconductor equipment parts cleaning market features a dynamic competitive landscape with prominent players leveraging cutting-edge cleaning technologies to meet the stringent requirements of advanced semiconductor manufacturing. UCT (Ultra Clean Holdings, Inc.) maintains a leading position due to its comprehensive cleaning solutions and strategic partnerships with major semiconductor manufacturers across North America and Asia.

Kurita (Pentagon Technologies) and Enpro Industries (LeanTeq and NxEdge) also command significant market shares, with their expertise in ultra-clean processing for critical semiconductor components. These companies have strengthened their market position through continuous innovation in contamination control solutions tailored for advanced node manufacturing.

The market is witnessing increasing competition from Asian players such as TOCALO Co., Ltd. and KoMiCo, who are expanding their technological capabilities to cater to the growing demand from foundries and memory manufacturers. Their proximity to major semiconductor hubs in South Korea, Taiwan, and China provides a competitive edge in service responsiveness.

Meanwhile, Mitsubishi Chemical (Cleanpart) and Frontken Corporation Berhad are enhancing their market presence through specialized cleaning technologies for emerging applications like extreme ultraviolet (EUV) lithography components and advanced packaging solutions. Their focus on R&D investments and vertical integration strategies is reshaping service delivery in the industry.

List of Key Precision Semiconductor Equipment Parts Cleaning Companies

- UCT (Ultra Clean Holdings, Inc.) (U.S.)

- Kurita Water Industries Ltd. (Pentagon Technologies) (Japan)

- Enpro Industries (LeanTeq and NxEdge) (U.S.)

- TOCALO Co., Ltd. (Japan)

- Mitsubishi Chemical Group (Cleanpart) (Japan)

- KoMiCo (South Korea)

- Frontken Corporation Berhad (Malaysia)

- Ferrotec (Anhui) Technology Development Co., Ltd (China)

- Shih Her Technology (Taiwan)

Segment Analysis:

By Type

300mm Equipment Parts Drive Market Growth Due to Rising Demand in Advanced Semiconductor Fabrication

The market is segmented based on type into:

- 300mm Equipment Parts

- 200mm Equipment Parts

- 150mm and Others

By Application

Semiconductor Etch Equipment Holds Significant Share Owing to Increased Miniaturization in Chip Manufacturing

The market is segmented based on application into:

- Semiconductor Etch Equipment

- Deposition (CVD, PVD, ALD)

- Ion Implant Equipment

- CMP Equipment

- Diffusion Cleaning

- Lithography Machines

- Others

By Technology

Wet Cleaning Dominates the Market Due to Superior Performance in Particle Removal

The market is segmented based on cleaning technology into:

- Wet Cleaning

- Dry Cleaning

- Cryogenic Cleaning

- Plasma Cleaning

By End-User

Foundries Capture Largest Market Share as Primary Consumers of Precision Cleaning Services

The market is segmented based on end-users into:

- Foundries

- IDMs (Integrated Device Manufacturers)

- OSAT (Outsourced Semiconductor Assembly and Test)

- Research Institutions

Regional Analysis: Precision Semiconductor Equipment Parts Cleaning Market

Asia-Pacific

The Asia-Pacific region dominates the global Precision Semiconductor Equipment Parts Cleaning market, accounting for the largest revenue share due to its concentrated semiconductor manufacturing hubs. Taiwan leads the region, with TSMC as the largest customer for cleaning services, driving demand for advanced process nodes (16nm to 3nm). By 2023, TSMC’s advanced process revenue reached 68% of its total, projected to exceed 75% in 2024. Other key players, such as UMC and Micron, also contribute significantly. This region benefits from high-volume chip production, particularly for applications like AI, data centers, and 5G smartphones. Local suppliers like Shih Her Technology and Frontken (Ares Green Technology Corporation) hold an 82% market share in Taiwan, reflecting a highly consolidated competitive landscape. Growth is further supported by governmental incentives and continuous fab expansions across South Korea, Japan, and Southeast Asia.

North America

North America remains a critical region due to its technological leadership and emphasis on R&D-driven semiconductor production. The U.S. houses key players like UCT (Ultra Clean Holdings, Inc.) and Enpro Industries, which provide precision cleaning solutions for etch and deposition equipment. Demand is bolstered by domestic investments in semiconductor self-sufficiency, such as the CHIPS and Science Act, which allocates $52 billion for fab construction and supply chain resilience. Additionally, stringent EPA and OSHA regulations push for greener cleaning technologies, further refining industry standards. While the region lacks the sheer production volume of Asia-Pacific, its focus on cutting-edge applications (e.g., automotive ICs, AI accelerators) ensures steady market growth, particularly for 300mm wafer equipment cleaning.

Europe

Europe’s market is characterized by specialized demand from automotive and industrial semiconductor manufacturers, with companies like Infineon, STMicroelectronics, and ASML driving cleaning service adoption. The region emphasizes environmentally sustainable practices, aligning with EU REACH and circular economy initiatives, which encourage water-based and low-chemical cleaning methods. However, Europe faces challenges due to limited local semiconductor production capacity compared to Asia, relying heavily on imports for advanced nodes. Collaborations between academia and industry, such as the European Chips Act, aim to bolster domestic capabilities, presenting long-term opportunities for precision cleaning providers. Key players like Cinos and TOCALO Co., Ltd. cater to niche applications in lithography and ion implant equipment.

Middle East & Africa

This region represents an emerging market, with potential growth tied to strategic investments in tech infrastructure. Nations like the UAE and Israel are fostering semiconductor ecosystems through partnerships with global foundries, though demand for precision cleaning remains nascent. High costs and limited local expertise hinder rapid adoption, but increasing focus on IoT and smart city projects could drive future opportunities. Providers such as Ferrotec and Persys Group are expanding their footprint here, targeting desert-environment-compatible cleaning solutions to address dust and contamination challenges unique to the region.

South America

South America’s market is modest but growing, primarily serving consumer electronics and automotive sectors in Brazil and Argentina. Economic instability and lack of localized semiconductor fabs limit scalability, though regional players like HCUT Co., Ltd. are exploring partnerships to modernize legacy equipment cleaning. The absence of strict regulatory frameworks slows the shift to advanced cleaning technologies, but incremental demand from telecom and industrial automation could gradually uplift the market.

Report Scope

This market research report provides a comprehensive analysis of the global Precision Semiconductor Equipment Parts Cleaning market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Precision Semiconductor Equipment Parts Cleaning market was valued at USD 869 million in 2024 and is projected to reach USD 1427 million by 2032, growing at a CAGR of 7.5% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (300mm Equipment Parts, 200mm Equipment Parts, 150mm and Others), application (Semiconductor Etch Equipment, Deposition, Ion Implant Equipment, CMP Equipment, etc.), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the market, with Taiwan accounting for significant demand due to major semiconductor manufacturers like TSMC, UMC, and Micron.

- Competitive Landscape: Profiles of leading market participants including UCT (Ultra Clean Holdings, Inc), Kurita (Pentagon Technologies), Enpro Industries (LeanTeq and NxEdge), TOCALO Co., Ltd., and Mitsubishi Chemical (Cleanpart), covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging cleaning technologies, integration of AI/automation, and evolving industry standards for ultra-clean semiconductor parts.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing semiconductor manufacturing, demand for advanced nodes) along with challenges (high cleaning standards requirements, supply chain constraints).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Precision Semiconductor Equipment Parts Cleaning Market?

->Precision Semiconductor Equipment Parts Cleaning Market was valued at 869 million in 2024 and is projected to reach US$ 1427 million by 2032, at a CAGR of 7.5% during the forecast period.

Which key companies operate in Global Precision Semiconductor Equipment Parts Cleaning Market?

-> Key players include UCT (Ultra Clean Holdings, Inc), Kurita (Pentagon Technologies), Enpro Industries (LeanTeq and NxEdge), TOCALO Co., Ltd., Mitsubishi Chemical (Cleanpart), KoMiCo, and Frontken Corporation Berhad, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor manufacturing, demand for advanced process nodes (especially below 7nm), and the need for higher cleaning standards in semiconductor fabrication.

Which region dominates the market?

-> Asia-Pacific dominates the market, with Taiwan being a key hub due to major semiconductor manufacturers like TSMC. The top six players in Taiwan accounted for approximately 82% market share in 2023.

What are the emerging trends?

-> Emerging trends include adoption of AI-powered cleaning validation, development of atomic-level cleaning technologies, and increasing focus on sustainable cleaning solutions in semiconductor manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...